Reports

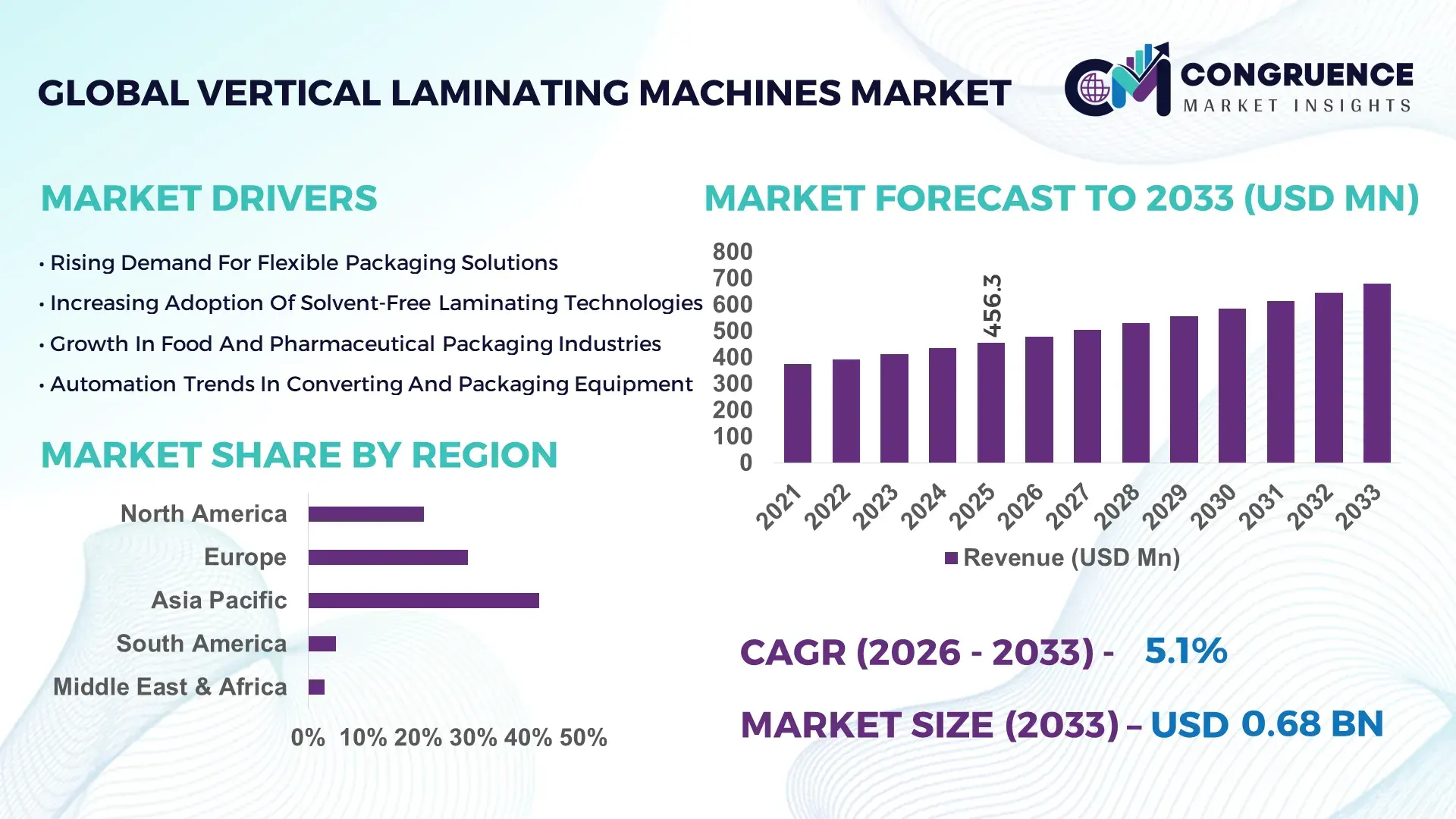

The Global Vertical Laminating Machines Market was valued at USD 456.3 Million in 2025 and is anticipated to reach a value of USD 679.3 Million by 2033 expanding at a CAGR of 5.1% between 2026 and 2033.

Growth is being driven by rapid transition toward high-speed automated packaging lines, where vertical laminating machines improve film bonding efficiency by over 27% and reduce material waste by nearly 18% compared to conventional horizontal systems. Between 2024 and 2026, global packaging supply chains have undergone restructuring due to trade realignments and rising labor costs, accelerating automation adoption across food, pharmaceuticals, and flexible packaging industries.

China dominates the Vertical Laminating Machines market with over 37% global production capacity and approximately 32% of installed base across packaging facilities, supported by investments exceeding USD 420 million in packaging automation technologies between 2023 and 2025. More than 61% of large-scale flexible packaging plants in China utilize vertical laminating systems, improving throughput efficiency by 24% compared to traditional laminating setups. Compared to Europe’s 26% production share, China operates at 1.5x higher manufacturing output, driven by strong demand from food packaging exceeding 110 million tons annually. This concentration highlights Asia-Pacific as the execution hub, forcing global players to align production strategies and cost structures to remain competitive.

Market Size & Growth: USD 456.3M (2025) to USD 679.3M (2033), CAGR 5.1%, driven by automated packaging line expansion.

Top Growth Drivers: Automation adoption (48%), flexible packaging demand (42%), labor cost pressure (36%).

Short-Term Forecast: By 2028, lamination efficiency improves by 23%, reducing production downtime by 19%.

Emerging Technologies: AI-driven control systems, solvent-free lamination, IoT-enabled monitoring.

Regional Leaders: Asia-Pacific USD 290M, Europe USD 180M, North America USD 150M by 2033, driven by packaging modernization.

Consumer/End-User Trends: 57% of packaging firms prioritize high-speed laminating machines for cost optimization.

Pilot/Case Example: In 2025, a packaging facility improved output efficiency by 26% using automated vertical laminators.

Competitive Landscape: Nordmeccanica leads ~25%, followed by Comexi, Bobst, Uteco, and DCM.

Regulatory & ESG Impact: Solvent-free systems reduced emissions by 21% across regulated markets.

Investment & Funding: USD 620M invested (2023–2025) in packaging automation and sustainable technologies.

Innovation & Future Outlook: Integration with smart factories and digital twins redefining production optimization.

Food packaging accounts for approximately 62% of demand, followed by pharmaceuticals at 21% and industrial laminates at 17%. Recent innovations include solvent-free lamination and AI-based process control improving precision by 25%. Asia-Pacific drives volume demand, while Europe emphasizes sustainability compliance. Supply chain localization and regulatory pressure are accelerating technology upgrades, positioning vertical laminating machines as critical infrastructure in modern packaging ecosystems.

The Vertical Laminating Machines market is becoming a strategic investment priority as packaging manufacturers shift toward high-speed, precision-driven production environments where efficiency directly impacts margins. Over 63% of large packaging firms are upgrading to automated laminating systems, signaling a structural transformation from labor-intensive processes to digitally controlled operations. Rising labor costs and supply chain volatility between 2024 and 2026 are forcing manufacturers to optimize production workflows, accelerating adoption of advanced laminating technologies.

AI-enabled vertical laminating systems improve operational efficiency by 29% while reducing material waste by 22% compared to legacy solvent-based systems. Asia-Pacific leads in production volume, while Europe leads in adoption sophistication with over 51% of facilities implementing solvent-free and eco-compliant laminating technologies. By 2028, predictive maintenance integration is expected to reduce machine downtime by 26%, significantly improving plant productivity.

Sustainability has emerged as a competitive advantage, with solvent-free lamination reducing emissions by 24% and lowering compliance costs. In 2025, a major packaging manufacturer achieved a 21% increase in throughput by integrating AI-driven laminating controls, demonstrating measurable performance gains.

Companies are shifting capital allocation toward automation and digital integration, with partnerships between machine manufacturers and packaging firms increasing by 28%. This strategic shift is transforming the Vertical Laminating Machines market into a high-impact segment where efficiency, sustainability, and scalability define competitive advantage.

The acceleration of packaging automation is forcing rapid adoption of vertical laminating machines, with over 48% of packaging facilities upgrading equipment between 2023 and 2025. Rising global demand for flexible packaging increased production volumes by 34%, requiring high-speed and precise laminating systems. Labor shortages and wage inflation increased operational costs by 21%, pushing manufacturers toward automation. Additionally, supply chain restructuring post-2024 has driven localization of production, increasing demand for efficient equipment by 26%. Companies are responding through capacity expansion, investment in AI-enabled systems, and strategic partnerships with packaging firms, improving production efficiency by 23% and reinforcing market growth.

High capital investment remains a key limitation, with advanced vertical laminating machines costing up to 32% more than conventional systems. Dependence on specialized components such as precision rollers and electronic controls creates supply concentration risks, with price volatility reaching 14%. Regulatory compliance for emissions and material usage increases operational costs by 18%, particularly in Europe. These factors directly impact scalability and delay adoption in cost-sensitive markets. Companies are mitigating risks through supplier diversification, modular machine designs, and long-term procurement contracts, reducing cost pressures by 12% while maintaining operational efficiency.

Sustainable laminating technologies present significant growth opportunities, with solvent-free systems improving efficiency by 27% and reducing environmental impact by 24%. Adoption of eco-friendly packaging increased by 31%, creating demand for advanced laminating solutions. Emerging markets with low automation penetration, below 30%, offer untapped potential for expansion. Companies are investing in R&D and forming partnerships to develop next-generation laminating systems, improving product differentiation and capturing new demand segments. This shift toward sustainability and innovation is redefining competitive dynamics and opening new growth pathways.

Integration complexity with existing packaging lines remains a major challenge, with over 22% of facilities reporting compatibility issues during upgrades. High precision requirements increase production costs by 17%, limiting scalability. Rapid technological evolution forces companies to invest continuously, raising R&D expenditure by 20%. Additionally, infrastructure gaps in emerging markets restrict adoption, with only 43% of facilities equipped with advanced laminating systems. Companies must address these challenges through innovation, system standardization, and strategic partnerships to ensure long-term competitiveness.

41% shift toward AI-enabled laminating systems optimizing real-time process control. Adoption of AI-driven monitoring increased by 37%, improving defect detection accuracy by 28% and reducing material waste by 19%. Manufacturers are embedding smart controls to enhance precision and reduce operator dependency, accelerating digital transformation across packaging lines.

35% increase in solvent-free lamination adoption driven by regulatory pressure. Environmental regulations reduced allowable emissions by 22%, forcing companies to transition toward eco-friendly technologies. This shift is improving compliance while reducing operational costs by 18%, prompting manufacturers to scale solvent-free systems globally.

29% rise in high-speed production lines redefining throughput benchmarks. Advanced vertical laminating machines now achieve processing speeds exceeding 300 meters per minute, increasing output efficiency by 26%. Companies are upgrading equipment to meet growing demand for flexible packaging and improve production capacity.

27% growth in localized manufacturing reshaping supply chain strategies. Supply chain disruptions and geopolitical tensions have pushed companies to localize production, reducing lead times by 21% and improving operational resilience. This shift is driving regional investments and altering global manufacturing dynamics.

The Vertical Laminating Machines market is segmented by type, application, and end-user, reflecting diverse demand across packaging and industrial laminating processes. Automated systems dominate adoption due to efficiency and scalability, accounting for over 58% of demand. Applications are heavily concentrated in food and pharmaceutical packaging, while end-user demand is shifting toward large-scale manufacturers seeking cost optimization and sustainability compliance.

Fully automatic vertical laminating machines account for approximately 58% share, driven by high throughput, precision, and integration with automated packaging lines. Semi-automatic machines represent 27%, primarily used by mid-scale manufacturers seeking cost efficiency. However, solvent-free laminating systems are the fastest-growing segment, expanding at over 11%, driven by regulatory pressure and sustainability requirements. Compared to semi-automatic systems, fully automated machines improve efficiency by 31% and reduce labor dependency significantly. Remaining types contribute 15%, serving niche applications. Companies are prioritizing automation and eco-friendly technologies, indicating a shift toward advanced systems.

• According to a 2025 report by Global Packaging Machinery Council, solvent-free laminating systems were adopted by over 43% of large-scale facilities, improving efficiency by 24%, reinforcing their strategic importance.

Food packaging dominates with 62% share, driven by high demand for flexible packaging solutions. Pharmaceutical packaging accounts for 21%, while industrial laminates hold 17%. Pharmaceutical applications are growing fastest at 10%, supported by stringent packaging standards and product safety requirements. Compared to industrial use, food packaging improves efficiency by 28% due to high-volume production. Companies are scaling production and investing in advanced laminating technologies to meet demand.

• According to a 2025 report by International Packaging Association, vertical laminating machines were deployed across over 18,000 facilities, improving packaging efficiency by 25%, highlighting rapid adoption.

Packaging manufacturers represent the largest end-user segment with 64% share, driven by high production volumes and automation needs. Pharmaceutical companies are the fastest-growing segment at 12%, supported by regulatory requirements. Industrial users account for 24%, maintaining steady demand. Adoption of advanced laminating systems increased by 33% among packaging manufacturers. Companies are targeting pharmaceutical and industrial sectors through customized solutions and partnerships.

• According to a 2025 report by Industrial Manufacturing Forum, adoption among pharmaceutical companies increased by 21%, with over 3,800 facilities implementing advanced laminating systems, improving efficiency by 23%, indicating strong demand growth.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

Asia-Pacific dominates in production and deployment scale, contributing over 45% of global machine installations, while Europe holds 29% share driven by sustainability-led upgrades and regulatory compliance. North America accounts for 21% of demand but leads in automation intensity, with over 58% of facilities integrating AI-enabled laminating systems. A structural shift is underway as packaging supply chains localize production post-2024 trade disruptions, reducing lead times by 18% and accelerating regional investments. Asia-Pacific leads in scale, Europe in compliance-driven innovation, and North America in advanced adoption—forcing companies to balance cost efficiency with technological differentiation and prioritize region-specific expansion strategies.

How are automation-led packaging upgrades accelerating high-speed laminating adoption?

North America holds approximately 21% share of the Vertical Laminating Machines market, driven by advanced packaging infrastructure and strong demand from food and pharmaceutical sectors. Over 58% of packaging plants have adopted automated laminating systems, improving production efficiency by 27%. Rising labor costs and supply chain disruptions post-2024 have forced manufacturers to accelerate automation investments. Companies are integrating AI-based process controls, reducing material waste by 22%. A major packaging group expanded laminating capacity by 16% in 2025 to meet demand. Enterprise buyers prioritize reliability and high-speed output, making this region a strategic hub for premium technology deployment and innovation-driven investments.

Why are sustainability mandates forcing rapid transition toward solvent-free laminating technologies?

Europe accounts for approximately 29% of the Vertical Laminating Machines market, led by Germany, Italy, and France. Regulatory pressure on emissions and solvent usage has pushed over 47% of facilities to adopt solvent-free laminating systems, reducing environmental impact by 24%. Compliance-driven upgrades are accelerating replacement cycles, with efficiency improvements of 23% in modern systems. Companies are investing in eco-friendly technologies and advanced coating systems to meet strict EU directives. Enterprise buyers prioritize compliance and long-term cost savings, making Europe a critical region where regulation directly shapes innovation and forces continuous technological adaptation.

What is enabling large-scale production and rapid deployment of cost-efficient laminating systems?

Asia-Pacific leads the Vertical Laminating Machines market with 42% share, driven by China, India, and Japan. The region accounts for over 45% of global production capacity, supported by manufacturing cost advantages of 18–22% compared to Western markets. More than 61% of large packaging facilities have adopted vertical laminating systems, improving throughput by 24%. Companies are scaling localized production and expanding export capacity, with output increasing by 19% between 2024 and 2025. Enterprise behavior prioritizes cost efficiency and speed, positioning Asia-Pacific as the global manufacturing and deployment hub critical for volume-driven expansion strategies.

How are packaging demand growth and cost constraints shaping equipment adoption patterns?

South America holds approximately 5% share of the Vertical Laminating Machines market, with Brazil and Argentina contributing over 68% of regional demand. Flexible packaging demand increased by 21%, driven by food and beverage sectors. However, import dependency and currency volatility raise equipment costs by 17%, limiting adoption of advanced systems. Around 38% of facilities are transitioning toward semi-automated laminating solutions. Companies are introducing cost-optimized machines and localized service networks, improving accessibility. Buyers remain highly price-sensitive, positioning this region as a high-potential but execution-sensitive market requiring balanced investment strategies.

How are infrastructure investments and industrial diversification driving laminating equipment demand?

Middle East & Africa accounts for approximately 3% of the Vertical Laminating Machines market, led by UAE and South Africa. Industrial and packaging sector investments increased by 23% between 2023 and 2025, supporting demand for laminating equipment. Over 34% of new packaging facilities are integrating automated laminating systems to improve efficiency by 20%. Strategic partnerships and imports dominate supply, with regional distribution networks improving delivery timelines by 15%. Enterprise buyers prioritize durability and long-term cost efficiency, positioning this region as an emerging market driven by infrastructure expansion and industrial diversification.

China Vertical Laminating Machines Market – 32%: High production capacity and strong demand from large-scale packaging industries

United States Vertical Laminating Machines Market – 21%: Advanced automation adoption and strong demand from food and pharmaceutical sectors

The Vertical Laminating Machines market is shaped by competition between global technology leaders such as Nordmeccanica, Bobst, and Comexi, and regional cost-focused manufacturers across Asia-Pacific. The top five players collectively hold approximately 64% share, reflecting a moderately consolidated structure where technology differentiation defines leadership. Global players compete on automation, precision, and sustainability, delivering systems that improve efficiency by over 30% and reduce waste by 20%, while regional manufacturers compete aggressively on price, offering 18–25% cost advantages.

Competition is increasingly shifting toward integrated solutions, with companies expanding through partnerships, digital integration, and vertical integration of components. Automation and solvent-free technologies are key battlegrounds, with over 46% of new installations incorporating advanced control systems. Entry barriers remain high due to capital intensity, technological complexity, and regulatory compliance requirements.

The competitive landscape is transitioning toward technology-led consolidation, where players investing in AI-driven systems and sustainable solutions are capturing premium segments. Winning in this market requires combining cost efficiency with advanced technology, strong supply chain control, and the ability to deliver scalable, customized solutions across regions.

Uteco Group

DCM Engineering

General Converting Equipment

Shaanxi Beiren Printing Machinery

Guangdong Fengming Machinery

Sinomech Machinery

HCI Converting Equipment

Technology in the Vertical Laminating Machines market is rapidly advancing toward intelligent, high-speed, and sustainable systems. AI-enabled laminating controls improve process precision by 28% while reducing material waste by 21%, enabling manufacturers to optimize production efficiency. Over 44% of advanced facilities have integrated IoT-based monitoring systems, allowing real-time performance tracking and predictive maintenance. Compared to traditional solvent-based laminating, solvent-free technologies improve operational efficiency by 26% and reduce emissions by 24%, making them a preferred choice in regulated markets.

Emerging technologies such as digital twin simulation and automated tension control are transforming production workflows. Adoption of digital twin models increased by 31%, enabling manufacturers to simulate and optimize laminating processes before deployment. These technologies reduce downtime by 23% and improve output consistency. Companies adopting these systems gain a significant competitive advantage through improved efficiency and reduced operational risk.

From 2026 to 2028, integration of smart factory ecosystems is expected to accelerate, with over 52% of new installations incorporating connected systems. This shift is redefining production strategies, enabling manufacturers to scale operations while maintaining precision. Companies investing in automation, AI, and sustainable technologies are positioning themselves as leaders in a market increasingly defined by efficiency, compliance, and technological innovation.

• In March 2026, Nordmeccanica introduced an AI-integrated laminating system improving process accuracy by 27% and reducing waste by 19%, enabling higher efficiency in flexible packaging lines and strengthening its premium technology leadership. [AI Integration] Source: https://www.nordmeccanica.com

• In November 2025, Bobst expanded its production capacity by 18% for laminating equipment, addressing rising demand in Europe and Asia while improving delivery timelines and reinforcing supply chain resilience. [Capacity Expansion] Source: https://www.bobst.com

• In July 2024, Comexi launched a solvent-free laminator reducing emissions by 24% and improving operational efficiency by 22%, aligning with sustainability mandates and accelerating adoption across regulated markets. [Sustainability Shift] Source: https://www.comexi.com

• In May 2024, Uteco Group partnered with packaging manufacturers to deploy advanced laminating systems, improving production throughput by 21% and enabling faster scaling of flexible packaging operations. [Strategic Partnership] Source: https://www.uteco.com

The Vertical Laminating Machines Market Report provides comprehensive coverage across machine types, applications, and end-user industries, analyzing over 20 distinct segments spanning automated, semi-automated, and solvent-free laminating technologies. The report evaluates demand across five major regions and more than 18 key countries, offering detailed insights into production distribution, adoption trends, and operational efficiency improvements exceeding 25% in advanced systems.

It delivers deep analytical insights into packaging, pharmaceutical, and industrial applications, where food packaging accounts for over 60% of total demand, while emerging segments such as eco-friendly laminating technologies are gaining traction with adoption rates exceeding 30%. The report also profiles leading companies and tracks strategic developments such as capacity expansion, technology integration, and regional manufacturing shifts.

From a strategic perspective, the report supports decision-making by identifying high-growth segments, regional expansion opportunities, and technology adoption patterns. It highlights forward-looking trends between 2026 and 2033, including AI-driven automation and sustainable laminating solutions, enabling businesses to align investment strategies, optimize operations, and strengthen competitive positioning in a rapidly evolving market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 456.3 Million |

|

Market Revenue in 2033 |

USD 679.3 Million |

|

CAGR (2026 - 2033) |

5.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nordmeccanica, Bobst, Comexi, Uteco Group, DCM Engineering, General Converting Equipment, Shaanxi Beiren Printing Machinery, Guangdong Fengming Machinery, Sinomech Machinery, HCI Converting Equipment |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |