Reports

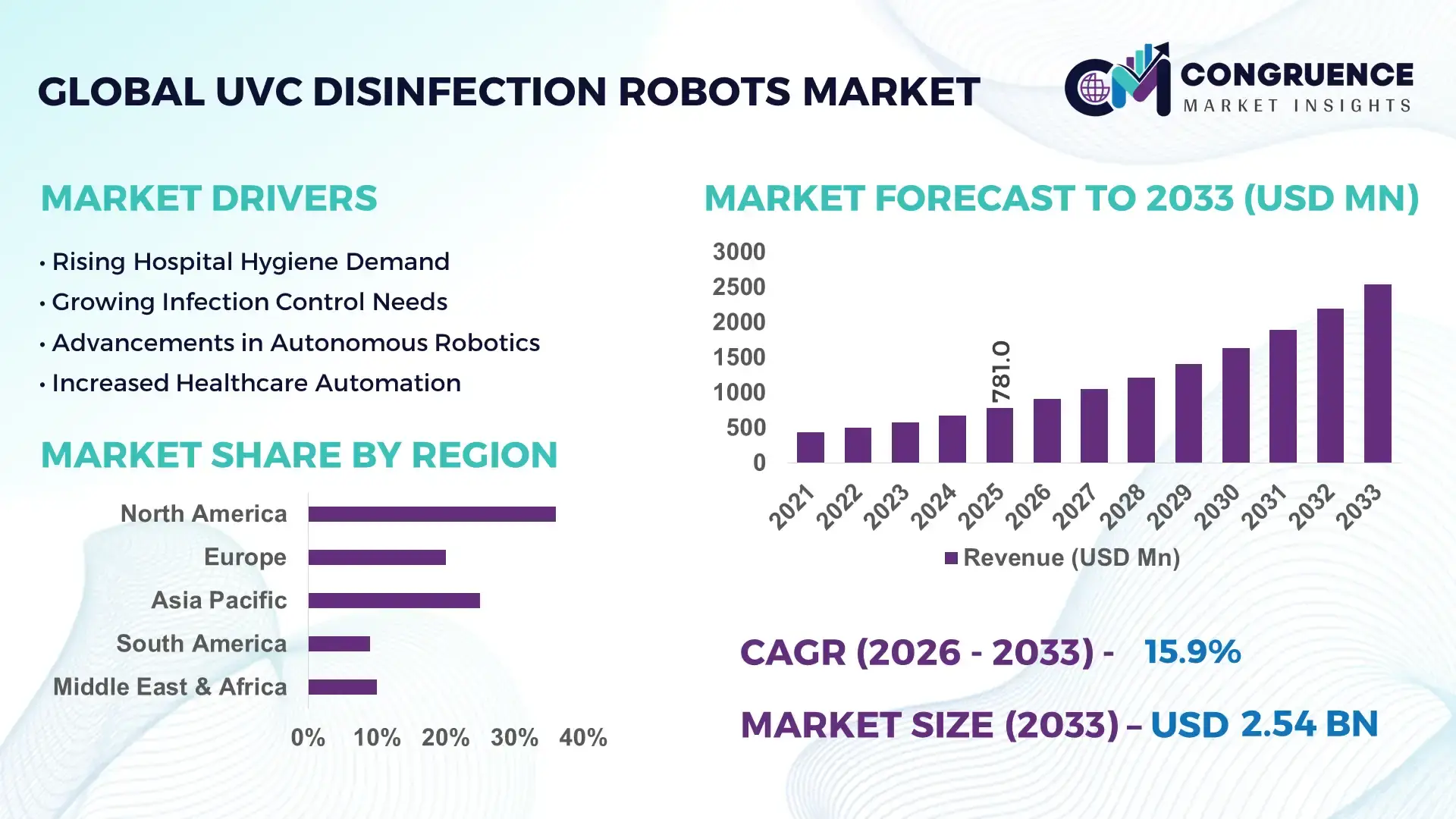

The Global UVC Disinfection Robots Market was valued at USD 781 Million in 2025 and is anticipated to reach a value of USD 2542.83 Million by 2033 expanding at a CAGR of 15.9% between 2026 and 2033. Rising hospital-acquired infection control mandates, labor shortages across healthcare facilities, and accelerated automation deployment in transport hubs and pharmaceutical manufacturing are driving large-scale adoption of advanced autonomous UVC disinfection robots worldwide.

The United States dominates the global UVC disinfection robots market with nearly 34% deployment share, supported by over USD 420 million in healthcare automation investments and rapid integration across hospitals, airports, and semiconductor cleanrooms in 2026. China follows with aggressive smart-hospital expansion and over 28% higher manufacturing output capacity for robotic UV systems compared to Europe. Increased infection-control spending after recent global biosecurity disruptions has pushed autonomous UVC fleet installations above 18,000 units across major healthcare networks globally.

Companies prioritizing AI-enabled navigation, energy-efficient UV-C modules, and healthcare-grade compliance certification are positioned to secure long-term contracts across high-growth institutional infrastructure segments.

Market Size & Growth: USD 781 million in 2025 to USD 2542.83 million by 2033, driven by autonomous healthcare sanitation and smart facility automation demand.

Top Growth Drivers: Hospital automation adoption up 41%, pharmaceutical cleanroom installations up 33%, and airport sanitation robotics deployment increased 27%.

Short-Term Forecast: By 2027, automated UVC systems reduce manual disinfection labor costs by 32% while improving room turnover efficiency by 38%.

Emerging Technologies: AI-guided navigation, LiDAR mapping, and multi-spectrum UV systems improve pathogen elimination efficiency by over 96% in high-traffic facilities.

Regional Leaders: North America exceeds USD 920 million with healthcare robotics expansion, Asia-Pacific crosses USD 780 million through smart-city integration, while Europe surpasses USD 520 million via strict hygiene compliance frameworks.

Consumer/End-User Trends: Over 58% of tertiary hospitals now prioritize autonomous disinfection systems within infection-control procurement strategies.

Pilot/Case Example: In 2026, a multi-hospital robotic deployment project reduced operating-room contamination incidents by 44% within six months.

Competitive Landscape: Top manufacturers control nearly 49% market share, led by healthcare robotics specialists and industrial automation providers expanding regional production footprints.

Regulatory & ESG Impact: Energy-efficient UV systems lower chemical disinfectant usage by 36%, supporting sustainability mandates across public infrastructure facilities.

Investment & Funding: Global investments surpassed USD 1.1 billion in 2026, fueled by robotics partnerships, healthcare digitization, and regional manufacturing expansion.

Innovation & Future Outlook: Next-generation robots integrate predictive analytics, cloud-connected fleet management, and adaptive UV intensity control for large-scale autonomous sanitation networks.

Advanced UVC disinfection robots are witnessing strong demand across hospitals, pharmaceutical plants, airports, and logistics hubs where automated sterilization efficiency directly impacts operational continuity. AI-powered navigation and multi-room fleet coordination systems improved cleaning cycle productivity by nearly 35% in 2026. Rising semiconductor and medical-device manufacturing standards, combined with tighter infection-control regulations and localized robotic component sourcing strategies, continue shaping the market’s long-term competitive positioning and strategic expansion landscape.

UVC disinfection robots are becoming strategically important as healthcare operators, transport authorities, and semiconductor manufacturers prioritize automated contamination control within infrastructure modernization programs. Hospitals in the United States and Japan increased robotic sanitation procurement by over 31% in 2026 following stricter infection-control compliance frameworks and workforce shortages. At the same time, supply-chain restructuring across China and South Korea accelerated localized UV-C component manufacturing, reducing procurement lead times by nearly 22% for autonomous sanitation systems.

AI-enabled UVC robots now deliver up to 40% lower operating costs compared to legacy manual chemical disinfection processes while improving room sterilization consistency above 95%. Germany is focusing on high-precision robotic integration for pharmaceutical cleanrooms, whereas China is scaling large-volume deployments across public transit and logistics hubs. Over the next two to three years, fleet-based robotic disinfection management platforms are expected to expand by more than 28% as facility operators centralize automation workflows and predictive maintenance systems.

In 2026, several airport operators integrated autonomous UVC robots with smart-building systems, cutting overnight sanitation cycles by 37% and lowering chemical disinfectant usage substantially. Companies are responding through robotics partnerships, UV sensor innovation, and regional assembly expansion to strengthen deployment speed and compliance readiness. Firms securing interoperable automation ecosystems and institutional service contracts are expected to establish stronger long-term competitive positioning.

Hospital networks, pharmaceutical facilities, and transit operators are accelerating deployment of autonomous UVC disinfection robots to improve operational efficiency and infection-control consistency. More than 58% of large hospitals in the United States expanded automated sanitation budgets in 2026, while pharmaceutical cleanroom automation installations increased by 33% across Germany and Singapore. Rising labor shortages in facility management and stricter hospital-acquired infection monitoring standards are pushing enterprises toward AI-guided robotic disinfection systems capable of reducing manual intervention by nearly 45%. Companies are responding through strategic partnerships with healthcare infrastructure providers and localized manufacturing expansion in China to shorten delivery cycles. A notable operational shift involves integrating UVC robots into smart-building management platforms, enabling centralized sanitation scheduling and asset tracking across multi-site healthcare campuses.

Advanced UVC disinfection robots require costly LiDAR sensors, medical-grade UV-C modules, and autonomous navigation software, increasing upfront deployment expenses by nearly 30% compared to conventional sanitation systems. Semiconductor supply volatility in Taiwan and South Korea disrupted robotic controller availability during 2025–2026, extending procurement timelines by over 18% for several manufacturers. Smaller hospitals and commercial facilities continue facing infrastructure compatibility limitations, particularly in aging buildings lacking integrated digital facility management systems. These constraints directly affect deployment scalability and procurement flexibility for mid-sized operators. Companies are mitigating risks through regional supplier diversification, localized assembly partnerships, and modular robotic platforms that lower maintenance complexity. Several manufacturers are also introducing subscription-based robotics service contracts to reduce capital expenditure pressure and improve long-term customer retention.

Growing integration of AI analytics, cloud connectivity, and autonomous fleet coordination is creating high-value opportunities for UVC disinfection robotics providers. Smart-hospital infrastructure programs in Japan and the United Arab Emirates increased robotics integration spending by more than 26% in 2026, while logistics facilities adopting automated sanitation systems improved operational uptime by nearly 21%. Emerging demand from semiconductor fabrication plants and food-processing facilities represents a non-traditional expansion avenue due to stricter contamination-control requirements. Companies are investing heavily in adaptive UV intensity systems and predictive maintenance software that optimize energy consumption and robot utilization rates. A significant strategic trend involves robotics firms partnering with building automation providers to create interoperable sanitation ecosystems, allowing centralized monitoring across hospitals, airports, and industrial campuses with lower operational staffing requirements.

Large-scale deployment of UVC disinfection robots faces execution challenges linked to interoperability, cybersecurity, and infrastructure standardization. Nearly 36% of healthcare facilities deploying multi-vendor automation systems reported integration delays in 2026 due to incompatible facility-management software architectures. High-traffic transport hubs and pharmaceutical sites also require continuous UV exposure validation and navigation recalibration, increasing maintenance workloads by approximately 19%. Regulatory evolution surrounding autonomous robotic safety protocols in the European Union and the United States is creating additional certification complexity for manufacturers operating across multiple jurisdictions. Companies must strengthen software integration capabilities, cybersecurity frameworks, and technician training programs to ensure deployment consistency. Firms investing early in standardized communication protocols and remote diagnostics infrastructure are better positioned to secure enterprise-scale contracts and sustain long-term operational reliability.

• AI-Guided Fleet Optimization Healthcare operators in the United States and Japan increased deployment of AI-enabled UVC robotic fleets by 34% in 2026 to reduce sanitation turnaround times and staffing dependency. Centralized fleet-management software improved robot utilization efficiency by nearly 29% across multi-building hospital campuses. Companies are integrating predictive maintenance analytics and cloud-based scheduling platforms to lower downtime, while robotics vendors are expanding software partnerships with smart-building infrastructure providers to strengthen recurring enterprise contracts.

• Localized Manufacturing Expansion Supply-chain disruptions and semiconductor component shortages pushed Chinese and South Korean manufacturers to localize UV-C module and sensor production, cutting procurement lead times by over 21% during 2025–2026. Domestic assembly expansion also reduced logistics costs by approximately 17% for large-volume institutional deployments. Several robotics companies are restructuring supplier networks and increasing regional inventory buffers to secure stable production capacity for hospitals, airports, and pharmaceutical facilities facing strict operational continuity requirements.

• Public Transit Sanitization Growth Airport terminals, metro systems, and railway operators accelerated autonomous UVC sanitation deployment by 31% following tighter passenger safety compliance standards and labor shortages in facility operations. Mobile robotic systems reduced overnight disinfection cycle times by nearly 38% in high-traffic transit hubs. Companies are prioritizing high-capacity mobile robot development and forming partnerships with transport infrastructure contractors to integrate robotic sanitation into broader smart-city modernization programs.

• Energy-Efficient UV-C Integration Advanced low-energy UV-C emitters and adaptive intensity control systems reduced power consumption by approximately 24% while maintaining pathogen elimination efficiency above 95%. Semiconductor cleanrooms and pharmaceutical plants increasingly favor hybrid robotic systems that automatically optimize UV exposure based on room occupancy and contamination risk profiles. Manufacturers are scaling R&D investments in energy-efficient robotics architectures as sustainability targets and rising electricity costs reshape institutional procurement priorities across industrial hygiene operations.

Autonomous Robots dominate the UVC disinfection robots market, accounting for nearly 42% of deployments due to strong scalability, reduced labor dependency, and seamless integration with hospital automation systems. Large healthcare networks in the United States and Germany increasingly prefer autonomous platforms capable of AI-guided navigation and centralized fleet coordination, improving operational productivity by over 35%. Mobile Robots continue holding significant demand across airports and commercial buildings because of deployment flexibility and lower infrastructure modification requirements. Fixed Robots remain relevant in pharmaceutical cleanrooms and semiconductor fabrication facilities where continuous high-precision sterilization is required.

Hybrid Robots represent the fastest-growing segment as enterprises seek systems combining autonomous navigation with fixed high-intensity UV coverage. Adoption of hybrid configurations increased by approximately 28% during 2026 within multi-zone healthcare campuses and industrial facilities requiring adaptive sterilization workflows. Semi-Autonomous Robots maintain steady demand among mid-sized facilities seeking lower acquisition costs and simplified operational control. Companies are responding through modular product development, AI software upgrades, and strategic partnerships with healthcare infrastructure providers to strengthen deployment customization and improve long-term maintenance economics.

Hospital Room Sanitization remains the leading application segment due to stringent infection-control standards, high patient turnover, and continuous sterilization requirements across critical care units. More than 58% of large hospitals expanded automated UVC sanitation programs in 2026 to reduce contamination risks and improve operational consistency. Surface Disinfection continues generating stable demand across pharmaceutical facilities and commercial buildings where robotic systems reduced chemical disinfectant usage by nearly 32%. Laboratory Disinfection is strengthening steadily as biotechnology and semiconductor research centers prioritize contamination-controlled environments with automated sterilization precision.

Public Area Sanitization is emerging as the fastest-growing application, particularly across airports, metro systems, and retail infrastructure where passenger safety protocols intensified after large-scale urban mobility expansion. Deployment of mobile UVC robots in transport hubs increased by approximately 30% in 2026, while Air Disinfection systems gained traction within educational institutions and hospitality properties seeking continuous pathogen-control workflows. Companies are expanding integrated UV-air purification systems and autonomous multi-room sanitation platforms to support large-scale facility management operations and improve sanitation cycle efficiency.

Hospitals remain the dominant end-user segment due to high sanitation frequency, infection-control compliance requirements, and large-scale deployment capability across intensive care, surgical, and isolation units. More than 63% of tertiary healthcare facilities in the United States and Japan integrated robotic disinfection workflows into facility management operations during 2026. Laboratories continue showing consistent adoption growth as pharmaceutical testing centers and semiconductor research facilities require contamination-controlled environments with automated precision. Commercial Buildings are steadily increasing procurement of mobile UVC robots to reduce operational staffing pressure and improve hygiene monitoring efficiency.

The Transportation Sector is emerging as the fastest-growing end-user category, driven by smart infrastructure modernization and rising sanitation automation across airports and railway systems. Robotic deployment across major transit facilities increased by nearly 33% in 2026 as operators prioritized faster overnight disinfection cycles and reduced labor dependency. Hospitality Industry and Educational Institutions are also expanding adoption through leasing models and managed-service sanitation contracts. Companies are targeting these sectors with modular robot configurations, subscription-based maintenance programs, and ecosystem partnerships that improve deployment affordability and operational scalability.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17.8% between 2026 and 2033.

Healthcare Automation and Smart Facility Integration Drive Regional Leadership

North America maintains a dominant position in the UVC disinfection robots market due to advanced healthcare infrastructure, strong institutional automation spending, and early adoption of AI-enabled sanitation systems. The region represented nearly 36% of global deployments in 2025, supported by high procurement activity across hospitals, airports, and pharmaceutical manufacturing sites. Large healthcare systems in the United States expanded autonomous sanitation integration by approximately 32% during 2026 to improve infection-control consistency and reduce labor dependency. Robotics suppliers are strengthening regional manufacturing partnerships and software integration capabilities to support fleet management, predictive maintenance, and centralized building automation. Rising investment in smart hospitals and high-containment laboratory infrastructure continues reinforcing long-term operational demand for autonomous UV-C disinfection platforms.

United States Market Outlook: The United States leads regional deployment activity through large-scale healthcare automation programs, advanced semiconductor manufacturing infrastructure, and strict institutional hygiene compliance standards. More than 61% of tertiary hospitals incorporated robotic sanitation workflows into facility operations by 2026, while major airport operators expanded autonomous disinfection coverage to improve overnight turnaround efficiency. Domestic robotics companies are increasing investments in AI-guided navigation software, LiDAR-enabled mapping systems, and cloud-connected fleet management platforms to strengthen enterprise-scale deployment capabilities.

Regulatory Compliance and Energy Efficiency Reshape Deployment Priorities

Europe continues strengthening its position through strict infection-control frameworks, sustainability-focused infrastructure modernization, and rising automation across pharmaceutical and healthcare facilities. The region accounted for nearly 27% of global deployment concentration in 2025, with Germany, France, and the Netherlands leading institutional integration. Energy-efficient UV-C robotic systems reduced chemical disinfectant dependency by over 30% across several healthcare facilities during 2026, supporting sustainability compliance targets. Pharmaceutical cleanrooms and biotechnology laboratories increasingly prioritize autonomous sterilization systems capable of maintaining continuous contamination-control standards. Robotics manufacturers are expanding collaborations with facility-management software providers to improve interoperability, remote diagnostics, and operational monitoring within large-scale healthcare and industrial environments.

Germany Market Outlook: Germany remains the region’s most strategically significant market due to its advanced pharmaceutical manufacturing base, industrial automation expertise, and strong hospital modernization initiatives. Healthcare operators expanded robotic disinfection integration by approximately 26% in 2026 to improve sterilization consistency and operational efficiency. German enterprises are prioritizing hybrid robotic platforms with adaptive UV intensity control and centralized building integration, while industrial robotics firms continue scaling R&D partnerships to strengthen precision sanitation capabilities for cleanroom and laboratory applications.

Manufacturing Scale and Rapid Urban Deployment Accelerate Expansion

Asia-Pacific is emerging as the fastest-expanding market due to large-scale smart infrastructure projects, localized robotics manufacturing, and aggressive healthcare modernization programs. The region accounted for nearly 31% of global deployment activity in 2025, supported by high-volume procurement across hospitals, transport hubs, and industrial facilities. China, Japan, and South Korea collectively increased autonomous sanitation deployments by over 35% during 2026 as urban mobility systems and semiconductor facilities expanded contamination-control automation. Regional manufacturers also improved domestic UV-C component production capacity by approximately 24%, reducing procurement lead times and strengthening export competitiveness. Companies are scaling regional assembly operations and forming AI software partnerships to support growing enterprise demand for autonomous sanitation ecosystems.

China Market Outlook: China leads the regional market through extensive smart-city development, large-scale healthcare automation investments, and strong domestic robotics manufacturing capacity. Public transit sanitation deployments increased by nearly 38% during 2026 as airport terminals and metro systems integrated autonomous UV-C disinfection workflows into smart infrastructure programs. Chinese manufacturers are expanding vertically integrated supply chains for sensors, robotic controllers, and UV-C modules, enabling faster production cycles and cost-efficient deployment across healthcare, logistics, and industrial sectors.

Healthcare Modernization Expands Institutional Adoption

South America is witnessing gradual but strategic expansion of UVC disinfection robot deployments as healthcare modernization and commercial hygiene automation gain traction. Brazil and Chile account for the majority of regional installations, particularly across private hospitals, laboratory networks, and airport facilities. Institutional procurement activity increased by approximately 19% during 2026 as operators sought automated sanitation systems to reduce labor-intensive cleaning workflows and improve contamination-control consistency. Infrastructure limitations and uneven digital facility integration continue affecting deployment scalability across smaller urban centers. Companies are responding through leasing models, regional distribution partnerships, and modular robotic platforms designed for lower operational complexity and reduced maintenance requirements.

Brazil Market Outlook: Brazil represents the region’s strongest market due to its large healthcare infrastructure base, expanding airport modernization projects, and growing private-sector investment in facility automation. Hospital groups increased robotic sanitation adoption by nearly 22% in 2026 to improve room sterilization turnaround and reduce manual chemical disinfection dependency. Domestic distributors and international robotics firms are strengthening local service networks and technician training partnerships to improve deployment reliability and accelerate institutional acceptance across major metropolitan healthcare systems.

Smart Infrastructure Investment Supports Automation Adoption

The Middle East & Africa market is expanding through smart-city development programs, healthcare infrastructure modernization, and rising investment in automated facility management technologies. Gulf countries accounted for the highest deployment concentration in 2025, driven by airport expansion projects, high-end healthcare facilities, and hospitality infrastructure upgrades. Autonomous sanitation integration across large commercial and healthcare properties increased by nearly 27% during 2026 as labor optimization and operational efficiency became key procurement priorities. Governments and enterprise operators are prioritizing advanced hygiene automation within broader digital transformation frameworks. Companies are establishing regional technology partnerships and localized support operations to strengthen deployment capabilities and improve maintenance responsiveness.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through aggressive smart-building investments, advanced airport infrastructure, and rapid healthcare digitization initiatives. Large hospitality and airport operators expanded autonomous UV-C sanitation coverage by approximately 29% in 2026 to improve operational continuity and high-traffic hygiene management. Enterprises are prioritizing integrated robotic ecosystems linked with centralized building-management platforms, while international robotics providers continue expanding regional partnerships to support enterprise-scale deployment and technical service capabilities.

The UVC disinfection robots market is led by global automation specialists, healthcare robotics providers, and emerging AI-navigation companies competing across technology capability, deployment speed, and institutional integration. Firms such as Xenex, UVD Robots, Finsen Technologies, Akara Robotics, and Blue Ocean Robotics collectively control nearly 48% of advanced healthcare and commercial deployments, while regional manufacturers in China compete aggressively through lower-cost production and faster delivery cycles. Competition increasingly centers on autonomous navigation precision, UV-C exposure efficiency, fleet-management software, and maintenance economics. AI-guided robotic systems improved operational productivity by over 35% compared to legacy programmable units, while localized manufacturing reduced component procurement timelines by approximately 20%. Companies are expanding through hospital partnerships, smart-building integration alliances, and vertically integrated UV-C component sourcing. Technology convergence and software-driven sanitation ecosystems are accelerating competitive consolidation. High certification requirements, interoperability complexity, and enterprise-scale servicing remain major entry barriers. Winning requires scalable automation platforms, strong institutional partnerships, and integrated software-driven operational reliability.

Xenex Disinfection Services

UVD Robots

Blue Ocean Robotics

Finsen Technologies

Akara Robotics

PURO Lighting

OTSAW Digital

Ava Robotics

Mediland Enterprise Corporation

Nevoa Inc.

TMiRob Technology

Skytron

Tru-D SmartUVC

Dimer UVC Innovations

AI-enabled autonomous navigation, LiDAR mapping, and multi-room fleet coordination currently define the operational core of advanced UVC disinfection robots. Hospitals and pharmaceutical facilities deploying AI-guided systems improved sanitation route efficiency by nearly 34% while reducing manual intervention requirements by approximately 41%. More than 58% of newly installed institutional robots in 2026 integrated cloud-based fleet-management platforms for centralized scheduling, predictive maintenance, and performance tracking. Compared with legacy manually programmed UV systems, modern autonomous robots complete room sterilization cycles nearly 38% faster with significantly lower workflow disruption, creating measurable operational advantages for large healthcare networks and transport infrastructure operators.

Emerging technologies between 2026 and 2028 include adaptive UV intensity control, digital twin-enabled facility mapping, and occupancy-sensitive sterilization systems. Hybrid UV-C robots equipped with environmental sensing technology reduced energy consumption by nearly 24% while maintaining pathogen elimination efficiency above 95%. Semiconductor cleanrooms and biotechnology laboratories are increasingly integrating robotic sanitation systems with smart-building platforms to automate contamination-control workflows. Companies with proprietary AI software, high-precision sensor integration, and interoperability capabilities are securing stronger enterprise contracts across regulated industrial environments.

Disruptive development is shifting toward fully connected sanitation ecosystems combining robotics, IoT infrastructure, and predictive analytics. Robotics providers expanding vertically integrated UV-C component manufacturing and cybersecurity-enabled remote diagnostics are expected to gain competitive advantage as institutional buyers prioritize scalable automation reliability and enterprise-wide deployment standardization.

January 2026 – Xenex Disinfection Services received Health Canada registration for its LightStrike6 UV-C robot, becoming the first company authorized for healthcare UV room disinfection in both the U.S. and Canada. The approval strengthened hospital procurement confidence and accelerated North American deployment expansion. Source: xenex.com

March 2026 – PSC Biotech partnered with UVD Robots to deploy autonomous UV-C disinfection systems across pharmaceutical facilities in the United States, Australia, and Singapore. The UVD Pharma Robot completed complex room disinfection nearly 7 times faster than manual chemical-based methods, improving contamination-control productivity and regulatory readiness. Source: pharmaceuticalonline.com

May 2026 – WVU Medicine United Hospital Center completed 18,027 robotic UV disinfection cycles during Q1 2026 using a fleet of nine Xenex robots. The deployment established one of the highest documented hospital utilization rates, improving room sanitation throughput and operational infection-control consistency.

November 2025 – Mason Technology became the exclusive Irish agency for UVD Robots’ fully autonomous UVD Pharma Robot designed for GMP-controlled environments. The 21 CFR Part 11 compliant platform strengthened pharmaceutical cleanroom automation adoption and expanded regulated-sector deployment opportunities across Ireland’s biopharmaceutical manufacturing ecosystem. Source: masontechnology.ie

The UVC Disinfection Robots Market report provides detailed analysis across autonomous robots, semi-autonomous robots, mobile robots, fixed robots, and hybrid robots, with operational evaluation spanning healthcare, transportation, hospitality, laboratories, educational institutions, and commercial infrastructure. The study assesses deployment concentration, automation adoption patterns, and enterprise sanitation workflows across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 60% of assessed institutional deployments are concentrated within hospitals, pharmaceutical facilities, and high-traffic public infrastructure environments.

The report further examines AI-guided navigation systems, LiDAR integration, adaptive UV-C intensity control, fleet-management software, and smart-building interoperability trends shaping market competitiveness between 2026 and 2033. It delivers strategic insights into supply-chain localization, enterprise procurement priorities, partnership activity, and infrastructure modernization programs. Coverage also includes emerging applications within semiconductor cleanrooms, logistics hubs, and automated public-area sanitization, supporting expansion planning, competitive benchmarking, operational optimization, and long-term investment positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 781 Million |

|

Market Revenue in 2033 |

USD 2542.83 Million |

|

CAGR (2026 - 2033) |

15.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Xenex Disinfection Services, UVD Robots, Blue Ocean Robotics, Finsen Technologies, Akara Robotics, PURO Lighting, OTSAW Digital, Ava Robotics, Mediland Enterprise Corporation, Nevoa Inc., TMiRob Technology, Skytron, Tru-D SmartUVC, Dimer UVC Innovations |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |