Reports

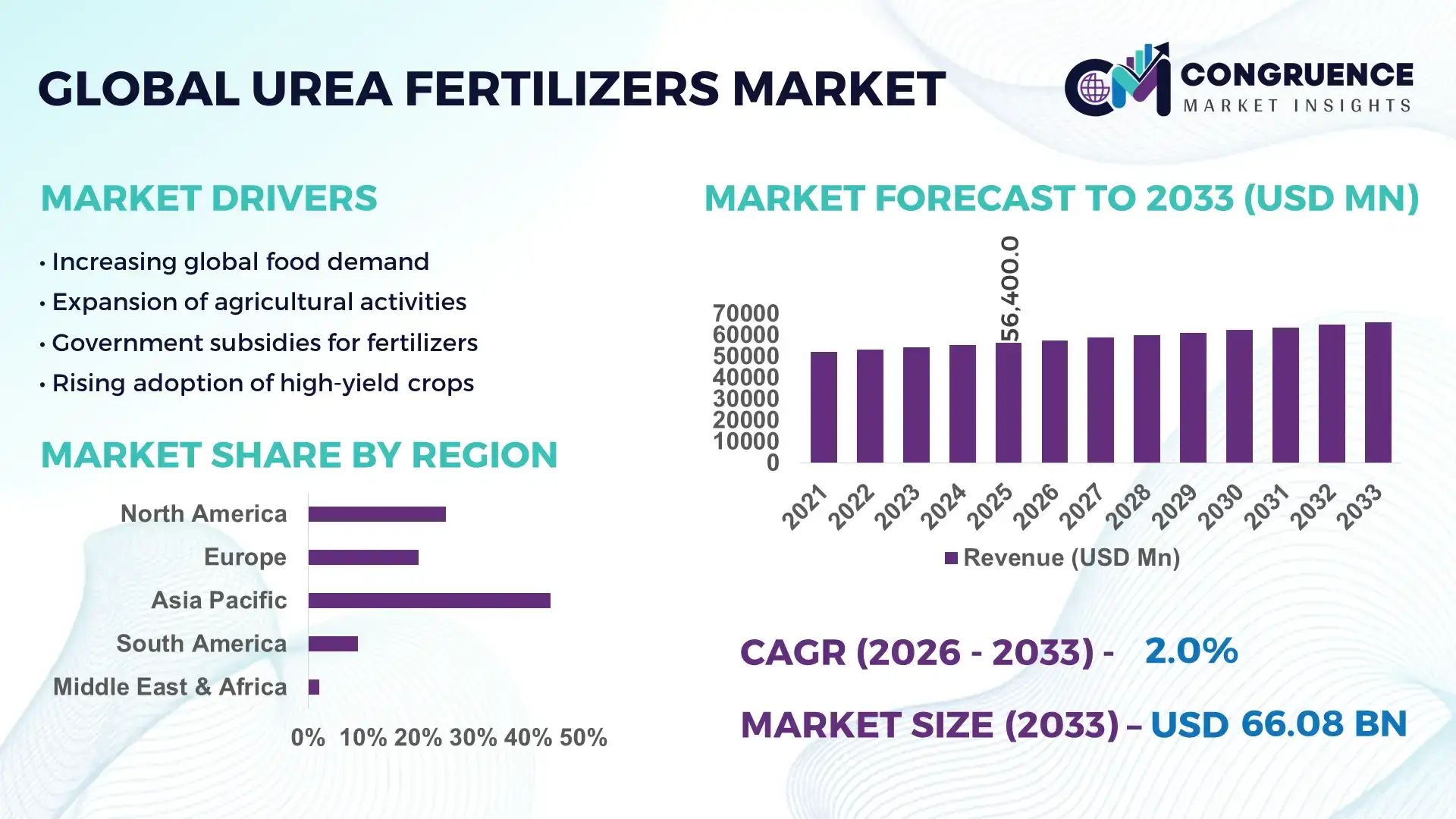

The Global Urea Fertilizers Market was valued at USD 56400 Million in 2025 and is anticipated to reach a value of USD 66081.58 Million by 2033 expanding at a CAGR of 2% between 2026 and 2033. The growth is primarily driven by rising global food demand and the need to enhance crop productivity through nitrogen-rich fertilizers.

China remains a central hub in the global urea fertilizers market, supported by an annual production capacity exceeding 70 million metric tons. The country continues to invest in coal-based ammonia production technologies, which contribute to over 65% of its total urea output. Technological upgrades in granulation and synthesis processes have improved energy efficiency by approximately 10–12% over recent years. Agricultural demand dominates usage, with more than 80% of urea consumption directed toward staple crops such as rice, wheat, and maize. Additionally, the adoption of enhanced-efficiency fertilizers, including controlled-release urea, has improved nutrient utilization rates by nearly 25%, supporting productivity improvements in large-scale farming operations.

Market Size & Growth: Valued at USD 56,400 million in 2025, projected to reach USD 66,081.58 million by 2033 at a CAGR of 2%, driven by increasing agricultural productivity requirements.

Top Growth Drivers: Precision farming adoption (28%), nitrogen-use efficiency improvement (22%), population-driven food demand (35%).

Short-Term Forecast: By 2028, advanced nutrient management systems are expected to reduce fertilizer wastage by 18%.

Emerging Technologies: Controlled-release urea coatings, AI-based soil nutrient analytics, and low-emission ammonia production technologies.

Regional Leaders: Asia-Pacific projected to reach USD 32,000 million by 2033 with intensive farming practices; North America USD 11,500 million with high-tech adoption; Europe USD 9,200 million driven by sustainability regulations.

Consumer/End-User Trends: Large-scale farmers contribute over 60% of total demand, with increasing preference for eco-efficient fertilizers.

Pilot or Case Example: In 2024, a precision fertilization initiative improved nitrogen efficiency by 21% across commercial farms.

Competitive Landscape: Leading player holds approximately 18% share, followed by several global manufacturers with diversified fertilizer portfolios.

Regulatory & ESG Impact: Environmental mandates target 15–20% reduction in nitrogen runoff by 2030.

Investment & Funding Patterns: More than USD 8 billion invested in fertilizer plant upgrades and green ammonia projects globally.

Innovation & Future Outlook: Integration of digital agriculture tools and sustainable fertilizer solutions is shaping long-term market evolution.

The urea fertilizers market is largely driven by the agriculture sector, which accounts for over 75% of total consumption, followed by industrial applications including resins and diesel exhaust fluid production. Innovations such as polymer-coated urea and nano-urea formulations have demonstrated up to 30% higher nutrient efficiency compared to conventional fertilizers. Regulatory frameworks aimed at reducing environmental impact are accelerating the shift toward sustainable fertilizer solutions, particularly in developed regions. Meanwhile, emerging economies in Asia and Africa are experiencing rising demand due to expanding agricultural activities and government support programs. The market outlook reflects a growing emphasis on precision farming and environmentally responsible nutrient management practices.

The urea fertilizers market plays a critical role in strengthening global agricultural productivity while aligning with sustainability objectives. With agriculture supporting nearly 40% of the global workforce, nitrogen-based fertilizers remain essential for improving crop yields by up to 50% under intensive cultivation. Nano-urea technology delivers approximately 35% higher nutrient absorption efficiency compared to conventional granular urea, significantly reducing losses and optimizing application. Asia-Pacific dominates in volume due to extensive agricultural activities, while North America leads in adoption, with over 55% of farms integrating precision agriculture technologies.

By 2028, AI-driven nutrient management systems are expected to improve fertilizer application efficiency by 20%, reducing operational costs and environmental impact. Companies are increasingly focusing on ESG commitments, targeting reductions in nitrogen runoff by 18% and greenhouse gas emissions by 12% by 2030. In 2024, India achieved a 15% reduction in urea usage per hectare through the deployment of nano-urea liquid formulations, demonstrating measurable gains in efficiency and cost optimization.

Strategic investments in green ammonia production using renewable energy sources are expected to reduce carbon emissions by up to 70% compared to traditional manufacturing methods. Digital agriculture platforms that integrate soil analysis, weather forecasting, and nutrient planning are enabling data-driven decision-making. The urea fertilizers market continues to evolve as a technologically advanced and sustainability-focused sector, positioning itself as a foundation for resilient agricultural systems and long-term food security.

The increasing global population, expected to surpass 8.5 billion by 2030, is significantly boosting the demand for agricultural output, thereby driving the need for efficient fertilizers such as urea. Crop production must increase by nearly 50% to meet future food requirements, positioning nitrogen fertilizers as a critical input. Urea enhances crop yields by up to 30–40% in key cereals such as rice and wheat, making it indispensable in large-scale farming. Developing regions across Asia and Africa are expanding their agricultural activities, leading to higher fertilizer consumption. Government support programs, particularly in countries like India, subsidize over 60% of urea usage, ensuring widespread accessibility. Advancements in irrigation and mechanization further support efficient fertilizer application, reinforcing demand growth.

Environmental issues associated with excessive urea usage are a major constraint for the market. Nitrogen runoff contributes to water pollution and eutrophication, while soil degradation impacts long-term agricultural productivity. Approximately 30–40% of applied nitrogen is lost to the environment, reducing efficiency and increasing ecological risks. Strict environmental regulations in regions such as Europe and North America are limiting fertilizer usage and encouraging alternative solutions. Additionally, urea production is energy-intensive, leading to significant greenhouse gas emissions, particularly in coal-based facilities. Compliance with environmental standards is increasing operational costs and pushing manufacturers toward sustainable yet cost-intensive technologies.

Sustainable fertilizer innovations present substantial opportunities for growth in the urea fertilizers market. Technologies such as controlled-release urea and nano-urea have shown up to 30% improvement in nutrient efficiency, reducing environmental impact and application frequency. Government initiatives promoting sustainable agriculture are encouraging the adoption of eco-friendly fertilizers. Emerging regions such as Africa and Southeast Asia offer strong growth potential due to lower fertilizer usage rates per hectare compared to global averages. Digital agriculture tools, including soil sensors and AI-based nutrient management systems, are enabling precise application, improving productivity while minimizing waste. Investments in renewable energy-based ammonia production are further enhancing sustainability and long-term market potential.

Volatility in raw material prices, particularly natural gas and coal, poses a significant challenge for the urea fertilizers market. These inputs account for a major portion of production costs, and price fluctuations can disrupt supply stability. Geopolitical tensions and trade restrictions further impact the availability and pricing of fertilizers across key agricultural markets. Transportation and logistics challenges, including rising fuel costs, add to distribution complexities, especially in developing economies. Additionally, transitioning to sustainable production technologies requires substantial capital investment, creating financial barriers for smaller manufacturers. These challenges collectively affect market stability and operational efficiency across the value chain.

• Expansion of Enhanced-Efficiency Urea Products Improving Nutrient Utilization by 25–35%:

The adoption of enhanced-efficiency fertilizers such as polymer-coated and stabilized urea is accelerating across key agricultural regions. These products reduce nitrogen losses by nearly 30% while improving crop uptake efficiency by up to 35%, particularly in high-value crops such as maize and wheat. Around 40% of large-scale farms in North America and Europe have integrated controlled-release urea into their nutrient management programs. This trend is further supported by regulatory pressure to limit nitrogen runoff, resulting in measurable reductions of up to 20% in environmental emissions. The shift toward precision nutrient delivery is transforming traditional fertilizer application methods into data-driven processes.

• Rapid Integration of Digital Agriculture Tools Driving 20% Efficiency Gains:

Digital farming technologies, including AI-based soil analysis and GPS-enabled precision application systems, are reshaping urea fertilizer usage. Approximately 55% of commercial farms in developed markets now utilize digital tools to optimize fertilizer input, leading to an average 20% improvement in application accuracy. Smart sensors and satellite-based monitoring systems enable real-time nutrient assessment, reducing over-application rates by nearly 18%. In emerging markets, adoption is growing steadily, with digital agriculture penetration increasing by over 12% annually. These advancements are enhancing productivity while lowering operational costs and environmental impact.

• Rising Adoption of Green Ammonia Reducing Carbon Emissions by Up to 70%:

The transition toward green ammonia production using renewable energy sources is gaining traction as sustainability becomes a priority. Green ammonia technologies have demonstrated the potential to reduce carbon emissions by up to 70% compared to conventional natural gas-based processes. Currently, over 15% of new fertilizer production projects globally are focused on low-carbon or renewable-based ammonia synthesis. Europe and parts of Asia are leading this transition, with pilot plants achieving energy efficiency improvements of approximately 25%. This trend aligns with global climate targets and is expected to reshape the environmental footprint of urea fertilizer manufacturing.

• Increasing Demand in Emerging Economies Driving Consumption Growth Above 40% Share:

Emerging economies across Asia-Pacific and Africa account for over 40% of global urea fertilizer consumption, driven by expanding agricultural activities and population growth. Fertilizer usage per hectare in these regions has increased by nearly 18% over the past decade, reflecting intensification in farming practices. Government subsidy programs support over 50% of fertilizer purchases in countries such as India, enhancing accessibility for farmers. Additionally, irrigation expansion projects have improved fertilizer efficiency by approximately 15%, further boosting demand. This growing consumption trend highlights the critical role of urea fertilizers in supporting food security in developing regions.

The urea fertilizers market is segmented based on product type, application, and end-user categories, each contributing uniquely to overall demand patterns. Granular and prilled urea dominate the product landscape due to ease of handling and widespread agricultural compatibility, while advanced formulations such as coated and liquid urea are gaining traction for improved efficiency. Application-wise, agriculture remains the primary sector, accounting for a substantial majority of consumption, followed by industrial uses such as resins and diesel exhaust fluid. End-user segmentation highlights the dominance of large-scale farming operations, though smallholder farmers continue to represent a significant portion in emerging economies. Regional consumption patterns indicate higher adoption in Asia-Pacific, where fertilizer usage intensity is significantly greater compared to global averages.

The urea fertilizers market by type includes granular urea, prilled urea, coated/controlled-release urea, and liquid urea formulations. Granular urea leads the segment, accounting for approximately 48% of total adoption due to its superior handling properties, uniform particle size, and compatibility with mechanized farming systems. Prilled urea follows with around 30% share, widely used in developing regions because of its lower production cost and accessibility. However, coated and controlled-release urea is the fastest-growing segment, expanding at an estimated CAGR of 6.5%, driven by its ability to improve nutrient efficiency by up to 30% and reduce nitrogen losses by nearly 25%.

Liquid urea and specialty formulations collectively account for the remaining 22% of the market, finding niche applications in fertigation and precision agriculture systems. These products are particularly relevant in regions with advanced irrigation infrastructure.

The application segment of the urea fertilizers market is primarily divided into agriculture, industrial use, and automotive applications such as diesel exhaust fluid. Agriculture dominates the segment with approximately 76% share, driven by the essential role of urea in enhancing crop productivity across cereals, fruits, and vegetables. Industrial applications, including resin and adhesive production, account for nearly 15%, while automotive uses contribute around 9%, particularly in emissions control systems.

The fastest-growing application is automotive diesel exhaust fluid, expanding at an estimated CAGR of 7.2%, supported by stringent emission regulations and the increasing adoption of selective catalytic reduction (SCR) systems in commercial vehicles. Agricultural applications continue to evolve with the integration of precision farming techniques, improving nutrient use efficiency by up to 20%.

End-user segmentation in the urea fertilizers market includes large-scale commercial farms, smallholder farmers, industrial manufacturers, and automotive sector users. Large-scale farms dominate the segment, accounting for approximately 52% of total usage due to their extensive landholdings and adoption of advanced farming technologies. Smallholder farmers represent around 30% of demand, particularly in Asia and Africa, where agriculture remains a primary livelihood. Industrial users contribute nearly 10%, while the automotive sector accounts for approximately 8%, primarily through diesel exhaust fluid consumption.

The fastest-growing end-user segment is the automotive sector, with an estimated CAGR of 6.8%, driven by increasing regulatory requirements for emission control. Large-scale farms are also witnessing steady growth, supported by mechanization and digital agriculture adoption rates exceeding 50% in developed markets. Other end-users collectively contribute around 18% of the market, reflecting diversified usage patterns.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 3.4% between 2026 and 2033.

Asia-Pacific’s dominance is supported by high agricultural dependency, with over 60% of global urea consumption concentrated in countries such as China and India. North America holds approximately 18% share, driven by advanced precision farming practices and high fertilizer application rates exceeding 130 kg per hectare. Europe contributes nearly 14%, with strict environmental regulations influencing demand for enhanced-efficiency fertilizers. South America accounts for around 12%, supported by large-scale soybean and maize cultivation in Brazil and Argentina. Middle East & Africa collectively represent about 10%, with increasing investments in fertilizer production facilities and agricultural expansion initiatives. Regional disparities in fertilizer usage intensity, ranging from 90 kg per hectare in Africa to over 150 kg per hectare in developed regions, highlight significant growth opportunities across emerging markets.

North America accounts for approximately 18% of the global urea fertilizers market, with demand largely driven by large-scale commercial agriculture and high-value crop production. The United States dominates regional consumption, with fertilizer application rates exceeding 140 kg per hectare in key farming states. Government programs promoting sustainable agriculture and nutrient management have resulted in a 15% reduction in nitrogen runoff over recent years. Digital transformation plays a crucial role, with over 55% of farms adopting precision agriculture technologies such as GPS-guided application and soil monitoring systems, improving efficiency by nearly 20%. A leading regional player has invested in advanced nitrogen stabilization technologies, reducing volatilization losses by up to 25%. Consumer behavior in this region reflects a strong preference for high-efficiency fertilizers and data-driven farming solutions, particularly among large enterprise farms.

Europe holds around 14% of the global urea fertilizers market, with key markets including Germany, France, and the United Kingdom. The region is heavily influenced by environmental regulations targeting a 20% reduction in nitrogen emissions by 2030, driving the adoption of controlled-release and low-emission fertilizers. Nearly 45% of farms have shifted toward enhanced-efficiency urea products to comply with sustainability mandates. Technological adoption is increasing, with digital nutrient management systems improving fertilizer utilization efficiency by approximately 18%. A major regional producer has implemented green ammonia technology, achieving a 30% reduction in carbon emissions at select production sites. Consumer behavior is strongly shaped by regulatory pressure, with farmers prioritizing environmentally compliant solutions and precision application methods to minimize ecological impact.

Asia-Pacific leads the global urea fertilizers market in both volume and consumption, accounting for nearly 46% of total demand. China and India are the top consuming countries, together representing over 70% of regional usage. Fertilizer application rates in intensive farming areas exceed 160 kg per hectare, supporting high crop yields. Infrastructure expansion, including new ammonia and urea production plants, has increased regional capacity by over 12% in recent years. Technological advancements such as nano-urea and controlled-release fertilizers are gaining traction, improving nutrient efficiency by up to 25%. A prominent regional producer has scaled nano-urea production, reducing conventional urea consumption by 15% in pilot regions. Consumer behavior reflects strong reliance on subsidized fertilizers, with over 50% of farmers benefiting from government support programs.

South America accounts for approximately 12% of the global urea fertilizers market, with Brazil and Argentina serving as key demand centers. Brazil alone represents over 60% of regional consumption due to its extensive soybean and corn production. Fertilizer usage has increased by nearly 20% over the past decade, supported by expanding agricultural land and export-driven farming. Infrastructure improvements in port logistics and storage facilities have enhanced supply chain efficiency by approximately 15%. Government policies encouraging agricultural exports and fertilizer imports have further strengthened market growth. A regional supplier has expanded distribution networks, improving fertilizer availability across remote farming regions. Consumer behavior is closely tied to crop cycles, with farmers prioritizing bulk purchases and cost-effective fertilizer solutions.

The Middle East & Africa region contributes around 10% of the global urea fertilizers market, with growing demand driven by agricultural expansion and industrial applications. Countries such as Saudi Arabia, UAE, and South Africa are investing in large-scale fertilizer production facilities, increasing output capacity by over 18% in recent years. The region benefits from abundant natural gas resources, enabling cost-effective ammonia production. Technological modernization initiatives have improved plant efficiency by approximately 20%, while trade partnerships have strengthened export capabilities. A leading regional producer has developed advanced urea granulation units, enhancing product quality and distribution efficiency. Consumer behavior varies widely, with African markets focusing on affordability and accessibility, while Middle Eastern markets emphasize industrial and export-oriented applications.

China – 28% market share in the urea fertilizers market, driven by high production capacity exceeding 70 million metric tons annually.

India – 18% market share in the urea fertilizers market, supported by strong agricultural demand and extensive government subsidy programs.

The urea fertilizers market exhibits a moderately consolidated structure, with the top five companies collectively accounting for approximately 42% of the global market share. Over 50 active global and regional players compete across production, distribution, and technological innovation. Leading companies focus on expanding production capacity, with several firms increasing output by 10–15% through plant upgrades and efficiency improvements. Strategic partnerships and joint ventures are common, particularly in green ammonia and sustainable fertilizer development projects.

Product innovation remains a key competitive factor, with investments in enhanced-efficiency fertilizers increasing by over 20% in the past three years. Companies are also integrating digital agriculture solutions, enabling precision fertilizer application and improving customer engagement. Mergers and acquisitions have intensified, with at least 8 major transactions recorded in recent years aimed at strengthening regional presence and technological capabilities. The market is characterized by high entry barriers due to capital-intensive production processes and regulatory compliance requirements. Competitive differentiation is increasingly driven by sustainability initiatives, cost efficiency, and advanced product offerings.

Yara International

Nutrien Ltd.

CF Industries Holdings Inc.

OCI N.V.

SABIC Agri-Nutrients Company

EuroChem Group

Indian Farmers Fertiliser Cooperative Limited (IFFCO)

Qatar Fertiliser Company (QAFCO)

Koch Fertilizer LLC

Coromandel International Limited

Yara International

Nutrien Ltd.

CF Industries Holdings Inc.

Technological advancements in the urea fertilizers market are increasingly focused on improving nutrient efficiency, reducing environmental impact, and optimizing production processes. Enhanced-efficiency fertilizers, including polymer-coated and sulfur-coated urea, have demonstrated up to 30% higher nitrogen utilization rates while reducing volatilization losses by nearly 25%. These innovations are particularly significant in regions with intensive farming, where nitrogen loss can exceed 35% under conventional practices. Nano-urea technology is emerging as a transformative solution, requiring application volumes that are nearly 90% lower than traditional granular urea while maintaining comparable yield outcomes.

On the production side, advancements in ammonia synthesis and urea manufacturing are improving energy efficiency and reducing emissions. Modern plants utilizing advanced catalysts and heat integration systems have achieved energy consumption reductions of approximately 15–20% per ton of urea produced. Additionally, the integration of carbon capture and utilization (CCU) technologies enables the recycling of up to 60% of carbon dioxide generated during ammonia production, significantly lowering the carbon footprint of fertilizer manufacturing.

Digital agriculture technologies are also playing a pivotal role in transforming fertilizer application. AI-driven soil analysis tools and satellite-based monitoring systems are enabling precision nutrient management, improving fertilizer application accuracy by nearly 20% and reducing input waste by up to 18%. Automation in fertilizer blending and distribution systems is enhancing supply chain efficiency, with logistics optimization reducing delivery times by approximately 12%. Emerging innovations such as green ammonia production using renewable energy sources are gaining traction, with pilot projects demonstrating up to 70% reduction in greenhouse gas emissions compared to conventional methods. These technological developments collectively position the urea fertilizers market toward a more sustainable, efficient, and data-driven future.

• In March 2025, Yara International announced the expansion of its green ammonia production project in Norway, targeting a reduction of up to 800,000 tons of CO₂ emissions annually through renewable-powered hydrogen integration into fertilizer production. Source: www.yara.com

• In January 2025, Nutrien Ltd. completed the upgrade of its nitrogen production facility in Canada, increasing operational efficiency by approximately 12% while implementing advanced emissions reduction systems to lower nitrogen oxide output. Source: www.nutrien.com

• In September 2024, CF Industries Holdings Inc. initiated a carbon capture and storage project at its Louisiana complex, designed to capture up to 2 million metric tons of CO₂ annually, significantly improving the sustainability profile of its urea production operations. Source: www.cfindustries.com

• In June 2024, OCI N.V. announced a strategic partnership to develop low-carbon ammonia export infrastructure, enabling large-scale supply of sustainable fertilizers and supporting global decarbonization efforts in agricultural inputs. Source: www.oci.nl

The Urea Fertilizers Market Report provides a comprehensive evaluation of the global industry across multiple dimensions, including product types, applications, technologies, and regional performance. The report covers key product categories such as granular, prilled, coated, and liquid urea, which collectively represent over 95% of total market consumption. It also examines application areas including agriculture, which accounts for more than 75% of usage, alongside industrial applications such as resins and automotive emissions control systems.

Geographically, the report analyzes five major regions—Asia-Pacific, North America, Europe, South America, and Middle East & Africa—capturing regional variations in fertilizer consumption, production capacity, and regulatory frameworks. Asia-Pacific alone contributes nearly half of global demand, while emerging markets in Africa show fertilizer usage growth exceeding 10% in certain agricultural zones. The study also highlights differences in fertilizer application rates, ranging from less than 90 kg per hectare in developing regions to over 150 kg per hectare in advanced agricultural economies.

The scope further includes an in-depth analysis of technological advancements such as controlled-release fertilizers, nano-urea innovations, and green ammonia production, which are reshaping industry standards. Additionally, the report evaluates supply chain dynamics, raw material dependencies, and trade flows influencing global distribution. Industry focus areas include sustainability initiatives, emission reduction strategies, and digital agriculture integration, offering decision-makers actionable insights into operational efficiency and long-term market positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Yara International, Nutrien Ltd., CF Industries Holdings Inc., OCI N.V., SABIC Agri-Nutrients Company, EuroChem Group, Indian Farmers Fertiliser Cooperative Limited (IFFCO), Qatar Fertiliser Company (QAFCO), Koch Fertilizer LLC, Coromandel International Limited, Yara International, Nutrien Ltd., CF Industries Holdings Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |