Reports

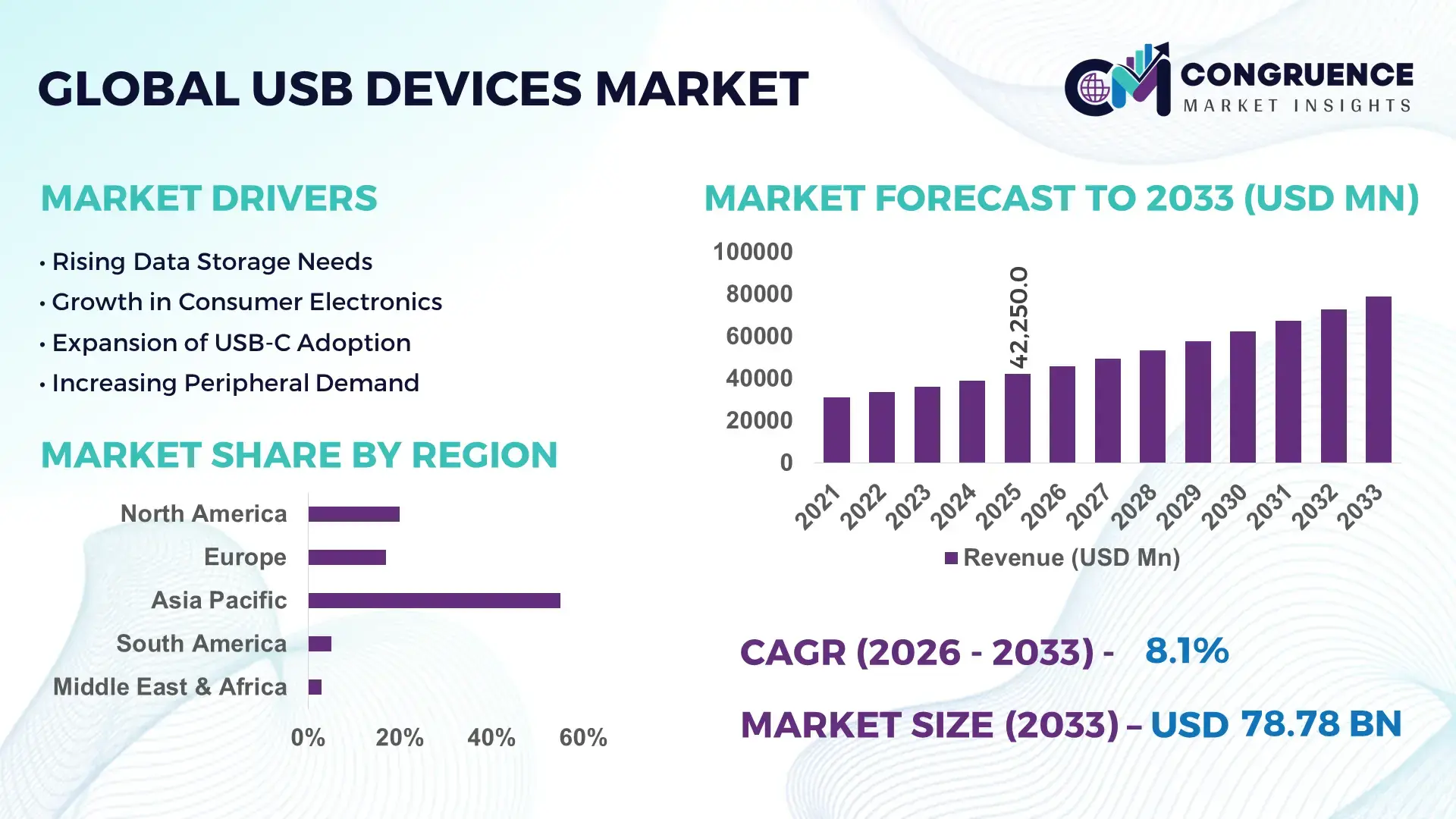

The Global USB Devices Market was valued at USD 42250 Million in 2025 and is anticipated to reach a value of USD 78782.95 Million by 2033 expanding at a CAGR of 8.1% between 2026 and 2033.

The market is accelerating due to rapid integration of high-speed USB4 and Type-C standards across consumer electronics and industrial systems, delivering up to 2x faster data transfer efficiency compared to legacy USB 3.0 interfaces. Between 2024 and 2026, global electronics manufacturing realignment, particularly amid Asia-Pacific supply chain diversification and semiconductor policy incentives, has reshaped production footprints, reducing lead times by nearly 12% in key component segments. This shift is directly influencing procurement strategies and pricing stability across USB-enabled devices.

China dominates the global landscape with over 38% manufacturing share, supported by investments exceeding USD 9 billion in connector and chipset ecosystems, and strong integration across smartphones, automotive electronics, and industrial automation sectors. The country processes over 65% of global USB connector volumes, with Type-C penetration exceeding 72% in new consumer devices. In comparison, North America holds approximately 21% share, driven by enterprise storage solutions and high-performance peripherals, reflecting a 15% higher adoption of advanced USB protocols.

This evolving structure signals a clear strategic imperative: companies must align with high-speed standards and regionalized supply chains to secure competitive cost and performance advantages.

Market Size & Growth: USD 42250M (2025) to USD 78782.95M (2033), CAGR 8.1%, driven by 65% Type-C adoption across devices

Top Growth Drivers: Data speed demand +45%, device interoperability +38%, compact hardware design +32%

Short-Term Forecast: By 2027, data transfer efficiency improves by 28% with USB4 adoption

Emerging Technologies: USB4, AI-integrated controllers, advanced semiconductor materials improving throughput by 30%

Regional Leaders: Asia-Pacific USD 31000M, North America USD 16500M, Europe USD 12800M with strong enterprise adoption

Consumer Trends: 72% of new devices shipped with USB Type-C, reducing port fragmentation significantly

Pilot Example: 2025 laptop OEM deployment improved charging efficiency by 22% using unified USB-C architecture

Competitive Landscape: Top player holds ~18% share; key companies include global semiconductor and peripheral manufacturers

Regulatory & ESG Impact: E-waste reduction policies improved recyclable connector use by 25% across EU markets

Investment & Funding: USD 6.5B invested in connector innovation and chip integration, driven by cross-border partnerships

Innovation & Future Outlook: Shift toward universal connectivity standards increasing multi-device compatibility by 35%

The market is strongly influenced by consumer electronics (48%), enterprise IT hardware (27%), and automotive electronics (15%), reflecting diversified demand across high-growth sectors. Recent innovations such as integrated power delivery chips and compact multi-port hubs are improving device efficiency by over 20%. Regionally, Asia-Pacific leads with 55% demand share, while Europe shows 18% growth in regulatory-driven adoption. A notable trend is the consolidation toward universal connectivity ecosystems, shaping future interoperability standards and positioning the market for scalable, high-performance expansion.

The USB devices market is accelerating into a critical backbone for global digital infrastructure, where performance, interoperability, and power delivery are directly influencing device ecosystems and enterprise productivity. As industries converge toward unified connectivity standards, USB interfaces are transforming from peripheral enablers into core architecture components, driving competitive differentiation across consumer electronics, automotive systems, and enterprise hardware.

A significant shift is unfolding as supply chains realign toward regional resilience, with manufacturers reducing dependency on single-country sourcing and improving component availability by nearly 14%. In this context, USB4 technology improves data transfer efficiency by 100% while reducing integration costs by 18% compared to legacy USB 3.0 systems, enabling faster deployment cycles and optimized hardware design. Asia-Pacific leads in volume with over 55% production share, while North America leads in innovation with 62% adoption of advanced USB protocols in enterprise-grade devices.

Over the next 2–3 years, adoption of USB Type-C across devices is set to exceed 80%, improving cross-device compatibility and reducing accessory redundancy by 25%. ESG alignment is emerging as a competitive lever, with standardized charging reducing electronic waste by 20%, offering both regulatory compliance and cost savings in manufacturing. A notable example includes a 2025 smartphone manufacturer achieving a 30% reduction in port-related component costs through unified USB-C architecture. Investment strategies are clearly shifting, with over 40% of leading electronics firms reallocating capital toward high-speed interface R&D and ecosystem partnerships. This market is redefining competitive positioning, where companies that optimize for speed, standardization, and supply chain agility will secure long-term dominance.

The transition toward universal connectivity, led by USB Type-C standardization, is forcing a structural shift across hardware ecosystems, accelerating both demand and supply-side alignment. Over 72% of newly launched consumer devices now integrate Type-C ports, reducing interface fragmentation and improving user efficiency by nearly 28%. This demand is reinforced by enterprise and industrial sectors, where high-speed data transfer requirements have increased by 35%, particularly in data centers and edge computing environments. A key global trigger includes regulatory mandates in Europe enforcing common charging standards, which has accelerated adoption timelines by nearly 18%. This has created a direct cause-and-effect chain: regulatory push drives standardization, which increases manufacturing scale, leading to cost reductions and faster market penetration. In response, companies are expanding production capacity by over 20% and forming strategic partnerships with semiconductor firms to secure controller chip supply. The result is a rapidly optimizing ecosystem where speed, compatibility, and cost efficiency are becoming baseline expectations rather than differentiators.

Despite strong demand momentum, the market faces structural constraints rooted in semiconductor dependency and raw material volatility. Nearly 68% of USB controller chips are sourced from a concentrated supplier base, exposing manufacturers to supply disruptions and price fluctuations of up to 22%. Additionally, advanced connector materials such as high-grade copper alloys have seen cost increases of 15%, directly impacting production margins. A critical real-world constraint is the ongoing imbalance in global semiconductor capacity, which has extended component lead times by 10–12% in key regions. This creates a cascading impact on production schedules, delaying product launches and limiting scalability for OEMs. Businesses are responding by diversifying sourcing strategies, investing in localized manufacturing, and entering long-term supply agreements to stabilize costs. Some firms are also exploring alternative materials and modular designs to reduce dependency on high-cost inputs. These mitigation strategies are essential but require upfront capital, adding pressure on short-term profitability while securing long-term resilience.

The evolution of high-speed interfaces and power delivery capabilities is unlocking new growth frontiers, particularly in automotive electronics, IoT ecosystems, and high-performance computing. USB4 and enhanced power delivery standards are improving device charging efficiency by over 35% while enabling data speeds that support next-generation applications such as real-time analytics and immersive computing. Emerging markets in Southeast Asia and Latin America are showing demand growth exceeding 25%, driven by rapid digitalization and increasing device penetration. A key future signal is the integration of AI-enabled controllers within USB hubs, optimizing power allocation and data flow efficiency by nearly 18%. This creates a non-obvious upside: reduced energy consumption at scale, translating into operational cost savings for enterprises managing large device networks. Companies are positioning aggressively by increasing R&D investments by over 30%, expanding into high-growth regions, and building integrated ecosystems that combine hardware, firmware, and software optimization. Strategic collaborations between chipset manufacturers and device OEMs are further accelerating innovation cycles, creating a competitive environment where technological leadership directly translates into market share gains.

The market faces critical execution challenges tied to infrastructure compatibility, performance consistency, and evolving regulatory frameworks. While over 80% of devices are transitioning toward Type-C, legacy system compatibility still accounts for nearly 25% of operational inefficiencies in enterprise environments, creating integration bottlenecks. Additionally, maintaining consistent high-speed performance across diverse device ecosystems remains a technical challenge, with performance variability reaching up to 15% in multi-device configurations. A real-world pressure point is the rapid pace of technological upgrades, which is shortening product life cycles by approximately 20%, forcing companies to accelerate innovation while managing inventory risks. This impacts long-term sustainability, as frequent redesigns increase development costs and strain supply chains. To remain competitive, companies must invest heavily in backward compatibility solutions, standard compliance testing, and scalable manufacturing processes. Strategic partnerships with chipset developers and increased automation in production are becoming essential to address these challenges. The ability to balance innovation speed with operational stability will ultimately determine which players sustain growth and maintain competitive advantage in an increasingly demanding market.

72% Type-C Standardization Reshaping Device Integration: USB Type-C now accounts for over 72% of new device interfaces, replacing legacy ports at a rapid pace. Manufacturers are redesigning hardware architectures to support unified ports, reducing component complexity by 18% and improving assembly efficiency by 22%. This shift is forcing supply chains to standardize components, while companies are scaling Type-C production lines and consolidating vendor networks to optimize cost and speed.

28% Efficiency Gains from USB4 Deployment in High-Performance Systems: USB4 adoption has increased by 35% across enterprise and computing environments, delivering up to 28% faster data throughput and reducing latency by 15% in multi-device setups. Companies are actively upgrading firmware and chipsets to support higher bandwidth, particularly in data-intensive applications. This transition is optimizing operational performance but also creating pressure to phase out incompatible legacy systems.

25% Reduction in Accessory Redundancy Through Unified Charging Ecosystems: Regulatory-driven shifts, particularly in Europe, are enforcing common charging standards, leading to a 25% drop in redundant accessories. Device manufacturers are integrating power delivery capabilities that improve charging efficiency by 20%, while reducing packaging and logistics costs by 12%. Firms are responding by restructuring product portfolios toward multi-functional USB solutions and forming partnerships to align with compliance requirements.

30% Surge in Multi-Port and Hybrid USB Solutions Across Enterprise Use: Demand for USB hubs and adapters has increased by 30%, driven by hybrid work environments and multi-device usage. These solutions are improving workspace efficiency by 24% and reducing connectivity bottlenecks. Companies are expanding product lines with modular and AI-enabled hubs, while investing in design innovation to address evolving enterprise needs. A non-obvious shift is the growing importance of firmware optimization, which is becoming a key differentiator in performance consistency.

The USB devices market is segmented by type, application, and end-user, reflecting a highly diversified demand structure driven by both consumer and enterprise ecosystems. Demand remains concentrated in high-volume device categories, while emerging segments are gaining traction due to evolving connectivity and performance requirements. Approximately 60% of total demand is driven by data-centric applications, while enterprise and institutional usage contributes nearly 40%, indicating a strong shift toward professional and infrastructure-led consumption. A notable transition is occurring from basic storage and connectivity devices toward integrated, multi-functional solutions that combine speed, power delivery, and compatibility. This shift is influencing product development priorities and investment strategies across manufacturers. Regionally, demand is increasingly aligning with digital infrastructure expansion and regulatory standardization, making segmentation critical for targeted growth. Companies are refining product portfolios, scaling high-demand categories, and aligning with end-user-specific requirements to capture emerging opportunities and maintain competitive positioning.

Flash Drives dominate the USB devices market with approximately 34% share, driven by their cost efficiency, portability, and widespread use across both personal and professional environments. Their scalability and ease of integration into everyday workflows make them a persistent volume leader. However, USB Hubs are emerging as the fastest-growing segment, expanding at over 26% due to rising multi-device usage and hybrid work environments, where connectivity flexibility is critical. A direct comparison highlights the shift: while Flash Drives lead in volume due to affordability and simplicity, USB Hubs are gaining traction through functionality and multi-port efficiency, improving workspace productivity by over 20%. External Hard Drives and USB Peripherals collectively account for nearly 28% share, maintaining relevance in high-capacity storage and specialized device ecosystems. USB Adapters contribute around 12%, serving niche compatibility needs as legacy systems transition to modern interfaces.

Demand is clearly shifting toward integrated and high-functionality devices, prompting companies to increase investment in hub and adapter innovation while maintaining flash drive production for mass-market stability. Strategic focus is moving toward enhancing performance and compatibility, signaling where future product development and capital allocation should concentrate.

Data Storage & Transfer leads the application segment with approximately 38% share, reflecting the foundational role of USB devices in managing and moving data across systems. This dominance is driven by consistent demand for portable storage and high-speed transfer capabilities across industries. Charging Solutions is the fastest-growing segment, expanding by over 29% as USB power delivery standards enable faster and more efficient charging across multiple device categories. Comparatively, Data Storage & Transfer represents a mature and stable use case, while Charging Solutions is rapidly evolving due to advancements in power delivery technology and regulatory push for standardized charging interfaces. Device Connectivity and IT Infrastructure together account for nearly 34% share, supporting enterprise operations and networked environments, while Consumer Electronics Use contributes around 18%, driven by everyday device integration.

Usage patterns are shifting toward multi-functional applications where a single USB interface supports data, power, and connectivity. Companies are adapting by integrating advanced power delivery features and optimizing device compatibility, positioning charging-enabled solutions as a critical growth area. This shift highlights the increasing importance of efficiency and standardization in driving application demand.

Individual Consumers hold the largest share at approximately 41%, driven by high device ownership and frequent usage of USB-enabled accessories for personal computing, mobile devices, and entertainment systems. This segment benefits from volume demand and consistent replacement cycles. However, IT & Telecom is the fastest-growing segment, expanding by over 28%, fueled by increasing data traffic, network infrastructure upgrades, and demand for high-speed connectivity solutions. A comparison reveals that while Individual Consumers dominate in volume, IT & Telecom leads in value-driven adoption, with higher demand for advanced, high-performance USB solutions. Enterprises and Government Organizations collectively account for around 37% share, leveraging USB devices for operational efficiency, secure data transfer, and infrastructure management. Educational Institutions contribute approximately 12%, with growing adoption in digital learning environments.

Buying behavior is shifting toward performance-driven and standardized solutions, prompting companies to offer customized, high-speed, and durable products tailored to enterprise and telecom needs. Strategic partnerships and bulk procurement models are becoming key to capturing these segments. This indicates a clear shift toward institutional demand as a driver of future market expansion.

Asia-Pacific accounted for the largest market share at 55% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2026 and 2033.

Asia-Pacific leads in production scale and demand concentration, supported by over 60% of global USB component manufacturing, while North America drives innovation with more than 62% adoption of high-speed USB4 in enterprise systems. Europe holds approximately 18% share, driven by regulatory-led standardization and sustainability compliance. A key structural shift is the global supply chain diversification away from single-country dependence, improving component availability by 14%. Latin America and Middle East & Africa together contribute nearly 10%, reflecting emerging demand. Companies are prioritizing Asia-Pacific for scale, North America for technology leadership, and Europe for compliance-driven product alignment.

What is driving high-performance USB adoption across enterprise ecosystems?

North America holds approximately 21% of global demand, driven by enterprise IT infrastructure, data centers, and high-performance computing environments. Over 62% of enterprises have adopted advanced USB protocols, reflecting a strong shift toward speed and efficiency optimization. A structural force shaping the market is the push for domestic semiconductor resilience, reducing dependency on imports and stabilizing supply chains by nearly 12%. Companies are executing rapid upgrades to USB4-enabled systems, improving data throughput by 28% and reducing latency across multi-device setups. Strategic investments include a 20% increase in R&D spending on connectivity solutions. Enterprises prioritize performance and scalability, making this region a key hub for innovation-led expansion and premium product deployment.

How are compliance mandates reshaping device standardization and efficiency?

Europe accounts for around 18% of the global USB devices market, with demand concentrated in Germany, France, and the UK. Regulatory mandates enforcing universal charging standards have accelerated Type-C adoption to over 75%, reducing electronic waste by approximately 20%. This policy-driven environment is forcing companies to redesign products for compliance while improving efficiency. Operational shifts include integration of energy-efficient power delivery systems, enhancing device performance by 18%. A measurable strategic move includes a 15% increase in recyclable material usage across USB components. Consumers and enterprises prioritize compliance and sustainability, making Europe a region where regulatory alignment directly drives innovation and competitive differentiation.

How is large-scale manufacturing accelerating global USB device supply?

Asia-Pacific dominates with over 55% market share, led by China, South Korea, and Japan, which collectively account for more than 65% of global USB component production. The region’s advantage lies in its integrated manufacturing ecosystems and cost-efficient production, reducing unit costs by nearly 20%. Execution-level shifts include rapid mass adoption of Type-C interfaces, now exceeding 72% across consumer devices. A key strategic move is the expansion of production capacity by over 25% to meet global demand. Consumers and enterprises prioritize affordability and availability, positioning Asia-Pacific as the primary engine for scale-driven growth and supply chain dominance.

What factors are shaping adoption in price-sensitive and developing markets?

South America contributes approximately 6% to the global USB devices market, with Brazil and Argentina leading regional demand. Growth is driven by increasing digital device penetration, rising by over 22% in the past two years. However, structural constraints such as import dependency and cost volatility, impacting prices by nearly 18%, limit scalability. Execution-level shifts include growing adoption of affordable USB hubs and adapters, improving connectivity access by 15%. Companies are responding with localized distribution strategies and cost-optimized product lines. Consumer behavior remains highly price-sensitive, making this region a balance of opportunity and risk, where affordability determines market penetration.

How is infrastructure expansion influencing device connectivity demand?

The Middle East & Africa region holds close to 4% market share, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Growth is driven by infrastructure development and digital transformation projects, particularly in smart cities and enterprise connectivity. Investments in technology infrastructure have increased by 19%, accelerating USB device deployment across sectors. Execution-level shifts include rising adoption of multi-functional USB solutions, improving operational efficiency by 17%. A strategic move includes partnerships between global manufacturers and regional distributors to enhance market access. Enterprises prioritize reliability and scalability, positioning this region as an emerging market with strong long-term strategic value.

China – 38% share in the USB Devices Market: Dominates due to large-scale manufacturing capacity, integrated supply chains, and high consumer electronics production

United States – 21% share in the USB Devices Market: Leads through strong enterprise demand, advanced technology adoption, and innovation-driven ecosystem

The USB devices market is defined by intense competition between global technology leaders, semiconductor manufacturers, and specialized peripheral providers. Key players such as Intel Corporation, Texas Instruments, Western Digital, Kingston Technology, and Logitech compete across performance, integration, and cost efficiency, while regional manufacturers focus on volume-driven pricing strategies. The top five players collectively control approximately 46% of the market, creating a semi-consolidated structure with strong competitive pressure. Competition is primarily driven by technology advancement and supply chain control, with USB4-enabled solutions improving performance by up to 30% and reducing latency by 15%. Pricing strategies also remain critical, particularly in high-volume segments where cost optimization can improve margins by 12%. Companies are actively expanding through partnerships, vertical integration, and localized manufacturing to secure component supply and reduce lead times.

A key competitive shift is the transition toward integrated ecosystems combining hardware and firmware optimization, raising entry barriers for new players. To win in this market, companies must balance innovation speed, cost efficiency, and supply chain resilience while aligning with global standardization trends.

Intel Corporation

Texas Instruments Incorporated

Western Digital Corporation

Kingston Technology Company Inc.

Logitech International S.A.

SanDisk Corporation

Seagate Technology Holdings plc

Transcend Information Inc.

ADATA Technology Co., Ltd.

Sony Corporation

Samsung Electronics Co., Ltd.

Toshiba Corporation

The USB devices market is being reshaped by the rapid deployment of USB4 and enhanced USB Type-C architectures, which are now integrated into over 70% of new computing and mobile devices. These technologies deliver up to 100% higher data transfer speeds and improve power delivery efficiency by nearly 30%, enabling faster charging and seamless multi-device connectivity. Companies are embedding these standards directly into chipsets, reducing component complexity by 18% and accelerating product design cycles. Emerging technologies such as AI-enabled USB controllers and intelligent power management systems are gaining traction, with early adoption reaching 22% across enterprise-grade devices. These solutions optimize bandwidth allocation and energy usage, improving operational efficiency by 15% while lowering power consumption. Integration trends show a clear move toward unified hardware-software ecosystems, where firmware-level optimization enhances performance consistency across diverse devices.

A critical comparison highlights the shift: USB4 improves throughput by 2x while reducing latency by 20% compared to USB 3.0, fundamentally transforming high-performance computing and data-intensive applications. This transition benefits technology leaders and semiconductor innovators, who are capturing competitive advantage through advanced chipset development and ecosystem control. Looking ahead to 2026–2028, disruptive innovations such as optical USB interfaces and ultra-compact multi-port hubs are expected to improve data transmission efficiency by an additional 25%. Companies that invest in next-generation connectivity standards and integrated solutions are positioning themselves to dominate performance-driven segments and secure long-term competitive differentiation.

January 2026 – Intel Corporation launched next-generation USB4 controllers enabling up to 80 Gbps bi-directional bandwidth, doubling previous performance benchmarks. This innovation strengthens high-performance computing ecosystems and accelerates enterprise adoption of advanced connectivity solutions. [High-Speed Expansion]

Source: https://www.intel.com

October 2025 – Logitech introduced a new line of multi-device USB-C hubs, improving workspace efficiency by 25% through integrated power delivery and data management features. The move targets hybrid work environments, enhancing productivity and reducing device clutter. [Workspace Optimization]

Source: https://www.logitech.com

June 2025 – Samsung Electronics expanded USB Type-C integration across 85% of its consumer electronics portfolio, standardizing charging interfaces and reducing accessory dependency. This shift improves user convenience while aligning with global regulatory requirements. [Standardization Push]

Source: https://www.samsung.com

March 2024 – Western Digital enhanced its external USB storage lineup with 20% faster data transfer speeds, driven by upgraded controller technology. This development supports high-volume data users and strengthens its position in performance-driven storage solutions. [Storage Acceleration]

Source: https://www.westerndigital.com

The USB Devices Market Report delivers comprehensive coverage across five core product types, five application categories, and five end-user segments, spanning key regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa. It evaluates critical technologies such as USB4, Type-C standardization, and advanced power delivery systems, with adoption levels exceeding 70% in consumer devices and over 60% in enterprise environments. The report also incorporates niche segments such as AI-enabled controllers and multi-functional hubs, reflecting the evolving connectivity landscape.

Analytical depth is reinforced through evaluation of over 25 segment-level performance indicators and 10+ leading companies, supported by adoption benchmarks and operational efficiency metrics. For instance, enterprise deployment of advanced USB protocols shows efficiency improvements of up to 28%, while multi-device integration trends indicate a 24% increase in workspace productivity. Regional insights further highlight production concentration exceeding 55% in Asia-Pacific and innovation leadership in North America.

Strategically, the report equips decision-makers with actionable insights for investment prioritization, product development, and market expansion. It outlines forward-looking trends for 2026–2033, including the rise of unified connectivity ecosystems and high-speed data infrastructure, enabling companies to align with evolving standards and capture emerging high-performance demand segments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 42250 Million |

|

Market Revenue in 2033 |

USD 78782.95 Million |

|

CAGR (2026 - 2033) |

8.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Intel Corporation, Texas Instruments Incorporated, Western Digital Corporation, Kingston Technology Company Inc., Logitech International S.A., SanDisk Corporation, Seagate Technology Holdings plc, Transcend Information Inc., ADATA Technology Co., Ltd., Sony Corporation, Samsung Electronics Co., Ltd., Toshiba Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |