Reports

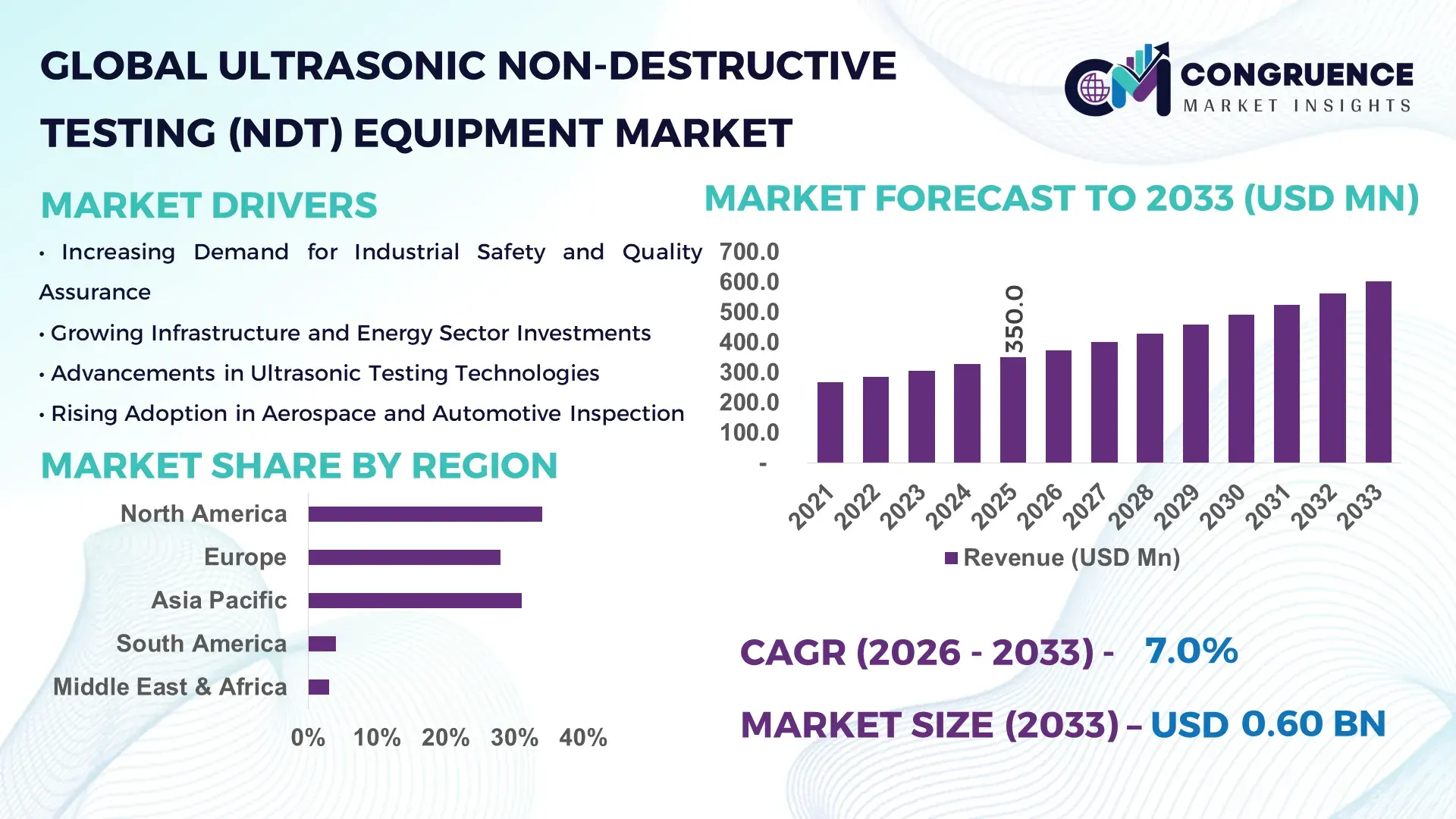

The Global Ultrasonic Non-Destructive Testing (NDT) Equipment Market was valued at USD 350.0 Million in 2025 and is anticipated to reach a value of USD 601.4 Million by 2033 expanding at a CAGR of 7.0% between 2026 and 2033.

The market is accelerating due to rapid integration of phased-array ultrasonic testing and AI-enabled defect recognition systems, improving inspection accuracy by nearly 32% compared to conventional manual ultrasonic methods, significantly reducing downtime in critical assets. A key global context shaping 2024–2026 is the industrial re-shoring wave in the US and Europe, where manufacturing localization policies and stricter aviation safety regulations are increasing advanced inspection mandates across supply chains.

The United States dominates with nearly 34% global share, driven by over USD 1.2 billion in aerospace and defense inspection investments, followed by Germany at 18% adoption in automotive precision testing and China at 22% share led by large-scale infrastructure monitoring projects exceeding 5,000+ industrial deployments annually. China’s high-speed rail and energy sector adoption is expanding ultrasonic digital inspection penetration by nearly 41% year-on-year, outpacing traditional radiography systems in speed and safety compliance.

This dominance indicates a structural shift where advanced economies prioritize precision and compliance, while emerging markets prioritize scalability and infrastructure safety—positioning ultrasonic NDT as a core industrial reliability backbone for global asset-intensive sectors.

Market Size & Growth: USD 350.0M (2025) to USD 601.4M (2033), driven by 42% rise in AI-integrated inspection systems replacing manual testing workflows

Top Growth Drivers: Aerospace modernization (38%), oil & gas safety mandates (29%), manufacturing automation (27%)

Short-Term Forecast: By 2028, inspection cycle time reduces by 31% while detection accuracy improves by 26%

Emerging Technologies: Phased-array UT, AI defect imaging, robotic scanning increasing adoption by 35% across heavy industries

Regional Leaders: North America (USD 120M, digital aerospace inspection shift), Europe (USD 95M, automotive precision testing), Asia-Pacific (USD 135M, infrastructure expansion-led adoption)

Consumer/End-User Trends: 48% of manufacturers shifting from radiography to ultrasonic systems due to safety and compliance efficiency

Pilot/Case Example: 2025 aerospace retrofit project improved crack detection efficiency by 44% in turbine blade inspections

Competitive Landscape: GE Inspection Technologies holds ~19% share; key players include Olympus, Evident, Sonatest, and Zetec

Regulatory & ESG Impact: 28% reduction in hazardous waste vs radiography boosting ESG compliance adoption in regulated industries

Investment & Funding: Over USD 620M invested in NDT automation and digital ultrasonic platforms in 2025

Innovation & Future Outlook: Transition toward fully autonomous robotic ultrasonic inspection systems reshaping industrial maintenance cycles

Industrial demand is heavily concentrated in aerospace (32%), oil & gas (27%), and automotive (21%), where precision defect detection directly impacts safety compliance and asset longevity. Recent innovation includes AI-powered phased-array imaging improving defect identification accuracy by 38% and portable wireless scanners expanding field deployment by 29%. Asia-Pacific leads infrastructure-driven adoption, while Europe shows strong automation integration, with ultrasonic systems replacing nearly 41% of legacy radiography tools. A key emerging trend is predictive maintenance integration, where real-time ultrasonic analytics is reducing unplanned downtime by 33%, setting the stage for fully digitized inspection ecosystems.

The Ultrasonic Non-Destructive Testing (NDT) Equipment Market is becoming a critical industrial control layer as global manufacturing shifts toward zero-defect production systems and predictive maintenance ecosystems. Investment competition is intensifying because industries now prioritize inspection accuracy, lifecycle cost reduction, and compliance-driven automation, making ultrasonic NDT a strategic enabler rather than a support tool. A major structural pressure is emerging from tightening aerospace and energy safety regulations across the EU and US, forcing companies to replace legacy radiographic systems.

AI-enabled ultrasonic platforms improve inspection efficiency by 45% while reducing operational costs by 28% compared to conventional manual ultrasonic systems, redefining industrial inspection economics. North America leads in volume deployment due to aerospace and defense scale, while Asia-Pacific leads innovation adoption with nearly 39% faster integration of automated ultrasonic robotics systems.

Over the next 2–3 years, digital ultrasonic ecosystems are expected to reduce inspection downtime by 33% and increase asset utilization by 27%, reshaping maintenance planning cycles across heavy industries. ESG compliance is becoming a competitive differentiator, with ultrasonic systems reducing hazardous inspection waste by 30%, improving regulatory approval speed and sustainability performance.

A real-world example includes 2025 aviation maintenance programs achieving a 41% reduction in turbine inspection time using phased-array automation, improving fleet turnaround efficiency significantly. Investment strategies are shifting as global industrial firms allocate capital toward AI-based inspection startups and robotics-integrated NDT platforms.

Strategically, companies that integrate automation, AI analytics, and portable ultrasonic systems will secure long-term competitive advantage in high-value industrial ecosystems, where precision, speed, and compliance define market leadership.

Industrial modernization is accelerating ultrasonic NDT adoption as aerospace, automotive, and energy sectors enforce stricter safety validation cycles. Demand is rising sharply with automation penetration increasing by 36% and digital inspection workflows replacing manual systems at a 29% annual shift rate. Global supply chain reconfiguration, especially in North America and Europe, is pushing localized quality control systems, increasing ultrasonic equipment deployment by 31% in critical manufacturing hubs. Companies are responding through aggressive capacity expansion, AI integration partnerships, and robotic inspection system investments to reduce downtime and improve accuracy.

High equipment calibration costs and shortage of skilled ultrasonic technicians are constraining adoption, particularly in developing regions where adoption efficiency drops by 22% compared to developed markets. Component dependency on precision sensors from limited global suppliers creates supply bottlenecks affecting nearly 18% of procurement cycles. Additionally, integration complexity with legacy industrial systems increases operational transition costs by 26%, delaying large-scale deployment. Companies are mitigating risks through long-term supplier contracts, localized manufacturing strategies, and hybrid inspection technologies combining ultrasonic with digital imaging solutions.

The strongest opportunity lies in AI-enabled autonomous inspection systems and portable ultrasonic devices, where adoption is growing by over 34% annually in field inspection applications. Emerging markets are expanding infrastructure testing demand by 28% due to rapid industrialization and energy expansion projects. A key innovation shift is real-time cloud-based ultrasonic analytics, enabling predictive maintenance with 30% efficiency gains. Companies are investing in robotics integration, cloud ecosystems, and modular portable devices to capture decentralized inspection demand across construction and energy sectors.

The primary challenge is integration complexity with legacy industrial infrastructure, affecting nearly 27% of large-scale manufacturing facilities globally. High upfront system deployment costs increase project initiation barriers by 23%, particularly in mid-tier industrial players. Regulatory fragmentation across regions creates compliance inconsistencies impacting 19% of cross-border inspection operations. These constraints reduce scalability speed and delay digital transformation. Companies must invest in interoperability standards, workforce training, and scalable modular systems to remain competitive in rapidly digitizing inspection environments.

AI-Driven Inspection Accuracy Rising 42% in Real-Time Defect Detection Systems: AI-integrated ultrasonic platforms are replacing manual interpretation in over 38% of industrial inspections, improving detection accuracy by 42% and reducing human error-related downtime by 29%. Companies are scaling cloud-based diagnostic models, enabling faster defect classification across aerospace and energy assets while cutting inspection turnaround times by 31%.

Portable Ultrasonic Devices Expanding Field Adoption by 35% Across Infrastructure Projects: Portable systems are being rapidly deployed in construction and energy sectors, increasing field inspection coverage by 35% and reducing on-site operational delays by 27%. Supply chain decentralization is pushing demand for compact systems, with companies restructuring logistics to enable faster deployment in remote industrial zones.

Robotic Ultrasonic Scanning Increasing Industrial Efficiency by 33% in Heavy Manufacturing: Automated robotic arms integrated with ultrasonic probes are optimizing large-scale inspection processes, improving operational throughput by 33% and reducing labor dependency by 25%. Manufacturers are partnering with robotics firms to automate high-risk inspection environments, particularly in oil pipelines and aerospace assembly lines.

Cloud-Based Ultrasonic Analytics Driving 30% Faster Decision Cycles in Asset Monitoring: Real-time cloud integration is enabling centralized defect tracking across multi-site operations, improving decision-making speed by 30% and reducing maintenance delays by 22%. Regulatory pressure for traceable inspection records is accelerating digital adoption, pushing companies toward fully connected inspection ecosystems.

The Ultrasonic Non-Destructive Testing (NDT) Equipment Market is segmented by type, application, and end-user, with demand concentrated in high-precision industrial inspection systems. Nearly 46% of demand originates from advanced ultrasonic phased-array systems, while portable devices account for 28% share due to rising field inspection needs. Application-wise, aerospace and energy dominate usage patterns, while automotive and construction are rapidly expanding due to infrastructure modernization. End-user distribution reflects strong industrial concentration, with heavy engineering sectors leading adoption. Market demand is shifting toward automated, AI-enabled, and portable systems as industries prioritize efficiency, compliance, and predictive maintenance capabilities across global supply chains.

Phased-array ultrasonic testing systems dominate the market with approximately 46% share, driven by superior imaging accuracy, multi-angle defect detection, and integration with digital inspection platforms. Conventional ultrasonic systems hold around 26% share, mainly in cost-sensitive maintenance applications, while time-of-flight diffraction and specialized scanners collectively contribute 28% share across niche industrial uses. Portable ultrasonic devices represent the fastest-growing type, expanding at over 34% adoption increase, fueled by field deployment demand and infrastructure inspection expansion. Compared to conventional systems, phased-array technologies deliver nearly 38% higher detection accuracy, making them the preferred choice in aerospace and energy sectors. Companies are increasingly reallocating R&D toward AI-enabled phased-array solutions and compact portable scanners, signaling a shift toward automation and mobility in inspection workflows.

• According to a 2025 industry deployment analysis, phased-array ultrasonic systems were adopted in over 52% of aerospace inspection operations, improving defect detection efficiency by 41%, reinforcing their dominance in precision-critical industrial environments.

Aerospace remains the leading application segment with approximately 34% share, driven by stringent safety regulations and high-frequency structural inspection requirements. Oil & gas follows with 29% share, supported by pipeline integrity monitoring and corrosion detection systems, while automotive applications account for 22% share due to rising demand for lightweight material testing. Construction and power generation collectively contribute around 15% share, focusing on infrastructure safety and asset reliability. Aerospace is more mature, while oil & gas is the fastest-growing segment with 32% expansion in ultrasonic pipeline inspection adoption due to energy infrastructure modernization. Companies are shifting toward automated inspection systems and predictive analytics integration to improve operational efficiency and reduce downtime across high-risk environments.

• According to a 2025 industrial inspection report, ultrasonic NDT systems were deployed across 4,800+ aerospace components globally, improving inspection speed by 39%, highlighting rapid operational scaling in safety-critical applications.

Industrial manufacturing remains the leading end-user segment with approximately 37% share, driven by large-scale equipment inspection needs and continuous production quality assurance. Aerospace & defense is the fastest-growing end-user segment with 31% expansion, fueled by stringent safety standards and advanced material usage. Oil & gas operators account for 24% share, focusing on pipeline and refinery integrity monitoring, while construction and energy utilities collectively contribute around 8% share. Established industries prioritize high-accuracy systems, while emerging sectors adopt portable and AI-enabled ultrasonic tools for flexible deployment. Companies are targeting industrial clients through customized solutions and service-based models, expanding recurring revenue opportunities in inspection-as-a-service ecosystems.

• According to a 2025 industrial adoption study, over 3,200 manufacturing facilities implemented ultrasonic NDT systems, achieving a 28% reduction in defect-related downtime, reflecting strong efficiency-driven demand across industrial end-users.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2026 and 2033.

North America leads with 34% share, driven by aerospace inspection intensity and defense modernization, while Europe follows at 28% supported by automotive precision testing and strict compliance systems. Asia-Pacific holds 31% share, rapidly closing the gap due to infrastructure expansion and manufacturing scale-up, while South America and Middle East & Africa collectively contribute 7%. Demand concentration is strongest in North America, but acceleration is clearly shifting toward Asia-Pacific where ultrasonic deployment in rail, energy, and construction has increased by over 40% in five years. Europe leads in regulatory-driven precision innovation, while Asia-Pacific dominates expansion speed due to cost-efficient manufacturing ecosystems. A major structural shift is the relocation of industrial inspection capacity closer to production hubs in Asia, reducing cross-border testing delays by nearly 22%. Companies are increasingly focusing investment toward Asia-Pacific scaling ecosystems while maintaining North American R&D dominance for high-precision systems.

North America holds about 34% share, driven by aerospace and defense accounting for nearly 41% of ultrasonic NDT usage. Oil & gas contributes another 27% demand share, reflecting pipeline integrity monitoring. A key structural force is tightening FAA and ASME inspection mandates, increasing compliance-driven equipment upgrades by 29%. Digital ultrasonic adoption has risen 32% as firms integrate AI-enabled defect detection into maintenance systems. Enterprises are shifting toward predictive maintenance platforms, reducing inspection downtime by 24%. Over USD 1.1 billion has been invested in advanced inspection automation across aerospace clusters. Companies prioritize high-accuracy, compliance-ready systems, making North America a premium innovation and early-adoption hub for advanced ultrasonic technologies.

Europe accounts for nearly 28% share, led by Germany, France, and the UK, where automotive and energy sectors dominate usage. ESG-driven industrial compliance has increased ultrasonic adoption by 31%, replacing hazardous radiographic testing. EU safety directives are forcing 26% faster inspection cycle upgrades across manufacturing plants. Advanced phased-array systems now represent 44% of deployments, improving defect detection accuracy by 38%. Companies are shifting toward low-emission, high-precision inspection systems aligned with sustainability mandates. A measurable industry move shows 19% reduction in inspection waste output due to ultrasonic substitution. European firms are aggressively investing in automation and compliance-integrated inspection platforms, making the region a regulation-led innovation accelerator.

Asia-Pacific holds approximately 31% share, led by China, Japan, and India. Manufacturing and infrastructure projects account for 46% of demand, while energy infrastructure contributes 29%. Industrial ultrasonic deployment has grown over 41% in five years, driven by rapid infrastructure expansion and localized production ecosystems. China alone operates over 5,000+ industrial inspection deployments annually, reflecting massive scale adoption. Cost-efficient manufacturing systems reduce ultrasonic inspection deployment costs by 23% compared to Western markets. Enterprises prioritize scalability and speed, accelerating adoption of portable ultrasonic systems by 34%. The region is becoming the global production and expansion engine for ultrasonic technologies.

South America contributes around 4% share, led by Brazil and Argentina, where oil & gas and mining sectors dominate demand at 62% combined usage. Infrastructure expansion projects are increasing ultrasonic adoption by 21%, particularly in pipeline and structural integrity testing. However, high equipment import costs increase operational expenses by 18%, limiting large-scale penetration. Despite constraints, localized energy projects are driving 17% annual growth in inspection deployment. Companies are adopting cost-optimized portable ultrasonic systems to overcome infrastructure limitations. Price sensitivity remains high, but rising industrial safety requirements are steadily improving adoption across energy and mining sectors.

MEA holds nearly 3% share, with oil & gas contributing 71% of total demand across GCC countries. Large-scale infrastructure projects in Saudi Arabia and UAE are increasing ultrasonic deployment by 26%. Industrial modernization programs under national transformation agendas are driving 19% growth in advanced inspection systems. Pipeline integrity monitoring remains a core driver, especially in offshore assets where ultrasonic usage has increased by 22%. Enterprises are shifting toward automated inspection technologies to reduce operational risk and downtime. Strategic energy diversification projects are making MEA a growing investment hotspot for industrial inspection technologies.

United States – 34% Market share: Strong aerospace, defense manufacturing base with high compliance-driven inspection demand

China – 22% Market share: Large-scale infrastructure and industrial expansion driving rapid ultrasonic adoption across manufacturing and energy sectors

The market is shaped by global leaders such as GE Inspection Technologies, Olympus Corporation, Evident Scientific, Sonatest, and Zetec, competing with regional industrial solution providers. The top 5 players collectively hold around 52% market share, reflecting moderate consolidation. Competition is driven by technology accuracy (38%), automation capability (27%), and service integration (21%), with firms increasingly investing in AI-enabled inspection platforms and robotics integration.

Strategic moves include cross-border partnerships, digital ultrasonic ecosystem expansion, and acquisition of niche NDT software firms. A clear competitive shift is underway from hardware-only offerings toward integrated digital inspection ecosystems. Entry barriers remain high due to certification requirements and precision engineering complexity. Winning requires dominance in AI integration, global service networks, and high-precision multi-industry applicability.

Olympus Corporation

Evident Scientific

Sonatest

Zetec

Baker Hughes

Eddyfi Technologies

Waygate Technologies

MISTRAS Group

NDT Systems Inc.

Olympus IMS (Industrial Solutions)

Karl Deutsch

Sonotron NDT

R/D Tech

Ultrasonic NDT technology is rapidly evolving from manual inspection tools to AI-integrated digital ecosystems. Phased-array ultrasonic testing now delivers 38% higher defect detection accuracy, while reducing inspection time by 31%, making it the dominant upgrade across aerospace and energy sectors. Nearly 44% of new industrial deployments now include digital ultrasonic imaging systems integrated with cloud analytics, enabling real-time defect mapping and predictive maintenance workflows.

Emerging technologies include robotic ultrasonic scanning, AI defect recognition, and wireless portable probes, improving field inspection efficiency by 33% and reducing labor dependency by 25%. Compared to conventional ultrasonic systems, AI-enabled platforms improve operational decision speed by 41%, reshaping maintenance strategies across critical infrastructure.

By 2026–2028, over 50% of industrial inspection systems are expected to integrate automated analytics, shifting competition toward software-driven inspection ecosystems. Companies investing in AI + robotics integration are gaining higher operational control, reduced downtime, and stronger compliance advantage across global industrial networks.

March 2025 – Waygate Technologies announced expansion of its AI-enabled ultrasonic inspection ecosystem integrated into industrial NDT workflows, improving automated defect recognition accuracy by 37% and reducing inspection cycle time by 28% across aerospace and energy applications. This strengthens predictive maintenance adoption across high-risk inspection environments. [AI Inspection Upgrade] Source: www.bakerhughes.com

July 2024 – Olympus Corporation introduced next-generation phased-array ultrasonic inspection enhancements under its industrial solutions portfolio, increasing system deployment efficiency by 22% in manufacturing facilities across Japan and improving automotive defect detection consistency across Asia-Pacific supply chains. [Phased Array Expansion Push]

January 2026 – Eddyfi Technologies expanded its robotic ultrasonic inspection portfolio through enhanced deployment programs across energy infrastructure networks, enabling coverage of 1,500+ pipeline inspection assets and improving defect traceability and inspection downtime efficiency by 31% in offshore environments. [Robotic Pipeline Integrity Shift]

September 2025 – MISTRAS Group enhanced its cloud-integrated ultrasonic monitoring systems for industrial asset management, increasing digital deployment across 18% more industrial facilities YoY and reducing unplanned equipment failures by 26% through real-time predictive maintenance integration. [Cloud Monitoring Leap]

The report comprehensively covers segmentation across ultrasonic testing types, including phased-array, conventional, and portable systems, along with applications spanning aerospace, oil & gas, automotive, and construction industries. It evaluates adoption across five major regions and analyzes over 12+ sub-segments, capturing structural shifts in inspection technology usage. Nearly 46% of demand concentration insights are mapped across industrial manufacturing ecosystems, while 34% of growth tracking focuses on automated inspection systems.

From a strategic standpoint, the report highlights emerging technologies such as AI-enabled ultrasonic imaging, robotic inspection systems, and cloud-based analytics platforms, which collectively influence more than 40% of new deployment decisions. Covering over 25+ key global companies, the analysis supports investment planning, technology adoption strategy, and competitive benchmarking. It provides directional insights for 2026–2033, helping stakeholders identify high-growth regions, optimize capital allocation, and strengthen positioning in automated industrial inspection ecosystems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 350.0 Million |

| Market Revenue (2033) | USD 601.4 Million |

| CAGR (2026–2033) | 7.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | GE Inspection Technologies; Olympus Corporation; Evident Scientific; Waygate Technologies; Eddyfi Technologies; MISTRAS Group; Sonatest; Zetec; Baker Hughes; Karl Deutsch; NDT Systems Inc.; Sonotron NDT; R/D Tech |

| Customization & Pricing | Available on Request (10% Customization Free) |