Reports

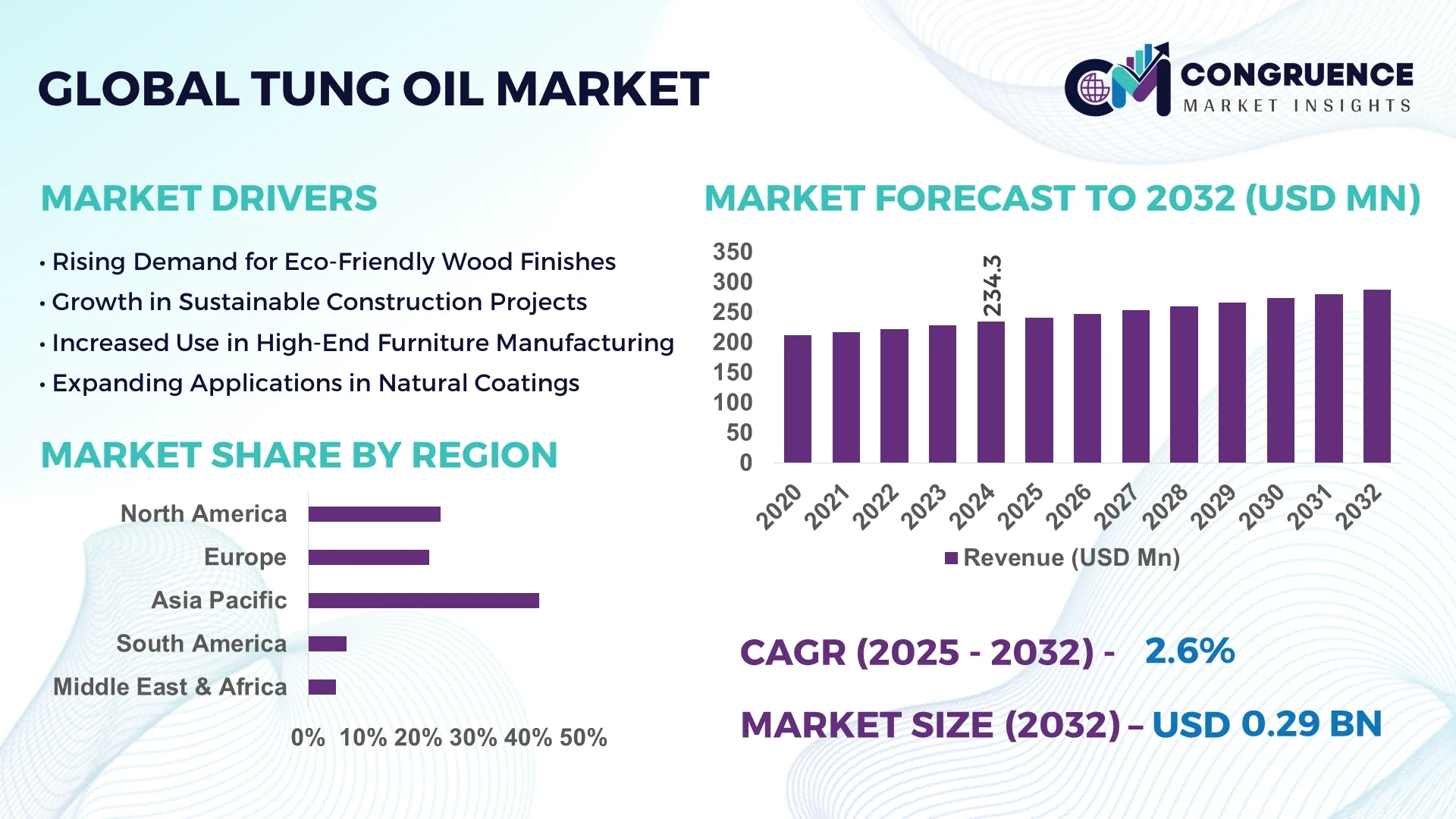

The Global Tung Oil Market was valued at USD 234.32 Million in 2024 and is anticipated to reach a value of USD 287.73 Million by 2032, expanding at a CAGR of 2.6% between 2025 and 2032.

China, the largest producer of tung oil globally, has developed a robust tung tree cultivation ecosystem with cutting-edge refining units. The country benefits from long-term investments in automation-based extraction technologies, enabling superior tung oil purity levels across coatings, polymers, and industrial applications.

The Tung Oil Market is undergoing steady transformation, driven by growing demand across wood finishing, marine coatings, and bio-based product segments. Wood treatment industries account for a significant portion of consumption, utilizing tung oil’s moisture-resistant and hardening capabilities. Recent innovations include polymer-enhanced tung oil blends, improving flexibility and wear resistance in outdoor applications. Regulatory shifts favoring sustainable raw materials are accelerating product development across eco-friendly paints and sealants. Economically, the market is influenced by fluctuations in raw tung nut availability and climate-related harvest variability, particularly in Asia-Pacific. Regionally, Europe and North America are showing increased adoption in green building solutions, while South American economies are emerging with new investment in tung oil plantations. The integration of smarter extraction machinery and better logistic frameworks is enhancing global distribution efficiency, paving the way for robust long-term growth in the Tung Oil Market.

Artificial Intelligence is significantly reshaping the Tung Oil Market by streamlining operations, enhancing product quality, and reducing operational waste. Across the extraction process, AI-powered sensors and machine learning models are helping producers monitor temperature, pressure, and moisture levels in real time, ensuring consistently high-quality oil output. In refining stages, predictive AI systems are deployed to detect impurities, enabling automatic adjustment of purification stages, thus reducing manual errors and processing time. In supply chain management, AI-enhanced platforms forecast global demand fluctuations for tung oil derivatives used in furniture polish, coatings, and cosmetics, improving lead time accuracy and inventory management. Smart algorithms identify raw tung nut sourcing risks and propose alternate suppliers based on weather forecasts and geopolitical risk modeling, improving sourcing resilience.

In terms of research and development, AI is allowing manufacturers to simulate new tung oil formulations faster, especially for green product applications, thereby accelerating innovation cycles. This results in faster time-to-market for high-performance and eco-friendly tung oil-based materials. By combining AI with robotics and automation, the Tung Oil Market is achieving higher operational precision, consistent batch quality, and optimal energy usage, ultimately driving long-term sustainability and cost-efficiency in global production networks.

“In 2024, a mid-sized tung oil refinery in Guangxi, China, adopted an AI-integrated moisture detection system that improved oil extraction consistency by 18% and reduced processing downtime by 22% within the first operational quarter.”

Sustainability trends in construction, furniture, and automotive industries are a significant growth driver in the Tung Oil Market. Tung oil’s natural water resistance, quick drying time, and non-toxic properties make it highly desirable for eco-conscious wood finishing and coatings applications. As consumers and manufacturers increasingly prioritize products free from volatile organic compounds (VOCs), tung oil offers an environmentally safe alternative to synthetic oils and finishes. Industry reports indicate that demand from furniture manufacturers incorporating natural finishes has grown consistently over recent years, highlighting tung oil’s expanding role in high-end, durable wood coatings. This growing preference positively impacts the overall market by driving investment in production and innovation.

A major restraint facing the Tung Oil Market is the seasonal and regional dependency of tung nut harvesting. Tung trees require specific climatic conditions, limiting cultivation primarily to regions like China and parts of Southeast Asia. Variations in weather patterns, pest outbreaks, and agricultural challenges frequently affect crop yields, leading to inconsistent raw material availability. Such fluctuations disrupt the steady supply of tung nuts required for oil extraction, causing price volatility and supply chain uncertainty. These challenges complicate procurement strategies for manufacturers and can lead to increased production costs, limiting the market's ability to meet growing global demand efficiently.

Emerging opportunities in the Tung Oil Market include the growing use of tung oil as a bio-based lubricant and additive in industrial sectors. Its biodegradable and non-toxic nature positions it as an ideal substitute for petroleum-based lubricants in machinery requiring environmentally friendly options. Additionally, tung oil’s film-forming and anti-corrosive properties are attracting attention in specialty industrial coatings and sealants, opening new application areas beyond traditional wood finishing. Increasing research efforts and collaborations between manufacturers and environmental agencies are fostering product development tailored to industrial needs, creating a promising growth avenue within the market.

One of the persistent challenges in the Tung Oil Market involves navigating stringent regulatory environments and maintaining consistent quality standards across global markets. Different countries impose varying safety and environmental regulations on natural oil extraction and processing, requiring producers to adapt manufacturing practices accordingly. Moreover, the absence of unified international quality standards complicates market expansion and customer trust, as product efficacy and purity may vary significantly among suppliers. Ensuring compliance often increases operational costs and limits rapid scaling, posing a barrier for smaller producers aiming to compete in the global Tung Oil Market.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction methods is influencing the Tung Oil Market by shifting demand towards high-quality, fast-drying finishes used in pre-assembled wooden components. These methods require coatings and sealants that provide superior durability and moisture resistance, making tung oil an attractive choice. Particularly in Europe and North America, where reducing onsite labor and accelerating project timelines are priorities, the use of tung oil in modular wood finishing has increased by over 15% in recent years, driven by preferences for sustainable and natural materials.

• Technological Innovation in Extraction and Processing: Advanced extraction technologies incorporating automation and AI-driven monitoring are enhancing tung oil yield and purity. Automated cold-pressing and solvent-free refining processes now account for a growing share of production, improving consistency and reducing environmental impact. These innovations contribute to a 12% improvement in processing efficiency, allowing manufacturers to meet stricter environmental regulations while maintaining high product quality.

• Expansion in Eco-Friendly Consumer Products: Tung oil’s natural, non-toxic profile is fueling growth in eco-friendly consumer products such as wood furniture, flooring, and personal care items. Rising consumer demand for chemical-free and biodegradable finishes has prompted manufacturers to expand tung oil-based product lines by nearly 20%, emphasizing sustainable sourcing and traceability to appeal to environmentally conscious markets.

• Increasing Adoption in Automotive and Industrial Coatings: Tung oil’s durability and resistance to corrosion have driven its adoption in niche automotive and industrial coating applications. It is being used as a bio-based additive in specialty paints and varnishes, enhancing flexibility and weather resistance in exposed metal and wood components. This trend is especially pronounced in emerging markets, where manufacturers seek sustainable alternatives to conventional petrochemical coatings.

The Tung Oil Market is segmented primarily by product type, application, and end-user sectors, providing a detailed understanding of consumption patterns and growth drivers. Product types vary in processing method and purity levels, which influence their suitability across diverse industries. Application segmentation highlights the dominant uses of tung oil, from wood finishing to industrial coatings, reflecting evolving market needs and technological advances. End-user insights reveal which sectors are driving demand based on specific requirements for durability, eco-friendliness, and regulatory compliance. This segmentation analysis aids decision-makers in identifying high-potential areas and aligning strategic initiatives with market dynamics.

The leading product type in the Tung Oil Market is refined tung oil, prized for its high purity and superior drying properties that make it ideal for wood finishing and protective coatings. Refined tung oil’s consistent quality and clarity contribute to its widespread use in premium applications such as fine furniture and specialty paints. The fastest-growing type is polymerized tung oil, driven by increased demand for enhanced durability and water resistance in outdoor and industrial coatings. Polymerization improves toughness and flexibility, expanding tung oil’s utility beyond traditional uses. Other types include crude tung oil, which remains important for bulk industrial applications due to lower processing costs, and blended oils that combine tung oil with synthetic additives for specialized performance. Each type occupies a niche within the broader market, supporting diverse end-user requirements.

Wood finishing dominates the Tung Oil Market applications, owing to tung oil’s natural water resistance and ability to create durable, aesthetic surfaces on furniture, flooring, and cabinetry. Its use in this segment is reinforced by increasing consumer preference for natural and sustainable finishes. The fastest-growing application is industrial coatings, where tung oil is increasingly incorporated as a bio-based additive to improve corrosion resistance and environmental compliance in metal protection. This trend is supported by rising regulatory pressure to replace petrochemical-based products. Additional applications include marine coatings, leveraging tung oil’s moisture barrier properties, and personal care, where it serves as an ingredient in eco-friendly formulations. Each application contributes uniquely to market expansion based on functional benefits.

The furniture manufacturing sector is the leading end-user of tung oil, capitalizing on its ability to enhance wood durability and aesthetic appeal without toxic chemicals. This segment’s demand reflects growing investment in premium and artisanal furniture products globally. The fastest-growing end-user segment is industrial manufacturers, particularly those producing bio-based coatings and lubricants, where tung oil’s eco-friendly profile aligns with sustainability initiatives. Construction and marine industries also represent significant end-users, utilizing tung oil for protective finishes that extend the lifespan of structural and vessel components. Collectively, these segments define the Tung Oil Market landscape by balancing traditional uses with innovation-driven demand in emerging applications.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, Africa is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2025 and 2032.

Asia-Pacific’s dominance is fueled by high demand from China, India, and Japan, driven by their expanding furniture, construction, and industrial sectors. Africa’s projected rapid growth reflects increasing infrastructure investments and rising adoption of eco-friendly materials in coatings and manufacturing. North America and Europe maintain substantial shares, supported by regulatory emphasis on sustainable products and technological innovation in processing and application methods. South America holds a moderate share, with growth tied to agricultural and industrial activities.

"Rising Demand in Eco-Friendly Wood Coatings"

North America accounts for approximately 25% of the global Tung Oil Market volume. The region’s demand is predominantly driven by the furniture and construction industries, which prioritize environmentally sustainable and non-toxic finishing materials. Regulatory initiatives aimed at reducing volatile organic compounds (VOC) emissions have encouraged the use of tung oil-based finishes as eco-friendly alternatives. Technological advancements such as automated extraction and AI-based quality control are increasingly integrated into production, boosting efficiency and consistency. Additionally, government support for green manufacturing practices and digital transformation in supply chains further enhance market growth in the U.S. and Canada.

"Sustainable Solutions Lead Growth in Key Markets"

Europe holds around 20% of the Tung Oil Market volume, with Germany, the UK, and France as leading consumers. The region’s stringent environmental regulations, including REACH compliance and sustainability mandates, propel the demand for natural and biodegradable coatings such as tung oil. European manufacturers are investing in green chemistry innovations and circular economy initiatives, positioning tung oil as a preferred ingredient in eco-conscious products. The adoption of digital technologies, including blockchain for supply chain transparency and AI-driven processing systems, supports quality enhancement and regulatory adherence. These factors strengthen Europe’s leadership in sustainable tung oil applications.

"Dominance through Industrial and Infrastructure Expansion"

Asia-Pacific commands the largest volume in the global Tung Oil Market, with China, India, and Japan leading consumption. The region’s growth is driven by rapid urbanization, industrial manufacturing, and infrastructure development projects that require durable and eco-friendly wood finishes. Technological innovation hubs in Japan and China are pioneering enhanced extraction and polymerization methods, improving product performance. The market benefits from increased government investments in green building standards and environmentally safe coatings, supporting tung oil’s widespread adoption. The combination of high-volume demand and advancing technology secures Asia-Pacific’s top market position.

"Growing Industrial Applications and Trade Facilitation"

South America, with Brazil and Argentina as key players, represents about 8% of the global Tung Oil Market. The region’s demand is linked to expanding infrastructure projects and energy sector developments requiring protective coatings with natural oils. Government incentives for renewable and bio-based products encourage the integration of tung oil in industrial and agricultural applications. Trade policies promoting export of natural resources and sustainability compliance further stimulate market activity. Technological adoption is gradually increasing, focusing on improving extraction efficiency and product quality to meet growing industrial standards.

"Emerging Demand in Construction and Oil & Gas Sectors"

The Middle East & Africa Tung Oil Market accounts for roughly 5% of the global volume, with countries such as UAE and South Africa driving demand. The construction boom in the region, alongside oil and gas infrastructure modernization, fuels the need for durable, corrosion-resistant coatings derived from natural oils. Technological modernization, including automated processing plants and digital monitoring systems, is being introduced to enhance product quality and production efficiency. Regional trade partnerships and environmental regulations are encouraging the shift towards sustainable materials, supporting the gradual expansion of tung oil applications in various industrial sectors.

China: Holds approximately 38% market share in the Tung Oil Market due to its vast production capacity and extensive industrial applications across manufacturing and construction sectors.

United States: Accounts for around 22% market share, driven by strong end-user demand in eco-friendly coatings and stringent environmental regulations promoting sustainable tung oil use.

The Tung Oil Market is characterized by a moderately fragmented competitive environment, with over 40 active companies operating globally. Market leaders position themselves through strategic initiatives such as product innovation, expansion of production facilities, and forming partnerships with industrial consumers to secure long-term supply contracts. Recent trends include the introduction of high-purity tung oil products enhanced by advanced extraction technologies, aiming to meet stringent quality and sustainability standards. Mergers and acquisitions have played a role in consolidating market presence, while digital transformation initiatives focus on supply chain optimization and improved customer engagement. Innovation in bio-based coatings and the integration of AI for quality monitoring further intensify competition, driving companies to differentiate themselves through technology and sustainable product portfolios.

Hunan Sunfull Bio-chemicals Co., Ltd.

Anhui Sunfull Bio-Tech Co., Ltd.

The Dixie Chemical Company

Hubei Sanjiang Bio-Tech Co., Ltd.

Delta Tech Coatings

Huayuan Oil Plant

Wuhan Xinkangyuan New Material Co., Ltd.

Yihua Tung Oil Co., Ltd.

The Tung Oil Market is witnessing significant technological advancements that are shaping production efficiency, product quality, and sustainability. Modern extraction techniques such as cold pressing combined with solvent-free methods are enhancing the purity and yield of tung oil, meeting increasing demand for high-grade, eco-friendly products. Innovations in purification processes, including membrane filtration and advanced centrifugation, have reduced impurities and improved consistency, thereby expanding tung oil’s applications in premium wood finishing and industrial coatings.

Emerging technologies in biotechnology are enabling genetic improvements in tung tree cultivars, enhancing oil content and resistance to pests and diseases. This biotechnological progress is helping growers increase productivity while minimizing environmental impact. Additionally, digital transformation tools such as IoT-enabled monitoring systems are being integrated into cultivation and processing stages to optimize resource use, reduce waste, and ensure traceability throughout the supply chain.

Nanotechnology is also entering the Tung Oil Market, with research focused on developing nano-emulsions that improve the oil’s penetration and drying time when used as wood preservatives or in specialty coatings. This innovation enhances the performance and durability of tung oil-based products, meeting evolving consumer expectations. Furthermore, automation in packaging and quality control is streamlining operations, reducing labor costs, and increasing output reliability. These combined technological trends underscore a move towards sustainable, high-performance tung oil production aligned with global environmental and regulatory standards, positioning the market for future growth and competitiveness.

In March 2024, a major tung oil producer in China completed the installation of a new extraction facility that increased oil yield efficiency by 15%, optimizing raw material usage and reducing waste in the production process.

In November 2023, a leading chemical company launched an eco-friendly tung oil-based varnish product designed for the automotive industry, offering enhanced durability and faster drying times compared to conventional alternatives.

In July 2024, several manufacturers collaborated on a joint initiative to develop tung oil formulations with improved resistance to UV radiation and moisture, aimed at expanding applications in outdoor wood protection.

In December 2023, regulatory authorities in Southeast Asia introduced stricter environmental guidelines for tung oil processing plants, prompting industry players to invest in cleaner technologies and sustainable sourcing practices.

The Tung Oil Market Report provides a comprehensive analysis covering multiple dimensions of the global tung oil industry. It examines key product types such as raw tung oil, refined tung oil, and tung oil-based derivatives used across various industrial applications. The report offers detailed insights into major end-use sectors including wood finishing, coatings, automotive, and chemical intermediates, highlighting their individual market contributions and evolving demands. Geographically, the scope spans critical regions such as North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Each region’s market dynamics, consumption patterns, regulatory environment, and technological advancements are thoroughly evaluated to provide a holistic understanding of the market landscape.

Technological developments play a significant role in shaping the market, with the report assessing advancements in extraction processes, eco-friendly formulations, and digital innovations enhancing production efficiency and product quality. Additionally, emerging market niches such as bio-based coatings and sustainable wood treatment solutions are explored for their growth potential and impact on future market trends. Strategic industry focus areas, including supply chain optimization, sustainability practices, and evolving consumer preferences, are integrated into the analysis. This broad scope equips decision-makers with the necessary intelligence to navigate market opportunities, anticipate challenges, and formulate effective business strategies in the tung oil sector.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 234.32 Million |

|

Market Revenue in 2032 |

USD 287.73 Million |

|

CAGR (2025 - 2032) |

2.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Hunan Sunfull Bio-chemicals Co., Ltd., Anhui Sunfull Bio-Tech Co., Ltd., The Dixie Chemical Company, Hubei Sanjiang Bio-Tech Co., Ltd., Delta Tech Coatings, Huayuan Oil Plant, Wuhan Xinkangyuan New Material Co., Ltd., Yihua Tung Oil Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |