Reports

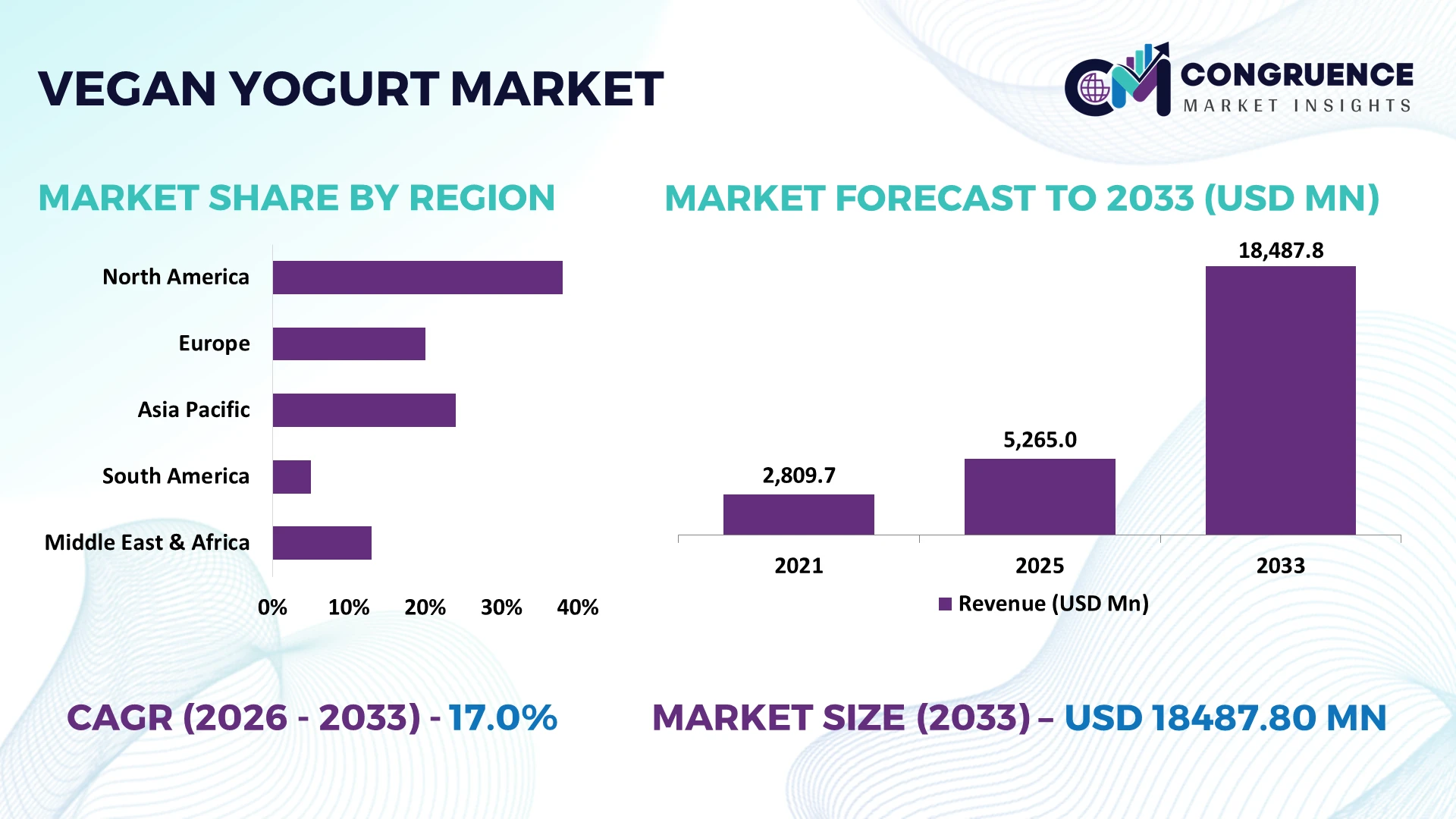

The Global Vegan Yogurt Market was valued at USD 5265 Million in 2025 and is anticipated to reach a value of USD 18487.8 Million by 2033 expanding at a CAGR of 17% between 2026 and 2033. Growth is being driven by advances in plant-based fermentation, expanded oat and almond protein processing, cleaner ingredient formulations, and wider retail distribution supported by dairy-alternative manufacturing investments.

Germany remains a dominant production and consumption hub, accounting for approximately 24% of Europe's plant-based yogurt manufacturing capacity, supported by large-scale food processing investments and advanced fermentation technologies. Compared with France, Germany records nearly 18% higher private-label vegan yogurt penetration, while EU sustainability policies and ingredient traceability standards continue accelerating innovation and manufacturing efficiency across regional supply chains in 2026.

Businesses should prioritize scalable fermentation capabilities, diversified plant-protein sourcing, and region-specific product portfolios to strengthen competitive positioning in high-growth vegan yogurt markets.

Market Size & Growth: USD 5265 Million (2025) to USD 18487.8 Million (2033) at 17% CAGR, driven by advanced plant-based fermentation and expanding dairy-free retail networks.

Top Growth Drivers: Fermentation efficiency +21%, clean-label preference +34%, retail shelf expansion +19% across premium food categories.

Short-Term Forecast: By 2028, production costs decline about 12% through automation, ingredient optimization, and improved manufacturing yields.

Emerging Technologies: AI-assisted formulation, precision fermentation, and enzyme optimization improve product consistency by nearly 18% across advanced manufacturing facilities.

Regional Leaders: Europe exceeds USD 6.8 Billion, North America USD 5.4 Billion, Asia-Pacific USD 4.9 Billion, supported by rapid retail expansion and localized production.

Consumer Trends: Around 42% of frequent plant-based consumers purchase vegan yogurt regularly, with protein-enriched varieties gaining stronger repeat demand.

Pilot Example: In 2026, automated fermentation deployment improved batch consistency by 16% while reducing production waste by 11% in commercial facilities.

Competitive Landscape: Leading manufacturers collectively control approximately 38% market share, alongside Danone, Oatly, Forager Project, Kite Hill, and Alpro.

Regulatory & ESG Impact: Sustainable packaging initiatives reduce virgin plastic usage by nearly 20%, supported by evolving environmental compliance requirements.

Investment & Funding: More than USD 1.2 Billion supports facility expansion, strategic partnerships, ingredient innovation, and resilient regional supply chains.

Innovation & Future Outlook: High-protein formulations, probiotic innovation, and precision ingredient development strengthen premium positioning and accelerate global product diversification.

Increasing demand from retail grocery chains, foodservice operators, and health-focused consumers is accelerating product diversification across oat, coconut, soy, and almond formulations. Advanced fermentation techniques and improved probiotic stability enhance taste and nutritional performance, while approximately 28% of new product launches emphasize high-protein positioning. In 2026, regional ingredient sourcing strategies strengthened supply-chain resilience, setting the foundation for the strategic market assessment that follows.

The Vegan Yogurt Market has become strategically important as food manufacturers compete through ingredient innovation, localized production, and premium nutritional positioning rather than product availability alone. Supply-chain restructuring is encouraging companies to source oats, almonds, and legumes closer to manufacturing sites, reducing transportation exposure while improving production continuity. This transition strengthens resilience against agricultural volatility and supports faster product commercialization in high-demand retail channels.

Advanced precision fermentation and AI-assisted formulation reduce formulation cycles by approximately 22% compared with conventional product development while lowering pilot-scale ingredient waste by nearly 15%. Germany continues expanding industrial-scale fermentation capacity, whereas Japan focuses on functional probiotic innovation and premium formulations with higher value-added differentiation. Over the next two to three years, automated quality monitoring is expected to exceed 45% deployment among large-scale manufacturers, improving production consistency and accelerating new product launches.

A leading deployment trend involves integrating digital quality analytics with continuous fermentation systems to maintain stable probiotic performance across production batches. Companies are expanding partnerships with plant-protein suppliers, investing in regional manufacturing facilities, and strengthening research collaborations to improve ingredient functionality and operational efficiency. Organizations establishing integrated sourcing, advanced processing capabilities, and differentiated nutritional portfolios will secure stronger competitive positioning as the vegan yogurt industry evolves toward higher-value production.

Rapid advances in plant-protein processing and fermentation technologies are strengthening product quality while improving manufacturing efficiency across the vegan yogurt industry. Fermentation optimization has increased culture stability by approximately 18%, while high-protein formulations have improved consumer acceptance by nearly 24%. In Canada, investments in oat-processing infrastructure and localized ingredient sourcing are reducing import dependence and improving supply reliability. These improvements enable manufacturers to launch premium formulations with cleaner ingredient labels and enhanced nutritional profiles. Companies are responding through expanded processing facilities, strategic partnerships with ingredient suppliers, and investments in proprietary cultures that improve taste, texture, and shelf stability. The strategic advantage increasingly depends on vertically integrated production rather than price-based competition alone.

Price fluctuations in almonds, coconuts, and specialty oat ingredients continue challenging cost management and production planning. Ingredient procurement costs have fluctuated by approximately 16%, while climate-related agricultural variability has affected harvest consistency by nearly 12% in key producing countries. Australia and California have experienced periodic water-related constraints that directly influence raw material availability for processors. These pressures reduce manufacturing flexibility, compress margins, and complicate long-term procurement planning for premium formulations. Companies are mitigating exposure by diversifying supplier networks, expanding local sourcing programs, adopting multi-ingredient recipes, and negotiating longer-term procurement contracts. Businesses with resilient sourcing strategies maintain stronger production continuity and greater pricing stability during supply disruptions.

Functional vegan yogurt featuring probiotics, protein enrichment, and micronutrient fortification is creating differentiated growth opportunities beyond conventional dairy alternatives. Approximately 31% of new product launches emphasize digestive health benefits, while AI-assisted formulation shortens product development timelines by nearly 20%. South Korea is encouraging innovation through advanced food biotechnology initiatives supporting next-generation plant-based nutrition. Manufacturers are increasing investment in precision fermentation, customized cultures, and sustainable ingredient processing while collaborating with biotechnology firms to accelerate commercialization. An emerging strategic opportunity lies in developing personalized nutrition products using digital consumer insights, allowing companies to strengthen premium positioning and improve customer retention across health-focused consumer segments.

Maintaining consistent texture, flavor, and probiotic performance across expanding production volumes remains a significant execution challenge for vegan yogurt manufacturers. Batch-to-batch quality deviations can increase processing adjustments by approximately 14%, while advanced production systems require nearly 25% higher technical workforce capability than conventional dairy processing. In the United States, manufacturers face increasing operational pressure to modernize quality-control infrastructure while complying with evolving plant-based labeling requirements. Companies must strengthen automation, digital process monitoring, workforce training, and advanced fermentation control systems to ensure manufacturing consistency. Organizations investing early in intelligent production infrastructure and specialized technical expertise will achieve stronger operational resilience and long-term competitive differentiation.

• Precision Fermentation Expands Production Advanced fermentation platforms are improving culture stability by approximately 19% while reducing formulation cycles by nearly 21%. Manufacturers in Germany are integrating automated process controls to standardize probiotic performance across facilities. Higher production consistency lowers batch losses and accelerates commercial launches, prompting companies to expand biotechnology partnerships and modernize fermentation infrastructure in response to stricter ingredient quality expectations.

• Localized Ingredient Networks Strengthen Supply-chain restructuring is shifting procurement toward domestic oat, almond, and legume suppliers, reducing transportation dependence by around 17% and shortening replenishment cycles by approximately 14%. Canada and the Nordic countries are increasing regional processing capacity following agricultural resilience initiatives. Companies are restructuring supplier portfolios and investing in multi-source procurement models to improve production continuity and inventory flexibility.

• Functional Nutrition Premiumization Accelerates High-protein and probiotic-enriched formulations now represent nearly 32% of premium product launches, while clean-label recipes have expanded by approximately 24%. Food manufacturers are integrating nutritional science with digital consumer analytics to refine formulations. This transition improves premium product positioning, strengthens repeat purchases, and encourages investment in specialized ingredient technologies and research collaborations.

• Smart Manufacturing Optimizes Operations AI-enabled production monitoring and automated quality inspection have improved manufacturing efficiency by approximately 18% while reducing quality deviations by nearly 13%. Japan is accelerating digital factory deployment to address skilled labor constraints and operational precision. Companies are investing in intelligent production systems, predictive maintenance, and connected manufacturing platforms that improve scalability while maintaining consistent product quality across expanding production volumes.

Soy-Based Yogurt remains the leading segment with an estimated 37% market share due to established processing infrastructure, reliable protein content, and competitive production economics. Its mature supply chain enables consistent large-scale manufacturing, making it the preferred choice for both retail brands and private-label producers. Almond-Based Yogurt continues to attract premium consumers seeking clean-label formulations, while Coconut-Based Yogurt maintains strong demand in dairy-free indulgence products through its naturally creamy texture.

Oat-Based Yogurt is the fastest-growing segment, supported by increasing investment in oat-processing technologies and improved fermentation techniques that have increased product acceptance by approximately 23%. Cashew-Based Yogurt continues expanding within premium and artisanal categories where differentiation outweighs production scale. Manufacturers are broadening product portfolios, strengthening ingredient partnerships, and investing in formulation innovation to balance cost efficiency with nutritional performance, reflecting a clear shift toward diversified plant-protein strategies.

Retail Consumption leads the Vegan Yogurt Market with approximately 56% share, supported by supermarket expansion, wider product assortments, and growing availability of premium plant-based offerings. Improved cold-chain logistics and digital inventory systems have increased shelf availability by nearly 18%, strengthening purchasing consistency. Bakery & Desserts remain an established application where vegan yogurt improves texture and moisture retention, while Frozen Desserts continue gaining attention through innovative dairy-free formulations.

Smoothies & Beverages represent the fastest-growing application, supported by increasing demand for convenient nutritional products and expanded ready-to-drink production capacity. Foodservice operators are integrating vegan yogurt into breakfast menus and healthy meal offerings, improving menu flexibility and operational efficiency. Companies are expanding production lines, introducing application-specific formulations, and strengthening partnerships with foodservice distributors to address evolving consumption patterns and diversify commercial demand.

Households remain the dominant end-user segment with an estimated 61% share, supported by frequent grocery purchases, expanding product availability, and increasing preference for plant-based nutrition. Improved packaging formats and shelf-life optimization have increased repeat purchasing by approximately 17%. Restaurants and Cafés continue expanding vegan menu offerings to address changing consumer expectations, while Hotels increasingly incorporate dairy-free breakfast alternatives into premium hospitality services.

Food Manufacturers represent the fastest-growing end-user group as demand rises for vegan yogurt as an ingredient in desserts, beverages, and functional foods. Production integration has improved manufacturing flexibility by approximately 20%, encouraging greater investment in specialized formulations and contract manufacturing. Companies are responding through customized ingredient solutions, long-term commercial partnerships, and dedicated production capacity that supports both branded and industrial customers while strengthening competitive differentiation.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 19.2% CAGR between 2026 and 2033.

Advanced Manufacturing and Retail Integration Strengthen Market Leadership

North America maintains its leadership through mature plant-based food manufacturing, strong cold-chain infrastructure, and extensive retail distribution networks. The region contributes approximately 36% of global vegan yogurt demand, supported by advanced fermentation capabilities and high consumer acceptance of dairy alternatives. Nearly 48% of premium product launches emphasize functional nutrition, while automated quality monitoring has improved production efficiency by around 17%. Companies continue expanding localized ingredient sourcing, investing in processing automation, and strengthening partnerships with retailers to improve inventory responsiveness. Enterprise investment increasingly targets premium formulations with enhanced protein profiles and probiotic stability, enabling manufacturers to optimize production consistency while responding quickly to changing consumer preferences.

United States Market Outlook: The United States leads regional production through large-scale manufacturing infrastructure, extensive retail penetration, and advanced food biotechnology capabilities. More than 60% of regional commercial production capacity is concentrated within the country, supported by investments in automated processing, digital quality management, and ingredient innovation. Major food manufacturers continue expanding plant-based product portfolios while strengthening partnerships with domestic oat and almond suppliers to improve supply resilience and manufacturing flexibility.

Sustainability Policies Drive Industrial Innovation

Europe remains a highly competitive vegan yogurt manufacturing hub supported by sustainability initiatives, advanced food processing technologies, and strict ingredient quality standards. The region accounts for approximately 31% of global market activity, with manufacturers integrating renewable processing technologies and recyclable packaging solutions. Facility modernization has improved production efficiency by nearly 15%, while localized sourcing programs continue reducing logistics complexity. Food producers are prioritizing clean-label formulations, precision fermentation, and environmentally responsible packaging to strengthen competitive differentiation. Regulatory alignment across major markets continues encouraging investments in advanced processing infrastructure and product innovation.

Germany Market Outlook: Germany represents the region's strongest production center due to its established food manufacturing ecosystem, biotechnology expertise, and extensive private-label manufacturing capabilities. Approximately 24% of Europe's plant-based yogurt manufacturing capacity is located in Germany, supported by continuous investment in fermentation technologies and ingredient traceability systems. Manufacturers continue expanding regional production facilities to improve operational efficiency and accelerate commercialization of premium plant-based products.

Manufacturing Scale and Urban Demand Accelerate Expansion

Asia-Pacific is experiencing rapid expansion through increasing investment in food processing infrastructure, urban retail development, and localized plant-based manufacturing. The region contributes nearly 24% of global market activity, with production facilities expanding to support rising demand for dairy alternatives. Manufacturing automation has improved production throughput by approximately 20%, while digital retail platforms continue accelerating premium product accessibility. Companies are strengthening regional partnerships with ingredient processors and expanding localized production to improve cost efficiency, shorten distribution timelines, and support country-specific product customization.

China Market Outlook: China leads regional expansion through large-scale food manufacturing capacity, advanced processing investment, and rapid commercialization of plant-based nutrition products. Industrial modernization initiatives have increased automated production deployment by approximately 22%, enabling manufacturers to improve quality consistency and production flexibility. Domestic enterprises continue investing in fermentation technologies and integrated supply chains to strengthen competitiveness across both domestic and export-oriented markets.

Agricultural Strength Supports Market Development

South America is leveraging abundant agricultural resources and expanding food manufacturing capabilities to strengthen its vegan yogurt industry. The region represents approximately 6% of global demand, with investments increasingly directed toward localized processing and value-added plant-based foods. Processing efficiency has improved by nearly 14% through equipment modernization, while regional partnerships are enhancing ingredient availability. Infrastructure limitations remain in cold-chain distribution, prompting manufacturers to prioritize localized production, strategic logistics partnerships, and flexible distribution models that improve operational resilience and market accessibility.

Brazil Market Outlook: Brazil serves as the region's primary production and consumption hub due to its diversified agricultural base, expanding food processing industry, and growing investment in plant-based nutrition. Approximately 45% of regional manufacturing capacity is concentrated in Brazil, supported by improved soybean and oat supply networks. Food manufacturers continue expanding production facilities and developing premium dairy-free product lines tailored to evolving consumer preferences.

Food Infrastructure Modernization Expands Commercial Potential

The Middle East & Africa market is developing through food manufacturing modernization, retail expansion, and investment in premium nutrition products. The region contributes approximately 3% of global market activity, while organized retail distribution continues improving product availability across major urban centers. Modern food processing facilities have increased operational efficiency by around 13%, supported by strategic partnerships and upgraded cold-chain infrastructure. Manufacturers are expanding local packaging operations and strengthening regional distribution capabilities to improve supply reliability while reducing import dependency for finished products.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional commercialization through advanced retail infrastructure, strong food import logistics, and growing investment in premium plant-based food production. Modern processing and distribution facilities support rapid product availability, while approximately 18% of newly introduced premium dairy-alternative products are manufactured or packaged locally. Companies continue investing in regional partnerships, automated packaging technologies, and specialized distribution networks to strengthen long-term market competitiveness.

The Vegan Yogurt Market features intense competition between Danone, Alpro, Oatly, Kite Hill, and Forager Project, while regional manufacturers challenge multinational brands through localized formulations and pricing flexibility. The top five players collectively control approximately 46% of the market, reflecting moderate consolidation with strong premium brand influence. Competition centers on formulation technology, ingredient sourcing, manufacturing scale, and distribution reach rather than price alone. Advanced fermentation improves production efficiency by nearly 18%, while localized procurement reduces logistics costs by around 14% and automated quality systems lower production deviations by approximately 12%. Companies are expanding regional manufacturing, securing plant-protein supply agreements, introducing functional probiotic products, and vertically integrating ingredient processing to strengthen operational resilience. Competitive dynamics increasingly favor technology-driven product differentiation over conventional flavor expansion. High capital requirements for specialized fermentation infrastructure and stable plant-protein sourcing create significant entry barriers. Winning requires scalable production, resilient supply networks, continuous formulation innovation, premium nutritional positioning, and rapid commercialization across diverse retail and foodservice channels.

Danone

Alpro

Oatly

Kite Hill

Forager Project

COYO Pty Ltd

The Coconut Collaborative

Nancy's Probiotic Foods

Chobani

Yeo Valley Organic

Lavva

Nush Foods

So Delicious Dairy Free

Current technology investment is centered on precision fermentation, automated process control, and advanced plant-protein extraction to improve product consistency and manufacturing efficiency. Precision fermentation enhances probiotic stability by approximately 19%, while automated quality monitoring reduces batch variation by nearly 15%. Around 44% of large-scale manufacturers are integrating AI-supported formulation platforms that shorten development cycles and optimize ingredient combinations. These technologies strengthen production reliability, accelerate product launches, and improve premium product differentiation in competitive retail environments.

Emerging technologies include enzyme-assisted protein modification, digital twin production systems, and intelligent fermentation analytics. Compared with conventional formulation methods, AI-assisted development reduces formulation time by nearly 22% while lowering pilot-scale ingredient waste by approximately 16%. Smart sensors continuously monitor microbial activity and fermentation parameters, enabling predictive process adjustments that improve operational performance. Large multinational manufacturers benefit most because integrated digital infrastructure supports rapid deployment across multiple production facilities while regional companies selectively adopt modular automation.

Between 2026 and 2028, continuous fermentation platforms, robotic packaging systems, and machine-learning quality optimization will become strategic differentiators. Automated manufacturing deployment is expected to exceed 50% among leading producers, improving throughput, reducing operating costs, and strengthening supply-chain responsiveness. Companies investing early in intelligent manufacturing, digital process integration, and next-generation fermentation capabilities will secure stronger operational resilience, faster commercialization, and sustainable competitive advantage as product complexity and quality expectations continue rising.

February 2024 Danone completed the conversion of its Villecomtal-sur-Arros facility in France from conventional dairy yogurt production to a dedicated Alpro plant-based manufacturing site, strengthening oat-based product capacity and supporting a market where around 25% of French consumers identify as flexitarians. Business impact: increased dedicated plant-based production capability.

December 2025 Danone North America entered a multi-year partnership with the Big Ten Conference, expanding the reach of its Silk plant-based portfolio across collegiate sports. The initiative targets more than 14,000 student-athletes and 580,000 students, strengthening brand visibility and consumer engagement.

April 2026 Danone Japan introduced refreshed packaging across its Alpro plant-based portfolio, following the 2025 launch of its three-plant blend range. Consumer research cited in the announcement found 51% purchase interest among surveyed women, supporting stronger retail visibility and brand differentiation.

March 2026 Danone Germany partnered with Dunkin' Germany to expand the availability of Alpro Barista plant-based beverages across coffee outlets, accelerating foodservice penetration. The collaboration broadened commercial distribution while reinforcing premium plant-based consumption in out-of-home channels.

The report provides comprehensive coverage of the Vegan Yogurt Market across major product types, applications, end-user categories, and key geographical markets. It evaluates Soy-Based, Almond-Based, Coconut-Based, Oat-Based, and Cashew-Based yogurt segments while assessing demand across retail consumption, foodservice, bakery and desserts, smoothies and beverages, and frozen desserts. The study also analyzes purchasing behavior among households, restaurants, cafés, hotels, and food manufacturers, supported by operational trends, deployment patterns, and competitive benchmarking across more than 10 leading industry participants.

The assessment examines regional manufacturing capabilities, supply-chain evolution, product innovation, precision fermentation, automated quality control, and advanced plant-protein processing technologies shaping market development between 2026 and 2033. Strategic analysis includes investment priorities, production localization, sustainability initiatives, partnership activity, competitive positioning, and emerging niche opportunities. The report is designed to support expansion planning, portfolio optimization, risk assessment, market entry evaluation, and long-term decision-making through actionable intelligence aligned with evolving consumer preferences and industrial transformation.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 5265 Million |

Market Revenue in 2033 | USD 18487.8 Million |

CAGR (2026 - 2033) | 17% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Danone, Alpro, Oatly, Kite Hill, Forager Project, COYO Pty Ltd, The Coconut Collaborative, Nancy's Probiotic Foods, Chobani, Yeo Valley Organic, Lavva, Nush Foods, So Delicious Dairy Free |

Customization & Pricing | Available on Request (10% Customization is Free) |