Reports

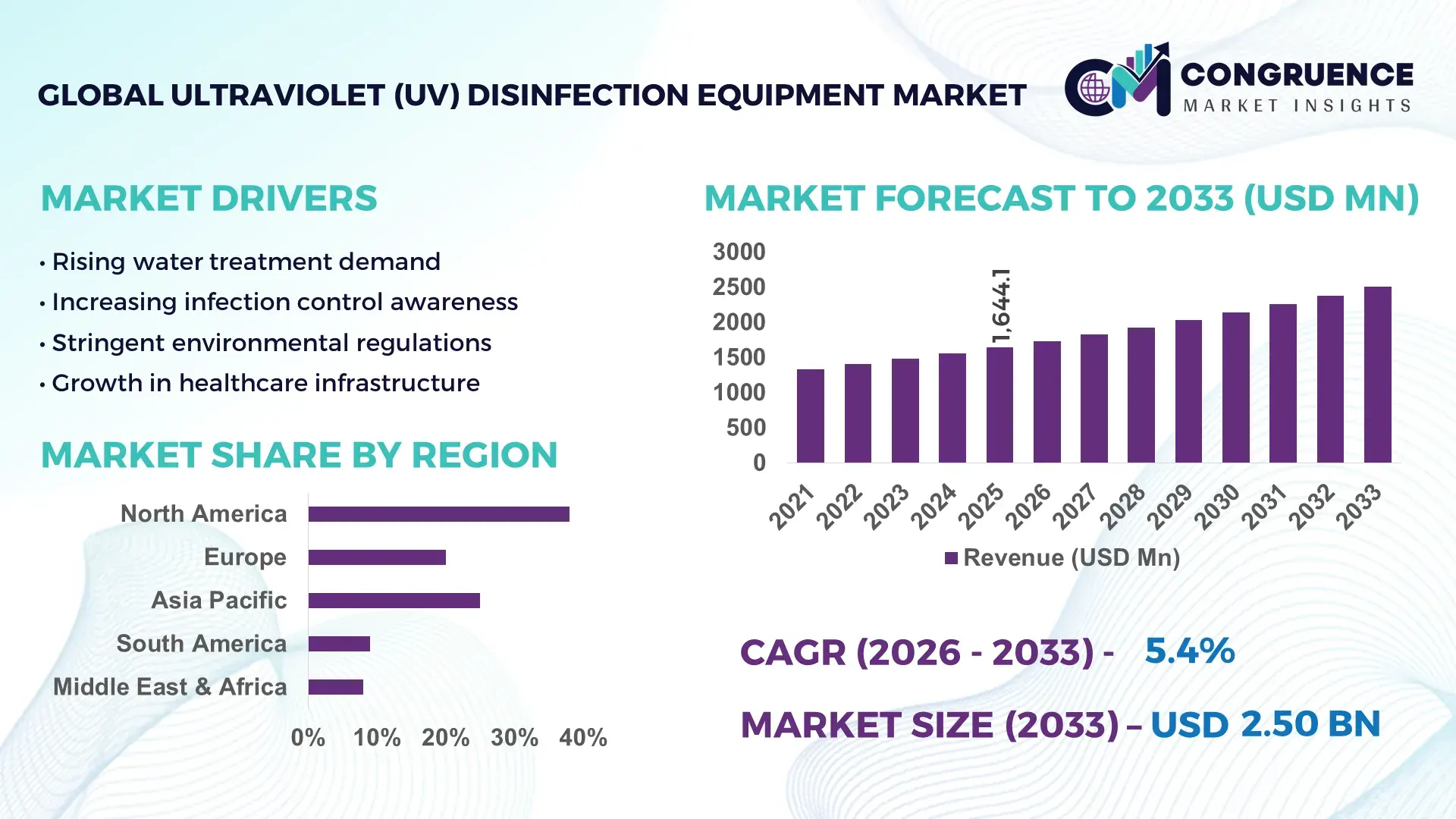

The Global Ultraviolet (UV) Disinfection Equipment Market was valued at USD 1644.06 Million in 2025 and is anticipated to reach a value of USD 2504.06 Million by 2033 expanding at a CAGR of 5.4% between 2026 and 2033. The growth is primarily driven by increasing demand for chemical-free, high-efficiency water and air purification solutions across municipal, healthcare, and industrial sectors.

The United States continues to demonstrate strong industrial leadership in the Ultraviolet (UV) Disinfection Equipment Market, supported by advanced manufacturing capabilities and high adoption across municipal water treatment facilities. Over 75% of large-scale wastewater treatment plants in the country have integrated UV disinfection systems as part of tertiary treatment processes. Annual infrastructure investments exceeding USD 50 billion in water and sanitation upgrades further strengthen deployment. In addition, the healthcare sector has seen more than 60% adoption of UV-based room disinfection systems in hospitals to reduce hospital-acquired infections. Technological advancements such as UV-C LEDs and smart monitoring systems are accelerating efficiency gains, with operational energy consumption reduced by nearly 30% compared to legacy mercury-based systems.

Market Size & Growth: Valued at USD 1644.06 Million in 2025, projected to reach USD 2504.06 Million by 2033, growing at 5.4% CAGR due to rising demand for sustainable and chemical-free disinfection solutions.

Top Growth Drivers: Water treatment adoption 68%, healthcare sterilization demand 55%, industrial hygiene compliance 47%.

Short-Term Forecast: By 2028, operational efficiency of UV systems is expected to improve by 25% through smart automation and sensor-based optimization.

Emerging Technologies: UV-C LED systems, IoT-enabled disinfection monitoring, and AI-driven predictive maintenance solutions.

Regional Leaders: North America projected at USD 780 Million by 2033 with strong municipal adoption; Europe at USD 620 Million driven by regulatory compliance; Asia-Pacific at USD 720 Million fueled by rapid urbanization.

Consumer/End-User Trends: Increasing adoption among hospitals, food processing units, and municipal utilities prioritizing non-chemical sterilization methods.

Pilot or Case Example: In 2024, a municipal water project achieved 40% energy savings and 35% maintenance reduction using advanced UV-C LED systems.

Competitive Landscape: Market leader holds approximately 18% share, with strong competition from established global manufacturers and emerging regional players.

Regulatory & ESG Impact: Stringent water quality regulations and sustainability mandates are driving adoption of low-carbon disinfection technologies.

Investment & Funding Patterns: Over USD 1.2 billion invested in water infrastructure modernization and clean technology innovation globally.

Innovation & Future Outlook: Integration of AI, digital twins, and compact modular systems is shaping next-generation UV disinfection solutions.

The Ultraviolet (UV) Disinfection Equipment Market is witnessing strong diversification across key industry sectors, including municipal water treatment, healthcare sterilization, food processing, and HVAC air purification. Municipal applications account for approximately 45% of total installations, followed by healthcare at 25%, reflecting rising infection control priorities. Technological advancements such as UV-C LED systems, which offer longer lifespan exceeding 10,000 hours and lower energy consumption, are reshaping product innovation. Regulatory frameworks focusing on chemical-free disinfection and environmental sustainability are accelerating adoption, particularly in Europe and North America. In Asia-Pacific, rapid urbanization and increasing access to clean water infrastructure are driving consumption growth. Emerging trends include portable UV devices, integration with smart building systems, and expansion into residential water purification, indicating a strong forward outlook for diversified applications.

The Ultraviolet (UV) Disinfection Equipment Market holds strategic importance in global public health infrastructure, industrial hygiene systems, and sustainable water management frameworks. With increasing regulatory emphasis on reducing chemical disinfectants, UV-based technologies are emerging as a core component of modern sanitation strategies. UV-C LED technology delivers nearly 30% energy efficiency improvement compared to traditional mercury vapor lamps, significantly enhancing operational performance and lifecycle cost savings. This transition is particularly relevant in large-scale municipal systems where energy optimization directly impacts operating budgets.

Regionally, North America dominates in volume due to extensive municipal installations, while Asia-Pacific leads in adoption with over 52% of new industrial facilities integrating UV disinfection systems as part of compliance frameworks. Rapid industrialization and population growth are driving large-scale deployment in water-stressed regions, further strengthening market relevance.

By 2028, AI-enabled predictive maintenance and real-time monitoring systems are expected to reduce system downtime by 35%, enhancing reliability and performance. Companies are also aligning with ESG commitments, targeting up to 40% reduction in chemical disinfectant usage by 2030 through UV integration. In 2024, a leading European water utility achieved a 28% reduction in operational costs through the deployment of smart UV systems combined with automated control mechanisms.

The future pathways of the Ultraviolet (UV) Disinfection Equipment Market are closely tied to digital transformation, decentralized water treatment solutions, and sustainable infrastructure development, positioning the market as a critical pillar of resilience, regulatory compliance, and environmentally responsible growth.

The growing emphasis on chemical-free and environmentally sustainable disinfection methods is a major driver of the Ultraviolet (UV) Disinfection Equipment Market. Traditional chemical disinfectants such as chlorine are associated with harmful byproducts, including trihalomethanes, which pose health risks. UV disinfection eliminates up to 99.99% of microorganisms without producing such byproducts, making it highly suitable for drinking water and healthcare applications. Over 70% of newly constructed municipal water treatment plants are incorporating UV systems as part of multi-barrier treatment strategies. In healthcare settings, UV disinfection has been shown to reduce hospital-acquired infections by up to 30%, reinforcing its critical role in infection control protocols. The food and beverage industry is also increasing adoption, particularly in surface and packaging sterilization, where hygiene standards are becoming more stringent. This growing demand across sectors continues to accelerate market expansion.

High upfront capital investment remains a key restraint in the Ultraviolet (UV) Disinfection Equipment Market, particularly for small and medium-sized enterprises and developing regions. Installation of large-scale UV systems for municipal water treatment can require significant infrastructure modifications, including reactor chambers, control systems, and integration with existing pipelines. Initial setup costs can be 20–30% higher than conventional chemical disinfection systems. Additionally, while UV systems reduce chemical usage, ongoing maintenance such as lamp replacement and periodic cleaning adds operational complexity. In regions with limited access to financing or government subsidies, adoption rates remain relatively slow. Furthermore, lack of technical expertise in installation and system optimization can lead to inefficiencies, discouraging potential adopters. These cost-related challenges create barriers to widespread deployment, especially in price-sensitive markets.

The rise of smart and decentralized water treatment solutions presents significant opportunities for the Ultraviolet (UV) Disinfection Equipment Market. Rapid urbanization and the need for localized water purification systems are driving demand for compact, modular UV units that can be deployed in residential complexes, remote communities, and industrial facilities. These systems are increasingly integrated with IoT-enabled sensors that provide real-time monitoring of water quality and system performance. Adoption of decentralized systems is growing at over 40% in emerging urban regions where centralized infrastructure is limited. Additionally, advancements in UV-C LED technology have enabled the development of portable and energy-efficient devices suitable for both residential and commercial applications. The integration of UV systems with smart city initiatives and digital water management platforms further expands market potential, creating new revenue streams and application areas.

Regulatory compliance and operational limitations present ongoing challenges in the Ultraviolet (UV) Disinfection Equipment Market. While UV systems are effective against a wide range of microorganisms, their performance depends heavily on water clarity and pre-treatment processes. High turbidity levels can reduce UV penetration, requiring additional filtration systems that increase complexity and cost. Regulatory standards for water and air disinfection vary across regions, creating compliance challenges for manufacturers and end-users operating in multiple markets. In some cases, validation and certification processes for UV systems can take several months, delaying project implementation. Moreover, the gradual phase-out of mercury-based UV lamps due to environmental concerns necessitates a transition to alternative technologies, which may involve higher costs and technical adjustments. These factors collectively create operational and regulatory hurdles that impact market scalability.

• Accelerated Adoption of UV-C LED Technology Enhancing Energy Efficiency: The transition from conventional mercury-based lamps to UV-C LED systems is gaining strong momentum, with adoption rates exceeding 35% across newly installed systems in 2025. UV-C LEDs offer up to 30% lower energy consumption and operational lifespans exceeding 10,000 hours, compared to 8,000 hours for traditional lamps. Industrial facilities report up to 25% reduction in maintenance frequency due to improved durability. In high-demand sectors such as healthcare and food processing, over 40% of new installations now prioritize LED-based UV systems, reflecting a measurable shift toward sustainable and energy-efficient disinfection solutions.

• Expansion of Smart and IoT-Enabled Disinfection Systems: Integration of IoT-based monitoring and automation technologies is transforming operational efficiency in the Ultraviolet (UV) Disinfection Equipment market. Approximately 48% of newly deployed UV systems now include real-time monitoring capabilities, enabling predictive maintenance and performance optimization. Facilities leveraging smart UV systems have achieved up to 35% reduction in downtime and 20% improvement in operational reliability. Data-driven analytics further enhance compliance tracking, particularly in regulated industries where automated reporting has improved audit readiness by 30%, reinforcing the value of digital transformation in disinfection infrastructure.

• Growing Demand in Air Disinfection and HVAC Integration: The use of UV disinfection in air purification systems is expanding rapidly, particularly in commercial buildings and healthcare environments. Over 50% of large hospitals have integrated UV-based HVAC disinfection systems to reduce airborne pathogens. Studies indicate that UV air disinfection can lower microbial load by up to 90% in enclosed environments. In commercial real estate, nearly 38% of newly constructed smart buildings are incorporating UV air purification units, driven by heightened awareness of indoor air quality and regulatory standards for occupant safety.

• Rise in Modular and Prefabricated Deployment Models: The adoption of modular and prefabricated UV disinfection systems is reshaping installation and deployment strategies. Approximately 55% of new infrastructure projects report cost savings through prefabricated system integration, with installation timelines reduced by up to 40%. Pre-engineered UV units enable rapid deployment in municipal and industrial settings, particularly in regions with infrastructure constraints. In Europe and North America, over 45% of large-scale water treatment upgrades now utilize modular UV systems, improving scalability and reducing on-site labor requirements by nearly 30%, thereby enhancing project efficiency and execution speed.

The Ultraviolet (UV) Disinfection Equipment Market demonstrates a structured segmentation across product types, applications, and end-user industries, each contributing distinctively to overall market expansion. Product types are primarily categorized into low-pressure UV systems, medium-pressure UV systems, and UV-C LED systems, each offering varying levels of intensity and energy efficiency. Application-wise, municipal water treatment remains dominant, followed by air disinfection and surface sterilization in healthcare and industrial environments. End-user segmentation highlights strong adoption across municipalities, healthcare institutions, and food processing industries, collectively accounting for over 70% of system installations. Regional variations further influence segmentation, with developed markets focusing on advanced LED technologies while emerging regions prioritize cost-effective conventional systems. Increasing regulatory emphasis and technological advancements are continuously reshaping segment dynamics, creating differentiated growth pathways across categories.

The Ultraviolet (UV) Disinfection Equipment market is segmented into low-pressure UV systems, medium-pressure UV systems, and UV-C LED systems, each serving distinct operational requirements. Low-pressure UV systems currently account for approximately 46% of total installations, driven by their high energy efficiency and suitability for municipal water treatment applications. Medium-pressure systems hold around 32% share, offering higher intensity output and faster disinfection cycles, making them ideal for industrial and wastewater treatment processes. In contrast, UV-C LED systems represent about 22% of adoption but are rapidly gaining traction due to technological advancements.

UV-C LED systems are the fastest-growing segment, expanding at an estimated rate exceeding 12% annually, fueled by their compact design, instant start capability, and mercury-free composition. Their adoption is particularly strong in portable and decentralized applications, where flexibility and low maintenance are critical. Meanwhile, low- and medium-pressure systems together contribute a combined 78% share, maintaining relevance in large-scale infrastructure projects.

Application segmentation in the Ultraviolet (UV) Disinfection Equipment Market includes water and wastewater treatment, air disinfection, surface disinfection, and industrial process water treatment. Water and wastewater treatment leads the segment with approximately 52% share, supported by stringent regulatory requirements and increasing investments in public water infrastructure. Air disinfection accounts for around 23% of applications, while surface disinfection and industrial processes collectively contribute about 25%.

Air disinfection is the fastest-growing application, expanding at an estimated rate of over 11% annually, driven by rising concerns over airborne pathogens and indoor air quality. Adoption in healthcare facilities and commercial buildings has increased significantly, with over 50% of hospitals integrating UV-based air purification systems. Surface disinfection is also gaining momentum in food processing and pharmaceutical manufacturing, where hygiene compliance is critical.

The Ultraviolet (UV) Disinfection Equipment Market is segmented by end-users into municipal, healthcare, industrial, commercial, and residential sectors. Municipal utilities dominate the market with approximately 48% share, driven by large-scale water treatment requirements and regulatory compliance mandates. Healthcare institutions account for around 22% of adoption, leveraging UV systems for infection control and sterilization. Industrial users, including food processing and pharmaceuticals, contribute approximately 18%, while commercial and residential segments collectively represent 12%.

Healthcare is the fastest-growing end-user segment, expanding at an estimated rate above 10% annually, supported by increasing focus on hospital-acquired infection prevention and stringent sanitation protocols. Over 60% of large hospitals now utilize UV-based room disinfection systems, indicating strong adoption trends. Industrial adoption is also rising, particularly in food safety applications where compliance standards are tightening.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

North America’s dominance is supported by over 70% penetration of UV disinfection systems in municipal wastewater treatment plants and more than 60% adoption in healthcare facilities. Europe follows with approximately 28% share, driven by strict environmental regulations and sustainability mandates, with over 65% of industrial water treatment plants utilizing UV systems. Asia-Pacific holds around 24% share but demonstrates strong expansion, with more than 50% of new urban infrastructure projects incorporating UV-based purification systems. South America and Middle East & Africa collectively contribute close to 10%, with increasing investments in water infrastructure exceeding USD 20 billion annually across developing economies. Regional disparities are influenced by regulatory frameworks, infrastructure maturity, and technological adoption rates.

North America holds approximately 38% share in the Ultraviolet (UV) Disinfection Equipment market, supported by strong demand across municipal water treatment, healthcare, and food processing industries. Over 75% of wastewater treatment facilities in the region have integrated UV systems, reflecting widespread infrastructure modernization. Regulatory frameworks such as stringent water quality standards and infection control mandates have accelerated adoption, with compliance rates exceeding 80% in large urban centers. Technological advancements include widespread deployment of UV-C LED systems and IoT-enabled monitoring platforms, improving system efficiency by up to 30%. A notable example includes a regional manufacturer implementing smart UV solutions across over 500 municipal installations, reducing operational downtime by 25%. Consumer behavior reflects higher enterprise-level adoption, particularly in healthcare and commercial sectors, where over 60% of facilities prioritize chemical-free disinfection solutions for safety and compliance.

Europe accounts for approximately 28% of the Ultraviolet (UV) Disinfection Equipment market, with key markets including Germany, the United Kingdom, and France leading adoption. Over 68% of industrial water treatment facilities in these countries have implemented UV disinfection systems to comply with environmental regulations. Sustainability initiatives targeting a 50% reduction in chemical disinfectant use by 2030 are driving demand for UV-based alternatives. Technological adoption is strong, with over 40% of new installations utilizing advanced UV-C LED technology. Regulatory bodies continue to enforce strict water and air quality standards, influencing procurement decisions across industries. A prominent regional player has expanded its modular UV system portfolio, achieving 20% improvement in energy efficiency across installations. Consumer behavior is shaped by regulatory pressure, with enterprises prioritizing transparent, sustainable, and compliant disinfection technologies in both public and private sectors.

Asia-Pacific ranks as the fastest-growing region in the Ultraviolet (UV) Disinfection Equipment market, contributing approximately 24% of global volume. Major consuming countries include China, India, and Japan, where rapid urbanization and industrial expansion are driving demand. More than 55% of new water infrastructure projects in urban areas incorporate UV disinfection systems, reflecting increased focus on public health and sanitation. Manufacturing trends indicate strong local production capacity, with regional output increasing by over 35% in recent years. Technological innovation hubs are emerging, particularly in China and Japan, focusing on compact and energy-efficient UV-C LED systems. A leading regional manufacturer has deployed over 2,000 decentralized UV units in rural water supply projects, improving access to clean water for more than 5 million users. Consumer behavior is influenced by population density and infrastructure needs, with adoption driven by government-backed sanitation initiatives and rapid industrialization.

South America holds approximately 6% share of the Ultraviolet (UV) Disinfection Equipment market, with Brazil and Argentina as key contributors. Infrastructure development in water and wastewater treatment is a primary growth driver, with over 40% of new projects integrating UV systems. Government initiatives aimed at improving water quality and sanitation coverage have increased adoption rates, particularly in urban areas. Energy and mining sectors are also contributing to demand, with industrial water treatment applications accounting for nearly 30% of installations. Trade policies supporting import of advanced disinfection technologies have further enabled market expansion. A regional player has introduced cost-efficient UV systems tailored for small municipalities, achieving a 20% reduction in installation costs. Consumer behavior reflects a growing emphasis on reliable and low-maintenance solutions, particularly in regions with limited access to centralized water treatment infrastructure.

The Middle East & Africa region accounts for approximately 4% of the Ultraviolet (UV) Disinfection Equipment market, with key growth countries including the UAE and South Africa. Water scarcity and desalination projects are major drivers, with over 35% of desalination plants integrating UV disinfection systems for post-treatment processes. Construction and oil & gas sectors are also contributing to demand, particularly for industrial water reuse applications. Technological modernization efforts include adoption of automated UV systems capable of reducing operational costs by up to 25%. Regional governments are promoting sustainable water management practices through policy frameworks and international trade partnerships. A local company has deployed UV systems across multiple desalination facilities, improving water treatment efficiency by 30%. Consumer behavior is shaped by resource constraints, with strong preference for energy-efficient and low-maintenance disinfection technologies.

United States – 32% share in the Ultraviolet (UV) Disinfection Equipment market, driven by advanced municipal infrastructure and high healthcare sector adoption.

China – 21% share in the Ultraviolet (UV) Disinfection Equipment market, supported by large-scale industrial expansion and government-backed water treatment initiatives.

The Ultraviolet (UV) Disinfection Equipment market is moderately fragmented, with over 50 active global and regional players competing across various product segments and application areas. The top five companies collectively account for approximately 42% of the total market share, indicating a competitive yet innovation-driven landscape. Market leaders are focusing on strategic initiatives such as product innovation, mergers, and partnerships to strengthen their positions. Over 30 new product launches were recorded in 2024 alone, primarily centered on UV-C LED technology and smart monitoring systems. Companies are increasingly investing in R&D, with expenditure levels rising by nearly 18% to enhance energy efficiency and system lifespan. Strategic collaborations between technology providers and municipal authorities have increased by 25%, facilitating large-scale deployment projects. Additionally, regional players are gaining traction by offering cost-effective and customized solutions tailored to local infrastructure needs. Digital transformation, including AI-based predictive maintenance and IoT integration, is emerging as a key differentiator, with over 45% of leading companies incorporating smart features into their product portfolios. The competitive environment continues to evolve with a strong focus on sustainability, operational efficiency, and regulatory compliance.

Xylem Inc.

Trojan Technologies

Halma plc

Evoqua Water Technologies

Atlantic Ultraviolet Corporation

Heraeus Holding GmbH

Severn Trent Services

Kuraray Co., Ltd.

Calgon Carbon Corporation

Atlantium Technologies Ltd.

Technological innovation in the Ultraviolet (UV) Disinfection Equipment Market is centered on improving energy efficiency, system lifespan, and real-time performance monitoring. One of the most transformative advancements is the adoption of UV-C LED technology, which now accounts for over 35% of newly deployed systems. These LEDs offer operational lifespans exceeding 10,000 hours and reduce energy consumption by approximately 25–30% compared to traditional mercury vapor lamps. Their compact size and instant on-off capability enable flexible integration into decentralized and portable disinfection units, expanding application potential across residential and industrial sectors.

Another key innovation is the integration of IoT-enabled sensors and AI-based predictive maintenance systems. Approximately 48% of advanced UV installations now incorporate smart monitoring features that track parameters such as UV intensity, flow rate, and system efficiency in real time. This has resulted in up to 35% reduction in unplanned downtime and nearly 20% improvement in maintenance efficiency. Digital twin technology is also emerging, allowing operators to simulate system performance and optimize operational parameters before deployment, improving system design accuracy by nearly 15%.

Advancements in reactor design are further enhancing system effectiveness. High-output medium-pressure UV reactors now deliver up to 3 times higher intensity compared to low-pressure systems, enabling faster disinfection cycles in industrial applications. Additionally, automated cleaning systems using mechanical or chemical wipers have reduced fouling-related efficiency losses by over 40%. Innovations in quartz sleeve coatings are improving UV transmittance by approximately 10–12%, further boosting performance.

Emerging hybrid technologies combining UV with advanced oxidation processes (AOP) are gaining traction, particularly in pharmaceutical and wastewater treatment applications. These systems can degrade complex organic contaminants by up to 90%, addressing limitations of standalone UV systems. Collectively, these technological advancements are reshaping the Ultraviolet (UV) Disinfection Equipment Market by enhancing operational reliability, reducing lifecycle costs, and expanding application versatility across industries.

• In March 2025, Xylem Inc. expanded its UV disinfection portfolio by launching advanced Wedeco systems with integrated smart sensors and digital monitoring capabilities, enabling real-time performance optimization and reducing maintenance interventions by approximately 20%. Source: www.xylem.com

• In September 2024, Trojan Technologies introduced an upgraded UV3000Plus system designed for municipal wastewater treatment, incorporating enhanced lamp efficiency and modular design, improving energy utilization by nearly 15% and enabling scalable deployment across large treatment facilities. Source: www.trojantechnologies.com

• In January 2025, Heraeus Holding GmbH advanced its UV-C LED technology platform by introducing high-output modules for industrial applications, achieving up to 25% higher irradiation intensity while reducing system footprint, supporting compact and energy-efficient disinfection solutions. Source: www.heraeus.com

• In July 2024, Atlantium Technologies Ltd. deployed its Hydro-Optic UV (HOD) system in a large-scale beverage production facility, achieving consistent microbial reduction above 99.99% and reducing operational energy consumption by approximately 20% through optimized hydraulic and optical design. Source: www.atlantium.com

The Ultraviolet (UV) Disinfection Equipment Market Report provides a comprehensive analysis of industry dynamics, covering a wide range of product types, applications, end-user segments, and regional markets. The report evaluates key product categories including low-pressure UV systems, medium-pressure systems, and advanced UV-C LED technologies, which collectively account for over 95% of installed systems globally. It also assesses emerging hybrid technologies such as UV combined with advanced oxidation processes, which are increasingly utilized in high-contamination environments. From an application perspective, the report encompasses municipal water and wastewater treatment, air disinfection systems, surface sterilization, and industrial process water treatment. Municipal applications represent the largest segment, accounting for more than 50% of installations, followed by healthcare and industrial sectors with a combined contribution exceeding 40%. The report also highlights niche and emerging applications such as residential water purification and portable UV devices, which are gaining traction due to rising awareness of hygiene and decentralized water systems.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, collectively representing 100% of the global market landscape. It provides detailed insights into regional infrastructure development, regulatory frameworks, and adoption trends. Additionally, the report examines technological advancements, including IoT integration, AI-based monitoring, and energy-efficient UV-C LED systems, which are influencing purchasing decisions and operational strategies. The scope further includes analysis of competitive dynamics, regulatory compliance requirements, and investment trends, offering decision-makers a structured understanding of market opportunities, operational challenges, and innovation pathways shaping the Ultraviolet (UV) Disinfection Equipment Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Xylem Inc., Trojan Technologies, Halma plc, Evoqua Water Technologies, Atlantic Ultraviolet Corporation, Heraeus Holding GmbH, Severn Trent Services, Kuraray Co., Ltd., Calgon Carbon Corporation, Atlantium Technologies Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |