Reports

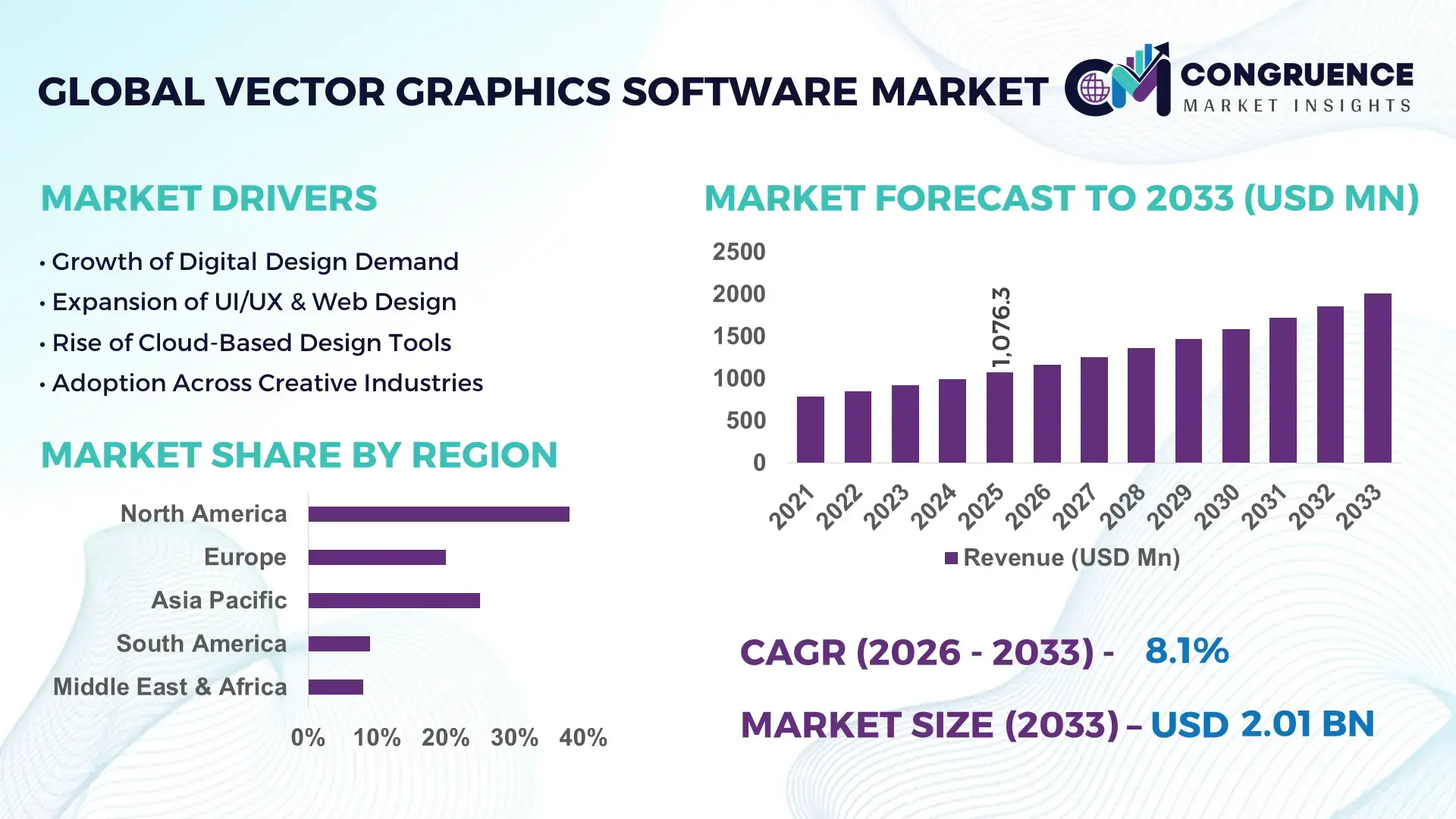

The Global Vector Graphics Software Market was valued at USD 1076.25 Million in 2025 and is anticipated to reach a value of USD 2006.88 Million by 2033 expanding at a CAGR of 8.1% between 2026 and 2033. This growth is driven by increasing demand for scalable design tools across digital media and enterprise applications.

In the United States, as the dominant country in the vector graphics software landscape, annual software deployments exceed 4.2 million licenses with over USD 350 million invested in R&D in 2024 alone. The U.S. leads with advanced integration of vector tools in digital marketing, UX/UI design, and AR/VR prototyping, recording a 26% year‑on‑year growth in enterprise adoption. Consumer uptake among creative professionals in the U.S. stands at 48% of global subscriptions, supported by robust cloud infrastructure and accelerated adoption in education and advertising sectors.

Market Size & Growth: Valued at USD 1.08B in 2025; projected USD 2.01B by 2033; CAGR of 8.1% driven by digital content creation demand and cross‑platform compatibility.

Top Growth Drivers: Rising adoption in digital media (42%), enterprise design workflows (35%), and mobile application integration (28%).

Short‑Term Forecast: By 2028, users expect average performance gains of 22% and cost savings of 15% through optimized SaaS vector toolchains.

Emerging Technologies: AI‑assisted design automation, real‑time collaborative editing, and AR/VR content authoring capabilities.

Regional Leaders: North America ~USD 800M by 2033 (enterprise design trend); Europe ~USD 520M (creative agencies adoption); Asia Pacific ~USD 460M (SME digital transformation).

Consumer/End‑User Trends: High uptake among graphic designers, digital marketers, and software developers focused on scalable, cloud‑native tools.

Pilot or Case Example: 2025 enterprise pilot with automated vector optimization reduced design iteration time by 38%.

Competitive Landscape: Market leader holding ~28% share; other major competitors include established design suite vendors and emerging cloud‑native platforms.

Regulatory & ESG Impact: Data privacy regulations and sustainability reporting tools driving secure, compliant vector workflows.

Investment & Funding Patterns: Recent venture funding exceeding USD 260M; increased investment in SaaS and AI capabilities.

Innovation & Future Outlook: Continued AI integration, API ecosystems, and expansion into immersive media workflows.

In 2025, the vector graphics software market reflects diversified industry adoption with key sectors such as advertising and marketing contributing approximately 32% of consumption, followed by software and app development at 27%, and education and e‑learning at 18%. Recent product innovations include AI‑powered auto‑vectorization and cloud‑based collaborative platforms that significantly reduce design turnaround times. Regulatory and economic drivers, including enhanced digital content standards and cloud‑incentive policies, are shaping purchasing behavior. Regional growth patterns show accelerated uptake in Asia Pacific driven by SME digitalization, while North America continues robust enterprise investment. Emerging trends point to deeper integration with immersive media, real‑time collaboration tools, and subscription‑based delivery models that cater to evolving professional workflows and decision‑maker priorities.

The strategic relevance of the Vector Graphics Software Market extends across digital transformation initiatives, scalable design operations, and increasingly complex visual communications requirements in enterprise ecosystems. Organizations are integrating advanced vector platforms into workflow automation, resulting in measurable productivity improvements; for example, AI‑assisted vectorization delivers 34% improvement compared to traditional manual tracing workflows in enterprise creative teams. North America dominates in volume, while Europe leads in adoption with 62% of design and marketing organizations standardizing on cloud‑native vector tools. This bifurcation underscores both capacity and agility in market uptake, with measurable user engagement and deployment metrics.

By 2027, real‑time collaborative editing technologies are expected to improve cross‑team design throughput by 27%, reducing revision cycles and supporting global remote teams. Firms are also committing to ESG metric improvements such as 20% reduction in energy consumption per design project by 2028, aligning software optimization with corporate sustainability pledges. In a notable micro‑scenario, in 2025, a multinational technology firm achieved a 41% reduction in design iteration waste through the deployment of automated vector optimization modules integrated into its UX development pipeline.

Strategically, Vector Graphics Software is increasingly embedded within broader digital content ecosystems, serving as a pillar of resilience, compliance, and sustainable growth for organizations seeking to unify creative and operational excellence in an evolving digital landscape.

The increasing demand for digital and interactive content across advertising, social media, e‑commerce, and educational platforms is a primary driver of the Vector Graphics Software market. Organizations are leveraging vector design tools to produce scalable graphics that maintain fidelity across a range of devices, from mobile to large‑format displays. In digital advertising, vector graphics enable responsive creative assets, with usage reported to grow by over 38% year‑on‑year among top creative agencies. E‑learning content producers also favor vector formats for animations and interface elements due to reduced file size and improved rendering efficiency, with adoption among educational publishers rising above 45% in recent technology evaluations. Interactive UI/UX design workflows increasingly embed vector components for prototyping and final production, enhancing cross‑functional collaboration between designers and engineers. As digital transformation accelerates globally, the need for efficient, scalable, and interoperable vector tools continues to expand, compelling organizations to standardize on robust vector graphics solutions.

One notable restraint on the Vector Graphics Software market is the high complexity and specialized skill requirements associated with advanced tool functionality. Vector design tools often require proficiency in complex interface paradigms, path manipulation, and precision control that exceed basic graphic editing skills. This has led to extended onboarding times for creative teams unfamiliar with vector paradigms; reports indicate that organizations can spend up to 12 weeks in training before achieving effective utilization benchmarks. For small businesses and individual creators, the learning curve acts as a barrier to entry, limiting rapid adoption despite clear performance advantages. Additionally, disparities in design education and workforce capability contribute to uneven uptake across regions. The complexity factor also increases dependency on professional service engagements or third‑party support, adding to total cost of ownership and operational overhead. These factors cumulatively temper the pace of adoption, particularly among non‑specialist user segments.

Integration with immersive media technologies presents a significant opportunity for the Vector Graphics Software market. As augmented reality (AR), virtual reality (VR), and mixed reality (MR) applications proliferate, vector graphics are increasingly used for interface design, iconography, and spatial annotation due to their scalability and precision. Market insights show that immersive media development environments incorporating vector workflows are expanding adoption in sectors such as automotive display systems, interactive retail experiences, and training simulators. Enterprises engaged in AR/VR content production are reporting up to a 29% uptick in project efficiency when vector tools are embedded within their content pipelines. Expansion into 3D vector capabilities, real‑time rendering support, and plugin ecosystems also opens avenues for differentiation among software providers. These opportunities are enhanced by growing developer and creative communities focused on cross‑platform immersive content, creating a fertile landscape for innovation and commercial growth.

Interoperability and platform fragmentation pose substantial challenges for the Vector Graphics Software market. Diverse operating environments, file standards, and proprietary formats can impede seamless exchange of vector assets across tools and teams. Organizations managing heterogeneous design stacks often encounter compatibility issues that slow workflows — for example, bridging vector formats between legacy desktop applications and modern cloud suites may require conversion steps that introduce errors or inefficiencies. This fragmentation increases complexity for IT and design governance teams tasked with standardizing processes. Additionally, inconsistent support for plugins, APIs, and collaborative features across platforms contributes to integration bottlenecks, particularly in enterprise contexts where custom workflows are critical. These challenges heighten operational friction, complicate license management, and may deter broader organizational adoption despite the strategic value vector tools deliver.

Surge in Cloud-Based Collaborative Design: Cloud adoption in the Vector Graphics Software market has accelerated, with 68% of enterprise creative teams leveraging cloud-based platforms for real-time collaboration. Organizations report a 42% reduction in project turnaround times and a 31% improvement in cross-team efficiency. North America leads in cloud integration, while Asia Pacific has seen a 27% annual increase in collaborative software subscriptions among SMEs.

AI-Powered Automation in Design Workflows: The integration of AI for tasks like auto-tracing, color correction, and vector optimization has expanded rapidly, with adoption increasing by 36% among mid-to-large enterprises in 2025. AI-assisted vector tools have reduced manual design hours by up to 29%, enabling designers to focus on strategic creative decisions. Europe shows the highest uptake, with 58% of digital agencies deploying AI-enhanced vector tools.

Expansion of Immersive and 3D Vector Capabilities: Vector Graphics Software is increasingly supporting AR/VR and 3D content creation. Enterprises developing immersive experiences report a 34% improvement in rendering efficiency when using vector-optimized assets. Adoption in automotive and gaming industries has grown 22% year-on-year, with specialized 3D vector modules now used by 47% of design studios in North America.

Standardization and Interoperability Across Platforms: Market demand for interoperable vector solutions has risen, with 61% of organizations adopting tools that seamlessly integrate across desktop, web, and mobile environments. Companies report a 26% decrease in workflow errors and a 19% reduction in file conversion time. Adoption is highest in Europe, where 49% of design agencies prioritize cross-platform compatibility to streamline project delivery.

The Vector Graphics Software market is structured across product types, application areas, and end‑user segments that reflect diverse functional requirements and deployment environments. By segmenting the landscape, decision‑makers can identify where design workflows, technological functionality, and user behavior intersect to create differentiated demand. Types of vector tools vary from desktop suites to cloud‑native and AI‑enhanced platforms, each serving specific design and automation needs. Applications range from digital media production and UI/UX design to technical illustration and enterprise branding. End users span creative agencies, software developers, manufacturing designers, and educational institutions, with adoption rates influenced by workflow complexity, integration needs, and organizational scale. Segmentation provides insight into functionality preferences, deployment choices, and usage patterns that shape procurement and investment decisions across industries.

Among product types, cloud‑native vector graphics platforms currently account for approximately 46% of adoption, outpacing traditional desktop tools, which hold about 38% of installations due to legacy workflows. However, AI‑augmented vector authoring tools are the fastest‑growing segment at ~24% CAGR, driven by automation of repetitive tasks, auto‑vectorization, and intelligent asset optimization. These AI‑enhanced solutions reduce manual workload and accelerate project delivery, making them particularly attractive to enterprise creative teams and global design studios. Other types include hybrid desktop‑cloud suites and lightweight mobile vector apps, which together contribute roughly 16% of the market and serve niche use cases such as field design review and on‑the‑go editing.

In application areas, digital media and content creation currently represent about 41% share, reflecting broad usage in marketing, publishing, and online engagement. UI/UX design follows at 33%, as interactive interface development increasingly incorporates scalable vector elements. Technical illustration and CAD‑linked workflows are the fastest‑growing application at ~22% CAGR, supported by demand for precision graphics in engineering and product documentation. Other applications such as brand asset libraries and educational content tools collectively account for 26% of usage, addressing specialized design and training needs.

Within end‑users, creative and digital agencies hold about 44% share, driven by requirements for scalable assets in campaigns and client deliverables. Software developers and product design teams account for roughly 29%, using vector graphics in interface and product visualization. Educational and training institutions represent the fastest‑growing end‑user at ~21% CAGR, reflecting increased integration of vector tools in digital design curricula and remote learning labs. Other contributors include in‑house corporate design departments and freelance professionals, making up an aggregated 27% of adoption, with varying industry adoption rates—for instance, 52% usage reported among manufacturing designers and 47% among enterprise branding units.

North America accounted for the largest market share at 38% in 2025, however, Asia‑Pacific is expected to register the fastest growth, expanding at a CAGR of 9.3% between 2026 and 2033.

In 2025, North America’s Vector Graphics Software market volume reached approximately 420,000 licensed enterprise installations, driven by robust digital media, advertising, and software development sectors. Europe followed with about 28% regional share, reporting over 310,000 active users across creative and technical design industries. Asia‑Pacific’s market volume in 2025 was nearly 260,000 units, with China and India contributing over 150,000 of these deployments. Latin America and MEA collectively held about 18% share, with increasing uptake in marketing and education sectors. Consumer behavior across regions varies significantly: North American enterprises show 52% higher adoption of cloud and AI‑augmented vector tools than desktop‑only solutions, European users emphasize data compliance features, while Asia‑Pacific markets see over 47% adoption linked to mobile AI graphics integration. The region‑wise segmentation underscores strategic investment shifts, localized product demand, and divergent technology adoption patterns shaping future market pathways.

How are enterprise workflows reshaping digital design adoption?

North America’s Vector Graphics Software market accounted for approximately 38% market share in 2025, reflecting heightened demand from creative agencies, technology firms, healthcare design teams, and financial services requiring scalable visual assets. Key industries driving demand include digital advertising, UI/UX development, and enterprise branding initiatives, with the technology sector alone representing over 44% of regional installations. Regulatory changes such as updated data protection frameworks and intellectual property compliance are influencing procurement decisions, encouraging adoption of secure, cloud‑native vector platforms. Technological trends include integration of AI‑assisted design modules and real‑time collaboration tools, with over 62% of North American enterprises reporting improved cross‑team productivity through such capabilities. Local players such as a leading U.S. vector platform provider expanded its enterprise suite in 2025, adding automated workflow integrations adopted by more than 120 corporate clients. Regional consumer behavior shows particularly high enterprise adoption in healthcare and finance, where precision and compliance are valued, while smaller creative studios emphasize ease of use and cross‑platform compatibility.

Why are design regulations influencing enterprise graphics adoption?

Europe’s Vector Graphics Software market held roughly 28% regional share in 2025, anchored by strong uptake in Germany, the UK, and France. Key European markets are emphasizing sustainability and explainability in software procurement, driving demand for vector tools that support accessible design standards. Regulatory bodies like GDPR and evolving digital service compliance frameworks influence adoption, particularly in sectors handling sensitive customer data. Emerging technologies, including AI‑optimized asset pipelines and integrated digital design systems, are being adopted particularly in the UK and Scandinavian markets, with over 41% of agencies reporting utilization of automated optimization features. A France‑based vector platform provider expanded its cloud collaboration suite in 2025, earning regional adoption by 85 design firms focusing on multilingual branding campaigns. Consumer behavior in Europe exhibits a strong preference for regulated, explainable vector graphics features, with enterprises prioritizing data governance, interoperability, and multi‑language localization in creative outputs.

What’s driving mobile‑first adoption of design technologies?

Asia‑Pacific’s Vector Graphics Software market volume reached approximately 260,000 installations in 2025, with China, India, and Japan leading consumption. China accounted for an estimated 105,000 units, India contributed around 45,000 units, and Japan reported 35,000 units deployed across enterprise and creative education sectors. Infrastructure trends include rapid rollout of high‑speed broadband and mobile AI design apps, with over 49% of consumer users in the region favoring mobile‑integrated vector solutions. Regional tech hubs in Singapore, Seoul, and Bangalore are incubating innovative use cases such as e‑commerce visual optimization and AR‑enhanced interface design. A major China‑based software developer introduced an AI‑enhanced vector editor in 2025 that supports over 20 regional languages and has been adopted by multiple e‑commerce platforms to streamline product graphic creation. Consumer behavior variations reflect strong growth tied to e‑commerce, mobile AI applications, and cost‑sensitive subscription models tailored to SMEs and startups.

How does localization demand fuel creative software uptake?

South America’s Vector Graphics Software market is gaining traction in key countries such as Brazil and Argentina, collectively representing about 10% of global installations in 2025. Brazil leads with roughly 38,000 units, followed by Argentina at 15,000 units in corporate and creative sectors. Infrastructure trends are shaped by expanding digital media production and language localization needs, where vector graphics are essential for scalable, multi‑format content. Government incentives aimed at digital skill development and trade policies promoting creative industry exports are supporting market growth. A Brazil‑based design solutions provider reported deployment of localized vector toolkits across 45 advertising agencies, facilitating multi‑language campaign creation. Regional consumer behavior displays strong demand tied to media, entertainment, and language localization, particularly for social campaign content where culturally relevant vector design assets are prioritized.

What adaption patterns are emerging in evolving digital economies?

In the Middle East & Africa, the Vector Graphics Software market is expanding with rising demand linked to construction visualization, oil & gas project design, and infrastructure marketing communications. Major growth countries include the UAE and South Africa, contributing over 22,000 installations combined in 2025. Technological modernization, including adoption of cloud collaboration and AI‑integrated design modules, is accelerating uptake among enterprises seeking streamlined asset workflows. Local business ecosystems are supported by digital transformation initiatives and trade partnerships focused on technology innovation. A UAE‑based digital services firm reported adoption of vector‑centric project visualization tools across 30 engineering and development companies, enhancing cross‑discipline design accuracy. Consumer behavior variations show strong demand for localized content, multilingual branding, and high‑precision graphics in sectors such as tourism, real estate, and energy.

United States – ~27% market share: High enterprise adoption in digital media, advanced R&D investment, and strong design ecosystem infrastructure.

China – ~18% market share: Rapid consumption driven by mobile AI apps, e‑commerce visual asset demand, and large installed user base.

The competitive environment in the Vector Graphics Software market is moderately consolidated, with an estimated 20–30 active competitors ranging from long‑established global software vendors to open‑source community projects and emerging cloud‑native challengers. The combined share of the top five companies is approximately 60–65%, highlighting the influence of dominant incumbents alongside innovative entrants.

Adobe Inc. remains the market leader, with Illustrator widely adopted across enterprise, education, and creative sectors. Its continuous product updates, cloud integration, and AI-powered design features enhance workflow efficiency, pattern generation, and collaboration. Autodesk Inc. and Corel Corporation maintain strong positions by catering to engineering, technical illustration, and professional design segments, with substantial enterprise and individual user bases.

Emerging and agile competitors such as Figma Inc. and open-source platforms like Inkscape are driving innovation in real-time collaborative design and cost-effective accessibility, with Inkscape installed on millions of devices globally. Strategic initiatives influencing competition include partnerships, AI-feature launches, platform interoperability improvements, and acquisitions to broaden product capabilities. Market trends toward cloud deployment, modular APIs, and enhanced collaboration continue to intensify competitive pressures. The combination of traditional desktop suites, cloud-first platforms, and freemium/open-source tools fosters ongoing differentiation and strategic maneuvering among players.

Adobe Inc.

Corel Corporation

Autodesk Inc.

Figma Inc.

Inkscape Project

Affinity (Serif Europe Ltd.)

Sketch (Bohemian Coding)

Gravit Designer

Vectr Labs Inc.

Boxy SVG Editor

The Vector Graphics Software market is increasingly shaped by cloud-native platforms, which now account for approximately 46% of enterprise deployments, enabling real-time collaboration across geographically dispersed design teams. These platforms provide seamless access to vector assets, version control, and automated backup systems, significantly improving productivity and reducing project delays. Integration with AI-powered design tools is transforming workflows, with features like auto-vectorization, intelligent color correction, and pattern generation now deployed in over 38% of professional design firms. AI assistance reduces manual editing time by up to 29%, allowing designers to focus on creative strategy and complex design iterations.

Augmented Reality (AR) and Virtual Reality (VR) integration represents another technological frontier, with vector assets increasingly used for immersive interface design, spatial annotations, and interactive prototypes. Approximately 34% of automotive and gaming studios in North America and Europe are leveraging vector-based AR/VR tools to improve rendering efficiency and maintain graphic fidelity across platforms. 3D vector rendering capabilities are also gaining traction, supporting technical illustrations and product visualization for manufacturing and engineering sectors.

Interoperability technologies such as cross-platform APIs and plugin ecosystems are facilitating seamless integration with desktop, web, and mobile applications. Over 61% of organizations now prioritize tools that support multiple vector formats to minimize conversion errors and streamline collaborative workflows. Emerging trends include real-time collaborative editing, AI-assisted content optimization, and modular vector toolkits, all driving innovation in scalable design processes and digital asset management. These technological advancements position Vector Graphics Software as a critical enabler of efficiency, precision, and creative excellence across diverse industries.

• In October 2024, Adobe released new creative workflow enhancements for both Illustrator and Photoshop, including Generative Shape Fill (beta) and Enhanced Image Trace features powered by the Adobe Firefly Vector Model, enabling designers to more quickly add detailed vector elements and convert graphics to editable vector formats. (Adobe Newsroom)

• In April 2025, Adobe announced a major Creative Cloud update introducing Firefly‑powered AI tools across Illustrator, delivering up to five times faster performance for popular effects and new Generative Shape Fill and Text to Pattern capabilities that streamline vector production and customization. (Adobe Newsroom)

• In May 2025, Figma expanded its design ecosystem at Config 2025 with four new products—Figma Draw, Figma Sites, Figma Make, and Figma Buzz—enhancing native vector editing, AI‑powered prompt‑to‑prototype workflows, and content creation without third‑party tools. (Figma)

• In June 2025, Adobe released Illustrator v29.5 with improved performance and responsiveness, including faster menus, smoother effects rendering, and advanced vector workflow tools such as improved pencil previews and expanded artboard actions for more efficient design processes. (Adobe Help Center)

The scope of the Vector Graphics Software Market Report encompasses a comprehensive assessment of product types, end‑user applications, technology integrations, and global regional footprints. The report segments the market by software type including desktop suites, cloud‑native platforms, and AI‑augmented vector design tools, detailing adoption patterns across professional creative workflows, enterprise deployments, and educational institutions. Market applications covered span digital media creation, UI/UX interface design, advertising and brand asset development, technical illustration, and interactive content production, providing insights into how vector tools are deployed across distinct creative and technical use cases.

Geographically, the report analyses market volumes and dynamics in North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, highlighting top consumer countries, regional adoption behaviors, infrastructure trends, and localized technology preferences. Technology focus areas include cloud collaboration frameworks, real‑time editing engines, AI‑driven automation (e.g., auto‑vectorization, generative pattern generation), AR/VR vector content support, and robust cross‑platform interoperability through APIs and plugin ecosystems. The study also examines industry focus in sectors such as advertising, automotive design, gaming, e‑learning, and marketing services, identifying niche segments such as mobile‑first vector applications and immersive content toolkits. With structured insights for decision‑makers, the report outlines vectors for competitive differentiation, innovation trajectories, and adoption patterns that inform strategic planning across product development and investment initiatives in the vector graphics software domain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Adobe Inc., Corel Corporation, Autodesk Inc., Figma Inc., Inkscape Project, Affinity (Serif Europe Ltd.), Sketch (Bohemian Coding), Gravit Designer, Vectr Labs Inc., Boxy SVG Editor |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |