Reports

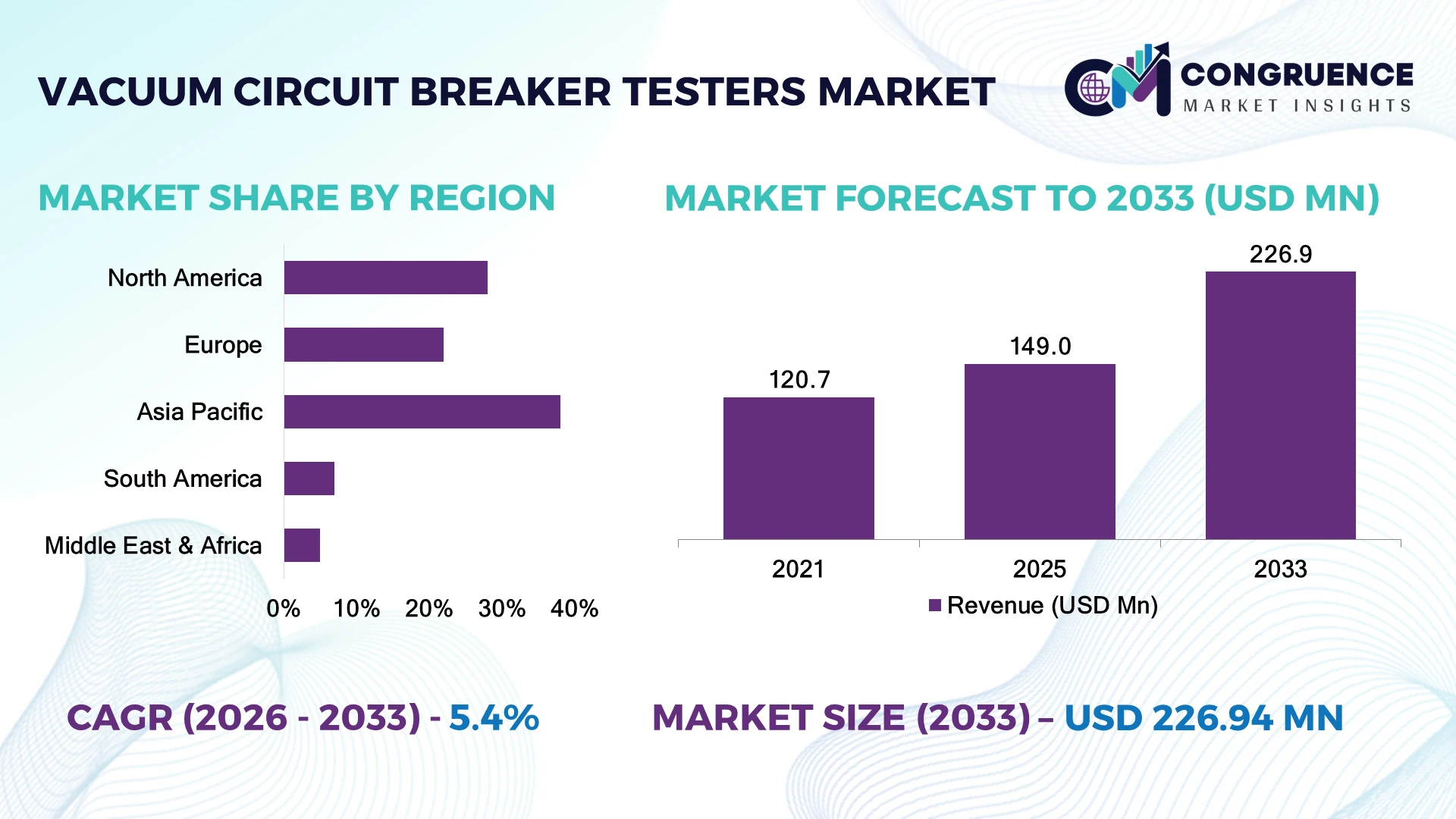

The Global Vacuum Circuit Breaker Testers Market was valued at USD 149.0 Million in 2025 and is anticipated to reach a value of USD 226.9 Million by 2033 expanding at a CAGR of 5.4% between 2026 and 2033. Growth is driven by rising grid modernization programs, increasing deployment of high-voltage switchgear testing solutions, and stricter preventive maintenance requirements across power utilities and industrial facilities.

China dominates the market with approximately 32% share, supported by large-scale power infrastructure upgrades, smart grid investments exceeding USD 100 billion annually, and rapid adoption of automated electrical testing systems across utility networks. The United States follows with nearly 24% share, driven by aging grid replacement initiatives and industrial automation. China’s annual grid expansion scale exceeds U.S. deployment levels by over 40%, creating a stronger demand base.

Strategic investment in digital testing capabilities will define competitive advantage as utilities prioritize reliability and predictive maintenance.

Market Size & Growth: Valued at USD 149.0 Million in 2025 and projected at USD 226.9 Million by 2033, with 5.4% CAGR, driven by smart grid upgrades and automated testing adoption.

Top Growth Drivers: Grid modernization (32%), industrial automation (28%), renewable power integration (22%) are the leading demand catalysts.

Short-Term Forecast: By 2028, automated diagnostic adoption is expected to improve testing efficiency by 25% and reduce maintenance downtime by 20%.

Emerging Technologies: AI-based fault detection, IoT-enabled monitoring, and advanced insulation diagnostic technologies are reshaping testing workflows.

Regional Leaders: Asia Pacific is projected at USD 105 Million with smart grid expansion; North America at USD 70 Million with aging infrastructure replacement; Europe at USD 38 Million with renewable integration projects.

Consumer/End-User Trends: More than 60% of utilities are shifting toward predictive maintenance models using digital testing platforms.

Pilot/Case Example: In 2024, utility automation projects using digital circuit testing reduced equipment inspection cycles by 30%.

Competitive Landscape: Leading players include Megger, OMICRON, DV Power, Vanguard Instruments, and BAUR, with leading manufacturers accounting for approximately 35% market share.

Regulatory & ESG Impact: Grid reliability standards and energy efficiency policies are accelerating adoption, with digital maintenance reducing unnecessary equipment replacements by nearly 15%.

Investment & Funding: More than USD 50 billion is being directed globally toward grid modernization, increasing partnerships between testing equipment providers and utilities.

Innovation & Future Outlook: Next-generation testers integrating AI analytics, cloud connectivity, and portable automation will strengthen operational resilience and competitive positioning.

The Vacuum Circuit Breaker Testers Market is witnessing increased demand from utilities, renewable energy operators, and industrial power users seeking accurate diagnostics and reduced equipment failures. Recent innovations include portable automated testers, real-time condition monitoring, and AI-supported fault analysis, with digital testing adoption rising by approximately 35% among modern utility operators. Global supply-chain restructuring and regional manufacturing expansion are improving equipment availability, supporting a transition toward smarter electrical asset management.

The Vacuum Circuit Breaker Testers Market is becoming strategically important as power infrastructure operators focus on grid reliability, asset longevity, and digital transformation. Aging electrical networks in North America and Europe, combined with rapid renewable energy integration in Asia Pacific, are accelerating investments in advanced diagnostic equipment. Global supply-chain diversification is also encouraging regional production of critical electrical testing components.

Modern automated vacuum circuit breaker testers provide faster diagnostics and higher accuracy compared with traditional manual testing systems. Digital platforms can reduce testing time by nearly 30% while improving fault identification accuracy by more than 20%, enabling utilities to shift from reactive maintenance toward predictive strategies.

Regional adoption patterns remain differentiated. Asia Pacific leads through large-scale transmission expansion and utility modernization, while North America emphasizes replacement of aging infrastructure and compliance-driven maintenance programs. In Europe, renewable power integration and grid stability initiatives are shaping demand.

Utilities are deploying portable testers at substations to minimize outage periods and improve operational efficiency. Manufacturers are strengthening partnerships with power companies and expanding digital capabilities to capture emerging opportunities. Competitive success will depend on delivering connected, intelligent testing solutions that improve reliability, reduce maintenance costs, and support the future transformation of global power networks.

Aging electrical infrastructure and expanding smart grid programs are driving demand for advanced vacuum circuit breaker testing solutions, particularly in China, the United States, and Germany. More than 35% of utility operators are shifting toward predictive maintenance models, while digital diagnostic tools improve testing efficiency by nearly 25–30% compared with conventional inspection methods. Global investments in transmission upgrades and renewable power integration are increasing the need for reliable switchgear assessment. Companies are responding by launching portable automated testers, integrating IoT-based monitoring, and forming partnerships with utilities to support faster fault detection and reduced outage risks.

High initial equipment costs, specialized component dependency, and calibration requirements limit adoption among smaller utilities and industrial users. Advanced vacuum circuit breaker testers containing precision measurement modules and digital communication systems can increase procurement costs by 20–35% compared with basic testing equipment. Supply-chain disruptions affecting electronic components and semiconductor availability have created longer delivery cycles for manufacturers. Companies operating in countries such as India and Brazil face additional challenges due to limited local service networks and skilled technicians. Manufacturers are reducing exposure through supplier diversification, localized assembly facilities, and long-term component agreements to stabilize production and improve market accessibility.

The integration of artificial intelligence, cloud analytics, and automated condition monitoring creates new opportunities for vacuum circuit breaker tester providers. AI-enabled diagnostic platforms can reduce fault analysis time by approximately 40%, while remote monitoring solutions are increasing adoption among digitally connected substations. Countries including India, South Korea, and Saudi Arabia are expanding power infrastructure investments, creating demand for advanced testing capabilities. Companies are strengthening their market position through R&D investments, software-enabled testing platforms, and partnerships with grid automation providers. A key opportunity lies in combining testing hardware with predictive analytics services, creating recurring value models beyond traditional equipment sales.

Integration complexity across diverse switchgear systems remains a major challenge for widespread deployment of advanced vacuum circuit breaker testers. Nearly 30% of industrial facilities still operate mixed-generation electrical equipment, creating compatibility issues between modern diagnostic platforms and legacy assets. Cybersecurity requirements for connected testing systems are also increasing as utilities adopt digital substations and remote monitoring solutions. Countries with rapidly expanding power networks face shortages of trained technicians capable of managing advanced testing technologies. Companies must invest in workforce training, cybersecurity frameworks, and interoperable software architectures to ensure consistent deployment, maintain operational reliability, and strengthen long-term competitiveness.

Portable Testing Expansion Utilities and industrial operators are increasingly adopting portable vacuum circuit breaker testers, with field-deployment models improving inspection flexibility by nearly 30% and reducing maintenance scheduling delays by around 20%. Mobile diagnostic workflows are replacing centralized testing approaches, especially across distributed substations in countries such as India and Australia. Manufacturers are responding by scaling lightweight designs, battery-powered systems, and ruggedized equipment platforms to support faster on-site testing.

Digital Diagnostics Integration Advanced testers are shifting toward software-driven diagnostics, with IoT connectivity, automated reporting, and predictive analytics adoption increasing by approximately 35% among digitally enabled utilities. Integration with asset management platforms is improving fault visibility and reducing manual data processing requirements by nearly 25%. Companies are expanding partnerships with automation providers to create connected testing ecosystems that support real-time maintenance decisions.

Automation-Driven Maintenance Models Power companies are moving from periodic inspection toward automated condition-based maintenance, driven by grid reliability requirements and skilled labor shortages. Automated testing workflows are reducing technician involvement by 20–30% while improving testing consistency across large infrastructure networks. Manufacturers are investing in intelligent calibration features and user-friendly interfaces to address workforce limitations and accelerate enterprise adoption.

Supply Chain Localization Shift Electrical equipment manufacturers are restructuring supply networks following global component availability pressures, with localized sourcing initiatives increasing by more than 25% in key manufacturing markets. Companies in China, Germany, and the United States are expanding regional production capabilities to improve delivery reliability and reduce dependency on imported electronic components. This shift is creating a non-obvious advantage for suppliers offering integrated hardware, software, and service support models.

Portable Vacuum Circuit Breaker Testers represent the leading type segment, accounting for approximately 55% of market demand due to their flexibility, lower installation requirements, and suitability for utility field operations. These systems enable faster testing across multiple locations and support preventive maintenance programs. Fixed/Laboratory Vacuum Circuit Breaker Testers continue to maintain demand among manufacturers and specialized testing facilities requiring high-precision validation. However, their deployment remains concentrated in controlled environments. Automated Vacuum Circuit Breaker Testers are emerging as the fastest-growing type segment, supported by increasing digitalization and demand for reduced testing time. Adoption is expanding by nearly 30% as utilities integrate automated diagnostics into maintenance workflows. Companies are prioritizing multifunction platforms, software connectivity, and portable automation features to improve testing accuracy and strengthen competitive differentiation. The shift toward intelligent testing solutions is influencing investment priorities across manufacturers.

Utility Maintenance is the dominant application segment, contributing approximately 60% of market demand due to extensive deployment of vacuum circuit breakers across transmission and distribution networks. Utilities require regular testing to improve equipment reliability, reduce outage risks, and extend asset lifecycles. Industrial Power Systems and Manufacturing Facilities represent established applications, supported by the need for uninterrupted electrical operations. Renewable Energy Infrastructure is the fastest-growing application area as solar, wind, and distributed energy projects require advanced switchgear monitoring capabilities. Adoption in renewable installations is increasing by approximately 35% as operators focus on grid stability and predictive maintenance. Data Centers are also gaining importance due to strict uptime requirements, with companies expanding automated testing integration to support critical power systems. Manufacturers are adapting through application-specific solutions, automation features, and service-based deployment models.

Electric Utilities represent the leading end-user segment, accounting for approximately 60% of market demand due to extensive grid assets, large-scale switchgear installations, and continuous maintenance requirements. Utilities require reliable testing equipment to manage aging infrastructure and improve operational resilience. Industrial Enterprises and Power Generation Companies remain important users, particularly where electrical reliability directly impacts production efficiency. Renewable Energy Operators are emerging as the fastest-growing end-user group, with adoption increasing by nearly 30% as distributed power generation expands. These operators require advanced testing solutions to maintain newly deployed electrical assets and ensure consistent performance. Infrastructure Organizations are also increasing adoption through modernization projects and public utility upgrades. Companies are targeting end-users through customized solutions, regional service partnerships, and integrated maintenance offerings to strengthen long-term customer relationships.

Asia Pacific accounted for the largest market share at 38% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

North America represented the second-largest market position in 2025, accounting for approximately 28% of global demand. The United States remains the key contributor due to aging transmission infrastructure, utility modernization programs, and increased adoption of automated electrical diagnostic systems. More than 40% of major utilities are incorporating digital asset monitoring practices to improve maintenance planning and reduce outage risks. Demand is concentrated among power utilities, industrial facilities, and infrastructure operators upgrading legacy switchgear systems. Manufacturers are strengthening partnerships with utility companies and expanding smart testing platforms to support predictive maintenance and faster field diagnostics.

United States Market Outlook: The United States leads North American adoption due to extensive power infrastructure and replacement requirements for aging electrical assets. Over 60% of utility infrastructure operators are prioritizing grid reliability improvements, increasing demand for portable and automated vacuum circuit breaker testing solutions. Domestic manufacturers and service providers are focusing on connected diagnostics, cybersecurity-ready platforms, and regional support networks.

Europe accounted for nearly 22% of global demand in 2025, supported by strict electrical safety standards, renewable energy integration, and modernization of aging power networks. Germany, France, and the United Kingdom represent major deployment centers, with utilities increasingly adopting automated testing systems to improve operational reliability. More than 35% of European grid operators are advancing digital monitoring initiatives to optimize asset performance. Regulatory focus on energy efficiency and infrastructure resilience is encouraging investment in advanced diagnostic equipment. Companies are responding through software integration, local service expansion, and partnerships with transmission operators.

Germany Market Outlook: Germany remains Europe’s most strategically significant market due to its advanced industrial base and strong power engineering ecosystem. Industrial facilities and utility operators are increasingly deploying automated testing platforms, with more than 50% of large electrical maintenance operations moving toward digital inspection workflows. Manufacturers are emphasizing precision diagnostics and integrated monitoring solutions.

Asia Pacific dominated the global vacuum circuit breaker testers market in 2025 with approximately 38% share, driven by large-scale electricity infrastructure expansion, industrial growth, and strong manufacturing capabilities. China represents the largest country market due to extensive transmission upgrades, smart grid investments, and domestic production capacity for electrical equipment. India, Japan, and South Korea are also increasing adoption through industrial electrification and renewable energy projects. More than 45% of new utility modernization projects in major Asian economies include digital monitoring and testing requirements. Companies are expanding production facilities, strengthening local partnerships, and developing cost-efficient automated testers to address large-scale demand.

China Market Outlook: China leads Asia Pacific adoption through its extensive power network, manufacturing strength, and continued grid modernization initiatives. The country accounts for more than 30% of global demand, supported by high-voltage transmission expansion and smart infrastructure deployment. Domestic manufacturers are increasing investment in automated testing technologies, localized components, and integrated diagnostic platforms to serve utility and industrial customers.

South America accounted for approximately 7% of global demand in 2025, with adoption concentrated in Brazil, Chile, and Argentina. The market is supported by transmission upgrades, renewable energy expansion, and industrial electricity requirements. Brazil represents the largest contributor due to its extensive utility network and ongoing infrastructure investments. However, limited local manufacturing capacity and dependence on imported testing equipment continue to affect deployment speed. Companies are addressing these challenges through regional service partnerships, distributor networks, and localized technical support. Increasing renewable integration is creating additional demand for reliable circuit breaker maintenance solutions.

Brazil Market Outlook: Brazil remains the leading South American market due to its large electricity network and expanding renewable energy infrastructure. Utility operators are increasing investment in maintenance technologies, with grid modernization projects supporting higher adoption of automated testing equipment. Companies are focusing on partnerships with regional utilities and service providers to improve equipment availability and technical coverage.

Middle East & Africa accounted for approximately 5% of global demand in 2025 but represents a high-potential market due to power infrastructure expansion and modernization programs. Countries such as Saudi Arabia, the UAE, and South Africa are investing in grid upgrades, industrial facilities, and energy diversification projects. More than 25% of regional power infrastructure initiatives involve modernization of electrical protection and monitoring systems. Companies are targeting this market through partnerships with utilities, infrastructure contractors, and industrial operators. Demand is increasing for portable testing equipment that supports remote locations and large-scale energy projects.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the most strategically important market in the region due to large-scale infrastructure transformation and energy sector investments. Utility modernization projects and industrial expansion are increasing demand for advanced testing solutions. Companies are strengthening regional presence through technology partnerships, service centers, and solutions designed for large power infrastructure deployments.

The Vacuum Circuit Breaker Testers Market features competition between global technology leaders such as OMICRON, Megger, Doble Engineering, and ISA against regional manufacturers including Vanguard Instruments and specialized testing suppliers. The top five players collectively account for approximately 45% of market share, reflecting a moderately consolidated structure. Competition is based on diagnostic accuracy, software integration, portability, pricing, and service support, with advanced platforms improving testing efficiency by 25–30%. Global leaders compete through automation, cloud connectivity, and ecosystem partnerships, while regional players compete through cost advantages and customization. Companies are expanding service networks, integrating AI-based diagnostics, and developing multifunction testing systems to strengthen market positions. The competitive landscape is shifting toward digital testing platforms and integrated maintenance solutions as utilities demand predictive capabilities. High technical expertise, calibration requirements, and established utility relationships remain major entry barriers. Winning requires combining reliable hardware, intelligent software, localized support, and faster deployment capabilities.

Megger

Doble Engineering Company

ISA Advanced Test Equipment

Vanguard Instruments Company

DV Power

BAUR GmbH

SMC Instruments

KoCoS Messtechnik AG

MEA Testing Systems

Manta Test Systems

Sverker Instruments

Huazheng Electric Manufacturing

Ponovo Power Co.

Vacuum circuit breaker testers are transitioning from standalone measurement devices to integrated digital diagnostic platforms. Modern systems combine timing analysis, contact resistance measurement, and automated reporting, improving testing efficiency by approximately 25% compared with conventional manual workflows. Portable multifunction testers are gaining adoption among utilities, with more than 50% of new deployments emphasizing compact and software-connected solutions. Companies such as OMICRON and Megger are benefiting from demand for integrated testing ecosystems.

Artificial intelligence, cloud analytics, and IoT-enabled monitoring are becoming important technologies for predictive maintenance strategies. AI-supported fault identification can reduce diagnostic analysis time by nearly 40%, while remote data access improves maintenance coordination across distributed assets. Compared with older inspection methods, digital platforms improve operational visibility and reduce repeat testing requirements by around 20%.

Between 2026 and 2028, connected testing solutions, automated calibration, and cybersecurity-enabled platforms will influence competitive positioning. Technology providers investing in software capabilities, interoperability, and lifecycle service models will gain advantage as utilities move toward intelligent asset management. The key shift is from equipment-focused sales toward data-driven reliability solutions.

January 2025 Megger expanded its electrical testing portfolio through the integration of Programma Electric AB capabilities, strengthening high-voltage circuit breaker testing solutions. The move combined product expertise and service capabilities, improving market reach for portable diagnostic instruments used in utility maintenance applications. Source: www.megger.com

March 2025 DV Power introduced a new test method for GIS circuit breakers operating under both-sides-grounded conditions. The innovation improves testing safety and simplifies maintenance procedures, supporting faster field diagnostics for high-voltage assets through advanced measurement techniques. Source: www.dv-power.co

June 2025 Doble Engineering Company expanded testing capabilities with its HD Logic I/O Module for power system testing platforms. The solution improves measurement flexibility for complex protection systems and supports utilities managing renewable integration and increasingly automated electrical networks. Source: www.doble.com

July 2025 OMICRON continued expanding training and deployment support for CIBANO 500 circuit breaker diagnostics, including time-optimized testing programs in India. The platform combines multiple testing functions and reduces setup complexity through integrated workflows for utility engineers.

The Vacuum Circuit Breaker Testers Market Report covers comprehensive analysis across product types, applications, end-users, and major geographic markets including North America, Europe, Asia-Pacific, South America, and Middle East & Africa. The study evaluates portable and advanced testing solutions, utility maintenance applications, industrial deployment, and emerging digital diagnostic technologies shaping market evolution.

The report examines competitive positioning, technology adoption, infrastructure modernization trends, and strategic opportunities between 2026 and 2033. It provides insights into deployment patterns, enterprise requirements, supplier strategies, and innovation priorities. With analysis of leading manufacturers, regional demand drivers, and automation trends, the report supports investment planning, expansion decisions, partnership strategies, and long-term competitive positioning in the evolving electrical testing ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 149.0 Million |

| Market Revenue (2033) | USD 226.9 Million |

| CAGR (2026–2033) | 5.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | OMICRON electronics; Megger; Doble Engineering Company; ISA Advanced Test Equipment; Vanguard Instruments Company; DV Power; BAUR GmbH; SMC Instruments; KoCoS Messtechnik AG; MEA Testing Systems; Manta Test Systems; Sverker Instruments; Huazheng Electric Manufacturing; Ponovo Power Co. |

| Customization & Pricing | Available on Request (10% Customization Free) |