Reports

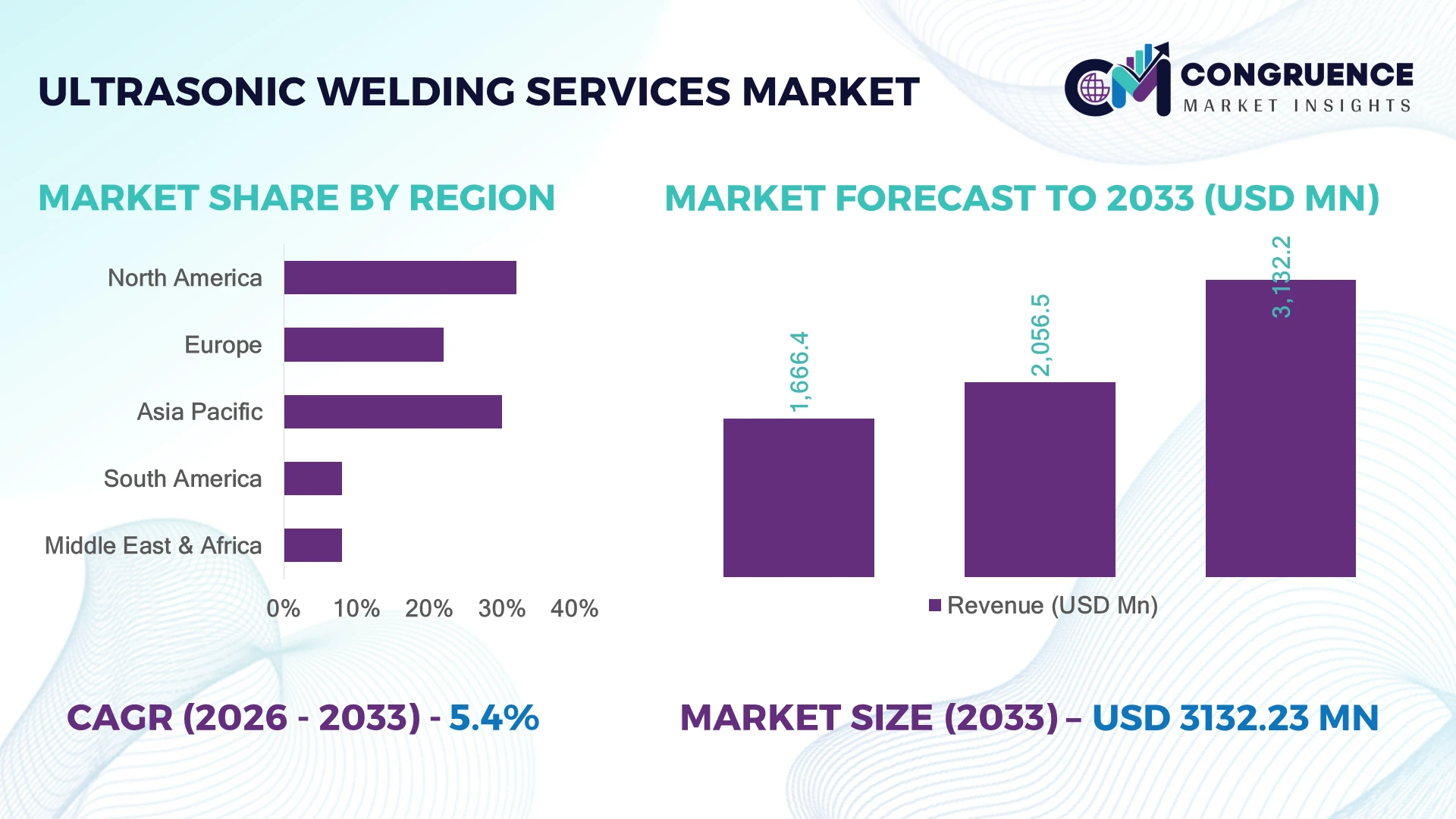

The Global Ultrasonic Welding Services Market was valued at USD 2,056.0 Million in 2025 and is anticipated to reach a value of USD 3,132.2 Million by 2033 expanding at a CAGR of 5.4% between 2026 and 2033. Growth is driven by rising adoption of precision ultrasonic joining in electric vehicle batteries, medical devices, electronics miniaturization, and lightweight automotive component manufacturing.

The United States dominates the market landscape with approximately 32% share, supported by advanced manufacturing investments, EV battery production expansion, and high adoption across automotive and healthcare sectors. China follows with nearly 28% share, backed by large-scale electronics manufacturing and government-led industrial automation initiatives under Made in China 2025. Germany contributes over 12% through automotive engineering expertise and Industry 4.0 integration. The U.S. operates more than 100 major EV battery and component facilities, while China maintains a significantly larger electronics production base.

Strategic implication: Companies prioritizing automated ultrasonic welding capabilities and regional service networks will strengthen their position in high-value manufacturing ecosystems.

Market Size & Growth: USD 2,056.0 Million (2025) to USD 3,132.2 Million (2033) at 5.4% CAGR, driven by EV battery and electronics manufacturing expansion.

Top Growth Drivers: Electric vehicle manufacturing (+35%), medical device production (+18%), and automated assembly adoption (+22%) accelerate ultrasonic welding service demand.

Short-Term Forecast: By 2028, automation integration reduces welding cycle costs by 15% and improves production efficiency by 20%.

Emerging Technologies: AI-based quality monitoring, robotic ultrasonic welding cells, and advanced thermoplastic joining technologies reshape manufacturing processes.

Regional Leaders: North America reaches USD 1.0 Billion by 2033 with EV adoption; Asia Pacific reaches USD 1.4 Billion with electronics expansion; Europe reaches USD 500 Million with Industry 4.0 adoption.

Consumer/End-User Trends: Over 60% of manufacturers prioritize precision joining solutions for lightweight and miniaturized components.

Pilot/Case Example: In 2024, automotive ultrasonic welding deployments achieved nearly 25% cycle-time reduction in battery component assembly operations.

Competitive Landscape: Leading providers include Emerson Electric, Herrmann Engineering, Dukane, Telsonic, and Sonics & Materials, with top players accounting for approximately 40% market presence.

Regulatory & ESG Impact: Lightweight vehicle component initiatives reduce material usage by nearly 20%, supporting global emission reduction targets.

Investment & Funding: More than USD 500 Million invested in smart manufacturing expansion, partnerships, and automated welding technology upgrades.

Innovation & Future Outlook: Next-generation ultrasonic systems focus on real-time analytics, digital twins, and localized manufacturing strategies across global supply chains.

The Ultrasonic Welding Services Market is gaining momentum as manufacturers seek faster, cleaner, and more reliable joining solutions across automotive, healthcare, and electronics applications. Demand is concentrated in battery assembly, wearable electronics, and medical consumables, where precision requirements are increasing. More than 55% of advanced manufacturing facilities are integrating automated joining technologies, while supply-chain localization initiatives in North America and Europe are accelerating investments in regional welding capabilities. The market is transitioning toward intelligent service models that combine automation, predictive monitoring, and application-specific engineering support.

The Ultrasonic Welding Services Market is becoming strategically important as industries shift toward lightweight materials, compact electronic designs, and localized manufacturing networks. Automotive and electronics companies are restructuring supply chains after global disruptions, increasing demand for specialized welding partners that provide reliable, scalable joining solutions.

Advanced ultrasonic welding systems deliver measurable advantages over traditional thermal joining methods by reducing energy consumption by nearly 30% and shortening assembly cycles by approximately 20%. North America leads in EV and medical device adoption, while Asia Pacific maintains greater production scale through electronics manufacturing hubs in China, Japan, and South Korea. Europe emphasizes high-precision applications through automation and sustainability-focused industrial modernization.

Over the next 2–3 years, manufacturers are expected to increase investments in robotic welding cells, AI-enabled inspection, and digital production monitoring. For example, battery manufacturers are deploying ultrasonic welding for copper and aluminum connections to improve conductivity and reduce material waste. Companies are expanding through technology partnerships, regional service centers, and automation upgrades to secure long-term contracts. Strategic positioning will depend on combining engineering expertise, faster deployment capabilities, and intelligent manufacturing integration to capture emerging opportunities.

The rapid transition toward lightweight assemblies and miniaturized electronic components is strengthening demand for ultrasonic welding services across automotive, medical, and electronics manufacturing. More than 65% of electric vehicle battery modules now incorporate ultrasonic welded connections for improved conductivity, while automated welding cells improve production throughput by nearly 20% and reduce joint defects by approximately 25%. The expansion of battery manufacturing under the U.S. Inflation Reduction Act and rising semiconductor investments are increasing outsourcing requirements for specialized welding service providers. In response, leading companies are expanding application engineering centers, investing in robotic welding platforms, and forming OEM partnerships to deliver customized joining solutions. A key strategic advantage lies in combining process validation with rapid production scaling, enabling manufacturers to shorten product launch timelines while maintaining consistent weld integrity.

High capital requirements for advanced ultrasonic welding equipment and inconsistent compatibility across engineered polymers and dissimilar metals continue to limit wider service deployment. Nearly 30% of manufacturers require customized tooling for new component designs, while specialized sonotrodes account for almost 18% of production setup costs. Supply-chain disruptions affecting precision titanium and hardened alloy tooling have extended equipment lead times in Germany and Japan, delaying capacity expansion. These structural limitations reduce operational flexibility, particularly for low-volume production and customized manufacturing programs. Service providers are mitigating risks through localized tooling production, multi-supplier procurement strategies, long-term equipment contracts, and hybrid joining capabilities that combine ultrasonic welding with complementary assembly technologies. Standardized tooling platforms are also emerging as an effective approach to improving asset utilization.

The convergence of artificial intelligence, industrial automation, and digital manufacturing platforms is creating high-value opportunities for ultrasonic welding service providers. More than 55% of advanced production facilities are integrating predictive quality monitoring, while AI-enabled inspection systems reduce defect detection time by approximately 40%. China's smart manufacturing initiatives and India's expanding electronics production ecosystem are accelerating investment in digitally connected welding operations. Companies are establishing application laboratories, expanding robotics partnerships, and developing cloud-enabled process analytics that support remote performance optimization. A significant emerging opportunity lies in providing data-driven welding validation services alongside production, enabling customers to improve traceability, regulatory compliance, and production efficiency through integrated digital quality management rather than standalone welding operations.

Maintaining consistent weld quality across multiple facilities, materials, and product configurations remains one of the industry's most significant execution challenges. Nearly 35% of manufacturers report shortages of skilled ultrasonic welding technicians, while multi-material assembly programs increase process validation requirements by approximately 30%. Growing demand for battery packs, medical devices, and precision electronics is placing additional pressure on quality assurance systems, operator certification, and equipment calibration. Companies must simultaneously manage digital integration, production standardization, and evolving customer specifications without disrupting manufacturing schedules. To overcome these barriers, industry leaders are investing in automated parameter optimization, workforce training academies, digital process twins, and centralized quality management platforms. Organizations that standardize process intelligence across global manufacturing networks will achieve stronger operational resilience and long-term competitive differentiation.

AI Quality Monitoring Expansion Manufacturers are integrating AI-powered inspection and real-time weld analytics into ultrasonic welding workflows, with adoption rising across approximately 45% of advanced production facilities. Automated defect detection improves quality verification speed by nearly 35% and reduces manual inspection dependency. Companies in Japan and Germany are partnering with automation providers to deploy intelligent monitoring platforms, creating a shift from reactive quality control toward predictive manufacturing management.

Battery Assembly Optimization The growth of EV battery production is accelerating ultrasonic welding specialization, with battery manufacturers reporting nearly 60% higher use of precision joining processes for copper and aluminum connections. New battery gigafactory projects in the United States and Europe are increasing demand for localized welding expertise. Companies are restructuring supplier networks and expanding technical service teams to support faster validation, traceability, and production ramp-up requirements.

Flexible Manufacturing Models Contract-based ultrasonic welding services are gaining traction as manufacturers seek lower equipment ownership costs, with outsourcing adoption increasing by approximately 25% among small and medium producers. Companies are shifting toward application-specific service partnerships that provide tooling, testing, and process optimization. This model is particularly relevant for medical device manufacturers requiring rapid product changes and regulatory documentation.

Advanced Material Joining The adoption of engineered plastics, lightweight alloys, and composite materials is changing welding requirements, with material-focused applications growing by nearly 30% in automotive and electronics sectors. Supply-chain localization efforts are encouraging companies to develop regional material testing capabilities. Service providers are investing in customized tooling, simulation software, and process databases to handle increasingly complex joining specifications.

Based on type, automated ultrasonic welding services represent the leading segment due to their scalability, repeatability, and integration with smart manufacturing environments. Automated solutions account for approximately 55% of industrial deployments, supported by demand from automotive battery, electronics, and medical device manufacturers requiring consistent high-volume production. Their ability to reduce manual intervention by nearly 30% and improve process monitoring makes them a preferred investment area for large enterprises. The fastest-growing segment is robotic ultrasonic welding solutions, driven by flexible manufacturing requirements and Industry 4.0 adoption. Robotic platforms are expanding as manufacturers seek adaptable production lines capable of handling multiple product configurations. Traditional manual ultrasonic welding services remain relevant for low-volume customized applications, while semi-automated systems continue serving mid-scale manufacturers. Companies are increasing investments in modular automation platforms and engineering partnerships to improve deployment speed and production flexibility.

Based on application, electric vehicle battery component welding is emerging as the leading application area due to rising demand for reliable electrical connections in battery modules and packs. Battery-related ultrasonic welding services represent nearly 40% of new industrial deployments, supported by increasing EV production capacity in the United States, China, and Germany. The technology reduces thermal impact and improves connection reliability compared with conventional joining approaches. The fastest-growing application is medical device manufacturing, where demand is increasing due to stricter quality requirements and miniature component designs. Medical applications are expanding by approximately 25% as manufacturers adopt clean, precise, and repeatable joining methods for disposable devices and diagnostic equipment. Electronics assembly, automotive components, and consumer products continue maintaining stable demand, but companies are prioritizing automated validation systems and specialized welding processes to meet tighter production standards.

Based on end-user, automotive manufacturers represent the dominant user group due to extensive deployment in EV batteries, sensors, lightweight components, and electronic assemblies. Automotive companies contribute nearly 45% of ultrasonic welding service demand as manufacturers prioritize faster production cycles and improved component reliability. Large vehicle producers are increasingly partnering with specialized welding service providers to accelerate battery manufacturing expansion. The fastest-growing end-user segment is medical device companies, supported by rising demand for compact, sterile, and high-precision products. Adoption among medical manufacturers is increasing by approximately 28%, driven by automation requirements and stricter quality standards. Electronics producers, aerospace companies, and industrial equipment manufacturers continue expanding usage through customized applications. Companies are responding with sector-specific solutions, regional service centers, and integrated engineering support models to capture specialized manufacturing opportunities.

North America accounted for the largest market share at 32% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of6.2% between 2026 and 2033.

North America holds the leading position in the ultrasonic welding services market, supported by strong EV battery production, medical device manufacturing, and advanced electronics ecosystems. The region contributes approximately 32% of global demand, with the United States representing the majority of deployments through automotive and industrial automation applications. More than 100 battery and component manufacturing facilities are supporting demand for precision joining solutions. Companies are expanding regional engineering centers, investing in automated welding capabilities, and partnering with OEMs to improve localized production resilience and reduce supply-chain dependencies.

United States Market Outlook: The United States is the primary growth engine within North America due to expanding EV manufacturing, semiconductor investments, and healthcare technology production. Over 60% of new battery manufacturing projects incorporate advanced joining technologies, including ultrasonic welding solutions. Strong federal support for domestic manufacturing and clean energy supply chains is encouraging companies to establish localized service networks and advanced production capabilities.

Europe maintains a strong position in ultrasonic welding services due to automotive innovation, medical technology production, and Industry 4.0 adoption. The region contributes nearly 22% of market demand, driven by Germany, France, and Italy’s advanced manufacturing infrastructure. Increasing focus on lightweight vehicle production and sustainable manufacturing practices is accelerating adoption of energy-efficient joining technologies. More than 50% of automotive suppliers in major European manufacturing hubs are integrating automation and digital quality monitoring systems. Companies are strengthening partnerships with equipment providers and expanding application-specific service capabilities to support complex material joining requirements.

Germany Market Outlook: Germany leads Europe’s ultrasonic welding services adoption through its automotive engineering base and industrial automation expertise. The country’s automotive sector accounts for a significant portion of regional demand, with manufacturers increasingly deploying robotic welding systems across EV component production lines. Over 40% of German industrial manufacturers are advancing smart factory initiatives, creating opportunities for specialized welding service providers.

Asia-Pacific represents the fastest-growing market for ultrasonic welding services, supported by large-scale electronics manufacturing, EV battery expansion, and industrial automation investments. The region contributes approximately 30% of global demand and benefits from China, Japan, South Korea, and India’s manufacturing ecosystems. China’s electronics and battery industries account for a major share of regional deployments, while India is emerging as a growing manufacturing hub. More than 55% of new electronics assembly facilities in leading Asian manufacturing centers are adopting automated precision joining technologies. Companies are expanding production partnerships, establishing local service capabilities, and investing in automation-driven welding solutions.

China Market Outlook: China dominates Asia-Pacific demand through its extensive EV battery, electronics, and consumer technology manufacturing infrastructure. The country produces a substantial share of global battery components and continues expanding smart manufacturing adoption. More than 70% of large-scale electronics manufacturers use automated assembly processes, increasing demand for ultrasonic welding expertise, advanced tooling, and localized technical support.

South America is gradually expanding its ultrasonic welding services market through automotive manufacturing, electronics assembly, and industrial modernization initiatives. The region accounts for approximately 8% of global demand, with Brazil and Argentina representing the primary industrial centers. Automotive component localization programs and investments in manufacturing efficiency are increasing interest in precision joining technologies. However, limited automation infrastructure and dependence on imported equipment remain operational constraints. Companies are addressing these challenges through regional partnerships, service collaborations, and targeted investments in application-specific welding capabilities.

Brazil Market Outlook: Brazil represents the largest opportunity within South America due to its automotive production base and expanding industrial modernization efforts. The country accounts for more than 50% of regional automotive manufacturing activity, supporting demand for welding services in vehicle components and electronics. Companies are focusing on localized support networks and technology partnerships to improve adoption across manufacturing facilities.

The Middle East & Africa market is developing through industrial diversification, healthcare expansion, and manufacturing modernization programs. The region contributes approximately 8% of global demand, with adoption concentrated in the United Arab Emirates, Saudi Arabia, and South Africa. Government-led industrial transformation initiatives are encouraging investments in automated production technologies and localized manufacturing capabilities. More than 20% growth in advanced manufacturing projects across key industrial hubs is increasing demand for specialized joining solutions. Companies are establishing partnerships with global technology providers and developing regional service capabilities to support emerging manufacturing clusters.

United Arab Emirates Market Outlook: The United Arab Emirates is emerging as a strategic market due to investments in advanced manufacturing, healthcare infrastructure, and industrial automation. The country’s technology-focused industrial zones are attracting manufacturers seeking efficient production solutions. More than 30% of new industrial facilities in major economic zones are incorporating automation technologies, creating opportunities for ultrasonic welding service providers focused on precision assembly and smart manufacturing applications.

The ultrasonic welding services market features global technology leaders such as Emerson Branson, Herrmann Engineering, Dukane, Telsonic, and Sonics & Materials competing against regional engineering specialists and contract manufacturing providers. The top five players collectively account for approximately 40% of market activity, with competition centered on automation capability, application expertise, customization, and delivery speed. Technology leaders compete through AI-enabled controls, robotic integration, and global service networks, while regional suppliers compete through lower-cost engineering support and faster customization. Companies are expanding through partnerships with automotive and medical OEMs, localized service centers, and vertical integration of tooling and validation capabilities. The market is shifting toward intelligent welding platforms as customers prioritize traceability and process optimization. High tooling expertise requirements and qualification barriers remain major entry challenges. Winning players will combine advanced automation, industry-specific engineering knowledge, and responsive global support ecosystems.

Herrmann Engineering GmbH

Dukane Corporation

Telsonic AG

Sonics & Materials, Inc.

Sonobond Ultrasonics

Crest Ultrasonics Corporation

Rinco Ultrasonics AG

Schunk Sonosystems GmbH

Forward Sonic Tech Co., Ltd.

MECASONIC

Sonimat Ultrasonics

Weber Ultrasonics AG

Ultrasonic welding services are moving toward intelligent automation with AI-based monitoring, servo-controlled systems, and digital process analytics. Modern systems improve weld consistency by nearly 25% compared with conventional manual controls and reduce inspection dependency by approximately 35%. Adoption is strongest in automotive battery and medical device manufacturing, where more than 50% of advanced facilities are integrating automated joining technologies.

Servo-driven ultrasonic platforms are replacing older pneumatic systems by improving force control, repeatability, and energy efficiency. Compared with legacy equipment, advanced servo systems deliver nearly 20% improvement in process accuracy and reduce setup adjustments by around 15%. Global technology providers are benefiting through partnerships with OEMs requiring scalable and traceable manufacturing solutions.

Between 2026 and 2028, disruptive technologies including machine learning weld validation, digital twins, and inline non-destructive monitoring will reshape service models. Companies deploying connected welding ecosystems will gain competitive advantages through faster qualification cycles, predictive maintenance, and reduced production downtime. Emerson’s Branson Polaris platform demonstrates the industry shift toward configurable ultrasonic welding systems designed for evolving manufacturing requirements.

March 2026 — Emerson Electric Co. launched the Branson Polaris Ultrasonic Welding Platform, introducing a configurable welding solution for evolving manufacturing needs. The platform improves flexibility through integrated hardware and software capabilities. Source: www.emerson.com

October 2025 — Dukane Corporation expanded digital ultrasonic welding resources with advanced process-control documentation and connected welding solutions supporting industrial automation applications. The company continues strengthening engineering support for precision assembly markets. Source: www.dukane.com

June 2026 — Research teams introduced inline ultrasonic monitoring technology for thermoplastic composite welding, detecting induced defects across 21 welds using advanced ultrasonic sensing methods. The development supports aerospace-quality manufacturing and intelligent quality assurance. Source: www.arxiv.org

April 2024 — Industrial researchers advanced machine-learning-based condition monitoring for ultrasonic metal welding, achieving 5.35%–8.08% accuracy improvement in new process domains. The innovation strengthens predictive maintenance capabilities for manufacturing operations.

The Ultrasonic Welding Services Market Report covers comprehensive analysis across service types, applications, end-user industries, and major geographic markets. The study evaluates automated and specialized welding solutions used in automotive components, EV batteries, medical devices, electronics, industrial equipment, and consumer products. It examines North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level insights on manufacturing capacity, technology adoption, and investment activity.

The report provides strategic evaluation of emerging technologies including AI-enabled monitoring, robotic welding systems, advanced tooling, and digital quality management. It highlights competitive positioning, deployment patterns, partnership strategies, and expansion opportunities among key market participants. The analysis supports investment planning, operational optimization, supplier selection, and long-term competitive strategy development from 2026 to 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,056.0 Million |

| Market Revenue (2033) | USD 3,132.2 Million |

| CAGR (2026–2033) | 5.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type:

By Application:

By End-User:

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Emerson Electric Co. (Branson Ultrasonics); Herrmann Engineering GmbH; Dukane Corporation; Telsonic AG; Sonics & Materials, Inc.; Sonobond Ultrasonics; Crest Ultrasonics Corporation; Rinco Ultrasonics AG; Schunk Sonosystems GmbH; Forward Sonic Tech Co., Ltd.; MECASONIC; Sonimat Ultrasonics; Weber Ultrasonics AG |

| Customization & Pricing | Available on Request (10% Customization Free) |