Reports

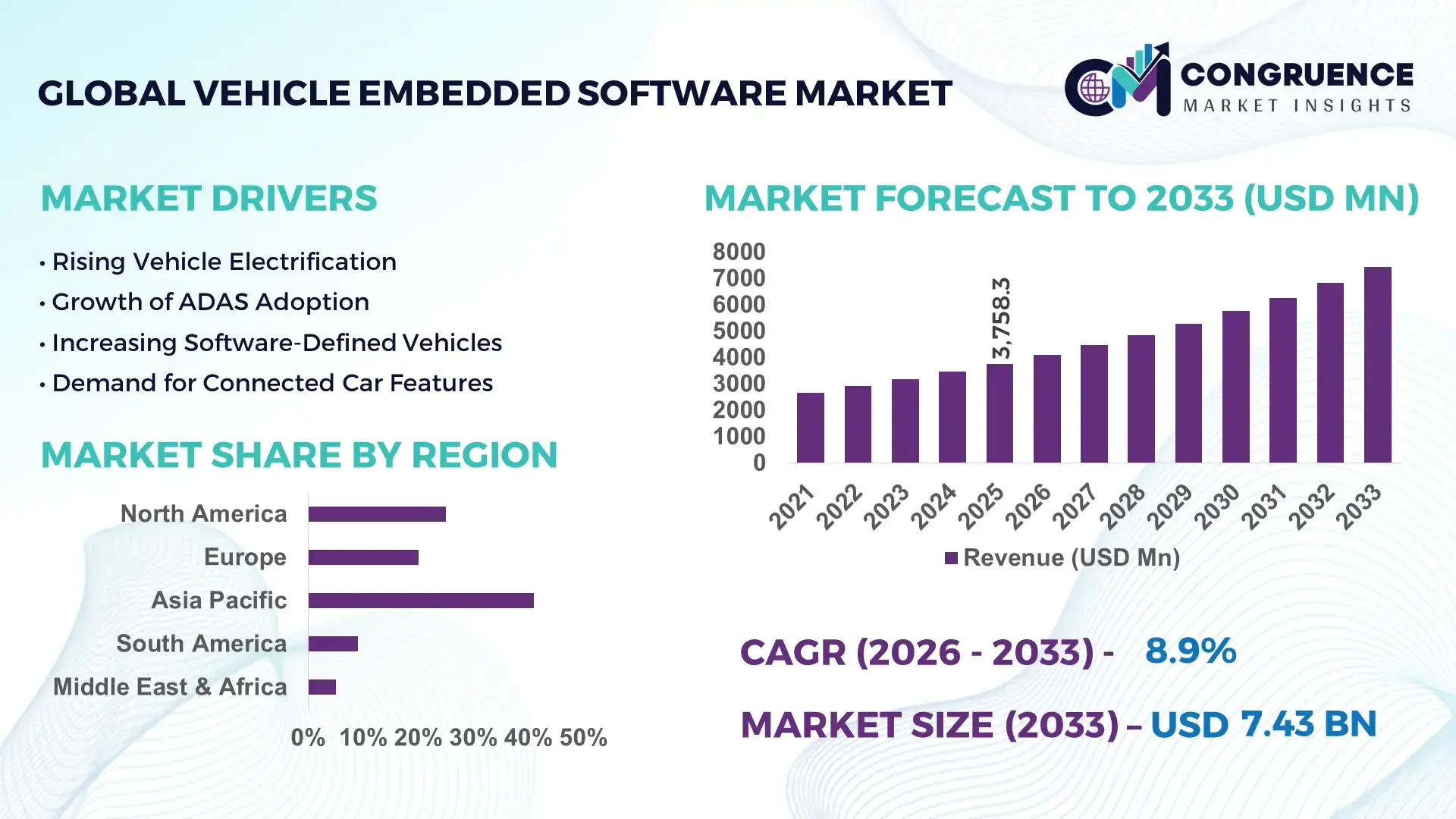

The Global Vehicle Embedded Software Market was valued at USD 3758.3 Million in 2025 and is anticipated to reach a value of USD 7433.86 Million by 2033 expanding at a CAGR of 8.9% between 2026 and 2033. This growth is driven by the accelerating transition toward software-defined vehicles, centralized electronic architectures, and AI-enabled safety and infotainment systems across passenger and commercial fleets.

China dominates the global vehicle embedded software ecosystem with extensive automotive electronics manufacturing capacity and large-scale domestic software investment. The country produced over 30 million vehicles in 2024, most integrating embedded operating systems across infotainment, ADAS, and body control modules. Annual automotive software R&D investment exceeds USD 15 billion, supported by more than 2,000 Tier-1 suppliers and system integrators. Over 65% of newly registered vehicles in China now feature connected infotainment and telematics software, while AI-based perception platforms and over-the-air update systems are being deployed at scale across smart factory clusters manufacturing ECUs and domain controllers.

• Market Size & Growth: USD 3758.3 Million in 2025, projected to reach USD 7433.86 Million by 2033, expanding at a CAGR of 8.9% due to software-defined vehicle platforms.

• Top Growth Drivers: ADAS penetration 42%, connected vehicle system adoption 38%, ECU consolidation efficiency 31%.

• Short-Term Forecast: By 2028, embedded software optimization is expected to improve in-vehicle system performance by 27%.

• Emerging Technologies: AUTOSAR Adaptive platforms, AI-based perception engines, real-time over-the-air update frameworks.

• Regional Leaders: Asia Pacific USD 3020 Million by 2033 with smart cockpit integration, Europe USD 2410 Million with safety software expansion, North America USD 2003 Million with autonomous-ready platforms.

• Consumer/End-User Trends: Passenger vehicles represent over 68% of total embedded software deployments, driven by infotainment, navigation, and driver monitoring demand.

• Pilot or Case Example: In 2024, a global OEM reduced in-vehicle software downtime by 34% through centralized domain controller deployment.

• Competitive Landscape: Market leader holds approximately 21% share, followed by Bosch, Continental, Aptiv, Denso, and NVIDIA.

• Regulatory & ESG Impact: Functional safety, cybersecurity compliance, and emission regulations are accelerating secure embedded software adoption.

• Investment & Funding Patterns: More than USD 9.6 Billion invested globally in automotive software platforms and AI-based vehicle control systems.

• Innovation & Future Outlook: Zonal architectures, cloud-connected vehicle software, and AI-driven system orchestration will reshape embedded automotive ecosystems.

The vehicle embedded software market is segmented across powertrain systems contributing approximately 29% of demand, infotainment and telematics at 26%, advanced driver assistance systems at 24%, and body electronics at 21%. Continuous innovations in centralized computing, sensor fusion algorithms, and real-time operating environments are redefining vehicle intelligence. Regulatory pressure for safety, cybersecurity, and emissions compliance, combined with rising electrification, is accelerating adoption. Asia Pacific leads consumption through high vehicle output, while Europe and North America show strong momentum in autonomous and connected platforms, positioning embedded software as a foundational technology for next-generation mobility.

The Vehicle Embedded Software Market has become a core strategic layer within the global automotive value chain as vehicles transition from hardware-centric machines to software-defined mobility platforms. More than 70% of new vehicle functionalities are now controlled by embedded software, including ADAS, infotainment, powertrain optimization, and battery management systems. Next-generation zonal and domain-based architectures are replacing legacy distributed ECUs, reducing electronic complexity by over 35% per vehicle and enabling faster feature deployment cycles. As a comparative benchmark, zonal vehicle computing delivers 28% improvement in data processing efficiency compared to traditional distributed ECU standards. Asia Pacific dominates in volume, while Europe leads in adoption with 61% of automakers integrating centralized software platforms into new vehicle programs.

By 2028, AI-based embedded control systems are expected to cut in-vehicle system latency by 32% through predictive task scheduling and real-time diagnostics. ESG and compliance priorities are also shaping market strategies, with automotive manufacturers committing to energy-efficiency improvements such as 25% reduction in in-vehicle electronic power consumption by 2030. In 2024, a leading Chinese automaker achieved a 30% reduction in system failure incidents through the deployment of AI-driven embedded diagnostics and over-the-air update frameworks across its electric vehicle portfolio. Looking forward, the Vehicle Embedded Software Market will serve as a critical pillar for resilience, regulatory compliance, and sustainable growth as software increasingly defines vehicle intelligence, safety, and lifecycle value.

Advanced driver assistance systems and connected vehicle technologies are major catalysts for embedded software deployment. More than 55% of new vehicles now include Level 1 or Level 2 ADAS functions, all of which rely on real-time embedded software for sensor fusion, object detection, and decision-making. Connected vehicle adoption has surpassed 60% globally, enabling navigation, remote diagnostics, and infotainment services. Each connected vehicle generates over 25 GB of data per hour, requiring high-performance embedded operating systems and middleware. Automakers are consolidating control functions into domain controllers, reducing wiring complexity by up to 40% while improving response times. This integration is pushing OEMs to invest heavily in scalable software platforms, directly strengthening demand across the Vehicle Embedded Software Market.

As vehicle software stacks grow more complex, development, testing, and validation cycles have lengthened significantly. A modern connected vehicle may contain over 100 million lines of code, increasing integration risks and system vulnerability. Cybersecurity threats targeting in-vehicle networks have risen by more than 40% over the past three years, forcing manufacturers to implement advanced encryption and intrusion detection systems. Compliance with safety standards such as ISO 26262 and cybersecurity regulations adds substantial cost and time to product launches. These challenges slow innovation cycles and increase operational overhead, limiting the pace at which new embedded software solutions can be deployed across global automotive platforms.

The transition toward software-defined vehicles presents significant growth opportunities as OEMs migrate from hardware-centric models to upgradable digital platforms. Over-the-air update capabilities are now being integrated into more than 50% of new vehicles, enabling feature enhancements without physical recalls. Centralized computing architectures reduce electronic components by up to 30%, lowering production costs while improving scalability. Emerging electric vehicle platforms increasingly rely on embedded software for battery health monitoring, energy optimization, and thermal management. This creates new demand for AI-enabled control systems and real-time operating platforms, positioning embedded software as a long-term value driver within the global automotive ecosystem.

Automotive embedded software must comply with stringent safety, cybersecurity, and data protection regulations across multiple regions. Meeting functional safety requirements alone can add up to 20% additional development time per project. Integration across heterogeneous hardware platforms further increases engineering complexity and testing costs. Supply chain disruptions and semiconductor shortages have also delayed software-hardware synchronization, impacting production timelines. These regulatory and operational pressures raise total development expenditure and limit rapid scalability, creating persistent challenges for suppliers and OEMs operating within the Vehicle Embedded Software Market.

• Rapid Shift Toward Centralized and Zonal Architectures (35% ECU Reduction, 28% Latency Improvement)

The transition from distributed electronic control units to centralized domain and zonal architectures is reshaping the Vehicle Embedded Software market. Automotive manufacturers are reducing in-vehicle ECUs by up to 35%, lowering wiring complexity and system weight while improving real-time data flow. Central computing platforms process over 5× higher data volumes per second compared to legacy layouts, while embedded middleware optimization has improved task response latency by 28%. This architectural shift enables faster software updates, reduces integration time by nearly 30%, and supports scalable deployment of AI-driven driver assistance and infotainment functions across multiple vehicle platforms.

• Expansion of Over-the-Air (OTA) Software Ecosystems (60% Connected Vehicles, 40% Update Cost Reduction)

OTA-enabled embedded platforms are now deployed in more than 60% of newly produced connected vehicles, enabling remote software patching, performance upgrades, and cybersecurity enhancements. Automakers report up to 40% reduction in service update costs and a 25% decrease in recall-related service visits through OTA frameworks. Vehicles now receive an average of 12–15 software updates annually, compared to fewer than 3 updates under traditional dealer-based models. This trend is strengthening lifecycle software management strategies and increasing embedded software’s role in post-sale customer engagement.

• AI-Driven Embedded Control Systems (32% Decision Accuracy Gain, 22% Energy Efficiency Improvement)

AI-based embedded software is increasingly deployed for sensor fusion, predictive maintenance, and driver behavior analysis. In-vehicle AI algorithms have improved object detection and decision accuracy by 32% while reducing false alerts by 21%. Powertrain and battery management software enhanced with machine learning now delivers up to 22% energy efficiency gains through adaptive load balancing and thermal control. These capabilities are enabling real-time performance optimization and smarter autonomous functions across electric and hybrid vehicle platforms.

• Rising Cybersecurity and Functional Safety Integration (45% Threat Detection Increase, 30% Risk Mitigation)

With connected vehicles generating more than 25 GB of data per hour, cybersecurity-focused embedded software adoption has increased sharply. Integrated security frameworks have improved threat detection rates by 45% and reduced system vulnerability exposure by 30%. Secure boot, encryption, and intrusion detection systems are now embedded across over 70% of new vehicle platforms. This trend reflects the growing regulatory and operational need for resilient software infrastructures that safeguard vehicle networks and ensure functional safety across increasingly complex automotive ecosystems.

The Vehicle Embedded Software market is segmented by type, application, and end-user, each reflecting distinct technological requirements and adoption behaviors. By type, operating systems, middleware, and application software form the core architecture supporting real-time control, connectivity, and functional safety. Application-wise, ADAS, infotainment, telematics, powertrain, and body electronics account for the majority of software integration across modern vehicles. End-user demand is primarily driven by passenger vehicle manufacturers, followed by commercial vehicle OEMs and fleet operators deploying connected and autonomous-ready platforms. Over 70% of new vehicles now integrate multi-domain embedded software stacks, indicating strong cross-segment convergence. The segmentation structure highlights how software is no longer confined to infotainment or navigation but is embedded across critical safety, performance, and connectivity layers. Growing regulatory requirements, consumer demand for digital experiences, and the transition toward electric and autonomous vehicles are accelerating multi-segment adoption, making segmentation analysis essential for technology providers and OEM strategy planning.

Operating systems currently account for 42% of adoption, while middleware platforms hold 25%. However, application-layer software is rising fastest, expected to surpass 30% by 2033. Real-time operating systems lead the type segment due to their role in controlling safety-critical functions such as braking, steering, and battery management, and they dominate embedded deployments across ADAS and powertrain systems. Middleware serves as the integration backbone between hardware and applications, supporting data exchange across vehicle domains and representing nearly one-quarter of total installations. Application software is the fastest-growing type, expanding at a CAGR of 13.4%, driven by the rapid rollout of digital cockpits, driver monitoring systems, and AI-based perception features. The remaining segments, including firmware utilities and diagnostic tools, together contribute approximately 33% of total demand, supporting lifecycle management and system reliability.

ADAS software accounts for 39% of embedded deployments, while infotainment and telematics hold 28%. However, autonomous driving software is rising fastest, expected to surpass 32% by 2033. ADAS leads due to regulatory mandates for collision avoidance, lane assistance, and adaptive cruise control, all of which rely on real-time embedded perception and decision engines. Infotainment and telematics follow, driven by consumer demand for connected navigation, media, and remote diagnostics. Autonomous and semi-autonomous driving applications represent the fastest-growing segment, expanding at a CAGR of 14.1%, supported by sensor fusion platforms and AI-based control algorithms. Other applications, including body electronics and climate control systems, together account for 33% of market usage, ensuring comfort, safety, and energy efficiency.

Passenger vehicle OEMs account for 68% of embedded software adoption, while commercial vehicle manufacturers hold 21%. However, mobility and fleet service providers are rising fastest, expected to surpass 25% by 2033. Passenger vehicles dominate due to high production volumes and consumer demand for digital cockpits, connectivity, and driver assistance features. Commercial vehicle OEMs follow, leveraging embedded telematics and fleet management software to optimize logistics and reduce downtime. Mobility platforms and fleet operators are the fastest-growing end-user group, expanding at a CAGR of 12.6%, driven by connected fleet analytics, predictive maintenance, and autonomous delivery pilots. Other end-users, including off-highway vehicle manufacturers and public transport authorities, together represent 11% of total adoption.

Asia Pacific accounted for the largest market share at 41% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2026 and 2033.

Asia Pacific recorded the highest vehicle production volume at over 48 million units in 2025, with embedded software integration present in more than 72% of new vehicles. Europe followed with 27% share, driven by regulatory compliance for ADAS and in-vehicle cybersecurity, while North America held 23% share supported by high connected-vehicle penetration exceeding 68%. The Middle East & Africa and South America together represented 9% of global demand, yet both regions posted double-digit increases in connected vehicle deployments. Across all regions, more than 65% of vehicles sold in 2025 featured multi-domain embedded software platforms, and over 58% supported over-the-air updates. The regional disparity reflects production capacity, regulatory frameworks, digital readiness, and consumer preference for connected mobility solutions.

How is digital vehicle intelligence reshaping enterprise mobility ecosystems?

North America held approximately 23% of the global Vehicle Embedded Software market in 2025, supported by strong demand from passenger vehicles, electric vehicle manufacturers, and commercial fleet operators. Over 70% of newly registered vehicles in the region integrate ADAS and connected infotainment software. Key demand drivers include automotive, logistics, and ride-sharing platforms that deploy real-time diagnostics and predictive maintenance systems. Regulatory initiatives focused on vehicle cybersecurity, functional safety, and emission monitoring are accelerating secure software adoption. Centralized domain controllers and AI-based perception software are increasingly deployed across next-generation vehicle architectures. A leading U.S.-based automotive technology company expanded its embedded AI software stack across electric platforms, improving vehicle data processing efficiency by 26%. Regional consumer behavior shows strong preference for connected dashboards, navigation, and driver monitoring systems, with over 62% of buyers prioritizing digital features when selecting new vehicles.

How are compliance-driven innovations redefining intelligent vehicle platforms?

Europe accounted for nearly 27% of global market demand in 2025, with Germany, the UK, and France contributing over 68% of regional deployments. Regulatory mandates on functional safety, cybersecurity, and emission compliance are shaping software integration strategies. More than 60% of new vehicles now include embedded safety and telematics software compliant with EU vehicle data and safety standards. Electric and autonomous vehicle programs are accelerating the adoption of real-time operating systems and AI-based driver assistance platforms. A leading German automotive supplier expanded zonal computing solutions, reducing ECU counts by 32% across next-generation vehicle platforms. Regional consumer behavior is compliance-driven, with fleet operators and manufacturers prioritizing explainable and secure embedded software to meet regulatory and sustainability requirements.

What is driving mass-scale digital vehicle transformation across manufacturing hubs?

Asia-Pacific led the market in volume with 41% share in 2025, driven by China, Japan, and India, which together produced over 38 million vehicles equipped with embedded software systems. Manufacturing automation, smart factories, and large EV production clusters are accelerating software integration across powertrain, infotainment, and ADAS platforms. Over 65% of vehicles in China now include connected infotainment and telematics software. Japan leads in automotive AI research, while India shows rapid adoption of digital cockpits and navigation systems. A major Chinese EV manufacturer deployed AI-based embedded diagnostics, reducing system failure rates by 30%. Regional consumer behavior is tech-driven, with high adoption of connected features and mobile-integrated vehicle applications.

How are digital vehicle platforms supporting regional mobility modernization?

South America represented approximately 5% of global demand in 2025, led by Brazil and Argentina. Growing automotive manufacturing, logistics fleets, and smart transportation initiatives are increasing embedded software adoption. Over 48% of newly produced vehicles in Brazil now integrate telematics and navigation software. Government incentives supporting electric and connected vehicles are encouraging OEM investments. A regional automotive software integrator partnered with fleet operators to deploy predictive maintenance systems, reducing vehicle downtime by 21%. Consumer behavior in this region is tied to localized infotainment and language-supported navigation systems, with over 44% of buyers preferring vehicles with digital dashboards.

How is smart mobility enabling digital transformation across emerging transport sectors?

The Middle East & Africa accounted for nearly 4% of global demand in 2025, led by the UAE and South Africa. Growth is supported by smart city programs, logistics digitization, and public transport modernization. Over 40% of new commercial vehicles in the UAE now deploy embedded telematics and fleet management software. Government initiatives supporting connected transport infrastructure are accelerating adoption. A regional mobility solutions provider implemented AI-enabled vehicle monitoring platforms, improving fleet efficiency by 24%. Consumer behavior shows rising demand for connected navigation and safety systems, particularly within urban commercial fleets.

• China – 26%: High vehicle production capacity and large-scale integration of embedded software across EV and connected platforms.

• United States – 18%: Strong demand for connected, autonomous-ready vehicles supported by advanced automotive software ecosystems.

The Vehicle Embedded Software market is characterized by a moderately fragmented competitive structure, with more than 150 active global and regional solution providers operating across operating systems, middleware, real-time platforms, and application-layer software. The top five companies collectively account for approximately 54% of total deployments, indicating gradual consolidation around large automotive software ecosystems. Competition is driven by rapid innovation in AI-based control systems, centralized computing architectures, and over-the-air update platforms. More than 40 strategic partnerships and joint development agreements were announced between 2023 and 2025 to accelerate autonomous, connected, and electric vehicle software platforms. Product innovation cycles have shortened by nearly 30%, while software integration timelines have improved by 25% through reusable code libraries and adaptive operating systems.

Tier-1 automotive suppliers and semiconductor-backed software firms are expanding vertically by integrating hardware abstraction layers, cybersecurity modules, and cloud connectivity into unified platforms. Over 60% of leading players have launched centralized domain controller software stacks, and more than 45% are actively investing in AI-enabled perception and predictive diagnostics solutions. Merger and acquisition activity has increased by 18%, reflecting the race to secure intellectual property and scalable software architectures. Open-source frameworks and standardized middleware are also intensifying price and feature competition, compelling vendors to differentiate through safety certifications, real-time performance optimization, and long-term software lifecycle management.

Bosch

Continental

NVIDIA

Aptiv

Denso

NXP Semiconductors

Infineon Technologies

Renesas Electronics

Qualcomm Technologies

BlackBerry QNX

The Vehicle Embedded Software Market is being reshaped by rapid advancements in centralized computing, artificial intelligence, real-time operating systems, and secure connectivity frameworks. Modern vehicles now integrate an average of 80–120 electronic control units, generating over 25 GB of data per hour, which has accelerated the shift toward domain and zonal architectures. These platforms reduce ECU counts by up to 35% and improve in-vehicle data processing efficiency by 28%, enabling faster response times for safety-critical functions. Real-time operating systems supporting deterministic performance now manage more than 70% of ADAS and powertrain control tasks, ensuring sub-millisecond latency for braking, steering, and battery management systems.

AI-driven embedded software is increasingly deployed for sensor fusion, object recognition, predictive maintenance, and driver monitoring. Machine learning algorithms have improved perception accuracy by 32% and reduced false alerts by 21%, enabling higher reliability in semi-autonomous driving environments. In electric vehicles, embedded battery management software enhanced with AI delivers up to 22% improvement in energy utilization and extends battery life cycles by approximately 18%.

Over-the-air update platforms are now integrated into more than 60% of connected vehicles, enabling remote patching, cybersecurity upgrades, and feature enhancements without physical recalls. Secure boot, encryption, and intrusion detection systems have increased threat detection capability by 45%, while reducing vulnerability exposure by 30% across connected vehicle networks.

Middleware platforms supporting AUTOSAR Adaptive and POSIX-compliant environments are improving cross-domain interoperability, reducing integration time by 25% and accelerating software reuse by 40%. Together, these technologies are transforming vehicles into software-defined platforms, positioning embedded software as the core enabler of intelligent, connected, and autonomous mobility systems.

• In January 2025, NXP Semiconductors agreed to acquire Austria-based TTTech Auto for USD 625 million, strengthening its automotive embedded software portfolio by integrating safety-focused middleware that enhances operating system-to-application connectivity without disrupting critical functions.

• In June 2025, Volvo and Daimler Truck launched a joint venture named Coretura to develop a dedicated vehicle software manufacturing platform for digitized commercial vehicles, commencing operations with around 50 employees and targeting its first software releases by the end of the decade. (Wall Street Journal)

• In September 2025, Qualcomm and BMW introduced the Snapdragon Ride Pilot hands-free driving system, built on Snapdragon Ride system-on-chips and jointly developed software for Level 2+ autonomous driving, validated for use in over 60 countries and planned for expansion to more than 100 by 2026. (The Verge)

• In May 2025, Tata Elxsi partnered with Mercedes-Benz Research and Development India to advance vehicle software engineering and software-defined vehicle (SDV) development, boosting Tata Elxsi’s automotive software capabilities and contributing to a 2.5% stock increase on the Bombay Stock Exchange. (The Economic Times)

The Vehicle Embedded Software Market Report covers a comprehensive analysis of technologies, segments, and regional adoption patterns within automotive software ecosystems. It includes detailed segmentation by software types such as real-time operating systems, middleware, application software, and firmware utilities, outlining their deployment across various vehicle functions including ADAS, infotainment, telematics, powertrain control, and body electronics platforms. The report also assesses regional consumption patterns, documenting volumes and integration trends in Asia Pacific, Europe, North America, South America, and Middle East & Africa, highlighting variations in embedded system requirements and digital mobility priorities.

Market technologies covered range from centralized domain computing platforms and zonal architectures to AI-enabled perception, predictive diagnostics, and secure over-the-air update frameworks. The report evaluates emerging trends including AI-driven embedded control, 5G and V2X connectivity, secure software stacks, and cloud-to-vehicle integration models. Industry focus areas such as compliance with safety standards, cybersecurity requirements, and software lifecycle management practices are examined across automotive OEMs, Tier-1 suppliers, and software integrators.

In addition to core passenger vehicle applications, the report incorporates commercial vehicle, fleet services, and mobility operator use cases, analyzing end-user behavior and software adoption drivers. It also explores niche segments like EV battery management systems, autonomous driving PILOT stacks, and personalized digital cockpit experiences. Forward-looking insights include technology roadmaps, strategic partnerships, and innovation hotspots, offering decision-makers a detailed view of competitive positioning and opportunity landscapes in the Vehicle Embedded Software ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bosch, Continental, NVIDIA, Aptiv, Denso, NXP Semiconductors, Infineon Technologies, Renesas Electronics, Qualcomm Technologies, BlackBerry QNX |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |