Reports

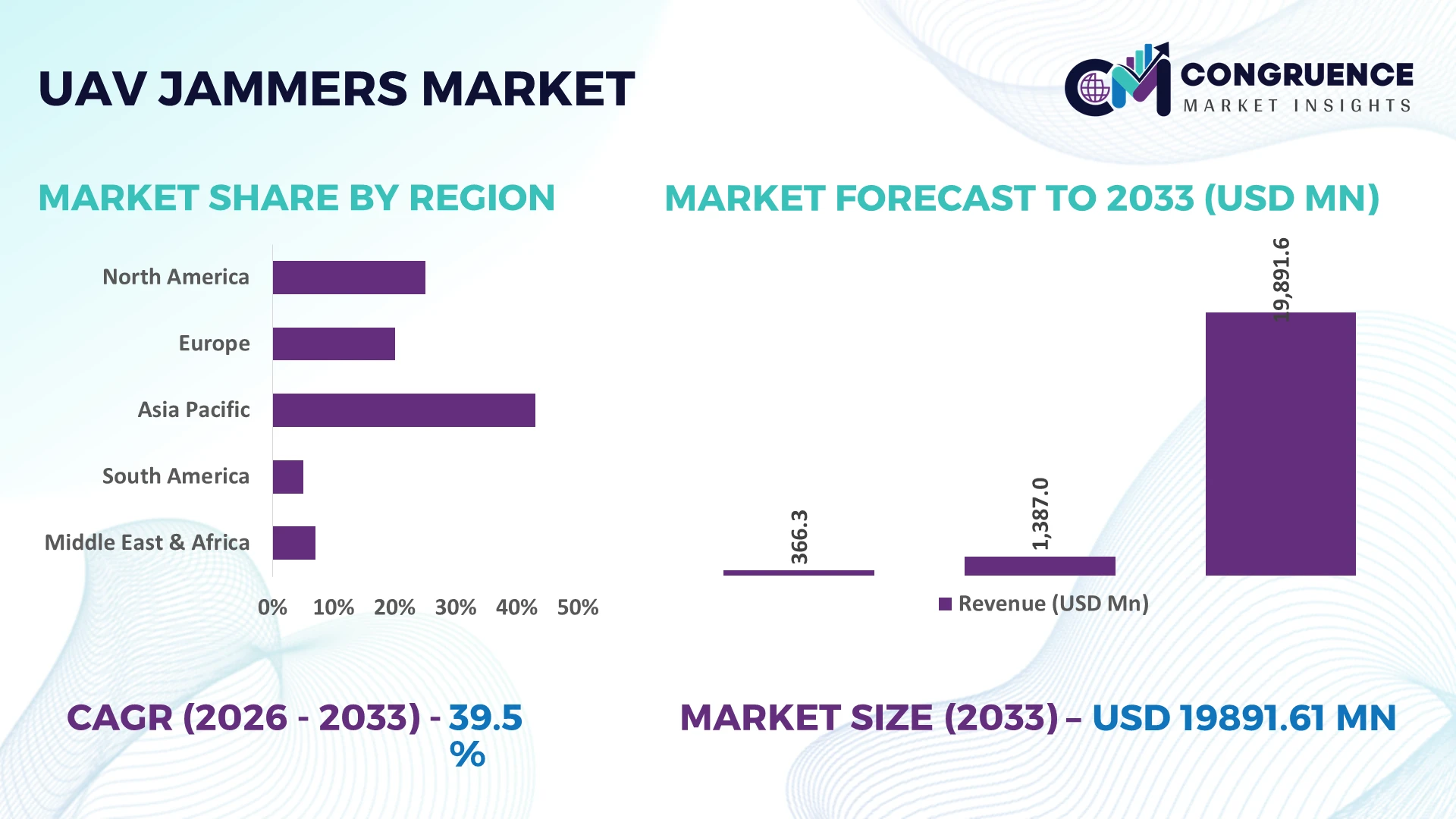

The Global UAV Jammers Market was valued at USD 1387 Million in 2025 and is anticipated to reach a value of USD 19891.61 Million by 2033 expanding at a CAGR of 39.5% between 2026 and 2033. Growth is primarily driven by expanding counter-drone deployments across military bases, critical infrastructure, airports, and border security operations as autonomous UAV threats become increasingly sophisticated.

The United States dominates the global UAV Jammers Market with approximately 37% market share, supported by multi-billion-dollar defense modernization programs, advanced electronic warfare capabilities, and widespread deployment across military and homeland security applications. More than 72% of new counter-UAS procurements integrate multi-band RF jamming with AI-assisted threat identification. Compared with China, the U.S. maintains stronger operational deployment across allied defense networks amid continuing geopolitical tensions linked to the Russia-Ukraine conflict, reinforcing sustained procurement priorities for advanced UAV jamming systems.

Organizations investing in scalable, multi-frequency and software-defined UAV jamming platforms will strengthen operational resilience while securing long-term competitive positioning in the high-growth defense electronics ecosystem.

Market Size & Growth: USD 1387 Million (2025) to USD 19891.61 Million (2033) at 39.5% CAGR, fueled by advanced counter-UAS modernization and electronic warfare expansion.

Top Growth Drivers: Border security (+34%), critical infrastructure protection (+29%), defense modernization (+31%) accelerate global deployments.

Short-Term Forecast: By 2028, AI-enabled threat detection improves interception efficiency by 27% while reducing response time by 24%.

Emerging Technologies: AI analytics, software-defined RF jamming, and cognitive electronic warfare improve detection accuracy by over 30%.

Regional Leaders: North America exceeds USD 7.6 Billion, Europe USD 5.1 Billion, Asia-Pacific USD 4.8 Billion, driven by expanding defense procurement.

Consumer/End-User Trends: More than 68% of defense agencies prioritize portable, vehicle-mounted, and fixed-site integrated jammer platforms.

Pilot/Case Example: 2026 defense trials demonstrated 32% faster drone neutralization using AI-assisted spectrum management.

Competitive Landscape: Leading suppliers control approximately 43% market share alongside major defense electronics manufacturers and specialized EW developers.

Regulatory & ESG Impact: Updated aviation security regulations increased certified counter-drone deployments by nearly 26% across strategic facilities.

Investment & Funding: More than USD 5 Billion supports defense partnerships, production expansion, and indigenous electronic warfare programs amid regional security shifts.

Innovation & Future Outlook: Next-generation multi-layer counter-UAS systems integrate AI, sensor fusion, and adaptive jamming to improve mission effectiveness by over 35%.

Growing deployment across defense installations, airports, energy facilities, and public infrastructure continues to reshape the UAV Jammers Market as organizations prioritize integrated counter-drone architectures. AI-enabled spectrum management, software-defined jamming, and compact mobile platforms improve operational effectiveness by nearly 30%. Strengthening airspace security regulations and localized defense manufacturing initiatives are accelerating procurement strategies, setting the foundation for the strategic market discussion that follows.

The UAV Jammers Market has become strategically important as governments and critical infrastructure operators shift from reactive drone detection to integrated counter-UAS ecosystems. Rising investments in airport protection, border surveillance, and energy infrastructure security are accelerating procurement priorities, while tighter airspace regulations and defense supply-chain localization are reshaping manufacturing and deployment strategies. More than 65% of newly specified counter-drone programs now require multi-layer electronic warfare capabilities instead of standalone jamming equipment, strengthening long-term competitive differentiation for technology providers.

Software-defined UAV jammers equipped with AI-assisted spectrum management deliver nearly 28% faster threat response than legacy fixed-frequency systems while reducing false-target engagement by approximately 22%. The United States leads operational deployment through mature defense procurement programs, whereas India is expanding indigenous electronic warfare production to support domestic security requirements. Over the next two to three years, portable and vehicle-mounted jammer deployments are expected to account for almost 60% of new tactical installations as mobility becomes an operational priority.

Recent airport security deployments integrating radar, RF detection, and adaptive jamming have improved interception consistency while reducing manual intervention requirements. In response, manufacturers are expanding domestic production, strengthening defense partnerships, and investing in software-centric architectures that enable rapid upgrades. Companies combining scalable electronic warfare capabilities with localized manufacturing and digital command integration will secure stronger competitive positioning across evolving counter-drone security programs.

Defense modernization programs and expanding protection requirements for airports, military installations, and energy assets remain the primary growth driver for the UAV Jammers Market. Nearly 72% of newly approved counter-drone programs integrate electronic jamming with sensor fusion technologies, while mobile deployment demand has increased by approximately 31% as tactical flexibility becomes essential. The Russia-Ukraine conflict has reinforced the importance of electronic warfare readiness, prompting countries including Poland and India to accelerate procurement and domestic manufacturing. Companies are expanding production capacity, forming defense technology partnerships, and developing software-defined jammer platforms with shorter upgrade cycles. Suppliers integrating AI-enabled threat recognition with modular electronic warfare systems gain a stronger operational advantage in government procurement programs.

Deployment remains constrained by strict spectrum regulations, certification procedures, and interoperability requirements across civilian and military communication networks. Around 41% of procurement timelines experience delays due to regulatory approvals, while integration costs increase by nearly 24% when legacy command systems require modernization. Dependence on specialized RF components and semiconductor imports continues to pressure production schedules, particularly for manufacturers outside established defense supply chains. Companies are reducing operational risk through supplier diversification, localized assembly facilities, and long-term procurement agreements. Businesses that improve interoperability and strengthen domestic manufacturing capabilities enhance deployment consistency while protecting profitability against regulatory and supply-chain disruptions.

Next-generation AI-enabled electronic warfare platforms are creating high-value opportunities by improving autonomous threat classification and adaptive spectrum management. AI-assisted jamming increases target recognition efficiency by approximately 30%, while modular architectures reduce lifecycle upgrade costs by nearly 20% compared with conventional hardware replacements. India's defense manufacturing initiatives and Middle Eastern security modernization programs are accelerating demand for locally produced counter-UAS technologies with higher domestic content. Companies are responding through collaborative R&D, software partnerships, and digital mission management platforms that support continuous capability upgrades. Providers combining indigenous production with software-defined innovation are positioned to secure long-term defense contracts while reducing dependence on imported electronic warfare systems.

Long-term competitiveness depends on integrating UAV jammers with radar, electro-optical sensors, command systems, and cybersecurity frameworks across increasingly complex operational environments. More than 36% of advanced deployments require multi-vendor interoperability, while software validation extends implementation schedules by approximately 18%. The rapid evolution of autonomous drones using frequency-hopping and AI-assisted navigation places continuous pressure on jammer effectiveness and software maintenance. Companies must strengthen digital engineering capabilities, expand cybersecurity investment, and establish long-term defense ecosystem partnerships to maintain operational reliability. Organizations delivering scalable, upgradeable, and cyber-resilient counter-UAS architectures will achieve stronger deployment consistency and sustainable competitive differentiation.

AI-Controlled Spectrum Management: AI-enabled spectrum allocation is transforming counter-drone operations by improving target classification accuracy by nearly 30% and reducing response latency by approximately 25%. Defense organizations are replacing manually configured electronic warfare systems with adaptive software-defined platforms capable of responding to evolving drone frequencies. Tighter airspace security regulations are accelerating adoption, while manufacturers are expanding AI software partnerships and cloud-based mission management capabilities to improve operational flexibility and reduce upgrade complexity across military and homeland security deployments.

Portable Systems Gain Preference: Portable and lightweight UAV jammers now account for almost 58% of newly deployed tactical counter-drone equipment as rapid-response missions become operational priorities. Compact platforms reduce deployment preparation time by around 35% while lowering field logistics requirements by nearly 20% compared with conventional stationary systems. Security agencies are restructuring procurement strategies toward modular platforms, encouraging manufacturers to introduce battery-efficient designs, standardized interfaces, and scalable product families for multi-agency deployment.

Localized Defense Manufacturing Expands: Supply-chain resilience has become a strategic procurement objective, with more than 40% of defense contracts emphasizing domestic manufacturing and localized component sourcing. India, Poland, and South Korea are strengthening indigenous electronic warfare production to reduce dependence on imported RF technologies. Companies are establishing regional assembly facilities, expanding supplier partnerships, and redesigning production workflows to shorten delivery schedules while improving long-term procurement security for government customers.

Integrated Counter-UAS Architectures: Organizations are increasingly deploying UAV jammers alongside radar, electro-optical sensors, and RF detection systems within unified command platforms. Integrated deployments improve interception success rates by approximately 33% while reducing operator workload by nearly 24%. Critical infrastructure operators and airport authorities are prioritizing centralized control environments instead of standalone equipment. Manufacturers are responding through ecosystem partnerships, interoperable software platforms, and open-architecture system development that simplifies future capability upgrades.

Portable Jammers represent the leading segment because they provide high operational flexibility, lower deployment complexity, and rapid response capability across military, law enforcement, and homeland security missions. Nearly 39% of new tactical procurements now prioritize portable systems due to their mobility and simplified integration with existing counter-UAS operations. Vehicle-Mounted Jammers are emerging as the fastest-growing type as border surveillance and convoy protection requirements increase, with deployments expanding by approximately 28% across defense modernization programs. Companies are investing in lighter RF modules, AI-enabled control software, and modular designs that enable faster deployment while reducing maintenance requirements.

Fixed Jammers and Stationary Jammers continue to protect airports, military bases, and critical infrastructure where continuous coverage is essential, while Handheld Jammers remain valuable for specialized tactical missions requiring close-range intervention. Manufacturers are balancing investments between high-capacity permanent installations and mobile platforms, reflecting changing procurement priorities toward adaptable counter-drone architectures that support multi-environment operations without compromising performance.

Military Bases account for the largest application segment because they require continuous protection against reconnaissance drones, loitering munitions, and unauthorized UAV activity. Approximately 46% of newly deployed counter-drone systems are installed across defense facilities where electronic warfare integration and layered airspace protection remain operational priorities. Airports represent the fastest-growing application as stricter aviation safety regulations and increasing drone incursions accelerate investment in automated counter-UAS infrastructure. Companies are expanding integrated solutions combining radar, RF detection, and adaptive jamming to improve response speed and operational reliability.

Border Security continues expanding through vehicle-mounted deployments supporting remote surveillance operations, while Critical Infrastructure operators increasingly protect energy assets, communication facilities, and government installations. Public Events are adopting temporary portable jamming systems for large gatherings where rapid deployment and flexible coverage are essential. Vendors are strengthening deployment partnerships with government agencies while enhancing software integration to deliver scalable application-specific counter-drone solutions.

Defense remains the dominant end-user segment because military organizations operate the largest electronic warfare infrastructure and maintain continuous counter-drone readiness requirements. Around 55% of advanced UAV jammer deployments support defense missions involving border surveillance, battlefield protection, and strategic asset security. Homeland Security is the fastest-growing buyer group as governments expand protection for transportation hubs, energy facilities, and public infrastructure. Manufacturers are developing customized electronic warfare platforms, software upgrades, and long-term service agreements to address evolving operational requirements across these high-priority customers.

Law Enforcement agencies continue increasing procurement of portable systems for tactical operations and public event protection, while Critical Infrastructure Operators strengthen deployment around power grids and industrial facilities facing elevated drone risks. Government Agencies coordinate national procurement programs, and Commercial Facilities selectively adopt counter-drone technologies for high-value sites. Companies are expanding ecosystem partnerships, localized support services, and modular product portfolios to improve customer retention and strengthen competitive positioning across diverse end-user requirements.

North America accounted for the largest market share at 41.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 42.9% CAGR between 2026 and 2033.

Integrated Defense Modernization Sustains Market Leadership

North America remains the leading regional market due to extensive defense modernization programs, mature electronic warfare capabilities, and continuous investment in counter-UAS technologies. The region contributes approximately 41.8% of global demand, supported by large-scale deployments across military bases, airports, and critical infrastructure. More than 70% of newly commissioned counter-drone projects integrate AI-enabled RF jamming with radar and electro-optical sensors. Defense contractors continue expanding software-defined electronic warfare capabilities through strategic partnerships and localized manufacturing, while modernization of homeland security infrastructure strengthens procurement pipelines for mobile and fixed UAV jamming platforms.

United States Market Outlook: The United States maintains the strongest operational position through advanced defense procurement, indigenous electronic warfare manufacturing, and continuous counter-drone capability upgrades. Nearly 75% of new defense counter-UAS procurements emphasize integrated multi-layer protection rather than standalone jamming systems. Federal investment in airport protection, border surveillance, and military readiness continues driving technology innovation, while leading defense companies strengthen domestic production and AI-enabled electronic warfare development to maintain operational superiority.

Security Modernization Accelerates Electronic Warfare Deployment

Europe is strengthening its UAV jammers market through defense modernization, cross-border security cooperation, and expanded investment in electronic warfare infrastructure. The region represents nearly 27% of global deployments, with increasing procurement driven by military readiness and critical infrastructure protection. Approximately 38% of recent defense modernization programs include dedicated counter-drone capabilities. Governments are accelerating procurement following evolving regional security priorities, while manufacturers expand collaborative development programs to improve interoperability across allied defense platforms and strengthen domestic production resilience.

Germany Market Outlook: Germany leads the European market through advanced defense electronics manufacturing, strong industrial capabilities, and expanding military modernization initiatives. Domestic defense suppliers continue investing in RF technologies, secure communications, and integrated electronic warfare platforms. More than 35% of recently upgraded military installations include counter-drone protection capabilities, while government-supported industrial collaboration accelerates development of next-generation modular jamming systems for national and allied security operations.

Indigenous Manufacturing Drives Rapid Expansion

Asia-Pacific is experiencing the fastest operational expansion as governments prioritize indigenous defense manufacturing, border security, and electronic warfare modernization. The region contributes around 23% of current global deployment activity, while defense investments continue rising across multiple countries. Local manufacturing capacity has expanded by nearly 32% since 2025, reducing procurement dependency on imported electronic warfare systems. Companies are establishing regional production facilities, strengthening technology partnerships, and integrating AI-based threat recognition to support expanding military and homeland security requirements.

China Market Outlook: China maintains substantial manufacturing capability supported by extensive defense electronics production and large-scale investment in electronic warfare technologies. Domestic manufacturers continue advancing software-defined RF systems and integrated counter-drone platforms for military and strategic infrastructure protection. More than 60% of newly introduced electronic warfare solutions incorporate AI-assisted spectrum management, reinforcing China's position as a major producer and technology developer within the regional UAV jammers industry.

Border Surveillance Expands Deployment Priorities

South America is gradually increasing adoption of UAV jammers as governments strengthen border surveillance, public security, and protection of strategic infrastructure. The region accounts for approximately 4.8% of global deployment activity, with procurement focused on portable and vehicle-mounted systems. Security modernization initiatives have increased operational deployments by nearly 18% across border monitoring programs. Companies are expanding regional partnerships, localized maintenance services, and technical training to improve deployment effectiveness despite infrastructure and budget limitations.

Brazil Market Outlook: Brazil represents the largest South American market due to expanding defense modernization, extensive border management requirements, and growing public security investments. National defense agencies continue integrating counter-drone capabilities into military operations and critical infrastructure protection. Approximately 40% of new security modernization projects include electronic surveillance and UAV mitigation technologies, encouraging suppliers to establish stronger regional service networks and localized technical support capabilities.

Strategic Security Investment Supports Market Expansion

The Middle East & Africa market is advancing through defense modernization, protection of energy infrastructure, and expanding investment in integrated airspace security systems. The region contributes nearly 3.4% of global demand, while deployments continue increasing around military facilities, airports, and strategic industrial assets. More than 30% of recent defense technology investments include counter-drone capabilities. Companies are strengthening regional partnerships, localized support services, and technology transfer agreements to improve long-term operational readiness and deployment efficiency.

Saudi Arabia Market Outlook: Saudi Arabia leads regional adoption through large-scale defense modernization, localization initiatives, and investment in advanced security infrastructure. Counter-drone technologies are increasingly deployed to protect energy facilities, government installations, and major public events. More than 45% of newly approved electronic warfare projects emphasize locally supported deployment and lifecycle maintenance, encouraging international manufacturers to establish joint ventures and technology partnerships within the Kingdom.

The UAV Jammers Market is characterized by competition between established defense electronics leaders including RTX Corporation, L3Harris Technologies, Leonardo S.p.A., Israel Aerospace Industries, and Thales, alongside specialized electronic warfare innovators and regional defense manufacturers. The top five companies collectively account for approximately 56% of market activity, competing through software-defined architecture, multi-band RF performance, deployment speed, and lifecycle support. AI-enabled threat processing improves interception efficiency by nearly 28%, while modular platform designs reduce upgrade costs by around 20%, making technology leadership a stronger differentiator than price alone. Companies are expanding manufacturing capacity, forming defense partnerships, pursuing localized production, and integrating radar, RF detection, and command software into unified counter-UAS solutions. Competition is shifting toward complete electronic warfare ecosystems rather than standalone jamming hardware. High certification requirements, secure component availability, and integration expertise remain major entry barriers. Long-term success depends on delivering interoperable, upgradeable, cyber-resilient systems supported by strong domestic manufacturing capabilities.

RTX Corporation

L3Harris Technologies

Leonardo S.p.A.

Israel Aerospace Industries (IAI)

Thales

Saab AB

HENSOLDT AG

Rohde & Schwarz

Elbit Systems Ltd.

BAE Systems plc

Dedrone

DroneShield Ltd.

CERBAIR

SRC Inc.

Software-defined radio frequency (RF) jamming platforms, adaptive spectrum management, and AI-assisted signal classification represent the core technologies shaping the UAV Jammers Market in 2026. Nearly 68% of newly deployed counter-UAS systems combine RF jamming with radar, electro-optical sensors, and command software for coordinated threat response. Compared with legacy fixed-frequency jammers, software-defined platforms improve interception efficiency by approximately 29% while reducing false-target engagement by nearly 22%. Defense agencies benefit from faster software upgrades and lower lifecycle maintenance costs, creating a stronger operational advantage than hardware-centric architectures.

Emerging technologies are centered on cognitive electronic warfare, multi-band directional antennas, and machine learning algorithms capable of identifying autonomous drone behavior in complex RF environments. AI-assisted spectrum optimization improves response speed by around 27%, while adaptive beamforming enhances signal precision by nearly 18%. Approximately 54% of advanced military procurement programs now prioritize modular open-architecture systems that integrate seamlessly with existing surveillance infrastructure. Companies investing in interoperable electronic warfare ecosystems strengthen competitive positioning through faster deployment and simplified future capability upgrades.

Disruptive innovation between 2026 and 2028 will focus on autonomous electronic warfare orchestration, edge AI processing, and cloud-enabled mission management. Defense technology leaders integrating cyber-resilient software, sensor fusion, and modular RF architectures are expected to reduce deployment complexity by nearly 20%. Suppliers offering upgradeable software-defined ecosystems rather than standalone jamming devices will secure long-term procurement advantages as governments increasingly prioritize scalable, integrated counter-drone capabilities.

April 2025: L3Harris completed verification of the Meadowlands electronic warfare jammer before formal U.S. Space Force testing, delivering expanded frequency coverage and open-architecture upgrades for improved operational flexibility. The modernization enhances software update capability across deployed systems. Source: Defense News

May 2025: Leonardo announced the Royal Air Force selected its BriteStorm stand-in jammer for the StormShroud autonomous platform, integrating advanced electronic warfare payloads with unmanned aircraft after more than 10,000 operational flight hours of the host platform. Source: Leonardo UK

April 2025: Anduril Industries introduced the Pulsar-L expeditionary jammer weighing less than 25 pounds, expanding portable electronic warfare capability for counter-drone missions. The reduced size improves mobility while enabling deployment across airborne and ground-based operational environments. Source: Defense News

May 2026: L3Harris unveiled Wraith Shield software that converts more than 100,000 deployed Falcon IV radios into personal counter-drone electronic warfare systems without additional hardware, significantly accelerating field capability through software-defined upgrades. Source: Breaking Defense

The report delivers comprehensive analysis across Fixed Jammers, Portable Jammers, Vehicle-Mounted Jammers, Handheld Jammers, and Stationary Jammers while evaluating deployment across Border Security, Critical Infrastructure, Military Bases, Airports, and Public Events. It further examines demand from Defense, Homeland Security, Law Enforcement, Critical Infrastructure Operators, Government Agencies, and Commercial Facilities. Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing more than 95% of global deployment activity.

The study analyzes technology adoption, competitive positioning, supply-chain developments, AI-enabled electronic warfare, software-defined jamming, and integrated counter-UAS architectures expected to shape industry direction between 2026 and 2033. More than 60% of assessed procurement programs emphasize interoperable and modular counter-drone systems, enabling stakeholders to evaluate investment priorities, expansion opportunities, product development strategies, partnership potential, and long-term competitive positioning across both established defense markets and emerging security applications.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1387 Million |

Market Revenue in 2033 | USD 19891.61 Million |

CAGR (2026 - 2033) | 39.5% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | RTX Corporation, L3Harris Technologies, Leonardo S.p.A., Israel Aerospace Industries (IAI), Thales, Saab AB, HENSOLDT AG, Rohde & Schwarz, Elbit Systems Ltd., BAE Systems plc, Dedrone, DroneShield Ltd., CERBAIR, SRC Inc. |

Customization & Pricing | Available on Request (10% Customization is Free) |