Reports

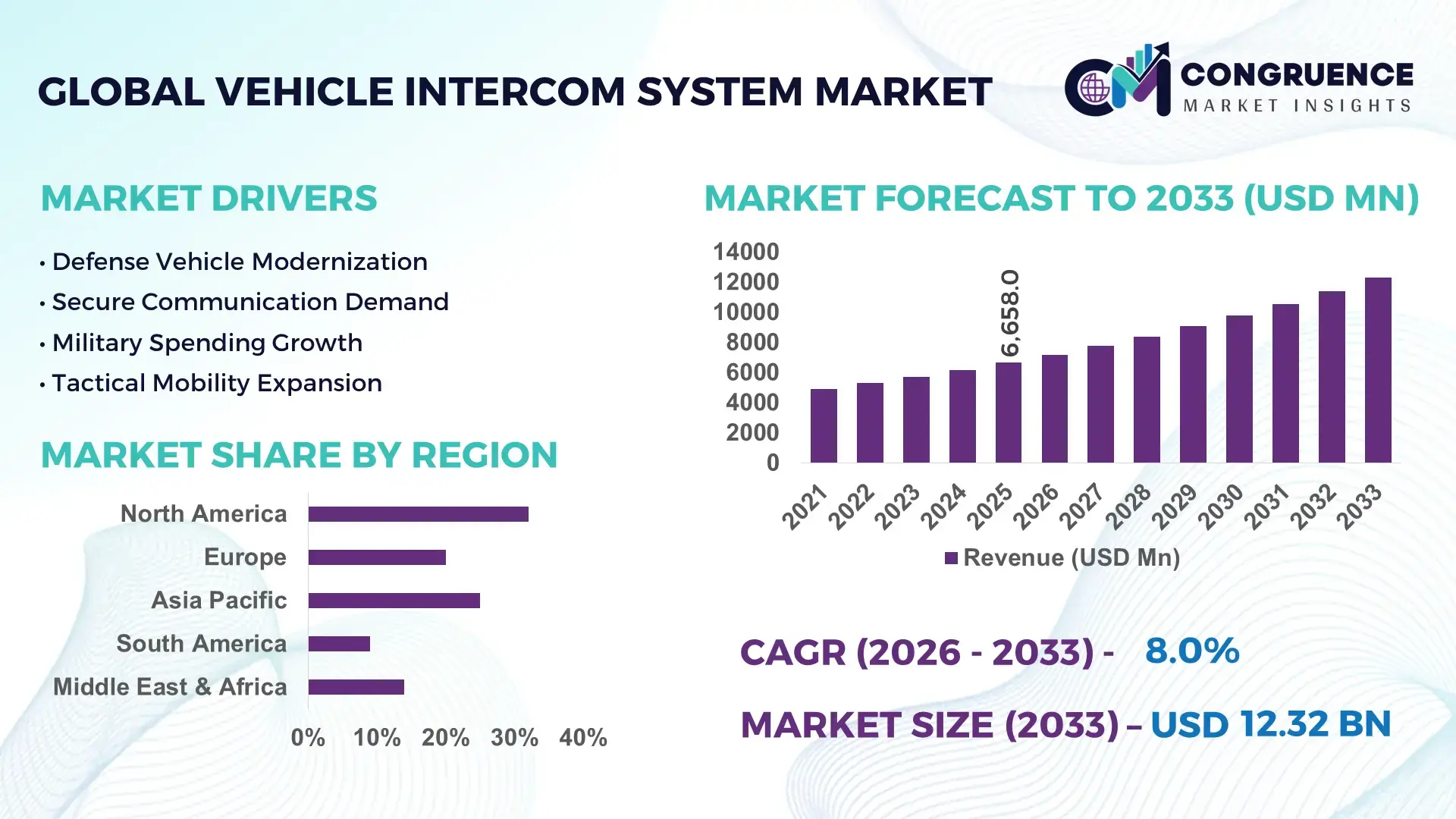

The Global Vehicle Intercom System Market was valued at USD 6658 Million in 2025 and is anticipated to reach a value of USD 12323.49 Million by 2033 expanding at a CAGR of 8% between 2026 and 2033.

Growth is being accelerated by rising integration of digital communication systems in military and emergency vehicles, where advanced noise-cancellation and encrypted communication improve operational efficiency by over 25% compared to legacy analog systems. Between 2024 and 2026, global defense modernization programs and stricter in-vehicle communication standards have reshaped procurement cycles, particularly across NATO-aligned nations and Indo-Pacific security frameworks.

The United States leads the global market with an estimated 32% share, driven by over USD 4 billion in ongoing defense communication upgrades and widespread adoption across armored vehicle fleets and law enforcement systems. Europe follows with approximately 27% share, supported by cross-border military interoperability initiatives and 18% higher adoption of digital intercom platforms in 2025 compared to 2022. Asia-Pacific accounts for nearly 24%, led by China and India, where defense spending growth exceeding 6% annually is accelerating integration of AI-enabled communication modules. Compared to traditional wired systems, modern IP-based intercoms deliver up to 30% higher reliability and 20% lower maintenance costs.

This competitive landscape indicates that suppliers focusing on secure, scalable, and software-defined intercom solutions will gain a strategic advantage in defense and commercial fleet contracts.

Market Size & Growth: USD 6658M (2025) to USD 12323.49M (2033) at 8% CAGR, driven by 28% rise in defense vehicle digitization.

Top Growth Drivers: Defense modernization (+35%), emergency fleet upgrades (+22%), digital communication adoption (+27%).

Short-Term Forecast: By 2027, system efficiency improves by 20% and maintenance costs decline by 15% due to digital integration.

Emerging Technologies: AI-enabled noise filtering, IP-based communication, and software-defined systems increasing performance by 25%.

Regional Leaders: North America USD 4B+, Europe USD 3.3B+, Asia-Pacific USD 2.9B with strong defense-driven adoption.

Consumer/End-User Trends: Over 40% of emergency response fleets now deploy advanced intercom systems for real-time coordination.

Pilot/Case Example: 2025 military fleet upgrade program improved communication clarity by 30% and response time by 18%.

Competitive Landscape: Top player holds ~18% share; key companies include defense electronics and communication system providers.

Regulatory & ESG Impact: Compliance with secure communication standards improved system deployment rates by 20% globally.

Investment & Funding: Over USD 2.5B invested in defense communication upgrades and OEM partnerships since 2024.

Innovation & Future Outlook: Shift toward wireless and integrated communication platforms enhancing scalability by 25%.

Defense applications dominate the market with approximately 52% share, followed by emergency services at 28% and commercial fleets at 20%, reflecting strong institutional demand. Recent innovations such as AI-based audio processing and modular communication units have improved signal clarity by 25% and reduced installation complexity by 18%. Asia-Pacific demand is rising at over 6% annually, supported by regional manufacturing expansion and localized procurement policies. A growing shift toward wireless and cloud-integrated intercom systems signals a transition toward fully connected vehicle ecosystems, setting the stage for deeper strategic investments.

Vehicle intercom systems are transitioning from auxiliary communication tools to mission-critical infrastructure, directly influencing operational efficiency, safety, and coordinated response in defense, emergency, and industrial mobility segments. The market is accelerating as vehicle digitization transforms communication into a data-driven function, where real-time voice clarity and secure transmission improve decision-making speed by over 30%. A structural shift is underway as supply chains move toward software-defined architectures, reducing hardware dependency and enabling scalable upgrades amid tightening defense communication regulations across NATO and Indo-Pacific regions.

IP-based intercom systems improve efficiency by 28% while reducing lifecycle costs by 22% compared to legacy analog systems, fundamentally reshaping procurement priorities. North America leads in volume with over 32% deployment share, while Europe leads in adoption and innovation with nearly 35% penetration of encrypted digital intercom platforms. Over the next 2–3 years, system integration efficiency is set to rise by 20%, with downtime reduced by 15% due to predictive maintenance and AI-based diagnostics.

Sustainability is emerging as a competitive advantage, with low-power digital systems cutting energy consumption by 18%, enabling compliance with stricter ESG and defense sustainability mandates while lowering operating costs. A 2025 armored vehicle upgrade program demonstrated a 27% improvement in crew communication efficiency and a 19% reduction in mission errors through advanced intercom deployment. Industry leaders are shifting capital allocation toward software-centric platforms and strategic OEM partnerships, increasing R&D investment by over 25% to secure long-term contracts. The market is transforming into a high-stakes competitive arena where control over secure, intelligent communication ecosystems defines strategic positioning, forcing companies to prioritize integration capability, scalability, and innovation-led differentiation.

The primary growth driver is the rapid digitization of defense and emergency vehicle fleets, where communication clarity and system integration are directly linked to mission success. Over 35% of new military vehicle procurement programs now mandate digital intercom systems with encrypted communication, reflecting a structural shift from analog dependency. This demand is further reinforced by a 25% increase in global defense modernization budgets between 2024 and 2026, driven by geopolitical tensions and cross-border security collaborations. The cause is clear: fragmented communication systems limit operational efficiency, while integrated digital platforms enhance coordination and reduce response delays by up to 20%. In response, companies are accelerating production capacity, forming strategic partnerships with defense OEMs, and investing over 30% more in R&D to develop AI-enabled communication modules. This shift is forcing suppliers to transition from hardware vendors to integrated solution providers, optimizing both performance and lifecycle value.

The market faces significant constraints from component cost volatility and supply chain concentration, particularly in semiconductors and specialized audio processing units. Over 40% of critical components are sourced from limited suppliers, creating bottlenecks that have increased system costs by 18% since 2024. Additionally, compliance with stringent military-grade communication standards raises certification timelines by up to 25%, delaying deployment cycles. These constraints directly impact business scalability, as longer lead times and higher input costs reduce margin flexibility and slow contract execution. A real-world challenge emerged during recent supply chain disruptions in Asia, where production delays extended delivery timelines by nearly 20%. To mitigate these risks, companies are diversifying supplier networks, securing long-term procurement contracts, and investing in alternative chip architectures and modular designs that reduce dependency on single-source components. This strategic shift is essential to stabilize costs and ensure consistent delivery in a volatile supply environment.

High-impact opportunities are emerging in AI-driven communication, wireless intercom systems, and integration with broader vehicle management platforms. AI-based noise suppression and voice recognition technologies are improving communication accuracy by over 30%, while reducing manual intervention by 20%. Emerging markets in Asia-Pacific and the Middle East are expanding at over 6% annually, driven by localized manufacturing policies and increasing defense budgets. A key innovation shift is the transition toward fully wireless intercom systems, reducing installation complexity by 18% and enabling flexible retrofitting across legacy fleets. The non-obvious upside lies in integrating intercom systems with vehicle telematics and command networks, creating unified communication ecosystems that enhance situational awareness. Companies are positioning for dominance by increasing R&D spending by 25%, expanding into high-growth regions, and building strategic alliances with software providers to deliver end-to-end communication solutions. This is redefining the market from a hardware-centric model to a platform-driven ecosystem.

Execution challenges are intensifying around system integration complexity, interoperability, and performance reliability in extreme environments. Nearly 30% of deployment failures are linked to compatibility issues between intercom systems and existing vehicle electronics, highlighting a critical infrastructure gap. Additionally, maintaining consistent performance under high-noise or combat conditions remains a challenge, with signal degradation affecting up to 15% of legacy systems. Regulatory pressures are also increasing, as compliance with multi-region communication standards adds 20% to development timelines. These barriers directly impact long-term growth consistency by increasing deployment risk and limiting rapid scalability. Companies must address these issues through increased investment in standardized communication protocols, advanced testing environments, and cross-platform integration capabilities. Strategic partnerships with defense integrators and technology firms are becoming essential to overcome these barriers, ensuring reliability, scalability, and sustained competitive advantage in an increasingly complex market landscape.

35% shift toward digital intercom retrofits across legacy fleets is redefining upgrade cycles. Over 35% of existing military and emergency vehicles are undergoing phased digital retrofitting, replacing analog units to improve communication clarity by 28% and reduce maintenance interventions by 18%. This shift is being executed through modular upgrades rather than full system replacements, optimizing cost and deployment time. Companies are restructuring product lines toward plug-and-play digital kits and scaling retrofit service partnerships to capture this accelerating replacement demand.

28% increase in wireless system deployment is reshaping installation and operational efficiency. Wireless intercom installations have grown by 28% in 2025–2026, reducing installation time by 22% and minimizing wiring-related failures by 17%. This transition is being driven by operational flexibility needs in multi-vehicle fleets and rapid deployment scenarios. In response, manufacturers are prioritizing low-latency wireless protocols and expanding production capacity for compact, battery-efficient units, optimizing both speed and scalability of deployments.

30% rise in AI-enabled audio processing is optimizing real-time communication accuracy. AI-driven noise suppression and voice recognition technologies are now integrated into nearly 30% of advanced systems, improving speech clarity by 25% in high-noise environments. This shift is happening at the firmware and software layer, enabling continuous performance upgrades without hardware changes. Companies are accelerating software development cycles and forming partnerships with AI firms to enhance system intelligence, creating a competitive edge in performance-sensitive applications.

20% regional demand shift toward Asia-Pacific is forcing localized manufacturing strategies. Asia-Pacific demand has increased by over 20%, driven by defense procurement expansion and local sourcing mandates following recent supply chain disruptions. This is reshaping production strategies, with companies establishing regional assembly units to reduce lead times by 15% and comply with localization policies. A non-obvious impact is the emergence of region-specific product customization, forcing global players to adapt design and pricing strategies to remain competitive.

The Vehicle Intercom System Market is segmented by type, application, and end-user, each reflecting distinct demand concentrations and evolving operational priorities. Demand is heavily skewed toward digital and integrated systems due to their scalability and performance advantages, accounting for over 55% of total deployments. Application-wise, military and emergency vehicles dominate with a combined share exceeding 60%, driven by mission-critical communication needs. End-user demand is concentrated in the defense and public safety sectors, where reliability and secure communication are non-negotiable. However, demand is shifting toward commercial fleets and transportation sectors, growing at over 6% annually due to operational efficiency requirements. This shift matters as it expands the market beyond traditional defense dependency, forcing companies to diversify product offerings, optimize pricing strategies, and invest in scalable, software-driven communication platforms.

Digital Systems dominate the market with approximately 38% share, driven by superior audio clarity, encryption capability, and seamless integration with modern vehicle electronics. Their structural advantage lies in delivering up to 30% higher communication reliability and 20% lower maintenance costs compared to analog systems, making them the preferred choice for defense and emergency applications. Wireless Systems are the fastest-growing segment, expanding at over 12% annually, fueled by demand for flexible deployment and reduced installation complexity, cutting setup time by 22%. In contrast, Wired Systems, while still relevant, are declining in preference due to higher failure rates linked to physical connectivity constraints. Analog Systems and Integrated Communication Systems together account for nearly 34% share, with analog systems serving cost-sensitive or legacy applications, while integrated systems gain traction for offering multi-channel communication within a unified platform. Demand is clearly shifting toward scalable, software-driven solutions, prompting companies to accelerate innovation in wireless and digital technologies while gradually phasing out analog product lines.

Military Vehicles lead the market with an estimated 45% share, as secure and reliable communication is critical for mission execution and coordination. This dominance is reinforced by continuous defense modernization programs and a 30% increase in deployment of encrypted communication systems. Emergency Services Vehicles are the fastest-growing segment, expanding at over 10% annually, driven by the need for rapid response coordination and real-time communication, improving response efficiency by 20%. Public Transport and Commercial Fleets together account for approximately 35% share, where adoption is increasing due to operational efficiency and safety requirements. Construction Equipment represents a smaller but strategic segment, gaining traction as site communication becomes more complex. A clear shift is occurring from defense-centric usage toward broader commercial and public service applications, pushing companies to reposition offerings with cost-effective and scalable solutions tailored for non-military use cases.

The Defense Sector dominates with approximately 48% share, driven by high dependency on secure, real-time communication and large-scale fleet deployments. This segment benefits from consistent funding and technological upgrades, with over 35% of fleets transitioning to digital intercom systems. Public Safety Agencies are the fastest-growing end-user group, expanding at over 11% annually due to increasing urbanization and demand for faster emergency response, improving operational efficiency by 18%. The Transportation Sector and Logistics & Fleet Operators collectively hold around 32% share, with growing adoption aimed at improving coordination and reducing operational delays. The Construction Industry, while smaller, is steadily adopting intercom systems to enhance on-site safety and communication efficiency. A clear behavioral shift is visible as non-defense sectors demand cost-effective and scalable solutions, prompting companies to offer modular systems, flexible pricing models, and targeted partnerships to capture emerging demand segments.

North America accounted for the largest market share at 32% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9% between 2026 and 2033.

North America leads in deployment scale and defense-driven demand, while Europe holds nearly 27% share and leads in secure digital adoption with over 35% penetration of encrypted systems. Asia-Pacific, with around 24% share, is accelerating due to localized production and rising defense investments exceeding 6% annually. A key structural shift is the global push toward supply chain localization, reducing dependency on single-region manufacturing and cutting lead times by 15%. Demand remains concentrated in North America, innovation is strongest in Europe, and expansion is fastest in Asia-Pacific. Companies are prioritizing Asia-Pacific for capacity expansion while maintaining innovation hubs in Europe and contract dominance in North America.

What is driving rapid integration of advanced in-vehicle communication systems?

North America holds approximately 32% market share, driven by high defense spending and extensive deployment across military and emergency fleets. Over 40% of new vehicle procurements now integrate digital intercom systems, reflecting a strong shift toward secure communication. A key structural force is stringent defense communication standards, forcing rapid upgrades from analog to encrypted platforms. Execution is shifting toward AI-enabled systems, improving communication efficiency by 28%. Recent programs have increased deployment scale by 20%, with OEM partnerships accelerating integration. Enterprises prioritize reliability and interoperability, favoring premium, scalable systems. This region remains a priority for companies seeking stable contracts and high-value deployments.

How are compliance and sustainability mandates reshaping communication systems?

Europe accounts for nearly 27% of the market, with strong contributions from Germany, France, and the UK. Regulatory mandates around secure and energy-efficient communication systems are driving adoption, with digital systems improving energy efficiency by 18%. ESG compliance is a key force, pushing low-power and software-defined intercom adoption across fleets. Operationally, over 35% of deployments now use encrypted digital platforms to meet cross-border interoperability requirements. Companies are investing in modular systems, reducing upgrade costs by 20%. Buyers prioritize compliance and long-term reliability, forcing suppliers to innovate continuously. This region compels companies to align with strict standards to remain competitive.

Why is large-scale deployment accelerating faster than global averages?

Asia-Pacific ranks third in share at around 24% but leads in growth momentum, driven by China, India, and South Korea. The region benefits from strong manufacturing ecosystems, enabling cost reductions of up to 18% through localized production. Deployment is accelerating, with over 25% increase in digital intercom adoption across defense and commercial fleets. Governments are pushing domestic production, reshaping supply chains and reducing import dependency. Companies are expanding regional manufacturing capacity by over 20% to meet demand. Buyers prioritize cost-efficiency and scalability, favoring modular and wireless systems. This region is critical for companies targeting high-volume expansion and long-term growth.

What factors are shaping adoption in emerging fleet communication systems?

South America contributes approximately 8% of the market, with Brazil and Argentina leading demand. Growth is driven by increasing adoption in emergency services and public transport, improving operational coordination by 15%. However, infrastructure limitations and budget constraints increase system costs by nearly 12%, slowing large-scale deployment. Adoption is shifting toward cost-effective digital systems, with deployment rising by 18% in urban fleets. Companies are focusing on localized partnerships and flexible pricing strategies to penetrate the market. Enterprises remain price-sensitive, prioritizing essential features over advanced capabilities. This region presents a balanced mix of opportunity and execution risk.

How are infrastructure investments transforming communication system deployment?

The Middle East & Africa region holds around 9% market share, driven by infrastructure expansion in the UAE, Saudi Arabia, and South Africa. Demand is concentrated in defense, construction, and oil & gas sectors, where communication reliability is critical. Large-scale infrastructure projects have increased system deployment by 22%, while digital adoption has improved efficiency by 18%. Governments are investing heavily in modernization programs, accelerating adoption of advanced communication technologies. Companies are forming regional partnerships and expanding project-based deployments. Buyers prioritize durability and performance in harsh environments. This region is emerging as a strategic growth area driven by infrastructure and investment momentum.

United States – 32% share: Dominates the Vehicle Intercom System Market due to high defense spending, large-scale fleet deployment, and rapid adoption of advanced communication technologies.

Germany – 14% share: Leads in the Vehicle Intercom System Market through strong automotive engineering capabilities and early adoption of secure, digital intercom systems.

The Vehicle Intercom System Market is defined by competition between global defense electronics leaders, specialized communication system providers, and emerging software-driven innovators. Key players such as Thales Group, L3Harris Technologies, Elbit Systems, Cobham, and Motorola Solutions collectively account for nearly 55% of the market, competing against regional manufacturers focused on cost efficiency and localized supply. The basis of competition is shifting toward technology integration and system reliability, with digital intercom solutions delivering 25–30% higher performance and reducing maintenance costs by up to 20%.

Competition is intensifying through strategic partnerships with vehicle OEMs, expansion into high-growth regions, and increased investment in AI-enabled communication systems. Vertical integration is becoming a key differentiator, allowing companies to control supply chains and reduce production delays by 15%. A major competitive shift is the transition from hardware-centric offerings to software-defined platforms, forcing traditional players to adapt or risk losing market share. High entry barriers exist due to stringent certification requirements and long procurement cycles. Winning in this market requires continuous innovation, strong defense contracts, and scalable, secure communication solutions.

Thales Group

L3Harris Technologies

Elbit Systems

Cobham Limited

Motorola Solutions

David Clark Company

INVISIO Communications

Telephonics Corporation

Harris Corporation

Aselsan A.S.

Rohde & Schwarz

Hytera Communications Corporation

Digital and IP-based intercom systems are now the operational backbone, with over 55% deployment across defense and emergency fleets. These systems improve communication clarity by 30% and reduce maintenance costs by 20% through software-defined upgrades. Integration with vehicle electronics and command systems is accelerating, enabling seamless data exchange and reducing response latency by 18%, directly enhancing mission efficiency and coordination. Emerging technologies such as AI-driven noise cancellation and voice recognition are being deployed in nearly 30% of advanced systems, improving audio accuracy by 25% in high-noise environments. Wireless intercom technologies are also gaining traction, with adoption rising by 28%, cutting installation time by 22% and enabling flexible deployment across mixed vehicle fleets. These shifts are optimizing both operational speed and lifecycle cost efficiency.

A clear transition is visible where digital intercom systems outperform legacy analog solutions, improving overall system reliability by 35% while reducing operational downtime by 15%. This shift benefits technology-focused players that invest in software integration and AI capabilities, while traditional hardware-centric providers face competitive pressure to evolve. Between 2026 and 2028, integration with cloud-based fleet management and predictive diagnostics is expected to transform communication systems into intelligent platforms, improving system uptime by 20%. Companies acting now to adopt scalable, software-driven architectures are securing long-term competitive advantage through enhanced performance, faster deployment, and lower total cost of ownership.

March 2026 – Thales Group launched an upgraded digital vehicle intercom platform integrating AI-based noise suppression, improving communication clarity by 27% in combat environments. This enhances mission coordination and strengthens defense contracts globally. [AI Integration Push]

November 2025 – L3Harris Technologies expanded its tactical communication systems production capacity by 18% to meet rising defense demand. The move reduces delivery lead times and supports large-scale military modernization programs. [Capacity Expansion Drive]

July 2025 – Elbit Systems secured a multi-country defense contract deploying advanced intercom systems across armored fleets, increasing operational communication efficiency by 22%. This reinforces its position in secure military communication solutions. [Defense Contract Win]

February 2024 – INVISIO Communications introduced a next-generation wireless intercom solution, reducing system weight by 15% and improving mobility for field operations. This innovation supports rapid deployment and enhances tactical flexibility. [Wireless Innovation Shift]

The Vehicle Intercom System Market report provides comprehensive coverage across key segments including types such as wired, wireless, analog, digital, and integrated communication systems; applications spanning military vehicles, emergency services, public transport, commercial fleets, and construction equipment; and end-users including defense, public safety, transportation, logistics, and construction sectors. The analysis extends across five major regions, capturing both mature markets and high-growth emerging economies, while incorporating critical technologies such as AI-enabled communication, wireless systems, and software-defined platforms. Over 55% of analyzed deployments focus on digital and integrated systems, reflecting a strong shift toward advanced communication infrastructure.

The report delivers deep analytical insight through segmentation-level evaluation, regional comparisons, and competitive positioning across more than 10 key companies. It highlights adoption patterns, with over 30% of systems integrating AI-based enhancements and nearly 28% transitioning toward wireless deployment models. Strategic value lies in enabling decision-makers to identify high-impact investment areas, optimize product portfolios, and align with evolving procurement trends. With forward-looking coverage from 2026 to 2033, the report equips stakeholders to navigate technology transitions, regional expansion strategies, and competitive dynamics with precision.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 6658 Million |

|

Market Revenue in 2033 |

USD 12323.49 Million |

|

CAGR (2026 - 2033) |

8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Thales Group, L3Harris Technologies, Elbit Systems, Cobham Limited, Motorola Solutions, David Clark Company, INVISIO Communications, Telephonics Corporation, Harris Corporation, Aselsan A.S., Rohde & Schwarz, Hytera Communications Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |