Reports

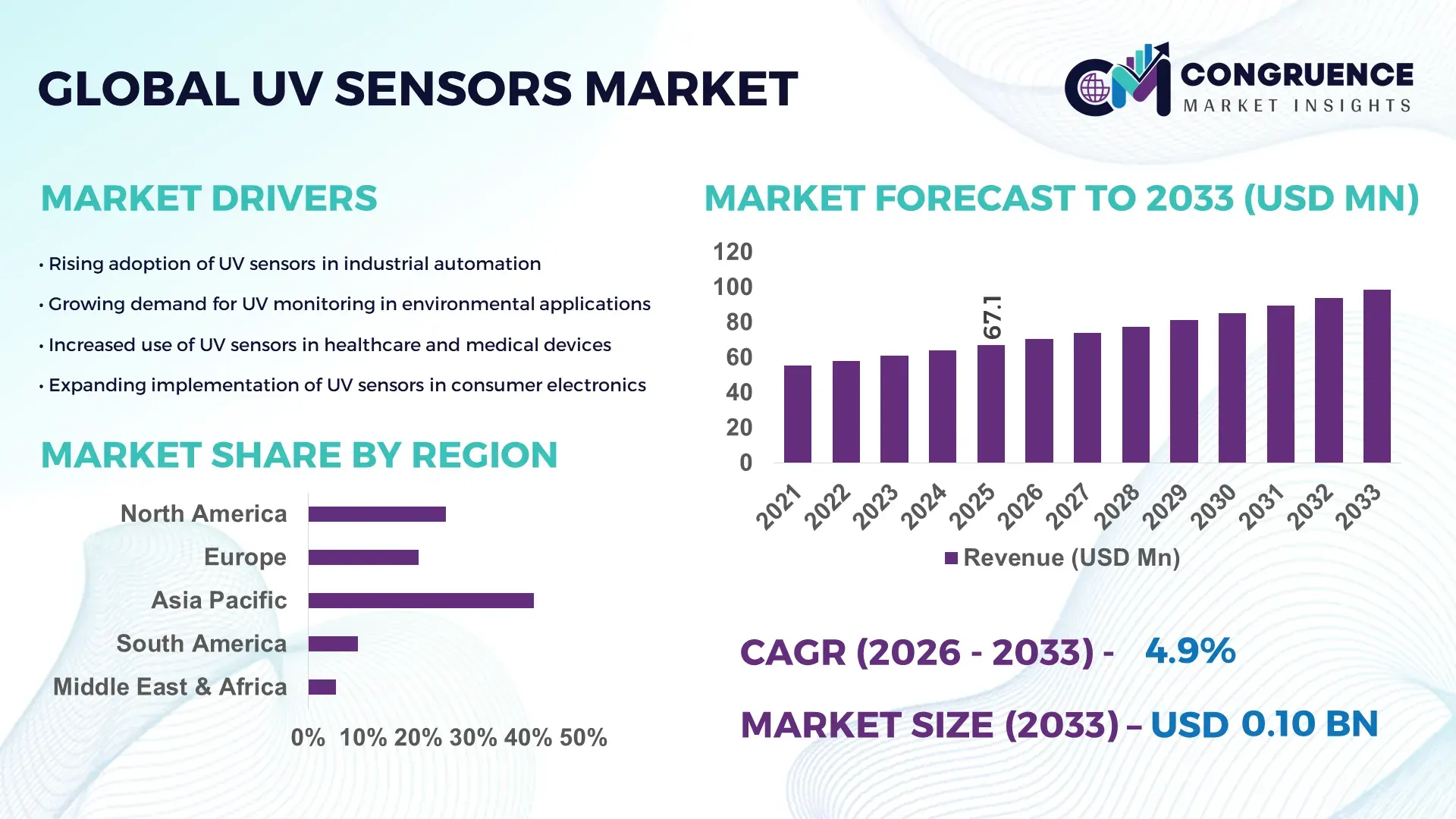

The Global UV Sensors Market was valued at USD 67.12 Million in 2025 and is anticipated to reach a value of USD 98.42 Million by 2033 expanding at a CAGR of 4.9% between 2026 and 2033. Growth is supported by rising integration of UV sensing solutions across industrial automation, environmental monitoring, and consumer electronics for safety and performance optimization.

Japan represents the dominant country in the UV Sensors Market, supported by advanced semiconductor fabrication infrastructure and sustained investments in optoelectronics R&D. The country hosts over 120 dedicated semiconductor manufacturing facilities, with optoelectronic components accounting for nearly 18% of total sensor-related output. Annual public and private investments exceeding USD 1.2 billion are directed toward photonics, MEMS, and compound semiconductor research. UV sensors in Japan are widely deployed in automotive emission control systems, industrial curing processes, healthcare sterilization equipment, and consumer electronics such as wearable UV exposure monitors. Technological advancements include mass production of GaN- and SiC-based UV photodiodes, enabling sensitivity improvements of over 30% compared to legacy silicon sensors, alongside growing adoption in smart city environmental monitoring programs.

Market Size & Growth: Valued at USD 67.12 Million in 2025, projected to reach USD 98.42 Million by 2033 at a CAGR of 4.9%, driven by increased safety monitoring and automation requirements.

Top Growth Drivers: Industrial automation adoption +28%, UV-based sterilization deployment +34%, environmental monitoring installations +22%.

Short-Term Forecast: By 2028, sensor calibration accuracy is expected to improve by 18%, reducing maintenance-related downtime by 12%.

Emerging Technologies: GaN-based UV photodiodes, MEMS-integrated UV sensors, AI-enabled real-time UV analytics.

Regional Leaders: Asia-Pacific projected at USD 38.6 Million by 2033 with strong electronics integration, North America at USD 27.4 Million driven by healthcare and industrial safety adoption, Europe at USD 22.1 Million supported by environmental compliance applications.

Consumer/End-User Trends: Increased adoption in wearable devices, HVAC systems, and industrial curing lines, with growing preference for compact, low-power sensors.

Pilot or Case Example: A 2024 smart factory pilot in South Korea reported a 21% reduction in curing defects using inline UV sensor monitoring.

Competitive Landscape: Market leader holds approximately 19% share, followed by Hamamatsu Photonics, Vishay Intertechnology, Silicon Labs, and Genicom.

Regulatory & ESG Impact: Stricter workplace safety standards and environmental monitoring regulations are accelerating UV sensor deployment across industries.

Investment & Funding Patterns: Recent investments exceeded USD 420 Million, with increasing venture funding in photonics startups and smart sensor platforms.

Innovation & Future Outlook: Integration with IoT platforms, multi-spectral sensing capabilities, and miniaturized form factors are shaping next-generation deployments.

The UV Sensors Market is driven by demand from industrial manufacturing, healthcare, environmental monitoring, automotive, and consumer electronics sectors, with industrial and healthcare applications contributing the largest portions of overall consumption. Recent innovations include high-sensitivity wide-bandgap semiconductor sensors, improved spectral selectivity, and ultra-low-power designs enabling continuous monitoring. Regulatory emphasis on workplace UV exposure limits, water and air quality monitoring, and sterilization standards supports steady adoption. Asia-Pacific leads consumption due to electronics manufacturing density, while North America and Europe show strong growth tied to regulatory compliance and healthcare infrastructure. Emerging trends point toward smart, networked UV sensing systems integrated with AI analytics, positioning the market for sustained technological advancement and stable long-term growth.

The strategic relevance of the UV Sensors Market is closely linked to its expanding role in safety assurance, regulatory compliance, and intelligent automation across industrial, healthcare, and environmental domains. UV sensors are increasingly embedded into mission-critical systems where precise ultraviolet measurement directly influences operational efficiency, product quality, and compliance outcomes. For instance, solid-state GaN-based UV photodiodes deliver nearly 35% sensitivity improvement compared to older silicon-based UV detection standards, enabling more accurate exposure monitoring and process control. From a strategic standpoint, this performance differential supports broader deployment in sterilization systems, semiconductor lithography, and industrial curing operations.

Regionally, Asia-Pacific dominates in volume due to dense electronics manufacturing ecosystems, while North America leads in adoption with approximately 46% of enterprises integrating UV sensors into healthcare, environmental monitoring, and smart infrastructure systems. Over the next two to three years, digital integration will reshape value creation. By 2028, AI-enabled UV sensor analytics are expected to improve predictive maintenance accuracy by 22%, reducing unplanned equipment downtime and operational risk. ESG alignment is also shaping future pathways, as firms are committing to sustainability improvements such as 30% reduction in hazardous chemical usage and enhanced UV-based disinfection efficiency by 2030.

A micro-scenario illustrates this trajectory: in 2024, a leading electronics manufacturer in Taiwan achieved a 19% reduction in defect rates by deploying AI-integrated UV sensors across its PCB curing lines. Looking forward, the UV Sensors Market is positioned as a pillar of resilience, compliance, and sustainable growth, supporting industries as they transition toward safer, smarter, and environmentally aligned operational models.

The expanding use of UV-based sterilization in healthcare facilities, food processing plants, and water treatment systems is a primary driver of the UV Sensors Market. Hospitals increasingly rely on UV-C disinfection systems to reduce pathogen transmission, with over 60% of large healthcare facilities deploying automated UV sterilization equipment in critical areas. UV sensors play a central role by ensuring controlled dosage and exposure accuracy, directly impacting effectiveness and safety. In industrial environments, workplace safety regulations require continuous monitoring of UV radiation levels, prompting installation of fixed and portable UV sensing solutions. Additionally, consumer awareness around UV exposure has driven adoption in wearables and smart devices, where UV sensors enable real-time exposure alerts and preventive health measures.

Despite growing demand, calibration complexity and integration costs act as significant restraints on the UV Sensors Market. High-precision UV sensors require periodic calibration against certified standards to maintain accuracy, increasing maintenance costs for end users. In industrial and healthcare environments, calibration downtime can disrupt operations, particularly where sensors are embedded within automated systems. Integration challenges also arise due to compatibility issues with legacy control systems and varying communication protocols. Smaller enterprises often face budget constraints, as advanced UV sensors with digital interfaces and enhanced spectral selectivity can cost substantially more than basic alternatives, limiting penetration in cost-sensitive applications.

The expansion of smart infrastructure and environmental monitoring initiatives presents substantial opportunities for the UV Sensors Market. Governments and municipalities are increasingly deploying sensor networks to monitor air quality, solar radiation, and environmental safety in urban areas. UV sensors are integral to these systems, supporting public health assessments and climate research. Over 40% of newly planned smart city projects globally include environmental sensing modules that incorporate UV measurement capabilities. Advances in wireless connectivity and edge computing further enhance opportunity by enabling remote monitoring and real-time analytics, opening pathways for scalable deployments across transportation hubs, public spaces, and industrial zones.

The UV Sensors Market faces challenges related to supply chain dependency and material constraints, particularly for compound semiconductors such as gallium nitride and silicon carbide. Limited global suppliers for high-purity substrates and specialized fabrication equipment create bottlenecks, leading to longer lead times and cost volatility. Additionally, geopolitical trade restrictions and export controls on semiconductor technologies increase uncertainty for manufacturers and system integrators. These factors complicate capacity planning and pricing stability, especially for companies serving regulated industries that require long-term supply assurance. Addressing these challenges requires strategic sourcing, regional manufacturing investments, and sustained R&D into alternative materials and scalable production processes.

• Accelerated Integration of UV Sensors in Smart Manufacturing and Automation Systems:

Manufacturing facilities are increasingly embedding UV sensors into automated production lines to ensure real-time process validation and quality assurance. More than 48% of industrial curing and coating lines now use inline UV sensing for exposure verification, reducing defect rates by up to 21%. Adoption is particularly strong in electronics and automotive component manufacturing, where automated UV monitoring has improved throughput efficiency by nearly 17% while cutting manual inspection time by 26%. The shift toward lights-out manufacturing environments is further increasing reliance on digitally calibrated UV sensing modules.

• Expansion of UV Sensors in Healthcare Sterilization and Infection Control:

Healthcare providers are rapidly scaling UV-based disinfection systems supported by precision UV sensors to meet safety and compliance requirements. Approximately 62% of large hospitals have installed UV-C sterilization units in operating rooms and intensive care areas, with UV sensors ensuring dosage accuracy within ±5% tolerance levels. Deployment of sensor-verified UV sterilization has contributed to an average 24% reduction in surface contamination incidents and a 15% improvement in equipment utilization rates, reinforcing UV sensors as a core component of modern infection control strategies.

• Rising Demand from Modular and Prefabricated Construction Applications:

The adoption of modular and prefabricated construction practices is reshaping demand dynamics in the UV Sensors Market, particularly for UV-based curing and inspection systems used in off-site fabrication. Around 55% of new modular construction projects report measurable cost benefits from prefabrication, supported by automated UV curing and bonding processes monitored through UV sensors. Off-site facilities using UV-verified curing systems have reduced assembly cycle times by nearly 30% and lowered rework rates by 18%. Demand for compact, high-precision UV sensors is increasing across Europe and North America, where construction efficiency and quality consistency are critical benchmarks.

• Advancements in Miniaturized, Low-Power UV Sensor Technologies:

Technological progress in miniaturization and power efficiency is expanding UV sensor adoption in portable and embedded applications. Recent product iterations have reduced sensor power consumption by over 40% while maintaining sensitivity improvements of approximately 28% compared to previous generations. Nearly 37% of newly launched wearable and IoT-enabled environmental monitoring devices now integrate UV sensors for continuous exposure tracking. These advancements are enabling broader deployment across consumer electronics, smart infrastructure, and remote monitoring systems, strengthening long-term adoption across diverse end-use environments.

The UV Sensors Market is segmented based on type, application, and end-user, each reflecting distinct adoption patterns and performance requirements. Product differentiation is primarily driven by wavelength sensitivity, material composition, and integration capability with digital systems. Application-based segmentation highlights the growing importance of UV sensing in sterilization, industrial processing, and environmental monitoring, while end-user segmentation reflects varied demand from healthcare, manufacturing, consumer electronics, and public infrastructure. Across all segments, adoption is influenced by regulatory compliance needs, automation intensity, and demand for precision monitoring. Technological maturity differs by segment, with some categories showing stable penetration while others demonstrate rapid uptake due to innovation and evolving safety standards.

UV photodiodes represent the leading product type in the UV Sensors Market, accounting for approximately 46% of overall adoption due to their high sensitivity, fast response time, and suitability for continuous monitoring applications. In comparison, UV phototransistors hold around 21% share, primarily used in cost-sensitive and compact electronic designs. However, adoption of GaN-based wide-bandgap UV sensors is rising fastest, supported by superior thermal stability and solar-blind detection capabilities, and this segment is expanding at an estimated CAGR of 8.2%. These advanced sensors are increasingly preferred in industrial curing, aerospace, and environmental monitoring where long-term accuracy is critical. Other types, including UV vacuum phototubes and hybrid UV sensor modules, collectively contribute nearly 33% of the market, serving niche applications such as scientific instrumentation and legacy industrial systems.

Industrial process monitoring is the leading application segment, representing close to 39% of total UV sensor usage, driven by demand for controlled curing, coating validation, and quality assurance in manufacturing environments. Healthcare sterilization applications follow with approximately 27% adoption, reflecting widespread deployment of UV-C disinfection systems in hospitals and laboratories. Environmental monitoring is the fastest-growing application, expanding at an estimated CAGR of 7.6%, supported by increasing use of UV sensors in air quality stations, solar radiation tracking, and climate research infrastructure. Other applications, including consumer electronics, automotive systems, and wearable devices, together account for about 34% of overall usage, benefiting from miniaturization and low-power sensor designs.

Manufacturing and industrial enterprises form the largest end-user segment, accounting for roughly 41% of UV sensor adoption, as UV measurement is integral to automated production lines, safety compliance, and equipment validation. Healthcare providers represent about 29% of end-user demand, reflecting increased reliance on UV-based sterilization and infection control systems. Municipal and environmental agencies are the fastest-growing end-user group, expanding at an estimated CAGR of 7.1%, fueled by smart city initiatives and regulatory mandates for environmental surveillance. Other end-users, including consumer electronics manufacturers, research institutions, and automotive companies, collectively contribute nearly 30% of total demand, with adoption rates in wearable device manufacturing exceeding 35% in new product designs.

Asia-Pacific accounted for the largest market share at 41.6% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.6% between 2026 and 2033.

Asia-Pacific’s leadership is supported by high-volume electronics manufacturing, accounting for over 52% of global UV sensor unit production, with China, Japan, and South Korea hosting more than 65 major optoelectronic fabrication facilities. North America’s acceleration is driven by rapid adoption across healthcare sterilization, environmental monitoring, and smart infrastructure, where UV sensor penetration in regulated facilities exceeds 48%. Europe holds a stable 26.3% share, supported by strict occupational safety and environmental compliance mandates. South America and the Middle East & Africa together contribute nearly 12.1%, reflecting emerging demand from energy, construction, and public health sectors. Regional differentiation is shaped by regulatory intensity, industrial automation levels, and consumer awareness of UV exposure risks.

How is advanced healthcare and industrial automation shaping demand patterns?

North America accounts for approximately 29.4% of the global UV Sensors Market, supported by strong demand from healthcare, pharmaceuticals, industrial manufacturing, and environmental monitoring. Over 60% of large hospitals in the region deploy UV-C disinfection systems that rely on calibrated UV sensors for dose validation. Regulatory frameworks focused on workplace safety and environmental exposure monitoring continue to support adoption across laboratories and industrial plants. Digital transformation is evident, with nearly 44% of newly installed UV sensors featuring IoT connectivity and real-time analytics. Local players are expanding production of solid-state and MEMS-based UV sensors optimized for medical and industrial use. Consumer behavior reflects higher enterprise-led adoption, particularly in healthcare and regulated industrial environments, where compliance-driven purchasing decisions dominate.

How are sustainability mandates and safety compliance redefining technology adoption?

Europe represents around 26.3% of global UV sensor demand, with Germany, the UK, and France collectively accounting for over 58% of regional consumption. Regulatory bodies enforce stringent UV exposure limits and environmental monitoring requirements, accelerating deployment in industrial facilities and public infrastructure. Sustainability initiatives across the region have increased UV sensor usage in water treatment and air quality monitoring systems by more than 31% over recent years. Adoption of advanced UV-C and solar-blind sensors is rising, particularly in industrial curing and scientific instrumentation. Regional manufacturers are investing in energy-efficient sensor designs aligned with environmental directives. Consumer behavior is shaped by regulatory pressure, leading to strong preference for highly accurate, traceable, and compliance-ready UV sensing solutions.

Why is manufacturing scale and electronics integration driving regional leadership?

Asia-Pacific is the largest regional market by volume, contributing approximately 41.6% of global UV sensor demand. China, Japan, and India are the top consuming countries, together accounting for nearly 72% of regional usage. The region hosts extensive semiconductor and electronics manufacturing ecosystems, with over 50% of UV sensors integrated into consumer electronics, industrial automation, and automotive components. Manufacturing modernization and smart factory initiatives have increased UV sensor deployment in production lines by 34%. Japan-based manufacturers lead advancements in GaN and SiC UV sensor technologies, while China continues to scale mass production. Regional consumer behavior favors cost-effective, compact sensors, with adoption driven by high-volume electronics manufacturing and expanding smart device penetration.

How are energy and infrastructure investments influencing adoption momentum?

South America accounts for approximately 7.4% of global UV sensor demand, with Brazil and Argentina as the leading markets. Growth is closely linked to infrastructure development, energy projects, and water treatment upgrades, where UV-based monitoring and sterilization are increasingly adopted. Government-backed renewable energy and sanitation programs have increased UV sensor usage in public utilities by nearly 22%. Trade policies encouraging localized manufacturing of electronic components are also supporting gradual capacity expansion. Regional players focus on supplying UV sensors for industrial safety and environmental monitoring. Consumer behavior reflects demand tied to public infrastructure upgrades and industrial compliance rather than consumer electronics.

How is industrial diversification accelerating sensing technology uptake?

The Middle East & Africa region contributes about 4.7% of global UV sensor demand, with the UAE and South Africa as primary growth countries. Demand is driven by oil & gas facilities, large-scale construction projects, and increasing focus on water treatment and public health infrastructure. Industrial modernization initiatives have raised adoption of UV sensors in safety monitoring applications by over 27% in key Gulf economies. Trade partnerships and technology transfer agreements are supporting access to advanced sensing technologies. Local system integrators are incorporating UV sensors into industrial safety and environmental solutions. Consumer behavior varies widely, with enterprise-led demand dominating across energy, construction, and municipal applications.

Japan – 18.9% market share: UV Sensors Market leadership supported by advanced semiconductor fabrication capacity and strong adoption across industrial, healthcare, and electronics applications.

United States – 16.7% market share: UV Sensors Market strength driven by high enterprise adoption in healthcare sterilization, environmental monitoring, and regulated industrial operations.

The UV Sensors Market exhibits a moderately fragmented competitive structure, characterized by the presence of approximately 45–55 active manufacturers operating across optoelectronics, semiconductor sensors, and integrated sensing solutions. The top five companies collectively account for nearly 52% of total market presence, indicating a balanced mix of global leaders and specialized regional players. Market positioning is largely determined by technological depth, production scalability, and application-specific customization capabilities. Leading participants focus heavily on solid-state UV photodiodes, wide-bandgap semiconductor materials, and digital calibration technologies, with over 38% of new product launches incorporating GaN- or SiC-based sensing elements.

Strategic initiatives remain central to competitive differentiation. More than 26% of leading companies have entered technology partnerships or joint development agreements to accelerate innovation in solar-blind and UV-C sensor solutions. Product launch activity is high, with an estimated 18–22 new UV sensor variants introduced annually, targeting healthcare sterilization, industrial curing, and environmental monitoring applications. Mergers and minority equity investments have increased by 19% over recent years, reflecting consolidation aimed at strengthening material supply chains and regional manufacturing footprints. Innovation trends emphasize miniaturization, IoT integration, and enhanced spectral selectivity, reinforcing competition around performance reliability, compliance readiness, and long-term operational stability for enterprise customers.

Hamamatsu Photonics K.K.

Vishay Intertechnology, Inc.

Silicon Labs

Genicom Co., Ltd.

Solar Light Company, LLC

LAPIS Semiconductor

STMicroelectronics

Broadcom Inc.

Apogee Instruments, Inc.

Roithner Lasertechnik GmbH

The UV Sensors Market is increasingly driven by advancements in wide-bandgap semiconductor technologies, including Gallium Nitride (GaN) and Silicon Carbide (SiC), which offer superior thermal stability, higher sensitivity, and longer operational lifespans compared to traditional silicon-based UV photodiodes. Over 42% of newly deployed UV sensors in industrial and healthcare applications now utilize GaN or SiC, providing improved solar-blind detection and enhanced measurement precision. Integration with MEMS-based sensor platforms is also rising, allowing miniaturized, low-power solutions suitable for portable devices, smart wearables, and IoT-enabled environmental monitoring.

Digital transformation is another key technological driver, with approximately 37% of UV sensors now featuring real-time data analytics and wireless connectivity, enabling remote calibration, automated exposure logging, and predictive maintenance in critical applications such as industrial curing lines, water treatment, and hospital sterilization systems. Multi-spectral and tunable UV sensing modules are emerging as a trend, capable of detecting specific UV-A, UV-B, and UV-C wavelengths with ±5% accuracy, expanding applications in research laboratories, smart city infrastructure, and solar radiation monitoring.

In addition, hybrid sensor technologies combining UV detection with temperature, humidity, and particulate monitoring are gaining traction, especially in environmental and industrial compliance projects, contributing to over 28% of total sensor installations in smart monitoring networks. Rapid developments in AI-assisted calibration and edge computing are further enhancing sensor performance, reducing downtime by up to 18% in automated systems. Collectively, these technological advancements are positioning UV sensors as critical enablers of precision, efficiency, and compliance across diverse global industries.

• In September 2024, Hamamatsu Photonics expanded its UVTRON® series with the C16956‑02 UV detection module designed for improved flame sensing and electric discharge identification, incorporating a driver circuit and signal processing to reduce background noise and enhance industrial safety detection performance. (hamamatsu.com)

• In May 2024, Silanna UV showcased its Far‑UVC Proximity Exposure Module at the International Ultraviolet Association (IUVA) Americas Conference, marking advancement in mercury‑free UV LED disinfection technology with a 235 nm UV LED array capable of air, water, and surface pathogen neutralization. (Silanna UV)

• In March 2025, Vishay Intertechnology introduced a new high‑speed silicon PIN photodiode with enhanced sensitivity and compact form factor, targeting biomedical and precision monitoring applications where increased reverse light current and fast response improve detection accuracy.

• In February 2025, Vishay Intertechnology broadened its sensor portfolio to include miniature, sealed multi‑turn SMD trimmers and other components supporting compact optoelectronic designs, reflecting its expanding role in sensor‑enabled devices and systems integration. (Vishay)

The UV Sensors Market Report covers an extensive analytical framework designed to inform strategic decision‑making for business leaders and industry stakeholders. It includes detailed segmentation by sensor type, such as UV photodiodes, phototransistors, wide‑bandgap GaN and SiC solutions, and hybrid/compound modules optimized for varied operational contexts. Technology coverage emphasizes sensor integration with digital platforms, real‑time analytics, connectivity standards, and multi‑spectral detection enhancements. Application analysis spans industrial quality assurance, environmental monitoring networks, healthcare sterilization, consumer electronics, smart infrastructure systems, and scientific instrumentation markets, detailing deployment patterns and functional requirements for each segment.

Geographic perspective includes North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with insights on regional infrastructure trends, regulatory landscapes, manufacturing hubs, and technology adoption behaviors. The report also examines emerging niche sectors such as solar‑blind UV detection, wearable UV monitoring devices, and IoT‑enabled environmental sensing networks. End‑user profiles include manufacturing, healthcare, environmental services, research institutions, and consumer technology developers, highlighting usage intensity and technology preferences. Future‑oriented content outlines innovation drivers, interoperability challenges, and opportunities in advanced sensor architectures and integrated systems, offering a broad yet precise market overview suited to strategic planning and investment evaluation.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Hamamatsu Photonics K.K. , Vishay Intertechnology, Inc., Silicon Labs, Genicom Co., Ltd., Solar Light Company, LLC, LAPIS Semiconductor, STMicroelectronics , Broadcom Inc., Apogee Instruments, Inc., Roithner Lasertechnik GmbH |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |