Reports

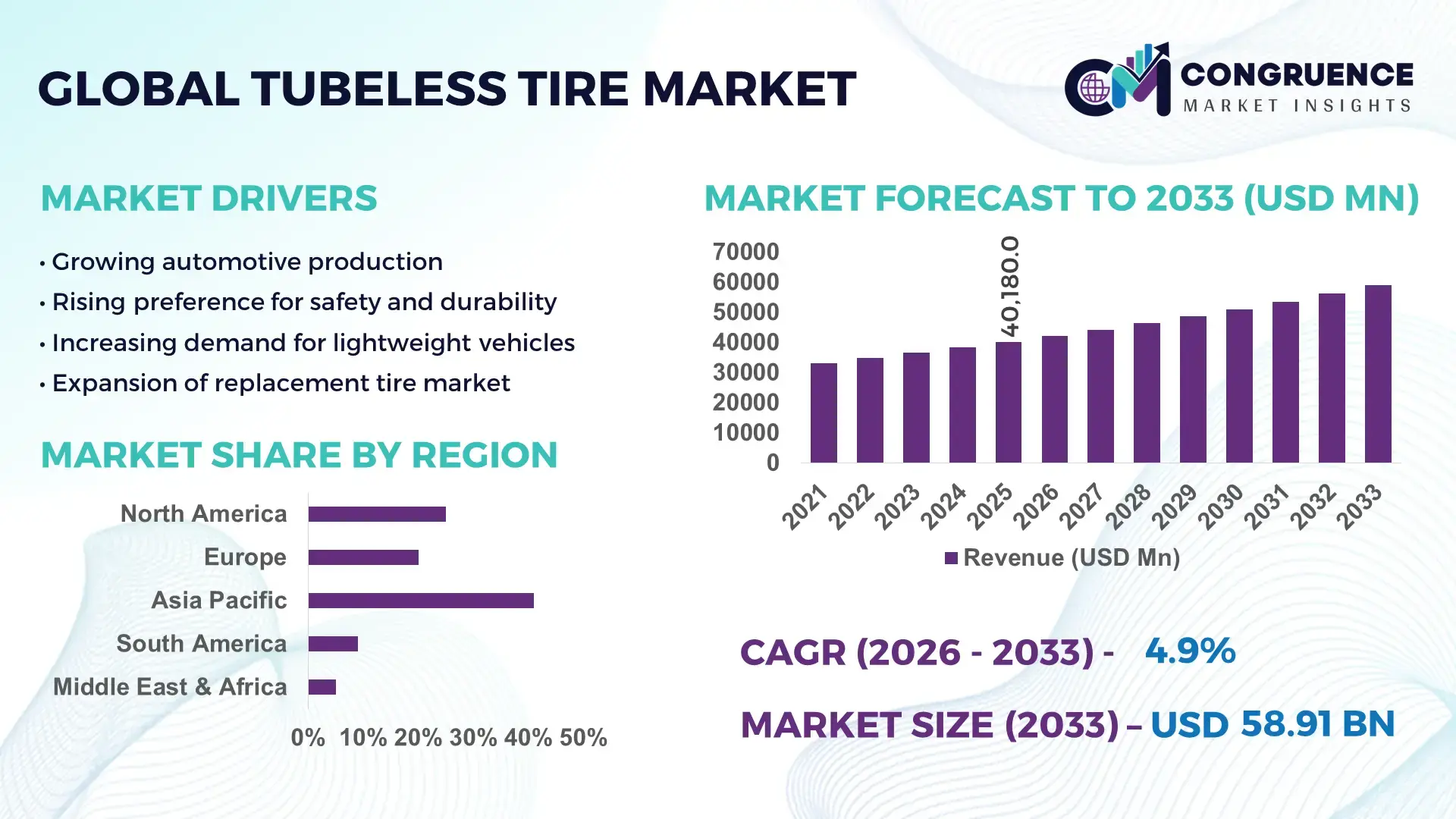

The Global Tubeless Tire Market was valued at USD 40180 Million in 2025 and is anticipated to reach a value of USD 58913.36 Million by 2033 expanding at a CAGR of 4.9% between 2026 and 2033. Growth is supported by rising vehicle production and increasing preference for safety-enhanced, low-maintenance tire solutions across passenger and commercial mobility sectors.

China represents the most influential country in this industry landscape, supported by annual vehicle production exceeding 30 million units and tire manufacturing capacity surpassing 700 million units per year. The country hosts large-scale smart tire plants integrating automated curing, AI-based defect detection, and advanced rubber compounding technologies. Investments in green tire production and silica-based compounds have increased fuel-efficient tire output by over 25% in the past five years. Major applications include passenger cars, electric vehicles, logistics fleets, and construction equipment, with strong domestic OEM integration and expanding export volumes across Asia-Pacific, Europe, and Africa.

Market Size & Growth: USD 40180 Million (2025) to USD 58913.36 Million (2033) at 4.9% CAGR, driven by demand for puncture-resistant, fuel-efficient mobility solutions.

Top Growth Drivers: Vehicle production growth 6%, fleet modernization 8%, fuel-efficiency improvement demand 10%.

Short-Term Forecast: By 2028, rolling resistance reduction technologies to improve fuel efficiency by 7%.

Emerging Technologies: Self-sealing compounds, silica-rich low-resistance tread designs, smart tire pressure monitoring integration.

Regional Leaders: Asia-Pacific USD 24 Billion, Europe USD 15 Billion, North America USD 13 Billion by 2033, each showing EV-compatible tire adoption acceleration.

Consumer/End-User Trends: Rising adoption among urban passenger vehicles and logistics fleets prioritizing durability and maintenance savings.

Pilot or Case Example: 2025 fleet pilot showed 12% downtime reduction using self-sealing commercial tires.

Competitive Landscape: Michelin ~15%, Bridgestone, Goodyear, Continental, Pirelli.

Regulatory & ESG Impact: Emission norms and tire labeling rules pushing low rolling resistance designs.

Investment & Funding Patterns: Over USD 3 Billion invested in automation and sustainable materials expansion.

Innovation & Future Outlook: Growth in EV-optimized, sensor-enabled, and recyclable tire structures.

Passenger vehicles contribute nearly 48% of overall demand, followed by light commercial vehicles at 22% and heavy-duty applications near 18%, with two-wheelers and off-road equipment forming the remainder. Innovations in puncture-resistant liners, sustainable synthetic rubber, and noise-reduction tread geometries are reshaping product portfolios. Regulatory pressure on carbon emissions and tire waste recycling is accelerating eco-friendly production. Asia-Pacific leads consumption volume, while Europe emphasizes performance and labeling standards. Future growth is linked to EV compatibility, digital tire monitoring, and advanced material science integration.

The Tubeless Tire Market holds strong strategic relevance within the global mobility, logistics, and industrial transport ecosystem due to its direct role in vehicle safety, fuel efficiency, and operational uptime. Tubeless designs reduce sudden air loss risks by nearly 30% compared to tube-type systems, making them a preferred specification across passenger vehicles, commercial fleets, and electric mobility platforms. From a strategic operations perspective, fleet operators report maintenance interval extensions of 15–20% when shifting fully to tubeless configurations, translating into measurable lifecycle cost control. Silica-based low rolling resistance compounds deliver 8% improvement in fuel efficiency compared to conventional carbon-black tread standards.

Asia-Pacific dominates in volume, supported by high vehicle production density and large-scale tire manufacturing infrastructure, while Europe leads in adoption with nearly 65% of new passenger vehicles fitted with advanced low-resistance or sensor-enabled tire systems. The market’s future pathway is closely tied to digitalization and sustainability. By 2028, AI-enabled tire monitoring systems are expected to cut fleet tire-related downtime by 18% through predictive pressure and wear analytics.

Sustainability strategies are also reshaping long-term positioning. Firms are committing to ESG metrics such as 40% recycled or bio-based material integration by 2030, alongside reductions in manufacturing emissions. In 2025, a leading Japanese manufacturer achieved a 12% defect reduction through AI-based visual inspection systems in automated curing lines. Going forward, the Tubeless Tire Market is positioned as a core pillar of industrial resilience, regulatory compliance, and sustainable transport growth across both developed and emerging mobility economies.

Global vehicle output exceeding 90 million units annually creates sustained baseline demand for durable tire systems. Fleet modernization initiatives, particularly in urban logistics and e-commerce distribution, prioritize operational reliability, where tubeless systems reduce puncture-related downtime by up to 25% compared to tube-type alternatives. Urban bus and delivery fleets report service interval extensions of nearly 15% due to improved heat dissipation and structural integrity. Growth in electric vehicle deployment further drives demand, as EV platforms typically require low rolling resistance designs to optimize driving range by 5–8%. Infrastructure development in emerging markets adds heavy commercial vehicle demand, while safety regulations in many regions encourage use of tires with enhanced blowout resistance. OEM standardization toward tubeless fitment across passenger and light commercial categories reinforces long-term structural growth.

Natural rubber prices have shown periodic fluctuations exceeding 20% year-over-year, while petrochemical-derived synthetic rubber costs are influenced by crude oil dynamics. These input cost shifts directly impact tire production expenses. Tubeless variants often incorporate advanced inner liners and silica compounds, raising manufacturing complexity. Replacement cycles can be longer, but upfront costs for premium low-resistance or run-flat variants can be 10–18% higher than basic alternatives, affecting price-sensitive markets. Additionally, improper maintenance practices—such as delayed pressure monitoring—can lead to uneven wear, increasing lifecycle costs. Retreading compatibility challenges in certain heavy-duty segments further limit adoption among cost-focused fleet operators. Supply chain disruptions affecting carbon black and specialty chemicals also introduce production scheduling risks.

Electric vehicles, projected to represent over one-third of new vehicle sales in several major economies within this decade, require specialized tire constructions capable of handling higher torque and vehicle mass. This creates opportunity for reinforced, low-noise, low-resistance tubeless designs. Integration of embedded pressure and temperature sensors enables predictive maintenance systems that can reduce unexpected failures by up to 20%. Smart city logistics networks favor connected fleet platforms, where tire performance data supports route optimization and asset life extension. Sustainable material innovation, including bio-based rubber and recycled carbon black, aligns with corporate carbon reduction commitments. Off-road electrification in mining and agriculture also opens new application niches requiring heavy-duty puncture-resistant structures.

Global tire performance regulations vary in labeling, rolling resistance thresholds, wet grip classifications, and noise emission limits, requiring manufacturers to maintain multiple product specifications. Testing and certification cycles can extend beyond 12 months for new designs, delaying commercialization. Environmental mandates on chemical usage and end-of-life recycling impose additional compliance costs. Increasing expectations for sustainable sourcing push manufacturers to redesign material supply chains. In heavy-duty segments, performance consistency across diverse terrains remains a technical hurdle, as balancing durability, efficiency, and load-bearing capacity involves trade-offs. Additionally, counterfeit or substandard products in some markets undermine brand trust and distort pricing structures, complicating quality assurance and enforcement efforts.

• EV-Optimized Tire Designs Improving Energy Efficiency by 6–10% Modern electric vehicles place 15–20% higher load stress on tires due to battery weight, accelerating the shift toward reinforced tubeless structures with low rolling resistance compounds. Advanced silica tread formulations and aerodynamic sidewall designs are enabling energy efficiency improvements of up to 10%, directly supporting extended driving range and reduced tire wear in urban EV fleets.

• Smart Sensor Integration Expanding Fleet Monitoring Adoption by 25% Embedded tire pressure and temperature monitoring sensors are increasingly integrated into commercial tubeless tires. Fleet operators deploying connected tire systems have reported up to 18% fewer roadside failures and 12% longer service intervals. Adoption of sensor-enabled tires in logistics fleets has increased by nearly 25% over the past three years, driven by predictive maintenance strategies.

• Sustainable Material Usage Rising with 30–40% Recycled Content Targets Manufacturers are scaling the use of recycled carbon black, bio-based rubber, and sustainable silica fillers. Several large producers have introduced tire lines incorporating up to 40% renewable or recycled materials, contributing to 8–12% reductions in lifecycle carbon footprint. Regulatory pressure on waste tire recovery is also pushing circular production models across Europe and parts of Asia.

• Growth in Run-Flat and Self-Sealing Technologies Reducing Downtime by 15% Safety-focused designs such as self-sealing inner liners and reinforced sidewalls are gaining traction in passenger and premium vehicle segments. Vehicles equipped with these tubeless variants show puncture-related downtime reductions of up to 15% and improved high-speed stability by nearly 7%, supporting adoption in both private mobility and executive fleet categories.

The Tubeless Tire Market segmentation reflects differentiated demand patterns across product types, vehicle applications, and end-user categories. Product diversification is shaped by performance requirements such as durability, rolling resistance, puncture protection, and load-bearing capacity. Radial and advanced compound-based variants dominate modern mobility platforms due to superior heat dissipation and structural stability. Application-based demand is concentrated in passenger mobility, commercial logistics, and specialized off-road operations, where reliability and operational uptime are critical performance metrics. End-user segmentation highlights the strong role of OEM fitment programs, which account for a large proportion of initial installations, while the aftermarket remains vital for replacement cycles and performance upgrades. Electrification trends are also influencing segmentation, with EV-compatible tires requiring up to 20% stronger load-handling capacity and noise-optimized tread designs. Regional consumption patterns differ, with high-volume adoption in industrialized manufacturing economies and technology-driven uptake in regions prioritizing fuel efficiency and environmental compliance. This segmentation structure provides a clear framework for product innovation, channel strategy, and long-term capacity planning.

Radial tubeless tires lead this segment, accounting for approximately 58% of total adoption, due to their superior tread life, 10–15% better fuel efficiency, and improved high-speed stability compared to bias constructions. Bias tubeless tires hold around 21%, remaining relevant in heavy-duty and off-road environments where sidewall strength is prioritized over rolling efficiency. Run-flat tires represent nearly 11%, gaining traction in premium passenger vehicles due to their ability to maintain mobility for up to 80 km after pressure loss. Self-sealing variants contribute about 6%, mainly in urban passenger applications focused on puncture resistance. Low rolling resistance specialty types form the remaining 4% niche, primarily in EV platforms.

While radial designs dominate, self-sealing tires are the fastest-growing type with an estimated CAGR of 7.2%, supported by safety preferences and urban fleet usage. Growth is driven by reduced roadside assistance incidents, which decline by nearly 15% in vehicles equipped with self-sealing liners. Other specialty performance types collectively serve industrial and defense mobility segments with targeted structural enhancements.

Passenger vehicles constitute the leading application, representing about 48% of total usage, supported by annual global car production exceeding 70 million units and rising safety compliance standards. Light commercial vehicles account for roughly 22%, driven by last-mile delivery fleets that require extended service intervals and 15% lower downtime rates. Heavy commercial vehicles hold around 18%, where tubeless configurations reduce blowout risks under high loads. Two-wheelers and off-the-road machinery together contribute the remaining 12%, serving mobility in developing regions and construction sectors.

Passenger vehicle applications dominate, yet electric vehicle usage is the fastest-growing application with a projected CAGR of 8.1%, fueled by rising EV production and demand for low-noise, reinforced load-bearing designs. EV-compatible tubeless tires improve driving range by 6–8% through optimized rolling resistance. Other segments, including agricultural and mining equipment, maintain steady demand due to puncture resistance and heat control benefits.

OEMs lead the end-user landscape, accounting for approximately 54% of installations, as vehicle manufacturers increasingly standardize tubeless configurations for safety and performance. The aftermarket represents about 31%, supported by replacement cycles averaging 3–5 years and growing consumer preference for premium variants. Fleet operators contribute nearly 10%, with adoption rising in organized logistics and public transportation networks. Automotive service providers and specialty industrial users make up the remaining 5%.

OEM dominance is evident; however, fleet operators are the fastest-growing end-user segment with an estimated CAGR of 7.8%, driven by predictive maintenance programs and connected tire monitoring that reduce breakdown incidents by up to 20%. Aftermarket demand is sustained by performance upgrades and EV tire replacements.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 5.6% between 2026 and 2033.

Asia-Pacific benefits from annual vehicle production exceeding 50 million units and tire output surpassing 900 million units, supporting strong replacement and OEM demand. North America holds close to 24% share, driven by high penetration of passenger vehicles, where over 70% of cars use radial tubeless configurations as standard. Europe contributes approximately 22%, supported by stringent rolling resistance and labeling standards influencing purchasing decisions. South America represents about 7%, with demand concentrated in Brazil and Argentina’s commercial transport and agricultural sectors. The Middle East & Africa account for nearly 6%, driven by construction fleets and mining operations. EV-compatible tire adoption has surpassed 18% of new installations in developed regions, while sensor-enabled tire penetration is approaching 12% in organized fleet networks, indicating rising digitalization in tire performance monitoring.

How is advanced mobility demand reshaping product innovation and replacement cycles?

North America contributes approximately 24% of global volume, supported by high passenger vehicle ownership exceeding 800 vehicles per 1,000 people in certain areas. Logistics, e-commerce distribution, and long-haul freight are key industries driving demand, with fleet operators seeking up to 20% longer service intervals through durable radial constructions. Regulatory emphasis on fuel efficiency and safety compliance standards influences design adoption, particularly low rolling resistance tread compounds. Digital transformation is evident as connected fleet solutions expand, with sensor-enabled tire monitoring used in nearly 15% of large fleet vehicles. A major regional manufacturer has expanded smart tire production lines integrating automated curing and AI-based quality inspection, increasing defect detection accuracy by 10%. Consumer behavior reflects preference for all-season durability and winter performance adaptability, with replacement purchases often tied to seasonal climate variation.

Why are sustainability mandates accelerating demand for high-efficiency tire technologies?

Europe accounts for about 22% of global consumption, with Germany, the UK, and France representing major automotive production and replacement hubs. Strict environmental and tire labeling frameworks encourage low rolling resistance products, improving vehicle efficiency by up to 7%. Sustainability initiatives target reductions in tire noise levels below 70 dB and improved wet grip classifications. Adoption of silica-rich tread compounds and recyclable material blends is increasing, with sustainable material incorporation reaching 30% in certain product lines. A regional tire producer has implemented renewable energy-powered manufacturing lines, reducing operational emissions by 15%. Consumers demonstrate higher preference for performance-certified, eco-labeled products, reflecting regulatory influence and environmental awareness.

How are manufacturing scale and mobility expansion driving demand acceleration?

Asia-Pacific leads global volume rankings, producing more than 900 million tires annually. China, India, and Japan are primary consumption centers, with strong OEM integration and expanding vehicle fleets. Infrastructure growth in logistics corridors and urban transport networks sustains commercial vehicle tire demand. Regional innovation hubs focus on automated production, advanced polymer blending, and EV-compatible designs. A leading domestic manufacturer recently expanded capacity by 12% through smart factory upgrades, improving production efficiency and reducing defect rates. Consumer behavior reflects price sensitivity in developing economies and rapid adoption of durable radial designs in urban passenger vehicles.

What factors are strengthening demand across transport and agricultural mobility segments?

South America represents about 7% of global share, with Brazil and Argentina leading consumption. Road freight transport and agricultural machinery are primary demand drivers, as long-distance haul routes require puncture-resistant structures. Infrastructure investments in road networks and logistics modernization contribute to replacement demand cycles. Trade agreements supporting regional manufacturing have improved component supply stability. A local producer increased regional distribution capacity by 8%, improving delivery lead times for commercial vehicle tires. Consumers show strong preference for durability and retread compatibility, especially in heavy transport and farming applications.

How are industrial operations and infrastructure expansion influencing adoption?

The Middle East & Africa account for nearly 6% of global demand, driven by oil & gas transport, mining, and large-scale construction fleets. Countries such as the UAE and South Africa lead regional consumption. Harsh climatic conditions create demand for heat-resistant and reinforced sidewall designs. Trade partnerships and import facilitation policies support steady supply chains. Technological modernization includes adoption of automated tire service systems in large fleets. A regional distributor expanded warehouse automation, reducing supply turnaround time by 9%. Consumer patterns emphasize durability under high-load and high-temperature conditions, particularly in industrial operations.

China – 28% share in the Tubeless Tire Market; dominance supported by large-scale manufacturing capacity and strong OEM integration.

United States – 17% share in the Tubeless Tire Market; leadership driven by high vehicle ownership levels and advanced fleet modernization programs.

The Tubeless Tire Market exhibits a moderately consolidated structure, with over 120 active global and regional manufacturers competing across passenger, commercial, and specialty mobility segments. The top five companies collectively account for approximately 46% of total industry volume, reflecting strong brand equity, global manufacturing networks, and advanced R&D capabilities. Competitive positioning is increasingly defined by innovation in low rolling resistance compounds, where new silica-based tread technologies improve fuel efficiency by 6–10%, and by safety-enhancing features such as self-sealing and run-flat systems.

Strategic initiatives include capacity expansions exceeding 8–12% at several major production facilities to meet EV-compatible tire demand. Partnerships between tire manufacturers and automotive OEMs are increasing, particularly for original fitment of sensor-enabled tire systems integrated with vehicle telematics. Product launches focusing on EV-specific load-bearing capacity have risen by nearly 20% over the past three years. Mergers and regional joint ventures are also strengthening distribution reach in emerging markets, improving delivery efficiency by up to 15%. Digital transformation in manufacturing—such as AI-driven defect detection—has reduced production scrap rates by around 10% among leading firms. Sustainability competition is intensifying, with several producers targeting 30–40% renewable or recycled material usage in next-generation tire lines.

Michelin

Bridgestone Corporation

Goodyear Tire & Rubber Company

Continental AG

Pirelli & C. S.p.A.

Sumitomo Rubber Industries

Hankook Tire & Technology

Yokohama Rubber Company

Toyo Tire Corporation

Nokian Tyres

Kumho Tire

Apollo Tyres

CEAT Limited

Maxxis International

Giti Tire

Technological advancement in the Tubeless Tire Market is centered on material science, digital integration, and performance optimization. Modern tubeless tires increasingly use silica-rich tread compounds, which lower rolling resistance by 6–10% compared to conventional carbon-black formulations, directly supporting vehicle fuel efficiency and EV range extension. Advanced synthetic rubber blends and functionalized polymers improve abrasion resistance by nearly 15%, extending service life in both passenger and commercial applications. Reinforced bead wire technology and improved inner liner compositions reduce air permeability by up to 20%, maintaining stable inflation pressure over longer operational cycles.

Digital transformation is another defining trend. Sensor-embedded tires capable of monitoring pressure, temperature, and tread wear in real time are now integrated in approximately 12–15% of organized fleet vehicles. These smart tire systems enable predictive maintenance models that reduce unexpected breakdown incidents by nearly 18%. AI-driven quality inspection during tire curing processes has improved defect detection accuracy by about 10%, while automation in mixing and molding operations increases production consistency and throughput efficiency.

Emerging technologies also include self-sealing elastomer layers capable of automatically closing punctures up to 5 mm in diameter, cutting roadside repair events by nearly 15%. Noise-reduction tread pattern engineering lowers external rolling noise by 2–3 decibels, supporting compliance with urban transport noise regulations. Sustainable material innovation is expanding, with recycled carbon black and bio-based oils contributing up to 30–40% of material composition in select product lines, aligning with industry decarbonization targets. These advancements collectively strengthen product differentiation, regulatory compliance, and operational efficiency across the market.

• In March 2025, Continental AG expanded its tubeless tire portfolio by launching the Conti Eco Gen 5 and Urban HA 5 lines featuring RFID chips and optional digital sensors, improving fleet pressure monitoring and lifecycle management across commercial applications.

• In 2024, Michelin introduced the X Multi Energy Z+ tubeless commercial vehicle tyre in India, engineered with the industry’s lowest rolling resistance for its category and delivering up to 15% fuel savings alongside 20% longer service life compared to conventional designs.

• In March 2025, Continental partnered with Bosch eBike Systems to co-develop tubeless-ready e-bike tyres with integrated pressure monitoring and data-sharing capabilities, advancing digital performance tracking for urban and recreational electric bicycles.

• In September 2024, Michelin expanded its off-road tubeless offerings with the Michelin e-Adventure TL tyre for electric mountain bikes, featuring reinforced sidewalls and enhanced puncture protection tailored to higher torque e-bike configurations.

The Tubeless Tire Market Report encompasses a detailed and structured analysis of industry breadth, examining product configurations, application sectors, regional deployment, technology integration, and end-user behavior. It covers segmentation by types—such as radial, bias, run-flat, self-sealing, and low rolling resistance variants—highlighting unique performance characteristics and engineering design considerations for passenger vehicles, commercial fleets, two-wheelers, and off-road equipment. The report also analyzes application scope across OEM fitments and aftermarket replacements, outlining how adoption patterns vary with vehicle usage intensity, maintenance cycles, and performance requirements.

Geographically, the report provides granular insights into North America, Europe, Asia-Pacific, South America, and Middle East & Africa, emphasizing regional consumption volumes, regulatory influences, and manufacturing ecosystems. It explores technology trends including smart sensor integration, predictive maintenance analytics, compound innovations, and EV-compatible designs, reflecting how digital and material advances reshape competitive dynamics. Detailed end-user profiling examines demand drivers among OEMs, fleet operators, automotive service providers, and individual consumers, alongside decision criteria influencing purchase preferences.

Additionally, the report assesses emerging and niche areas like e-bike tubeless systems, commercial EV fleet tyres, and sustainable material initiatives. Regulatory and policy landscapes—including labeling, fuel-efficiency standards, and environmental mandates—are evaluated for their impact on product specifications and compliance priorities. Overall, the scope provides strategic decision-making support through a comprehensive overview of operational, technological, and market direction factors.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Michelin , Bridgestone Corporation, Goodyear Tire & Rubber Company , Continental AG, Pirelli & C. S.p.A., Sumitomo Rubber Industries, Hankook Tire & Technology, Yokohama Rubber Company, Toyo Tire Corporation, Nokian Tyres, Kumho Tire, Apollo Tyres , CEAT Limited, Maxxis International, Giti Tire |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |