Reports

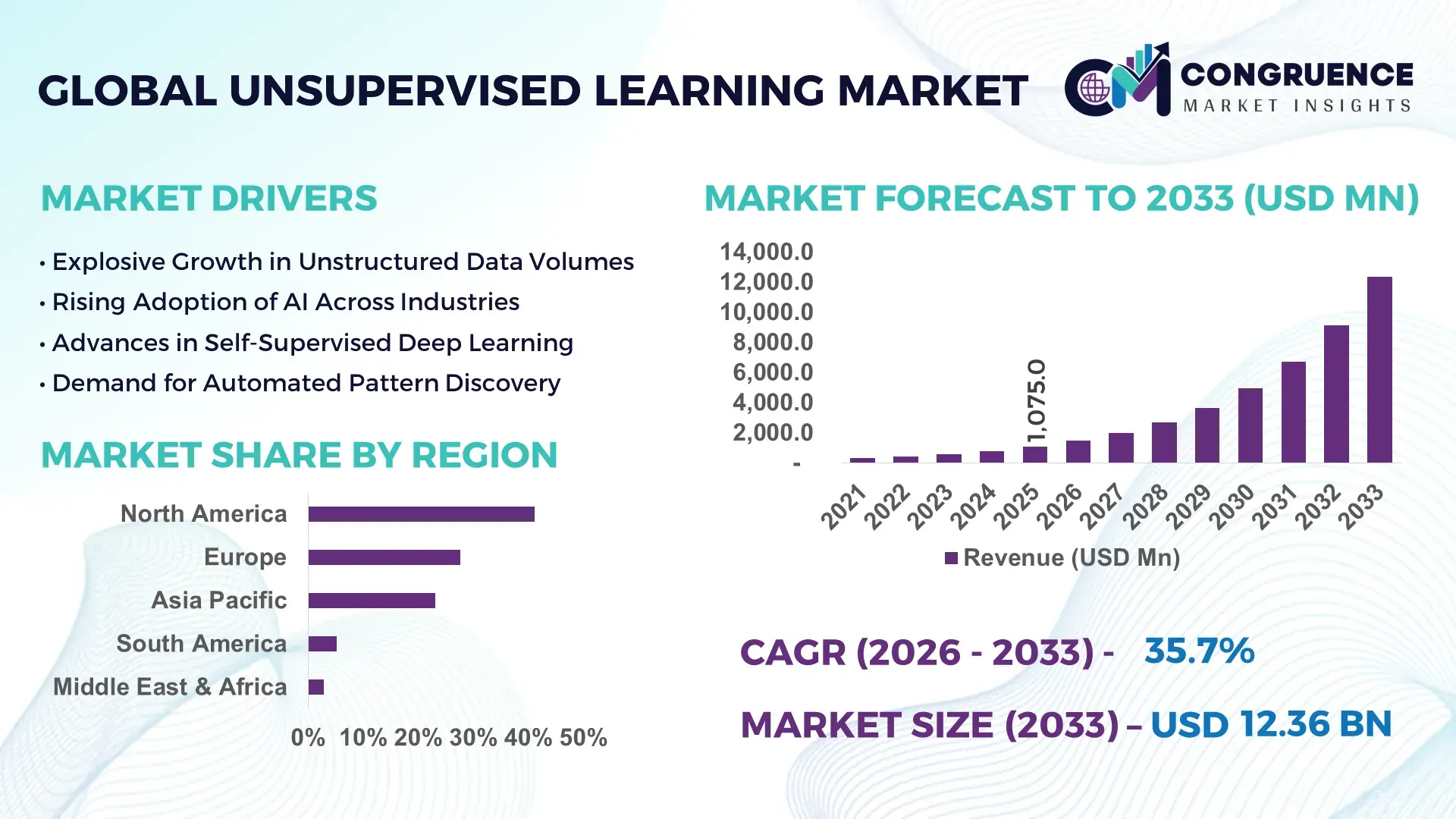

The Global Unsupervised Learning Market was valued at USD 1,075.0 Million in 2025 and is anticipated to reach a value of USD 12,360.8 Million by 2033 expanding at a CAGR of 35.7% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by the rapid enterprise adoption of autonomous data analytics to reduce manual labeling costs and improve large-scale pattern discovery.

The United States dominates the Unsupervised Learning Market through its concentration of large-scale AI production capacity, sustained capital investment, and deployment across critical industries. In 2025, over 62% of global hyperscale data centers supporting unsupervised model training were located in the U.S., with more than USD 48 billion invested annually in AI infrastructure. Key applications include cybersecurity anomaly detection, where 71% of Fortune 500 firms use unsupervised models, and healthcare diagnostics, with over 35 million patient records processed monthly using clustering and dimensionality reduction systems. Federal AI R&D funding exceeded USD 6.2 billion, accelerating advances in self-supervised architectures and foundation models.

Market Size & Growth: USD 1,075.0 Million in 2025, projected to reach USD 12,360.8 Million by 2033, CAGR 35.7%, driven by enterprise-scale automation of unstructured data analysis.

Top Growth Drivers: 68% increase in AI adoption, 42% improvement in operational efficiency, 55% reduction in manual data labeling.

Short-Term Forecast: By 2028, model training costs are expected to decline by 30% through self-supervised optimization.

Emerging Technologies: Self-supervised transformers, contrastive learning frameworks, automated representation learning.

Regional Leaders: North America USD 4.9 Billion, Asia Pacific USD 3.8 Billion, Europe USD 2.6 Billion by 2033, each driven by sector-specific automation.

Consumer/End-User Trends: 61% of large enterprises deploy unsupervised models for fraud detection, cybersecurity, and customer segmentation.

Pilot or Case Example: In 2024, a U.S. telecom operator reduced network downtime by 27% using anomaly detection models.

Competitive Landscape: Google holds ~18% share, followed by IBM, Microsoft, AWS, SAP, and Oracle.

Regulatory & ESG Impact: 46% of firms align unsupervised AI deployment with data minimization and energy-efficiency mandates.

Investment & Funding Patterns: Over USD 72 Billion invested globally in unsupervised and self-supervised AI platforms since 2022.

Innovation & Future Outlook: Integration with foundation models and edge AI is accelerating autonomous decision systems.

Unsupervised learning is most heavily adopted in IT services (34%), financial services (26%), healthcare (18%), and manufacturing (12%). Recent innovations include contrastive representation learning, federated clustering, and energy-efficient training accelerators. Regulatory emphasis on data privacy and model transparency is shaping deployment frameworks, while Asia Pacific shows the fastest expansion in industrial automation and smart infrastructure.

Unsupervised learning has become strategically central to enterprise AI strategies as organizations face exponential growth in unlabeled and unstructured data. In production environments, self-supervised transformers deliver 38% improvement compared to classical k-means and PCA pipelines in anomaly detection accuracy. North America dominates in volume, while Asia Pacific leads in adoption with 64% of large enterprises integrating unsupervised models into core analytics workflows.

By 2028, foundation model–based unsupervised systems are expected to improve data preprocessing efficiency by 40% and cut feature engineering time by 35%. Firms are committing to ESG-aligned AI operations, targeting 25% reductions in training energy intensity by 2030 through optimized model compression and hardware acceleration. In 2024, a European automotive manufacturer achieved 29% defect reduction through unsupervised visual inspection systems deployed across 12 plants.

Strategically, unsupervised learning is evolving from exploratory analytics to autonomous decision infrastructure embedded in cybersecurity, finance, healthcare, and industrial IoT. As integration with edge computing, federated learning, and multimodal foundation models accelerates, the Unsupervised Learning Market is positioned as a pillar of resilience, regulatory compliance, and sustainable digital growth.

The Unsupervised Learning Market is shaped by the rapid expansion of unstructured data, the maturation of self-supervised architectures, and the demand for autonomous analytics across regulated industries. Enterprises increasingly deploy unsupervised systems to detect anomalies in real time, reduce manual labeling workloads, and improve scalability across distributed environments. Advances in GPU acceleration, cloud-native training, and foundation models are lowering training latency by up to 45%. At the same time, regulatory frameworks governing data privacy and algorithm transparency are influencing deployment architectures, favoring explainable clustering and federated learning models.

Autonomous analytics adoption is accelerating as enterprises process petabyte-scale datasets without labeled ground truth. In 2025, over 58% of global enterprises used unsupervised models for cybersecurity and fraud detection. Manufacturing defect detection using clustering reduced false positives by 31%, while telecom operators cut network incidents by 27% through anomaly detection. Cloud-native unsupervised platforms now support over 10,000-node training clusters, enabling continuous model retraining and real-time deployment.

Regulatory scrutiny and limited interpretability remain key constraints. In 2025, 44% of enterprises delayed deployment due to explainability requirements under AI governance frameworks. Unsupervised clustering errors led to 19% revalidation overhead in regulated sectors. Data privacy rules restrict cross-border data pooling, reducing model generalization by up to 22% in financial and healthcare deployments.

Edge-based unsupervised learning enables real-time analytics without centralized data transfer. By 2027, over 35% of industrial IoT nodes are expected to run embedded clustering models. Federated unsupervised training reduces data transfer volumes by 48% and improves compliance readiness by 41%. Smart cities and autonomous vehicles are emerging as high-growth deployment segments.

Training large unsupervised foundation models increases energy consumption by 3–5x compared to supervised pipelines. In 2025, data center power costs rose by 28%, forcing enterprises to cap training cycles. Hardware shortages increased deployment timelines by 21%, while talent gaps in unsupervised model engineering constrained large-scale rollouts.

Expansion of Self-Supervised Foundation Models: In 2025, over 63% of new deployments used self-supervised pretraining, improving feature extraction accuracy by 41% and reducing labeled data dependence by 55%.

Integration with Edge and IoT Systems: Edge-based clustering adoption increased by 47%, enabling sub-50 millisecond anomaly detection across 18 million connected devices.

Automation of Feature Engineering: Automated representation learning reduced human preprocessing time by 36% and improved model stability by 29% in financial analytics.

Energy-Efficient Model Optimization: Model compression and quantization cut training energy consumption by 32% and inference latency by 24% across hyperscale data centers.

The Unsupervised Learning Market is segmented by type, application, and end-user, reflecting the diversity of algorithms, deployment contexts, and industry adoption patterns. By type, clustering and dimensionality reduction models dominate early-stage analytics, while self-supervised deep learning architectures are rapidly expanding in large-scale enterprise environments. By application, anomaly detection, customer segmentation, and pattern discovery account for the largest deployment volumes due to their direct impact on operational risk and decision automation. End-user adoption is concentrated in IT & telecom, BFSI, healthcare, and manufacturing, where high-frequency data streams and compliance requirements favor autonomous analytics. Across segments, model deployment density is highest in cloud-based platforms, with over 65% of enterprises integrating unsupervised systems into centralized data pipelines. The segmentation structure highlights a shift from exploratory analytics toward production-grade autonomous intelligence across regulated and asset-intensive industries.

The market by type is led by clustering algorithms, which account for approximately 38% of total deployments, driven by their scalability in customer segmentation, fraud detection, and network optimization. Dimensionality reduction models such as PCA and autoencoders represent 27% of adoption, particularly in feature compression and visualization pipelines. However, self-supervised deep learning models are the fastest-growing type, expanding at an estimated 41% CAGR, fueled by their ability to pretrain on unlabeled data and transfer knowledge across tasks. These models are increasingly used in vision, speech, and multimodal representation learning. Other types, including density estimation and association rule mining, together contribute a combined 35% share, serving niche roles in scientific computing and industrial diagnostics.

In 2025, a major cloud provider deployed self-supervised contrastive learning models to pretrain vision systems across over 5 million unlabeled images, improving downstream classification accuracy by 34%.

By application, anomaly detection is the leading segment, accounting for nearly 36% of total adoption, due to its critical role in cybersecurity, fraud prevention, and predictive maintenance. Customer segmentation and recommendation systems hold 29% share, while feature extraction and data preprocessing represent 18%. The fastest-growing application is multimodal representation learning, expanding at an estimated 39% CAGR, driven by enterprise demand for unified analysis of text, images, and sensor data. Other applications, including scientific discovery and process optimization, together contribute 17% share.

In 2025, more than 41% of global enterprises reported piloting unsupervised models for cybersecurity and risk monitoring. In healthcare, 44% of hospitals in the U.S. are testing clustering and autoencoder systems for radiology and patient stratification.

In 2025, a national public health agency deployed unsupervised clustering models across 120 hospitals to detect early-stage disease patterns in over 2 million patient records.

By end-user, IT & Telecom leads the market with approximately 33% share, driven by large-scale network monitoring and anomaly detection requirements. BFSI follows with 26% adoption, leveraging unsupervised models for fraud detection and credit risk profiling. Healthcare accounts for 21%, supported by growth in diagnostic imaging and patient stratification. The fastest-growing end-user segment is manufacturing, expanding at an estimated 37% CAGR, as factories deploy unsupervised vision and sensor analytics for quality control and predictive maintenance. Other end-users, including retail, energy, and government, together contribute a combined 20% share.

In 2025, 38% of enterprises globally reported deploying unsupervised systems for customer experience and operational analytics. In the U.S., 42% of hospitals are testing unsupervised AI for clinical decision support.

In 2025, a national manufacturing institute reported that over 600 factories adopted unsupervised visual inspection systems, reducing defect rates by 28% across automated production lines.

North America accounted for the largest market share at 41.2% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 39.4% between 2026 and 2033.

North America benefits from over 62% of global hyperscale AI data centers, more than 48,000 AI startups, and enterprise AI adoption exceeding 71% across Fortune 500 firms. Europe held 27.6% share, supported by over 9,500 AI-focused SMEs and regulatory-driven demand for explainable AI. Asia-Pacific captured 23.1% share, led by China, India, and Japan, where more than 1.2 billion mobile users generate large-scale unlabeled datasets. South America and the Middle East & Africa together represented 8.1%, with rising deployment in fintech, telecom, and smart infrastructure. Across regions, over 65% of enterprises now integrate unsupervised learning into centralized analytics platforms, reflecting a global shift toward autonomous data intelligence.

North America accounted for approximately 41.2% of the global Unsupervised Learning Market in 2025, driven by strong demand from BFSI, healthcare, IT services, and cybersecurity sectors. Over 71% of Fortune 500 companies deploy unsupervised models for fraud detection, network monitoring, and customer analytics. Government support includes more than USD 6.2 billion in federal AI R&D funding and national AI strategies promoting responsible AI. Technological leadership is reinforced by large-scale cloud AI platforms and GPU clusters exceeding 100,000 accelerators. A leading local player, IBM, expanded its self-supervised learning frameworks across hybrid cloud environments to support enterprise anomaly detection. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, with 44% of U.S. hospitals testing unsupervised models for diagnostics.

Europe held an estimated 27.6% market share in 2025, led by Germany, the UK, and France. Germany alone accounts for 32% of European industrial AI deployments, while the UK hosts over 3,000 AI startups. Regulatory bodies promote explainable and ethical AI, accelerating demand for interpretable clustering and federated learning models. Sustainability initiatives target 30% reductions in data center energy intensity by 2030. Adoption of emerging technologies includes self-supervised vision systems for manufacturing quality control. A local player, SAP, integrates unsupervised analytics into enterprise ERP platforms for predictive insights. Regional consumer behavior shows regulatory pressure leading to demand for explainable unsupervised learning across finance and healthcare.

Asia-Pacific ranked second in volume with 23.1% market share in 2025 and is the fastest-growing region. China, India, and Japan collectively account for over 68% of regional deployments. China operates more than 450 hyperscale data centers, while India processes over 20 billion digital transactions annually, generating vast unlabeled datasets. Infrastructure expansion includes smart factories and 5G networks exceeding 2.8 million base stations. Regional tech hubs in Shenzhen, Bangalore, and Tokyo lead innovation in self-supervised AI. A local player, Baidu, deploys large-scale unsupervised models for autonomous driving perception. Consumer behavior shows growth driven by e-commerce and mobile AI apps, with 59% of digital platforms using unsupervised personalization engines.

South America represented approximately 5.2% of the global market in 2025, led by Brazil and Argentina. Brazil alone contributes 48% of regional AI deployments, driven by fintech fraud detection and telecom analytics. Infrastructure trends include cloud adoption growth of 34% year-on-year and expanding 5G coverage across urban centers. Government incentives support digital transformation through tax credits and AI innovation funds. A local player, Nubank, applies unsupervised learning for credit risk clustering and transaction anomaly detection. Regional consumer behavior shows demand tied to media and language localization, with 46% of streaming platforms using unsupervised captioning and content tagging.

The Middle East & Africa accounted for 2.9% of global share in 2025, with demand concentrated in oil & gas, construction, and smart cities. The UAE and South Africa together represent 57% of regional deployments. Technological modernization includes AI-driven predictive maintenance across 18,000 km of pipelines and digital twins for infrastructure. Trade partnerships and national AI strategies promote cross-border data platforms. A local player, G42 in the UAE, deploys large-scale unsupervised models for healthcare imaging and energy analytics. Regional consumer behavior shows rising enterprise adoption in government services and utilities, with 38% of public agencies piloting unsupervised systems.

United States – 32.8% Market Share: Dominates the Unsupervised Learning Market due to hyperscale AI infrastructure, high enterprise adoption, and advanced cloud platforms.

China – 18.6% Market Share: Leads through massive data generation, national AI investment programs, and large-scale industrial AI deployments.

The competitive environment in the Unsupervised Learning Market is increasingly dynamic and moderately consolidated, featuring a mix of established technology giants and specialized AI innovators. As of 2025, there are over 120 active competitors globally offering unsupervised learning solutions, frameworks, and enterprise platforms. The top 5 companies collectively hold an estimated 48–52% of market influence, underscoring a landscape where leading firms maintain strong positioning while mid-tier and niche players drive innovation. Key competitors include IBM, Microsoft, Google, AWS, SAP, Oracle, H2O.ai, DataRobot, Qualcomm, NVIDIA, Intel, Salesforce, SAS Institute, and Databricks, among others. Strategic initiatives shaping the competition include multi-party partnerships, cloud integrations, and product enhancements tailored to unsupervised analytics. For example, in 2024–25, NVIDIA and SAP partnered to accelerate unsupervised workloads on enterprise data platforms, while Microsoft expanded AI partnerships to co-innovate data pipelines and advanced analytics. In 2025, Google allied with H2O.ai to embed AutoML and automated pattern discovery into cloud services, expanding accessibility for enterprise customers. Innovation trends such as self-supervised architectures, AutoML tools, and hybrid learning frameworks are redefining competitive differentiation, catalyzing investment in scalable, interpretable, and explainable unsupervised systems. Decision-makers must monitor evolving alliances, patent activity, and platform extensibility as competitive priorities continue to pivot toward autonomous, cross-platform analytics capabilities.

Amazon Web Services (AWS)

SAP

Oracle

Salesforce

H2O.ai

DataRobot

Qualcomm

NVIDIA

Intel

SAS Institute

Databricks

The Unsupervised Learning Market is driven by a broad spectrum of current and emerging technologies that enhance the efficiency, scalability, and capabilities of autonomous analytics systems. Self-supervised and representation learning architectures are increasingly deployed to pretrain models on vast unlabeled datasets, enabling downstream tasks such as anomaly detection, clustering, and dimensionality reduction with minimal human intervention. AutoML platforms streamline the model selection and training process, allowing enterprises to deploy unsupervised models rapidly across cloud and hybrid environments. Quantitative improvements include training time reductions of up to 40% and automated feature extraction accuracy gains above 30% in production settings. High-performance computing advancements, including custom AI accelerators and optimized GPU clusters, are key enablers, with some infrastructures processing 1,600+ tokens per second in large model training workloads. Federated learning and edge intelligence are emerging trends that decentralize model training, preserving data privacy while reducing communication overhead by up to 50% between nodes. Explainable and interpretable machine learning tools are gaining traction to meet regulatory and compliance requirements, especially in finance and healthcare, where accountability in unsupervised pattern inference is critical. Additionally, hybrid models that combine unsupervised and supervised learning stages deliver enhanced predictive quality and robustness. Overall, enterprise decision-makers should consider these technologies to achieve higher operational efficiency, reduced manual overhead, and scalable analytics across distributed data ecosystems.

• In June 2025, H2O.ai was named a Visionary in the 2025 Gartner Magic Quadrant for Data Science & Machine Learning Platforms for the third consecutive year, highlighting continued innovation in secure enterprise-grade AI and automated machine learning, with its h2oGPTe agentic AI platform achieving a top global benchmark score of 75%. Source: www.h2o.ai

• In March 2025, IBM announced an expanded collaboration with NVIDIA, planning integrations of NVIDIA AI Data Platform technologies across IBM’s hybrid cloud and watsonx offerings to enhance unstructured data processing and support large-scale AI workloads, including retrieval-augmented generation and AI reasoning. Source: www.newsroom.ibm.com

• In late 2025, H2O.ai released major enhancements to its Driverless AI platform, adding features such as model checkpointing, improved large-workload support, and expanded unsupervised algorithms (K-Means, PCA, SVD) for feature engineering — enabling faster retraining, lower memory footprint, and broader use cases in fraud detection and cyber-threat prevention. Source: www.prnewswire.com

• In December 2024, Google Cloud officially rolled out Google Agentspace — an enterprise platform integrating advanced Gemini-powered AI agents designed to unify unstructured and structured data workflows and accelerate enterprise AI adoption across search, automation, and analytic tasks. Source: www.cloud.google.com

The scope of the Unsupervised Learning Market Report encompasses a comprehensive analysis of key segments, technologies, regional landscapes, deployment contexts, and industry applications. It covers segmentation by model type — including clustering, dimensionality reduction, self-supervised deep learning, and density estimation — highlighting adoption patterns and use-case relevance across enterprise functions. Application areas in the report span anomaly detection, customer segmentation, feature extraction, natural language pattern discovery, and autonomous analytics operations, offering detailed insights into how unsupervised methods are embedded into business workflows. The report also evaluates end-user segments such as BFSI, healthcare, IT services, telecommunications, manufacturing, and retail, illustrating consumption behavior and operational drivers across sectors. Technological focus areas include AutoML platforms, hybrid learning frameworks, edge and federated learning approaches, and high-performance computing infrastructures that support large-scale model training and deployment. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa regions, with regional market dynamics, adoption trends, and digital ecosystem maturity indicators. In addition, the report assesses innovation patterns, competitive strategies, technology partnerships, and regulatory influences shaping the market environment. It identifies niche segments such as explainable unsupervised learning and sector-specific solutions, ensuring decision-makers gain a full understanding of opportunities, challenges, and technological pathways impacting the future of autonomous analytics at enterprise and industry scales.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,075.0 Million |

| Market Revenue (2033) | USD 12,360.8 Million |

| CAGR (2026–2033) | 35.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | Asia-Pacific, North America, Europe, South America, Middle East & Africa |

| Key Players Analyzed | IBM, Microsoft, Google, Amazon Web Services (AWS), SAP, Oracle, Salesforce, H2O.ai, DataRobot, NVIDIA, Intel, SAS Institute, Databricks, Qualcomm |

| Customization & Pricing | Available on Request (10% Customization Free) |