Reports

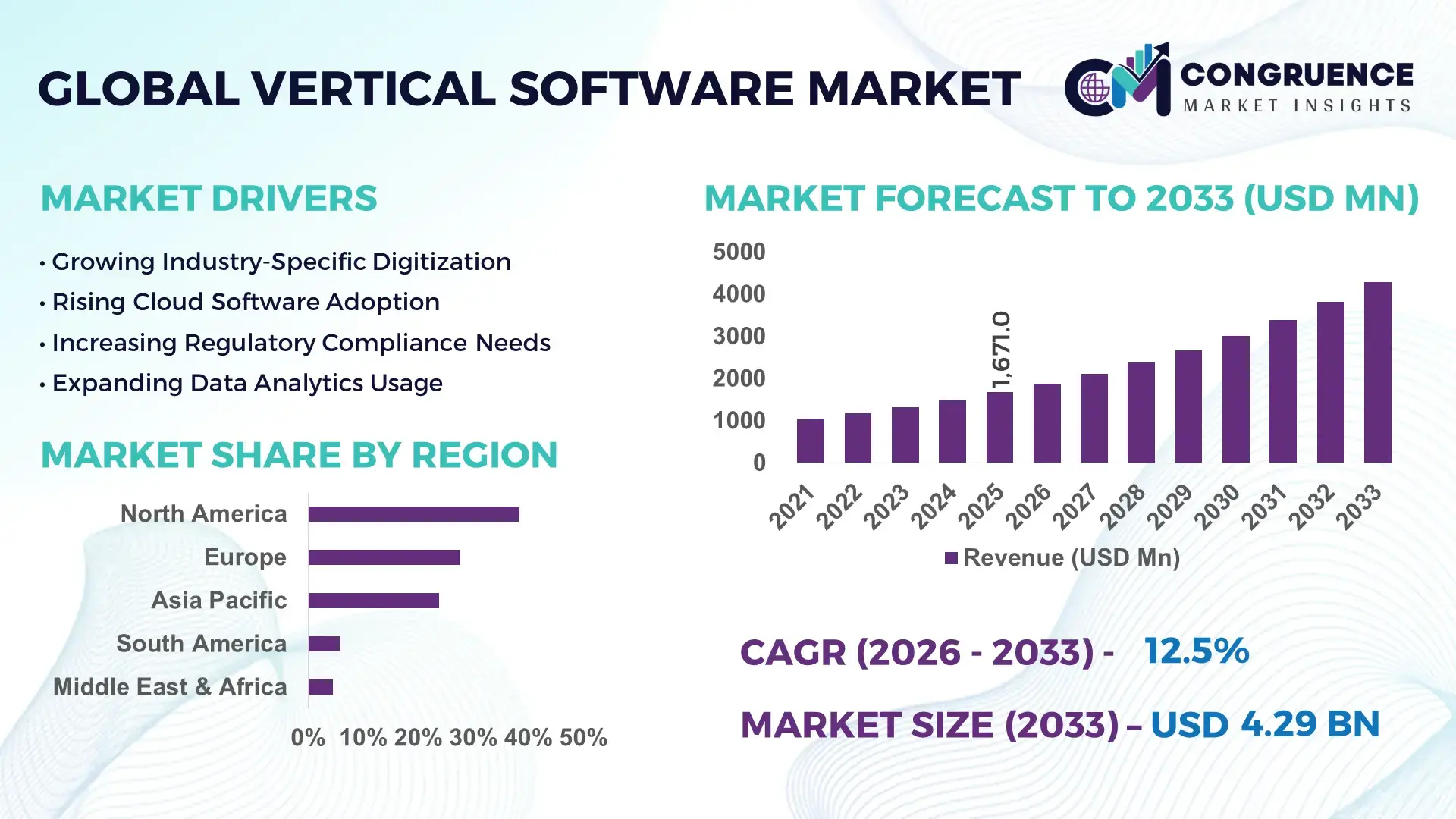

The Global Vertical Software Market was valued at USD 1,671.0 Million in 2025 and is anticipated to reach a value of USD 4,287.4 Million by 2033 expanding at a CAGR of 12.5% between 2026 and 2033. Growth is being accelerated by industry-specific cloud platforms, AI-driven workflow automation, and rising regulatory compliance requirements across healthcare, financial services, manufacturing, and public-sector operations.

The United States dominates the market with an estimated 34% share, supported by over 92% enterprise cloud adoption, more than USD 80 billion in annual software investment activity, and strong deployment across healthcare, financial services, and industrial operations. Compared with Germany, where Industry 4.0 initiatives drive manufacturing-focused deployments, U.S. organizations demonstrate broader cross-sector software penetration. The continued expansion of digital compliance frameworks following evolving cybersecurity regulations further reinforces enterprise spending priorities.

Organizations that align vertical software investments with industry-specific automation, compliance, and data intelligence capabilities are strengthening operational resilience and long-term competitive positioning.

Market Size & Growth: USD 1,671.0 Million in 2025, reaching USD 4,287.4 Million by 2033 at 12.5% CAGR, driven by AI-enabled industry-specific workflow automation and compliance modernization.

Top Growth Drivers: Cloud-native deployment adoption exceeds 68%, AI-assisted workflow utilization surpasses 41%, and regulatory technology spending has increased by 29%.

Short-Term Forecast: By 2028, automated workflow deployment is expected to reduce administrative processing costs by 22% while improving operational efficiency by 31%.

Emerging Technologies: Generative AI, predictive analytics, and low-code automation platforms are accelerating software configuration and reducing deployment timelines by up to 35%.

Regional Leaders: North America (USD 1.6 Billion), Europe (USD 1.1 Billion), and Asia-Pacific (USD 0.9 Billion) lead adoption through cloud transformation, industrial digitization, and smart enterprise initiatives.

Consumer/End-User Trends: More than 74% of enterprises prioritize industry-specific platforms over generic ERP systems to improve process accuracy and compliance visibility.

Pilot/Case Example: In 2025, a healthcare software deployment program improved patient workflow efficiency by 28% and reduced reporting delays by 19%.

Competitive Landscape: Top providers collectively control approximately 42% market share, led by Oracle, Microsoft, SAP, Salesforce, and Guidewire.

Regulatory & ESG Impact: Automated compliance platforms have reduced audit preparation time by 30% while strengthening data governance and reporting transparency.

Investment & Funding: Annual enterprise software investment exceeds USD 80 Billion, supported by strategic partnerships, cloud migration programs, and industry-focused platform expansion.

Innovation & Future Outlook: AI copilots, embedded analytics, and vertical SaaS ecosystems are becoming core differentiators as companies pursue outcome-driven digital transformation.

Vertical Software Market demand is expanding rapidly across healthcare, banking, insurance, manufacturing, construction, and public administration environments where specialized functionality delivers measurable operational value. Recent innovations include AI copilots, predictive analytics engines, and industry-specific compliance automation modules. More than 60% of enterprise software buyers now prioritize sector-focused platforms over generic solutions. Growing cybersecurity mandates and evolving digital governance frameworks are further shaping procurement strategies, creating a foundation for deeper strategic market evaluation.

Vertical software is becoming a strategic pillar of enterprise competitiveness because organizations increasingly require industry-specific functionality that generic platforms cannot efficiently deliver. Financial institutions, healthcare providers, manufacturers, and logistics operators are prioritizing specialized software environments to address regulatory complexity, operational visibility, and process automation requirements. The ongoing modernization of digital infrastructure and tightening cybersecurity regulations are reinforcing investment priorities across mission-critical business applications.

Modern vertical software platforms deliver measurable advantages over legacy systems. AI-enabled workflow engines can reduce manual processing requirements by 25–40% while improving operational accuracy by more than 30% through automated decision support and real-time analytics. The United States leads in large-scale enterprise deployments, while Germany and Japan demonstrate stronger adoption in manufacturing-focused digital transformation initiatives. Over the next two to three years, embedded analytics, workflow orchestration, and cloud-native architectures are expected to become standard procurement criteria across regulated industries.

Organizations are increasingly deploying vertical platforms through ecosystem partnerships, cloud migration programs, and industry-focused integration strategies. For example, healthcare providers are integrating patient management, compliance reporting, and predictive resource planning into unified environments. Companies that establish specialized software ecosystems today are positioning themselves to achieve stronger operational control, faster decision-making, and sustainable competitive differentiation.

Enterprise demand is increasingly shifting toward software platforms designed for sector-specific operational requirements. More than 70% of large organizations now prioritize industry-focused applications over generalized software suites due to superior workflow alignment and regulatory support. AI-enabled automation is reducing administrative workloads by approximately 30%, while cloud deployment adoption has exceeded 68% across key industries. The expansion of cybersecurity regulations in the United States and Europe has further increased demand for integrated compliance management capabilities. In response, software vendors are expanding vertical SaaS portfolios, investing in AI functionality, and forming strategic partnerships with industry specialists. A key operational insight is that organizations adopting purpose-built software often achieve faster implementation cycles and higher user adoption rates than enterprises relying on heavily customized horizontal platforms.

Interoperability limitations remain a significant structural constraint for software deployment programs. Nearly 45% of enterprises continue operating legacy infrastructure that lacks compatibility with modern cloud-native architectures, creating integration delays and elevated implementation costs. Data migration projects frequently account for 20–30% of total deployment expenditures, particularly in healthcare and financial services environments. Regulatory requirements regarding data residency and cross-border information management add further complexity in countries such as Germany and India. To mitigate these constraints, vendors are expanding API frameworks, investing in interoperability standards, and localizing deployment capabilities. A critical operational challenge is that fragmented technology ecosystems often extend implementation timelines, delaying the realization of productivity and compliance benefits.

The convergence of artificial intelligence, predictive analytics, and industry-specific datasets is creating substantial opportunities for software providers. More than 55% of enterprises are actively evaluating AI-powered decision-support capabilities, while automated analytics tools have demonstrated efficiency improvements exceeding 25% in several operational environments. India's digital public infrastructure expansion and Southeast Asia's accelerating enterprise digitization initiatives are creating attractive deployment opportunities. Emerging technologies such as industry-trained AI models and autonomous workflow orchestration are enabling higher-value software outcomes beyond traditional process management. Companies are increasing R&D investments, establishing ecosystem partnerships, and expanding localized cloud infrastructure to capture this demand. A notable strategic opportunity lies in embedding intelligence directly into operational workflows rather than offering analytics as a standalone function.

As software platforms become increasingly interconnected, cybersecurity and governance requirements are emerging as critical long-term challenges. Enterprise software attacks have increased by more than 20% in recent years, while organizations now manage substantially larger volumes of regulated operational data. Approximately 58% of enterprises identify cybersecurity readiness as a major consideration when selecting software vendors. The growing adoption of AI-powered applications further intensifies governance requirements surrounding model transparency, data quality, and regulatory compliance. Software providers are responding through enhanced security architectures, zero-trust frameworks, and expanded investment in threat monitoring capabilities. The most significant strategic challenge is maintaining scalable innovation while ensuring security, compliance, and operational consistency across increasingly complex digital ecosystems.

AI-Native Workflow Orchestration Enterprise software deployments are rapidly shifting from rule-based automation to AI-native workflow orchestration. More than 58% of large enterprises have integrated AI assistants into industry-specific applications, while automated task routing has reduced processing times by nearly 35% and improved workflow accuracy by over 25%. Labor shortages in healthcare and financial services are accelerating adoption. Vendors are embedding predictive decision engines directly into operational platforms and expanding strategic AI partnerships to improve productivity without increasing workforce requirements.

Industry Cloud Consolidation Strategies Organizations are replacing fragmented software stacks with unified vertical cloud ecosystems. Nearly 64% of enterprises now prioritize integrated industry platforms, reducing application sprawl by approximately 28% and lowering software administration workloads by 22%. Regulatory reporting requirements and cybersecurity governance pressures are driving consolidation efforts. Companies are responding through platform acquisitions, ecosystem integration programs, and standardized deployment frameworks that improve visibility across business-critical processes while simplifying compliance management.

Embedded Compliance Intelligence Expansion Compliance functionality is evolving from standalone modules into embedded operational capabilities. Automated regulatory monitoring adoption has increased by 41%, while compliance-related manual reporting workloads have declined by almost 30%. New cybersecurity disclosure requirements and expanding data governance obligations are influencing software design priorities. Providers are integrating real-time audit trails, policy engines, and automated documentation tools, enabling organizations to reduce operational risk while maintaining deployment speed across highly regulated industries.

Vertical Data Ecosystem Development Enterprises are increasingly treating proprietary industry datasets as strategic assets rather than operational byproducts. More than 52% of software buyers now evaluate data integration capabilities before platform selection, while connected ecosystem deployments have improved cross-functional visibility by nearly 27%. A less obvious shift is the growing use of sector-specific data exchanges between suppliers, customers, and regulators. Software vendors are expanding interoperability partnerships and industry data networks to strengthen customer retention and create higher-value operational intelligence environments.

Cloud-Based Vertical Software remains the leading segment, accounting for an estimated 61% of deployments due to superior scalability, faster implementation cycles, and lower infrastructure management requirements. Enterprises increasingly favor cloud environments because deployment timelines are typically 30–40% shorter than traditional on-premise implementations. The segment also benefits from continuous software updates, integrated cybersecurity controls, and easier interoperability with analytics and automation tools. Vendors are prioritizing multi-tenant architectures, subscription-based delivery models, and industry-specific cloud suites to strengthen adoption across healthcare, financial services, and manufacturing operations. On-Premise Vertical Software represents the fastest-evolving segment within highly regulated industries where data sovereignty and operational control remain critical. Although mature sectors continue relying on established infrastructure, hybrid deployment models have expanded by nearly 24% as organizations seek greater flexibility. Large manufacturers, government agencies, and critical infrastructure operators are modernizing legacy environments through selective cloud integration rather than full migration. Software providers are responding through hybrid architecture development, enhanced API connectivity, and industry-focused deployment services. This shift reflects changing investment priorities toward deployment flexibility, cybersecurity resilience, and long-term operational continuity.

Operational Process Management is the leading application segment due to its direct impact on workflow efficiency, compliance management, and resource utilization. Nearly 67% of enterprises prioritize process-centric software investments to reduce manual intervention and improve operational visibility. Industry-specific workflow automation has reduced administrative processing requirements by approximately 28% across healthcare, insurance, and manufacturing environments. Organizations continue integrating operational management platforms with analytics, compliance monitoring, and enterprise resource planning systems to improve execution consistency and decision quality. Predictive Analytics and Decision Support is the fastest-growing application area as enterprises increasingly seek real-time operational intelligence. Adoption of predictive modules has increased by more than 38% in the past two years, particularly among financial institutions and logistics operators managing complex operational environments. Customer Management, Compliance Management, and Asset Optimization applications continue expanding as organizations pursue broader digital transformation objectives. Vendors are enhancing platform functionality through embedded AI, automated reporting, and intelligent recommendations. Demand is increasingly shifting toward applications capable of delivering measurable operational outcomes rather than basic transaction processing, creating stronger differentiation opportunities for software providers.

Large Enterprises represent the dominant end-user segment, accounting for approximately 63% of overall deployments due to extensive operational complexity, regulatory obligations, and multi-location business structures. These organizations typically manage larger software ecosystems and require advanced customization, integration, and governance capabilities. More than 70% of large enterprises have expanded investments in industry-specific platforms to streamline workflows, strengthen compliance oversight, and improve operational visibility. Software vendors continue targeting this segment through enterprise-scale deployment frameworks, strategic consulting services, and long-term ecosystem partnerships. Small and Medium Enterprises (SMEs) are emerging as the fastest-growing end-user group as cloud delivery models reduce implementation barriers and upfront infrastructure requirements. Adoption among SMEs has increased by nearly 32%, supported by subscription-based pricing structures and simplified deployment options. While large enterprises prioritize integration depth and operational control, SMEs increasingly focus on automation, workforce efficiency, and rapid implementation. Vendors are responding through modular product offerings, industry-specific templates, and channel partner expansion strategies. Competitive positioning is gradually shifting toward solutions that balance advanced functionality with deployment simplicity, creating new opportunities across underserved business segments.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.2% between 2026 and 2033.

North America maintains its leadership position through high enterprise software spending, mature cloud infrastructure, and strong adoption of industry-specific digital platforms. The region represents approximately 38.4% of global market activity, supported by widespread deployment across healthcare, financial services, insurance, logistics, and government sectors. More than 72% of large enterprises have integrated industry-specific cloud applications into core operational workflows. Organizations are increasingly replacing fragmented software environments with unified vertical platforms that improve compliance management and operational visibility. Recent strategic partnerships between cloud providers and software vendors have accelerated deployment efficiency, reducing implementation timelines by nearly 25% for enterprise-scale projects.

United States Market Outlook: The United States serves as the primary innovation and deployment hub for vertical software solutions due to its advanced enterprise technology ecosystem and strong software investment culture. More than 90% of large enterprises utilize cloud-based business applications, while healthcare, financial services, and insurance sectors continue expanding software modernization programs. Regulatory requirements related to cybersecurity, data governance, and operational transparency are increasing demand for specialized software capabilities. Leading technology providers continue expanding AI-enabled workflow automation and industry-specific analytics, reinforcing the country's position as the largest contributor to enterprise software transformation initiatives.

Europe remains a strategically important market driven by industrial digitization, regulatory compliance requirements, and enterprise modernization initiatives. The region accounts for approximately 27.6% of global demand, supported by strong deployment activity across manufacturing, healthcare, banking, and public-sector organizations. Data governance frameworks and cybersecurity regulations continue influencing procurement decisions, encouraging adoption of industry-specific platforms with embedded compliance capabilities. Enterprise software modernization programs have increased by nearly 29% across key industrial economies. Organizations are prioritizing operational transparency, process standardization, and digital resilience, while software vendors expand localized deployment capabilities and industry-focused service offerings.

Germany Market Outlook: Germany represents the region's most influential market due to its industrial strength, advanced manufacturing ecosystem, and leadership in Industry 4.0 initiatives. More than 60% of large manufacturing organizations have expanded investments in specialized operational software to support smart factory programs and predictive maintenance strategies. Strong integration between industrial automation systems and vertical software platforms is improving production visibility and operational efficiency. The country's emphasis on engineering excellence, cybersecurity standards, and industrial digitization continues creating favorable conditions for advanced software deployment across mission-critical business environments.

Asia-Pacific is emerging as the fastest-expanding regional market due to accelerating enterprise digitization, cloud adoption, and industrial modernization efforts. The region contributes approximately 23.8% of global market activity and continues gaining momentum through technology investments across manufacturing, retail, banking, healthcare, and telecommunications sectors. Enterprise cloud adoption has increased by more than 35% in several major economies, creating strong demand for industry-specific software platforms. Governments and private-sector organizations are investing heavily in digital infrastructure, while software vendors expand local data centers, implementation networks, and ecosystem partnerships to support large-scale deployment requirements.

China Market Outlook: China remains the region's largest market due to its extensive industrial base, expanding digital economy, and strong government support for enterprise modernization. Large manufacturers increasingly deploy vertical software platforms to improve supply-chain visibility, production planning, and quality management. More than 65% of major industrial enterprises have accelerated smart manufacturing initiatives involving specialized operational software. Rapid expansion of cloud infrastructure and enterprise AI adoption continues strengthening software deployment activity across manufacturing, logistics, healthcare, and financial services environments, positioning China as a major center for digital industrial transformation.

South America is experiencing steady software adoption driven by digital transformation initiatives across financial services, retail, logistics, and public administration sectors. The region represents approximately 5.7% of global market demand and benefits from increasing enterprise migration toward cloud-based operational platforms. Organizations are modernizing legacy systems to improve efficiency, regulatory reporting, and customer engagement capabilities. Software deployment activity has increased by nearly 21% among mid-sized enterprises seeking scalable technology environments. Infrastructure limitations and integration challenges remain considerations; however, ongoing investment in cloud connectivity and digital services continues improving deployment readiness across major economies.

Brazil Market Outlook: Brazil serves as the largest software market in South America due to its extensive enterprise base, growing financial technology ecosystem, and expanding cloud infrastructure investments. Banking institutions, healthcare providers, and retail organizations are actively deploying industry-specific software to enhance operational control and customer service performance. Enterprise cloud utilization has surpassed 55% among large organizations, supporting broader adoption of specialized software platforms. Regulatory modernization and digital service expansion initiatives are also encouraging organizations to invest in advanced workflow automation and compliance-focused technology solutions.

The Middle East & Africa market is advancing through national digital transformation programs, cloud infrastructure expansion, and modernization of government and enterprise operations. The region accounts for approximately 4.5% of global market activity and is witnessing increased deployment across energy, healthcare, banking, and public-sector organizations. Large-scale smart city projects and digital government initiatives are generating demand for industry-specific software capabilities. Enterprise cloud adoption has increased by nearly 26% over recent years, supported by investments in regional data centers and technology partnerships. Organizations are prioritizing operational efficiency, compliance modernization, and service delivery improvements through specialized software deployments.

Saudi Arabia Market Outlook: Saudi Arabia has emerged as the region's most strategically significant market due to substantial investments in digital infrastructure, smart city development, and economic diversification programs. Public-sector agencies and large enterprises are accelerating software modernization initiatives to support operational efficiency and digital governance objectives. Enterprise technology adoption continues expanding across healthcare, energy, financial services, and logistics sectors. More than 70% of major digital transformation projects now incorporate cloud-based operational platforms, strengthening demand for specialized software solutions aligned with national modernization priorities and long-term infrastructure development goals.

The Vertical Software Market is characterized by competition between global enterprise software leaders such as Oracle, Microsoft, SAP, Salesforce, and Guidewire, alongside specialized vertical-focused vendors targeting healthcare, insurance, manufacturing, and financial services. The top five players collectively control approximately 42% of market activity, creating a moderately concentrated competitive structure. Competition is increasingly centered on AI integration, cloud-native architecture, industry-specific functionality, and deployment speed rather than pricing alone. Enterprises adopting AI-enabled workflow platforms report implementation efficiency improvements of 25–35%, while integrated cloud ecosystems reduce administrative workloads by nearly 22%. Vendors are responding through ecosystem partnerships, vertical acquisitions, and embedded analytics innovation. Guidewire continues expanding insurance-focused cloud integrations, while Microsoft and Oracle are accelerating industry-specific AI capabilities. The current competitive shift favors specialized platforms with strong data intelligence and compliance automation capabilities. High switching costs, integration complexity, and regulatory requirements remain major entry barriers. Winning requires deep industry expertise, scalable cloud infrastructure, AI-driven operational outcomes, and strong partner ecosystems.

Microsoft Corporation

SAP SE

Salesforce Inc.

Guidewire Software Inc.

Infor Inc.

Epic Systems Corporation

Blackbaud Inc.

Tyler Technologies Inc.

Veeva Systems Inc.

Bentley Systems Inc.

Procore Technologies Inc.

Temenos AG

nCino Inc.

Current technology development is centered on AI-enabled workflow orchestration, cloud-native industry platforms, and embedded analytics. More than 58% of enterprise software buyers now prioritize AI-enhanced functionality during procurement evaluations. Automated workflow engines are reducing manual processing workloads by approximately 30%, while embedded analytics improve operational decision speed by nearly 25%. Organizations increasingly integrate vertical software with ERP, CRM, cybersecurity, and compliance systems to create unified operational environments.

Emerging technologies include industry-trained AI models, low-code configuration platforms, and intelligent process automation. Compared with legacy rule-based systems, AI-driven vertical platforms deliver 35–40% faster process execution and significantly improve exception handling capabilities. Adoption of low-code deployment frameworks has exceeded 45% among large enterprises seeking faster customization and reduced implementation complexity. Industry leaders benefit most because proprietary datasets enhance model accuracy and strengthen competitive differentiation.

Disruptive innovation is increasingly focused on autonomous software agents, predictive intelligence, and sector-specific digital ecosystems. Between 2026 and 2028, organizations are expected to accelerate deployment of AI copilots capable of automating complex operational workflows across healthcare, insurance, and manufacturing environments. Companies investing early in intelligent automation, industry data platforms, and interoperable cloud architectures will secure stronger operational agility, lower process costs, and higher customer retention as software competition shifts from functionality toward outcome-based performance.

November 2024 – Microsoft Corporation introduced adapted AI models specifically designed for industries including manufacturing, healthcare, and financial services through Microsoft Cloud. The initiative expanded industry-specific AI deployment capabilities and improved use-case precision through specialized training models. Business impact: accelerated sector-focused AI adoption and workflow optimization. Source: www.blogs.microsoft.com

January 2025 – Guidewire Software announced its PartnerConnect ecosystem surpassed 110 cloud-native integrations, strengthening interoperability across insurance technology environments. The expansion enables insurers to accelerate deployment and improve operational flexibility. Business impact: broader ecosystem value and faster customer modernization initiatives.

June 2025 – Guidewire Software and Docusign launched integrated solutions for PolicyCenter and ClaimCenter, enabling insurers to achieve more than 80% straight-through processing for e-signature workflows. Business impact: reduced manual effort, faster claims processing, and improved customer experience.

June 2026 – Oracle Corporation secured a U.S. federal government contract to deploy a unified cloud-based HR platform replacing multiple agency systems. The modernization initiative supports government-wide operational standardization and technology consolidation. Business impact: strengthened Oracle’s position in large-scale public-sector vertical software deployments.

The report provides comprehensive analysis of industry-specific software platforms across deployment types, operational applications, and end-user categories. Coverage includes cloud-based and on-premise software environments, alongside key applications such as process management, compliance management, predictive analytics, customer engagement, and operational intelligence. The study evaluates adoption patterns across large enterprises and SMEs while examining deployment trends, integration strategies, and industry-specific digital transformation priorities.

Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level evaluation of technology adoption, infrastructure readiness, and enterprise modernization activity. More than 60% of current enterprise demand is concentrated within regulated industries requiring advanced compliance and workflow automation capabilities. The report further examines AI-enabled automation, embedded analytics, low-code development, cloud ecosystems, and emerging intelligent software architectures. Strategic insights support investment planning, product expansion, competitive benchmarking, partnership development, and long-term market positioning across the 2026–2033 outlook period.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,671.0 Million |

| Market Revenue (2033) | USD 4,287.4 Million |

| CAGR (2026–2033) | 12.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Oracle Corporation; Microsoft Corporation; SAP SE; Salesforce Inc.; Guidewire Software Inc.; Infor Inc.; Epic Systems Corporation; Blackbaud Inc.; Tyler Technologies Inc.; Veeva Systems Inc.; Bentley Systems Inc.; Procore Technologies Inc.; Temenos AG; nCino Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |