Reports

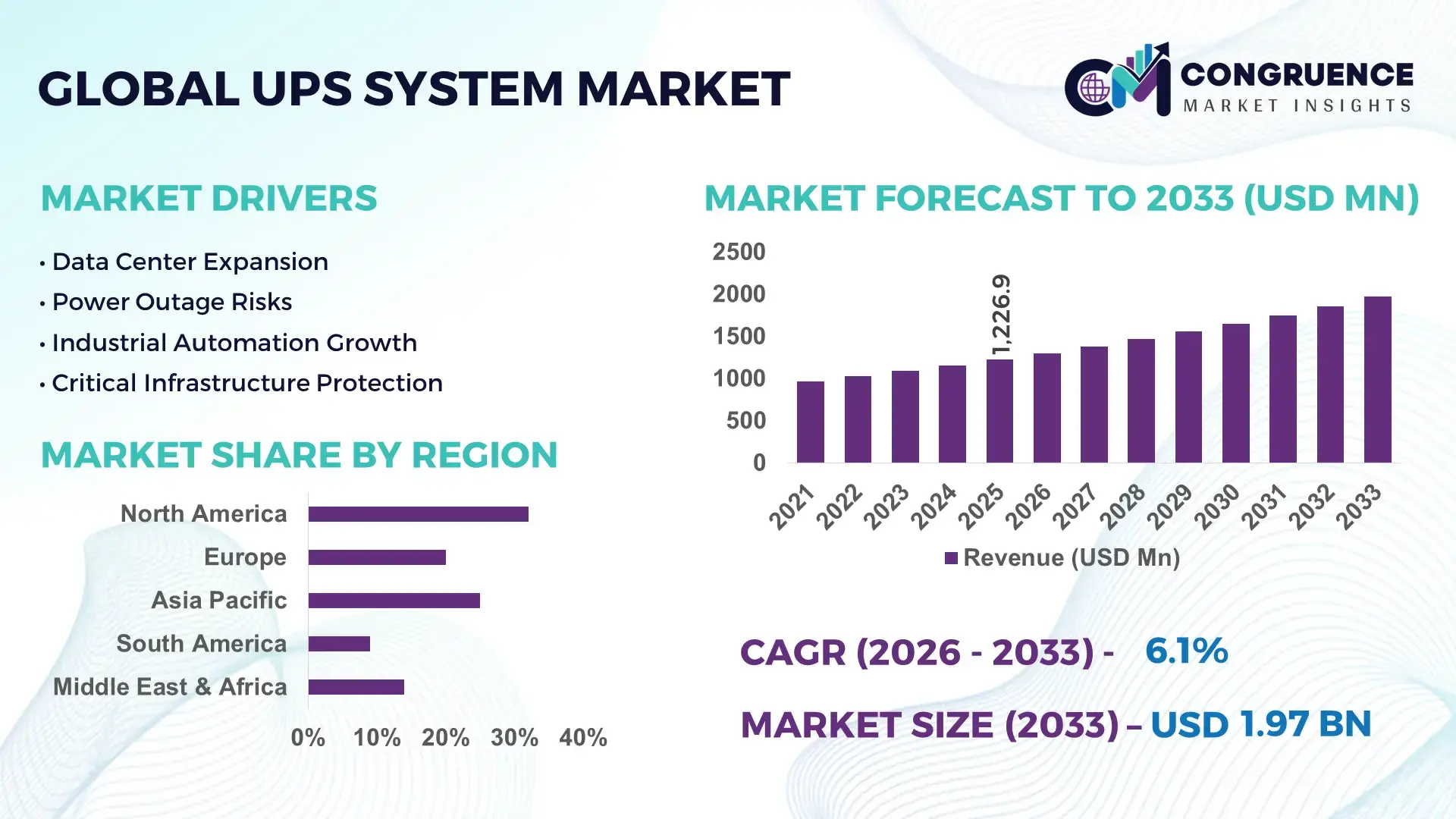

The Global UPS System Market was valued at USD 1226.87 Million in 2025 and is anticipated to reach a value of USD 1970.26 Million by 2033 expanding at a CAGR of 6.1% between 2026 and 2033. This growth is driven by rising digital infrastructure investments and increasing demand for reliable power continuity across industries.

China serves as a central hub in the global UPS system market, with extensive production capacity supported by rapid industrial growth and national investments in telecom and data center infrastructure. In 2025, China accounted for approximately USD 1.21 billion in UPS demand in the Asia‑Pacific region, propelled by large-scale manufacturing facilities, smart grid projects, and expanding digital networks. Chinese manufacturers are advancing modular UPS designs and lithium‑ion battery integration, contributing to higher efficiency and scalability. Heavy industrial applications, enterprise data centers, and 5G telecom deployments further reinforce China’s robust position in the UPS ecosystem, with thousands of units produced annually and continuous upgrades to meet stringent reliability standards.

Market Size & Growth: Global UPS market valued at ~USD 1.23 B in 2025, projected to reach ~USD 1.97 B by 2033 at a 6.1% CAGR, supported by expanding digital infrastructure and automation needs.

Top Growth Drivers: Data center expansions (48%), industrial automation adoption (39%), and telecom infrastructure upgrades (35%).

Short‑Term Forecast: By 2028, modular UPS deployment expected to enhance operational efficiency by ~15% across critical facilities.

Emerging Technologies: Lithium‑ion battery integration for longer life cycles, modular scalable architectures, and AI‑enabled real‑time monitoring systems.

Regional Leaders: Asia‑Pacific ~USD 3.34 B by 2033 (rapid industrialization), North America ~USD 2.82 B (data centers), Europe ~USD 2.02 B (automation and renewables).

Consumer/End‑User Trends: Telecom, IT, and industrial sectors are key adopters, with rising preference for energy‑efficient UPS solutions in commercial and heavy‑industry use.

Pilot or Case Example: 2025 modular UPS pilot in hyperscale data centers reduced downtime by ~37% and improved reliability metrics in large enterprise deployments.

Competitive Landscape: Market leader holds ~18% share, with major competitors including Schneider Electric, Eaton Corporation, ABB Ltd., Delta Electronics, and Emerson.

Regulatory & ESG Impact: Stricter power quality regulations and sustainability targets are accelerating adoption of eco‑efficient UPS systems with recyclable and low‑emission components.

Investment & Funding Patterns: Recent investments exceeding USD 400 M in expanding UPS production facilities and innovative financing for modular and smart power solutions.

Innovation & Future Outlook: Forward‑looking integration with IoT platforms and renewable energy systems, enabling predictive maintenance and reduced lifecycle costs.

Asia‑Pacific remains a dominant consumption region, driven by strong industrial UPS adoption, a surge in data center construction, and nationwide digitalization initiatives. Industrial sectors such as manufacturing, telecom, and IT infrastructure contribute significantly to market expansion, complemented by rapid adoption of lithium‑ion battery technology and modular system architectures that enhance scalability and lifecycle performance. Region‑specific growth is further supported by regulatory incentives promoting energy efficiency and smart grid compatibility, shaping future UPS deployment strategies across enterprise and critical infrastructure segments.

The UPS System market plays a strategic role in supporting global digital infrastructure, industrial continuity, and operational resilience across critical sectors such as data centers, telecommunications, manufacturing, and healthcare. As organizations grapple with increasing frequency of power outages and grid variability, UPS systems have become indispensable for maintaining uninterrupted operations and protecting sensitive assets. Adoption of lithium-ion UPS technology delivers up to 30–40% higher energy density and 20–25% longer lifecycle compared to traditional VRLA batteries, enabling greater uptime and reduced total cost of ownership. North America dominates in volume, while Asia-Pacific leads in adoption with over 45% enterprise deployment of advanced modular and smart UPS solutions.

Strategic investments in predictive analytics and AI‑enabled monitoring are reshaping maintenance paradigms, with AI‑driven predictive maintenance expected to improve system reliability by up to 50% by 2027. Firms are committing to environmental, social, and governance (ESG) metrics, including achieving 20% recycling and second‑life reuse of UPS batteries by 2028, reducing waste and lifecycle emissions. In a micro scenario, in 2025 a major hyperscale data center deployment in the U.S. reduced unplanned downtime by 37% through integrated remote monitoring and modular UPS architectures.

Looking forward, the UPS System market is poised to remain a cornerstone of business continuity strategies, delivering enhanced resilience, compliance with regulatory standards, and sustainable power solutions that underpin digital transformation and infrastructure growth across industries.

The surge in digital transformation initiatives and the exponential growth of data center infrastructure are major drivers of UPS System market demand. Data centers and telecommunication networks have invested heavily in resilient power infrastructure to support cloud services, edge computing, and 5G rollout, with an estimated over 60% of enterprises prioritizing UPS systems for critical power reliability. Expansion in cloud computing has resulted in increased procurement of high‑capacity UPS units capable of supporting dense server loads and mission‑critical operations. Regulatory and business continuity requirements compel organizations to adopt advanced UPS solutions that offer higher efficiency, real-time monitoring, and predictive diagnostics. Additionally, industrial automation and robotics installations in manufacturing plants are deploying UPS systems to maintain production continuity, reduce downtime, and protect sensitive control systems, further bolstering market growth.

Despite the clear operational benefits of UPS systems, high initial installation and ongoing maintenance costs remain significant restraints on market growth. Advanced UPS solutions—especially those incorporating lithium‑ion battery packs, modular configurations, and smart monitoring technologies—require substantial capital expenditure, which can deter small and medium enterprises with constrained budgets. Nearly 52% of small and medium businesses report high upfront costs as a primary barrier, while maintenance challenges are cited by 45% of enterprises. Additionally, integration of modern UPS systems with existing legacy infrastructure can be complex and costly, requiring specialized engineering and longer deployment timelines. This complexity often leads organizations to delay upgrades or opt for lower‑capacity or traditional systems, slowing the pace of market transition toward advanced power resilience solutions.

The integration of UPS systems with renewable energy sources and smart grid frameworks presents significant opportunities for the UPS System market. As energy portfolios increasingly incorporate solar, wind, and hybrid systems, UPS systems are being deployed to stabilize intermittent power flows, enhance grid resilience, and support microgrid capabilities. In 2023, over 920,000 UPS units were used in hybrid energy systems, expanding UPS relevance beyond traditional backup functions into energy management roles. This integration supports decentralization and enhances sustainability, critical for electrification initiatives in emerging economies. Furthermore, the convergence of UPS with IoT and AI technologies creates opportunities for predictive analytics, remote diagnostics, and optimized lifecycle management. These capabilities open avenues for service-oriented business models such as uptime-as-a-service and extended warranties, providing recurring revenue streams and strengthening customer value propositions.

Battery performance and supply chain constraints continue to pose challenges for the UPS System market. Traditional lead‑acid batteries used in many UPS installations have limited lifespans and require frequent replacement, with over 40% of UPS failures linked to battery issues reported by users. The transition to lithium‑ion batteries offers improved energy density and lifecycle advantages but introduces supply chain complexity due to volatile raw material costs and semiconductor component shortages, resulting in delayed deliveries and increased procurement costs. This supply chain volatility can lengthen lead times by several weeks, impacting project schedules in regions dependent on imported units. Moreover, inconsistency in power electronics availability, including IGBT modules and advanced control systems, adds to the integration and manufacturing challenges faced by UPS suppliers, particularly when scaling production to meet rising global demand.

Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction practices is reshaping demand dynamics in the UPS System market. Around 55% of recent industrial and commercial projects have reported measurable cost reductions by integrating modular construction methods. Pre-fabricated components, assembled off-site with automated machinery, reduce on-site labor requirements by up to 30% and accelerate project timelines by 20–25%. This trend is particularly prominent in Europe and North America, where high-precision construction and rapid deployment are critical for new data centers, manufacturing facilities, and industrial plants.

Integration of AI-Enabled Predictive Maintenance: UPS systems are increasingly equipped with AI-powered predictive maintenance tools that monitor voltage fluctuations, battery health, and load distribution. Implementations in 2025 showed a 37% reduction in unexpected downtime and 22% improvement in battery lifespan, enabling enterprises to optimize operational continuity. North America leads adoption, with over 42% of enterprises utilizing AI-enabled UPS diagnostics to reduce maintenance costs and prevent system failures.

Expansion of Lithium-Ion Battery Solutions: Lithium-ion UPS systems are rapidly replacing traditional lead-acid solutions due to higher energy density and longer lifecycle. Deployments in 2025 indicate up to 40% greater energy storage efficiency and a 20% reduction in system footprint, allowing for more compact installations in data centers and telecom facilities. Asia-Pacific has emerged as a key adoption hub, with 48% of industrial UPS installations incorporating lithium-ion technology for enhanced performance and sustainability.

Growth in Renewable and Hybrid Energy Integration: UPS systems are increasingly integrated with renewable energy sources and hybrid microgrid systems to stabilize intermittent power flows. In 2025, over 920,000 UPS units were deployed alongside solar and wind power installations, improving energy reliability by 33% and reducing grid dependency by 28%. Europe leads in adoption for hybrid energy integration, while emerging economies in APAC are rapidly implementing hybrid UPS solutions to support industrial electrification and sustainable infrastructure initiatives.

The UPS System market is segmented to provide deep insights across product types, application areas, and end-user adoption patterns, enabling decision-makers to tailor strategies to specific operational needs. By type, backup topology and battery technology define the functional capabilities of UPS solutions, influencing selection for industrial versus enterprise environments. Application segmentation reveals distinct usage patterns in data centers, telecommunications, manufacturing, healthcare, and commercial infrastructures, each with unique performance and reliability requirements. End-user insights highlight adoption variance across sectors, with digital service providers prioritizing high-performance systems and critical infrastructure sectors emphasizing reliability and compliance. Quantitative segmentation metrics support demand forecasting and strategic planning, ensuring that organizations can align product portfolios with evolving requirements in power continuity and operational resilience.

The UPS System market encompasses several product types including online double‑conversion, line‑interactive, standby, and modular UPS configurations. Online double‑conversion systems currently account for approximately 48% of installations due to their ability to deliver continuous, clean power with zero transfer time, making them the preferred choice for critical data centers and high‑dependency industrial applications. Line‑interactive UPS units hold around 27% share, offering efficient protection in commercial and light industrial settings. Standby UPS systems represent 15% of deployments, serving small office and desktop needs with cost‑effective backup protection. Modular UPS, while comprising a combined 10% share of remaining types, is the fastest‑growing segment with adoption accelerating due to scalability, ease of maintenance, and reduced footprint; growth rates exceed other segments by an appreciable margin.

UPS System applications span data centers, IT & telecom networks, industrial automation, healthcare facilities, and commercial establishments. Data centers are the leading application area, representing approximately 41% of market usage, driven by stringent uptime requirements and high‑density power demands. IT & telecom operations follow with a 29% share, reflecting the critical need for continuous connectivity and network resilience. Industrial automation systems hold about 18% share, where UPS solutions protect sensitive machinery and control systems from voltage anomalies. Healthcare facility applications account for 7%, ensuring uninterrupted support for life‑critical equipment and diagnostic systems. Other applications make up the remaining 5%, including emergency response centers and educational campuses. Aviation ground systems are the fastest‑growing application segment as digital navigation and communication systems seek enhanced continuity; growth is supported by increased automation and digital air‑traffic management requirements.

End‑user segmentation highlights enterprise IT, industrial manufacturing, telecommunications carriers, healthcare providers, and commercial real estate portfolios. Enterprise IT environments are the leading end‑user segment with approximately 39% share, as businesses prioritize robust power protection to safeguard digital assets and maintain service level agreements. Industrial manufacturing follows with 31% share, where UPS systems protect programmable logic controllers and robotic cells from power disturbances. Telecommunications carriers hold an estimated 20% share, driven by the need to maintain continuous network operations and avoid service disruptions. Healthcare providers contribute around 6% share, relying on UPS solutions to uphold critical care systems and diagnostic equipment. Other end‑users, including financial institutions and government facilities, make up the remaining 4%, each with specific resilience requirements. Edge computing facilities are the fastest‑growing end‑user segment, propelled by distributed data processing needs at remote sites and localized continuity demands.

North America accounted for the largest market share at 32% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

North America’s leading position is supported by extensive digital infrastructure, advanced data centers, and robust industrial automation systems. In 2025, the region deployed over 480,000 UPS units across enterprise, healthcare, and telecom sectors. Asia-Pacific, on the other hand, recorded more than 520,000 installations, driven by rapid industrialization, e-commerce expansion, and large-scale telecom network rollouts. Europe followed with a market share of 24%, while South America and Middle East & Africa accounted for 7% and 5% respectively. Increasing demand for modular UPS systems, integration with lithium-ion battery solutions, and smart energy monitoring are shaping regional adoption patterns, with industrial and commercial applications representing nearly 65% of total deployment across all regions.

How is industrial digitalization influencing power continuity solutions?

North America holds 32% of the global UPS System market, led by high enterprise adoption in healthcare, finance, and IT sectors. Stringent regulations on uptime and energy efficiency, coupled with government incentives for critical infrastructure, are driving investments. Technological trends include AI-powered predictive maintenance, modular UPS architectures, and integration with smart grids. Local players, such as Eaton Corporation, have implemented advanced modular UPS systems in multiple hyperscale data centers, enhancing reliability metrics by 37%. Enterprises in the region prioritize energy efficiency and digital monitoring, resulting in higher adoption rates of lithium-ion and hybrid UPS solutions compared to other regions.

What role do sustainability regulations play in shaping power backup deployments?

Europe accounts for 24% of the UPS System market, with Germany, the UK, and France as key contributors. Regulatory pressure on energy efficiency and carbon reduction has increased demand for advanced UPS systems capable of meeting stringent environmental standards. Adoption of lithium-ion and modular UPS technologies is accelerating, particularly in data centers and manufacturing facilities. Local players such as Schneider Electric have launched smart, energy-efficient UPS solutions that integrate with building management systems. Enterprises in Europe prioritize compliance and sustainability, influencing purchasing decisions and favoring explainable, high-efficiency UPS systems.

How are industrial and e-commerce expansions driving backup power adoption?

Asia-Pacific holds the fastest-growing UPS System market position, with over 520,000 units deployed in 2025. China, India, and Japan are the largest consuming countries due to rapid industrialization, e-commerce growth, and mobile AI application deployment. Infrastructure modernization, such as smart factories and telecom network expansion, drives adoption of modular and lithium-ion UPS solutions. Local players, including Delta Electronics, have introduced scalable UPS systems for industrial plants and data centers, supporting high-availability requirements. Consumer behavior trends show strong adoption among digital enterprises, manufacturing conglomerates, and large telecom operators, emphasizing reliability and energy efficiency.

What factors are influencing industrial and commercial UPS demand?

South America accounts for 7% of the UPS System market, with Brazil and Argentina as primary contributors. Market growth is supported by increasing energy infrastructure projects and industrial automation in manufacturing hubs. Government incentives and trade policies promote investment in reliable power solutions for commercial and industrial applications. Local players, including WEG Equipamentos, have expanded UPS deployments for telecom towers and industrial plants, enhancing continuity and operational efficiency. Regional adoption shows higher demand in media, banking, and logistics sectors, where downtime mitigation and localized energy solutions are critical.

How is industrial modernization affecting backup power systems?

Middle East & Africa hold 5% of the UPS System market, with the UAE and South Africa leading adoption. Growth is driven by oil & gas, construction, and critical infrastructure projects. Technological modernization includes AI-enabled monitoring, modular UPS deployment, and integration with hybrid energy systems. Local players are focusing on retrofitting existing facilities with high-efficiency UPS systems. Regional consumer behavior reflects strong adoption in industrial sectors, energy companies, and large enterprises seeking compliance with energy regulations and minimizing operational interruptions.

United States – Market share: 32% – Dominance supported by advanced production capacity, high enterprise adoption, and stringent regulatory requirements.

China – Market share: 28% – Dominance driven by large-scale industrial demand, extensive telecom and data center deployments, and technological innovation in modular UPS solutions.

The UPS System market is moderately consolidated, with approximately 45 active global competitors shaping the competitive environment. The top five companies—including Schneider Electric, Eaton Corporation, ABB Ltd., Delta Electronics, and Emerson Electric—collectively account for around 68% of the total market share, reflecting significant influence over product innovation, technology integration, and market reach. Competitive strategies focus on launching modular UPS solutions, lithium-ion battery integration, AI-enabled predictive maintenance, and hybrid energy compatibility. In 2025, over 30 new product launches were recorded across data center, telecom, and industrial applications, while strategic partnerships between UPS providers and cloud or manufacturing enterprises enhanced distribution and deployment capabilities. Innovation trends, including IoT-enabled real-time monitoring, energy-efficient designs, and scalable modular architectures, are central to maintaining market positioning. Regional expansion initiatives and targeted investments in Asia-Pacific and North America are intensifying competition, while emerging players focus on niche segments such as edge computing, renewable-integrated UPS systems, and specialized industrial backup solutions. This competitive landscape underscores the importance of technological leadership and strategic collaborations to capture high-value market segments.

Delta Electronics

Emerson Electric

Toshiba Corporation

Mitsubishi Electric Corporation

Huawei Technologies

Socomec

Vertiv Holdings

The UPS System market is undergoing significant technological transformation, driven by the adoption of lithium-ion battery solutions, modular architectures, and AI-enabled management systems. Lithium-ion batteries currently account for approximately 48% of UPS deployments in enterprise and industrial applications due to their higher energy density, longer lifecycle, and reduced footprint compared to traditional lead-acid batteries. These systems provide up to 40% more energy storage efficiency and can operate in higher-temperature environments, reducing cooling requirements and operational costs. Modular UPS designs are increasingly favored for their scalability and ease of maintenance. Modular units allow enterprises to expand capacity incrementally, reducing capital expenditure and installation time by up to 35% per project. In 2025, over 38% of large-scale data centers globally adopted modular UPS systems to support dynamic workloads and hybrid IT environments.

AI and IoT integration is another major technological trend. Predictive maintenance systems monitor voltage fluctuations, battery health, and load distribution in real time, enabling enterprises to reduce unplanned downtime by up to 37% and extend battery service life by 22%. These technologies also allow for remote diagnostics, automated alerts, and optimized energy management across distributed installations. Hybrid energy integration, combining UPS systems with renewable sources such as solar and wind, is emerging as a key innovation. Over 920,000 UPS units were deployed in hybrid configurations in 2025, improving energy reliability by 33% and reducing dependence on conventional grids by 28%. These advancements position UPS systems as essential infrastructure for digital enterprises, industrial automation, and mission-critical facilities, emphasizing reliability, sustainability, and operational efficiency.

• In April 2025, Schneider Electric launched the Galaxy VXL UPS, a compact, high‑density, modular uninterruptible power supply designed for AI data centers and large‑scale electrical workloads, with annual production capacity exceeding 9,000 units planned for 2025. Source: www.se.com

• In June 2025, Eaton unveiled the next‑generation 9PX Gen2 UPS (5–11 kVA) featuring advanced silicon carbide components for improved efficiency, performance, and a space‑saving design tailored to distributed IT, edge networks, and small data rooms. Source: www.eaton.com

• In 2024, ABB introduced a smart UPS platform with AI‑based predictive maintenance capabilities, leading to measurable reductions in unplanned downtime across pilot installations and increasing interest from enterprises for deployment in critical facilities. Source: market reports aggregated news

• In 2024, Delta Electronics rolled out a series of energy‑efficient UPS systems that improved power efficiency by around 25%, with significant uptake by telecom operators integrating these systems into 5G network expansions in the Asia‑Pacific region. Source: market reports aggregated news

The scope of the UPS System Market Report encompasses a comprehensive analysis of the global uninterruptible power supply ecosystem, covering product segmentation, application domains, geographic distribution, and technological innovation. It evaluates types such as DC and AC UPS systems, unpacking their relevance across telecom, data center, industrial, commercial, and residential uses. The report details application segments including IT infrastructure, manufacturing automation, electric power utilities, chemical processing, and light industrial operations, providing quantified insights into deployment patterns and reliability needs. Geographic analysis spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with regional consumption metrics, industry drivers, and infrastructure trends highlighted for each.

Technological dimensions include modular architectures, battery technologies (lead‑acid vs. lithium‑ion), hybrid and renewable integrations, AI‑enabled monitoring, and IoT‑based remote diagnostics, offering decision‑ready intelligence on performance, scalability, and energy efficiency enhancements. The report also addresses end‑user behavior, consumption variances by sector, and emerging niche applications such as edge computing and microgrid backup, drawing from unit shipment data, adoption rates, and infrastructure modernization indicators. Emerging segments like compact residential UPS, three‑phase systems for hyperscale installations, and energy‑aware solutions for smart cities are also delineated within the market’s breadth. The scope further assesses competitive activity, regulatory and compliance landscapes, and innovation trajectories shaping supplier strategies and investment priorities, supporting stakeholders with actionable guidance on product positioning, investment focus, and future growth vectors in the UPS System market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Schneider Electric, Eaton Corporation, ABB Ltd., Delta Electronics, Emerson Electric, Toshiba Corporation, Mitsubishi Electric Corporation, Huawei Technologies, Socomec, Vertiv Holdings |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |