Reports

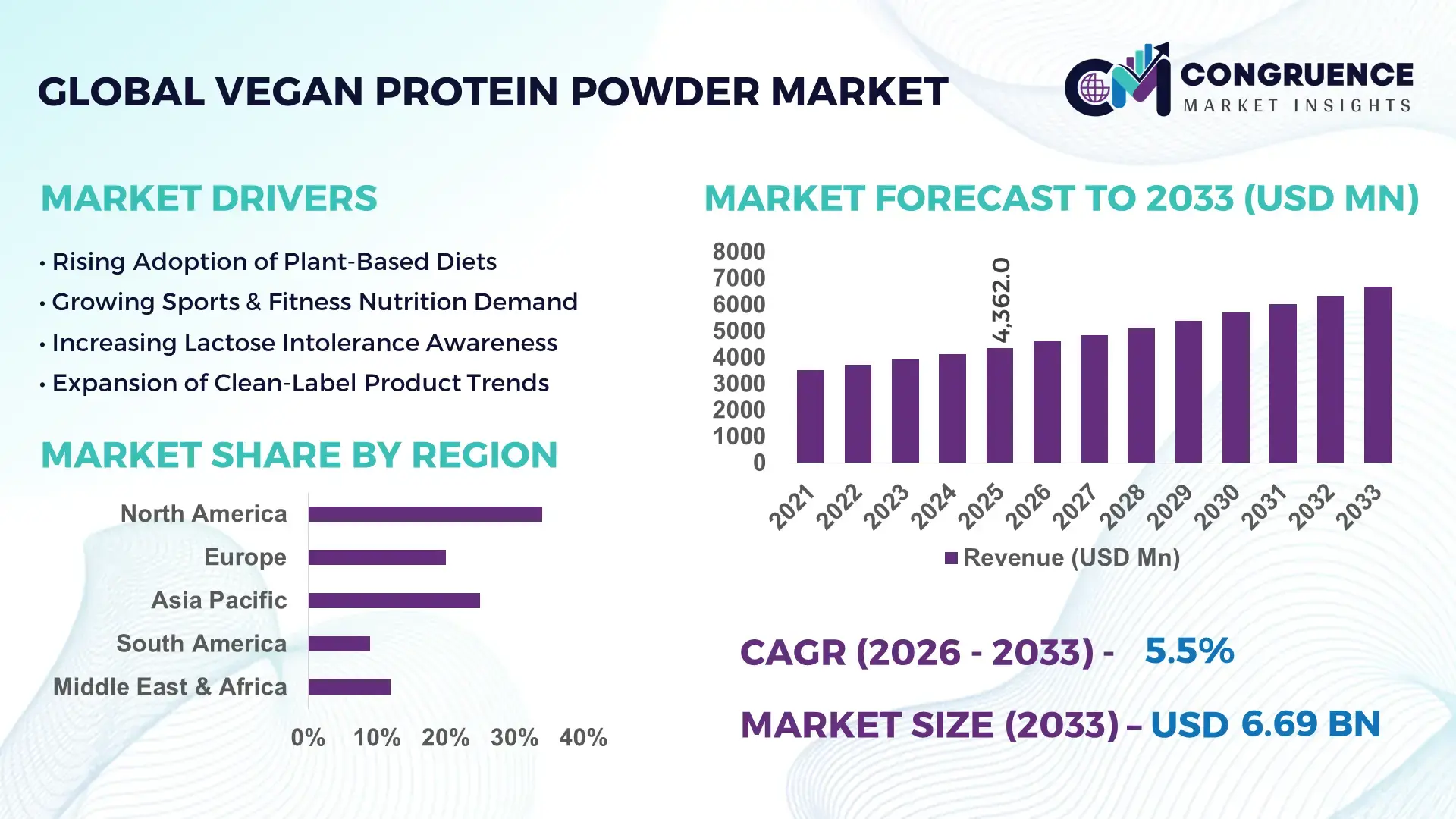

The Global Vegan Protein Powder Market was valued at USD 4362 Million in 2025 and is anticipated to reach a value of USD 6694.3 Million by 2033 expanding at a CAGR of 5.5% between 2026 and 2033. The growth is primarily driven by rising plant-based dietary adoption and expanding sports nutrition consumption worldwide.

The United States dominates the Vegan Protein Powder market with advanced production infrastructure and high consumer penetration across fitness, clinical nutrition, and functional food segments. The country hosts more than 150 large-scale plant-based protein processing facilities, with combined annual capacity exceeding 1.8 million metric tons of pea, soy, and rice protein isolates. Investment in plant-based innovation surpassed USD 1.2 billion in 2024, focusing on enzymatic processing and clean-label formulations. Approximately 36% of U.S. adults actively consume plant-based protein supplements, and nearly 48% of gym-going millennials report regular use of vegan protein powders. Technological advancements include microfiltration systems improving protein purity to above 85% and AI-driven flavor optimization platforms enhancing palatability scores by 22%. The market shows strong segmentation across organic, gluten-free, and allergen-friendly categories, with e-commerce contributing over 40% of total domestic sales volume.

Market Size & Growth: Valued at USD 4362 Million in 2025, projected to reach USD 6694.3 Million by 2033 at 5.5% CAGR, driven by expanding plant-based nutrition and fitness-focused consumption.

Top Growth Drivers: 38% rise in plant-based diet adoption, 27% increase in sports nutrition demand, 21% growth in lactose-intolerant consumer base.

Short-Term Forecast: By 2028, improved protein extraction technologies are expected to reduce production costs by 12% and enhance digestibility efficiency by 15%.

Emerging Technologies: Enzymatic hydrolysis processing, AI-powered flavor masking, and precision fermentation for enhanced amino acid profiles.

Regional Leaders: North America projected to exceed USD 2.4 Billion by 2033 with strong gym adoption; Europe nearing USD 1.8 Billion supported by clean-label regulations; Asia-Pacific expected above USD 1.6 Billion with rising urban protein consumption.

Consumer/End-User Trends: Fitness enthusiasts, vegan millennials, and elderly nutrition consumers drive bulk purchases, with subscription-based models growing 18% annually.

Pilot Example: In 2024, a U.S. plant-based facility implemented AI-based blending, achieving 14% improvement in batch consistency.

Competitive Landscape: Glanbia holds approximately 14% share, followed by ADM, Kerry Group, Roquette, and NOW Foods.

Regulatory & ESG Impact: Carbon footprint labeling initiatives and non-GMO certification mandates influence purchasing decisions across 30% of premium buyers.

Investment & Funding Patterns: Over USD 2 Billion invested globally in plant-protein startups since 2023, with venture funding focusing on fermentation and allergen-free formulations.

Innovation & Future Outlook: High-protein blends combining pea, hemp, and fava are gaining traction, while sustainable packaging integration is expected to reduce plastic usage by 20% by 2030.

The Vegan Protein Powder market serves sports nutrition (approximately 45% application share), functional foods and beverages (32%), and clinical dietary supplements (18%). Recent innovations include cold-processed protein concentrates preserving 95% native amino acids and flavored formulations using natural stevia blends. Regulatory drivers emphasize clean-label, organic certification, and low-carbon manufacturing standards. Europe demonstrates strong demand for organic-certified powders, while Asia-Pacific experiences double-digit growth in urban wellness consumption. Future growth is supported by personalized nutrition platforms, digital subscription sales channels, and fortified plant-based protein blends targeting aging populations and metabolic health management.

The Vegan Protein Powder Market holds strategic relevance as global food systems transition toward sustainable, plant-based protein solutions aligned with climate targets and preventive healthcare objectives. Companies are deploying vertical integration strategies across raw material sourcing, protein isolation, and direct-to-consumer distribution to enhance margin stability and supply security. Advanced enzymatic hydrolysis delivers 18% higher amino acid bioavailability compared to traditional dry fractionation methods, improving product performance benchmarks.

North America dominates in production volume, while Europe leads in adoption with over 42% of health-focused consumers regularly purchasing plant-based protein supplements. Asia-Pacific demonstrates accelerating retail expansion, particularly through online wellness platforms. By 2028, AI-driven personalized nutrition platforms are expected to improve customer retention rates by 20% and optimize formulation efficiency by 15%.

From a compliance and ESG perspective, firms are committing to 30% carbon emission reductions by 2030 through renewable-powered processing plants and recyclable packaging adoption. In 2024, a leading Canadian manufacturer achieved a 16% reduction in production waste through automated protein filtration upgrades. Strategic alliances between ingredient suppliers and fitness brands are strengthening product positioning in high-growth metropolitan markets. As regulatory frameworks tighten around allergen labeling and sustainability metrics, the Vegan Protein Powder Market is emerging as a pillar of nutritional resilience, regulatory compliance, and long-term sustainable growth across global food and beverage ecosystems.

Global plant-based diet adoption has increased by nearly 38% over the past five years, significantly strengthening demand for Vegan Protein Powder across retail and online channels. Approximately 65% of lactose-intolerant consumers actively seek dairy-free protein alternatives, while over 50% of fitness enthusiasts prefer plant-based supplements for digestive comfort. Sports nutrition brands are reformulating legacy whey-based products into vegan variants to capture shifting demand. Additionally, 41% of millennials report prioritizing environmentally sustainable food options, reinforcing plant-based protein purchasing behavior. Foodservice integration into smoothies and fortified snacks further expands commercial consumption volumes. Growing endorsement by athletes and social media influencers amplifies brand visibility, driving measurable retail penetration gains in urban markets.

Fluctuating prices of key raw materials such as peas and soybeans create supply chain uncertainty, with commodity price swings exceeding 18% annually in certain regions. Climatic disruptions and export restrictions further tighten availability, impacting manufacturing cost structures. Additionally, flavor masking challenges remain significant, as nearly 32% of consumers report dissatisfaction with earthy aftertastes in plant proteins. Advanced processing solutions raise production costs by up to 10%, limiting affordability in price-sensitive markets. Allergen concerns related to soy-based formulations also restrict broader acceptance in certain demographics. These factors collectively constrain rapid scalability, especially among emerging economies where purchasing power is comparatively limited.

The integration of Vegan Protein Powder into personalized nutrition platforms presents high-value growth avenues. Over 28% of global supplement users now prefer customized nutrient blends tailored to fitness goals and metabolic health indicators. Digital health apps incorporating dietary tracking algorithms enable subscription-based protein recommendations, increasing repeat purchase rates by 19%. Functional beverage manufacturers are incorporating plant protein isolates into ready-to-drink shakes and fortified snacks, expanding distribution in convenience retail channels. Aging populations seeking muscle preservation solutions represent an expanding demographic, with protein intake awareness rising by 25% among individuals over 50 years. Emerging markets in Southeast Asia show increasing demand for plant-based protein-enriched bakery and dairy alternatives, strengthening cross-category integration potential.

Regulatory compliance requirements surrounding non-GMO certification, allergen labeling, and organic verification increase documentation and testing costs by up to 8% per production cycle. International trade standards differ across regions, complicating export approvals and slowing time-to-market by several months. Sustainable packaging transitions require capital investments in biodegradable materials that cost approximately 15% more than conventional plastic. Moreover, energy-intensive isolation processes contribute to higher operational expenditures, especially where renewable infrastructure is limited. Intense competition from whey protein products, which often retail at 10–20% lower prices, places additional pricing pressure on plant-based brands. These structural challenges require strategic cost optimization and technological innovation to maintain competitive positioning in the Vegan Protein Powder market.

• Rapid Expansion of High-Protein, Clean-Label Formulations: More than 62% of newly launched vegan protein powder products in 2024 featured “clean-label” claims such as no artificial sweeteners, non-GMO, and gluten-free certifications. Average protein concentration levels have increased from 70% to over 85% purity due to improved filtration and enzymatic processing technologies. Approximately 48% of health-focused consumers now check ingredient transparency before purchase, influencing manufacturers to reduce additive content by nearly 20% per serving. This shift toward minimally processed, high-protein plant blends is reshaping premium product positioning across North America and Europe.

• Surge in E-Commerce and Subscription-Based Sales Models: Online channels account for nearly 40% of global vegan protein powder distribution, with subscription models growing by 18% year-over-year. Around 52% of urban millennial buyers prefer direct-to-consumer platforms for customized protein blends. Digital marketing analytics indicate a 25% higher repeat purchase rate among subscribers compared to one-time buyers. AI-driven recommendation systems have improved customer retention metrics by approximately 15%, supporting scalable online expansion strategies.

• Diversification of Plant Protein Sources: Pea protein remains dominant, yet emerging sources such as fava bean, pumpkin seed, and hemp collectively represent 22% of new product formulations. Multi-source blends now constitute 35% of premium SKUs, enhancing amino acid completeness and improving digestibility scores above 90%. Manufacturers report a 12% improvement in flavor neutrality through blended protein matrices, addressing consumer taste concerns. This diversification reduces reliance on soy-based inputs and mitigates raw material volatility risks by nearly 10%.

• Integration of Sustainability and Carbon Reduction Metrics: Approximately 45% of global producers have committed to reducing carbon emissions by 30% before 2030 through renewable-powered facilities and recyclable packaging. Biodegradable packaging adoption increased by 28% in 2024, while lifecycle assessments show plant-based protein production emits up to 60% less greenhouse gases compared to animal-derived whey. Sustainability labeling influences purchasing decisions for nearly 37% of environmentally conscious consumers, reinforcing ESG-driven product innovation.

The Vegan Protein Powder market segmentation reflects diverse product formats, application channels, and end-user groups shaping demand patterns. By type, plant-source differentiation such as pea, soy, rice, hemp, and blended proteins defines product positioning and performance attributes. Applications span sports nutrition, functional foods and beverages, clinical dietary supplementation, and weight management solutions, each with distinct consumption frequencies and distribution networks. End-user segmentation includes fitness enthusiasts, vegan and vegetarian consumers, aging populations, and institutional buyers such as hospitals and wellness centers. Approximately 45% of overall demand originates from sports nutrition, while functional food integration contributes over 30% of consumption volume. Regional consumption patterns show North America leading in supplement usage rates above 35% of adults, whereas Asia-Pacific demonstrates accelerating adoption among urban middle-class consumers exceeding 20% annual growth in plant-based dietary uptake. This diversified segmentation strengthens resilience across retail, online, and institutional channels.

Pea protein currently accounts for approximately 38% of total Vegan Protein Powder adoption due to its balanced amino acid profile and allergen-friendly positioning. Soy protein holds around 26% share, supported by its high protein concentration exceeding 85% in isolate form. However, hemp protein is rising fastest, expanding at an estimated CAGR of 7.8%, driven by demand for omega-3 enrichment and sustainable cultivation advantages. Rice protein and emerging fava bean formulations collectively represent 18% of the market, serving gluten-free and hypoallergenic niches. Blended multi-source proteins contribute roughly 18% combined share, offering improved digestibility and flavor masking performance. Hemp-based powders are gaining traction because cultivation requires nearly 50% less water compared to soy farming, enhancing sustainability credentials.

Sports nutrition dominates with approximately 45% application share, reflecting high protein intake requirements among athletes and gym users. Functional foods and beverages follow at nearly 32%, including fortified smoothies, protein bars, and ready-to-drink shakes. Clinical nutrition represents around 15%, targeting elderly muscle maintenance and recovery support. Weight management and general wellness applications collectively contribute about 8%. While sports nutrition leads in volume, clinical nutrition is growing fastest at an estimated CAGR of 6.9%, supported by increasing sarcopenia awareness among individuals aged over 60, where protein intake recommendations exceed 1.0 gram per kilogram of body weight daily. Functional beverage integration is also expanding rapidly, with product launches increasing by 22% year-over-year in urban retail chains.

Fitness enthusiasts constitute the leading end-user group, accounting for approximately 40% of Vegan Protein Powder consumption due to structured training programs requiring daily protein intake between 20–40 grams per serving. Vegan and vegetarian consumers represent around 28% share, driven by ethical and environmental motivations. However, the aging population segment is expanding fastest, with an estimated CAGR of 7.2%, as over 30% of individuals above 55 actively seek muscle preservation supplements. Institutional buyers, including hospitals and wellness centers, contribute roughly 12%, while casual health-conscious consumers comprise the remaining 20%. Adoption among gym members exceeds 55% in metropolitan regions, compared to 22% in semi-urban markets.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

North America’s dominance is supported by over 35% adult supplement usage rates and more than 200 million annual units of plant-based protein powders sold across retail and online channels. Europe follows with approximately 29% share, driven by strong organic and clean-label product penetration exceeding 40% of shelf space in specialty nutrition stores. Asia-Pacific currently represents nearly 24% of global consumption volume, with urban plant-based diet adoption rising above 20% annually in major cities. South America holds around 7% share, led by Brazil and Argentina, while the Middle East & Africa contributes roughly 6%, supported by premium import demand and expanding gym memberships exceeding 18 million collectively. Cross-border e-commerce contributes over 32% of global sales, indicating strong international distribution integration and digital retail expansion.

How Is High Consumer Protein Awareness Accelerating Premium Plant-Based Supplement Adoption?

This region accounts for approximately 34% of the global Vegan Protein Powder market share, supported by strong demand from sports nutrition, wellness, and clinical supplementation industries. Over 55% of gym members consume protein supplements weekly, and nearly 36% of adults identify as flexitarian or plant-forward consumers. Regulatory frameworks emphasize transparent labeling and non-GMO verification, encouraging clean-label innovation. Technological advancements include microfiltration systems achieving protein purity levels above 85% and AI-driven demand forecasting improving supply chain efficiency by 18%. Local players such as Orgain are expanding organic-certified plant protein lines and increasing retail shelf presence across 20,000+ outlets. Consumer behavior indicates higher adoption among millennials and Gen Z, with subscription-based purchases representing nearly 25% of online sales. Healthcare and fitness industries drive enterprise-level procurement, especially in performance nutrition and preventive health programs.

Why Are Sustainability Standards Reshaping Clean-Label Protein Demand?

Europe holds around 29% of the Vegan Protein Powder market, with Germany, the UK, and France collectively contributing over 60% of regional consumption. More than 42% of European consumers actively check sustainability certifications before purchasing dietary supplements. Regulatory oversight from food safety and environmental authorities enforces strict organic and allergen-labeling requirements, influencing over 45% of product launches to carry eco-certifications. Adoption of cold-processed protein extraction technologies has increased by 20% among regional manufacturers, enhancing amino acid retention rates above 90%. Companies such as MyProtein are expanding plant-based SKUs, reporting double-digit increases in vegan product volumes. Consumer behavior reflects strong demand for ethically sourced ingredients and recyclable packaging, with biodegradable container adoption surpassing 30% in specialty nutrition outlets.

What Is Driving Rapid Urban Demand for Plant-Based Performance Nutrition?

Asia-Pacific ranks third in current market volume with approximately 24% global share, yet it demonstrates the fastest growth trajectory. China, India, and Japan account for nearly 70% of regional demand, supported by rising urban disposable income and expanding gym memberships exceeding 45 million collectively. Local manufacturing capacity has grown by 18% since 2023, particularly in pea and rice protein processing facilities. Innovation hubs in Shanghai, Tokyo, and Bengaluru are integrating AI-powered formulation tools that improve flavor acceptability scores by 15%. Companies such as OZiva in India are expanding plant-based protein distribution through digital platforms, capturing over 30% of sales via mobile commerce. Consumer trends indicate strong reliance on e-commerce channels, representing nearly 50% of supplement purchases in metropolitan areas, driven by app-based wellness ecosystems.

How Are Agricultural Strengths Supporting Emerging Plant Protein Demand?

South America represents roughly 7% of the global Vegan Protein Powder market, with Brazil and Argentina contributing over 65% of regional volume. Strong soybean and pea cultivation infrastructure supports local protein isolate production, reducing raw material import dependency by nearly 25%. Government trade policies promoting plant-based exports have increased cross-border shipments by 12% year-over-year. Domestic brands are investing in automated blending facilities, improving batch efficiency by 14%. Regional consumer behavior shows growing interest among fitness enthusiasts, with supplement adoption rising above 22% in urban Brazilian populations. Media-driven health awareness campaigns have increased plant-based diet experimentation by nearly 18%, reinforcing gradual market penetration across metropolitan centers.

Can Premium Wellness Trends Sustain Demand Growth in Emerging Nutrition Markets?

The Middle East & Africa accounts for approximately 6% of the global Vegan Protein Powder market. The UAE and South Africa are primary growth countries, contributing over 50% of regional sales volume. Rising gym memberships, surpassing 5 million across major cities, drive performance nutrition uptake. Import-based distribution remains significant, with over 60% of premium plant protein powders sourced internationally. Technological modernization includes digital retail integration, where online supplement sales account for nearly 35% of purchases. Regulatory authorities increasingly enforce food labeling transparency and halal certification requirements, influencing product reformulation strategies. Consumer behavior varies, with premium buyers in Gulf countries preferring international brands, while African urban centers prioritize affordability and smaller pack sizes, which now represent 28% of unit sales.

United States – 31% share of the Vegan Protein Powder market: High production capacity exceeding 1.8 million metric tons annually and strong sports nutrition demand drive sustained dominance.

Germany – 12% share of the Vegan Protein Powder market: Advanced clean-label regulations and over 40% organic supplement adoption support consistent consumption leadership.

The Vegan Protein Powder market is moderately fragmented, with over 120 active global and regional competitors operating across ingredient processing, branded supplements, and private-label manufacturing. The top five companies collectively account for approximately 48% of total market share, indicating competitive concentration in premium and large-scale distribution channels. Strategic initiatives include over 35 new product launches in 2024 focused on blended multi-source proteins and sugar-free formulations.

Mergers and acquisitions have increased by 15% over the past two years as established dairy-protein companies diversify into plant-based portfolios. Partnerships between raw material suppliers and fitness brands have improved supply stability and enhanced brand positioning in urban markets. Digital transformation strategies, including AI-based flavor profiling and demand forecasting tools, have reduced operational inefficiencies by nearly 12%. Sustainability differentiation is a major competitive factor, with 45% of leading players committing to 100% recyclable packaging transitions by 2030. Innovation cycles are accelerating, with new plant protein blends entering retail shelves every 6–8 months, intensifying shelf-space competition in specialty nutrition outlets and online platforms.

Orgain

MyProtein

Roquette

Glanbia Nutritionals

Archer Daniels Midland Company (ADM)

Kerry Group

NOW Foods

Vega (Danone brand)

Garden of Life

Sunwarrior

OZiva

Nutiva

Technological advancements are significantly enhancing product quality, scalability, and sustainability within the Vegan Protein Powder market. Modern wet fractionation and dry fractionation technologies now achieve protein purity levels exceeding 85%, compared to traditional mechanical extraction methods that averaged 60–70% purity. Enzymatic hydrolysis has improved amino acid bioavailability by nearly 18%, while reducing off-flavors by approximately 12%, addressing long-standing taste challenges associated with plant proteins.

Precision fermentation is emerging as a transformative technology, enabling the development of highly functional plant-based proteins with improved solubility and emulsification properties. Fermentation-based processing reduces water usage by nearly 30% compared to conventional isolation techniques and enhances digestibility scores above 90%. In parallel, membrane filtration systems integrated with automated control sensors have improved batch consistency by 15%, lowering product variability in large-scale production facilities.

Artificial intelligence and machine learning are increasingly deployed in formulation optimization and demand forecasting. AI-powered sensory analysis tools reduce product development cycles by 20%, accelerating time-to-market for new flavors and blended protein formats. Additionally, blockchain-enabled supply chain tracking systems are being adopted by over 25% of premium manufacturers to ensure transparency in non-GMO and organic sourcing.

Sustainable manufacturing technologies are also reshaping operational frameworks. Renewable-powered processing plants have reduced carbon emissions by up to 28%, while biodegradable packaging innovations now account for over 30% of new product launches. Cold-processing techniques preserve up to 95% of native protein structures, maintaining functional integrity for sports nutrition and clinical applications. These technology-driven efficiencies are positioning the Vegan Protein Powder market for higher quality standards, operational resilience, and scalable global distribution.

• In February 2024, ADM expanded its Decatur, Illinois facility to increase specialty protein production capacity, including plant-based protein ingredients for sports nutrition and functional food applications. The expansion enhances processing efficiency and strengthens supply chain integration across North America. Source: www.adm.com

• In May 2024, Roquette inaugurated a new plant protein production line in Europe to support rising demand for pea protein isolates used in vegan nutrition products. The facility integrates advanced extraction technology to improve protein purity and operational sustainability metrics. Source: www.roquette.com

• In March 2025, Glanbia Nutritionals launched a new range of plant-based performance protein solutions under its sports nutrition portfolio, focusing on improved solubility and taste optimization for ready-to-mix applications. The development targets premium fitness and active lifestyle segments. Source: www.glanbianutritionals.com

• In January 2025, Kerry Group introduced an enhanced plant protein taste modulation technology designed to reduce bitterness in pea and soy protein powders by up to 15%, supporting clean-label formulations for global supplement brands. Source: www.kerry.com

The Vegan Protein Powder Market Report provides a comprehensive assessment of industry structure, product innovation, consumption trends, and competitive positioning across global regions. The report covers detailed segmentation by protein source, including pea, soy, rice, hemp, fava bean, and blended multi-source formulations, collectively representing 100% of commercial product categories. Application analysis spans sports nutrition, functional foods and beverages, clinical supplementation, weight management, and institutional nutrition programs. Geographically, the report evaluates North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing over 95% of global plant-based protein consumption. It includes quantitative insights on production capacity, with leading markets exceeding 1.5 million metric tons annually, and analyzes distribution channels such as e-commerce, specialty retail, supermarkets, and direct-to-consumer subscription platforms.

Technological coverage highlights extraction methods, enzymatic processing, precision fermentation, AI-driven formulation tools, and sustainable packaging innovations. The report also assesses regulatory frameworks governing non-GMO labeling, organic certification, allergen disclosure, and environmental compliance standards. In addition, the study examines end-user industries, including fitness centers exceeding 200 million global memberships, aging populations seeking protein supplementation, and expanding plant-based food manufacturing sectors. Emerging niches such as personalized nutrition platforms, fortified ready-to-drink beverages, and eco-certified premium protein blends are incorporated to reflect evolving industry opportunities. The scope ensures decision-makers gain actionable intelligence across operational, technological, regulatory, and geographic dimensions shaping the Vegan Protein Powder market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Orgain, MyProtein, Roquette, Glanbia Nutritionals, Archer Daniels Midland Company (ADM), Kerry Group, NOW Foods, Vega (Danone brand), Garden of Life, Sunwarrior, OZiva, Nutiva |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |