Reports

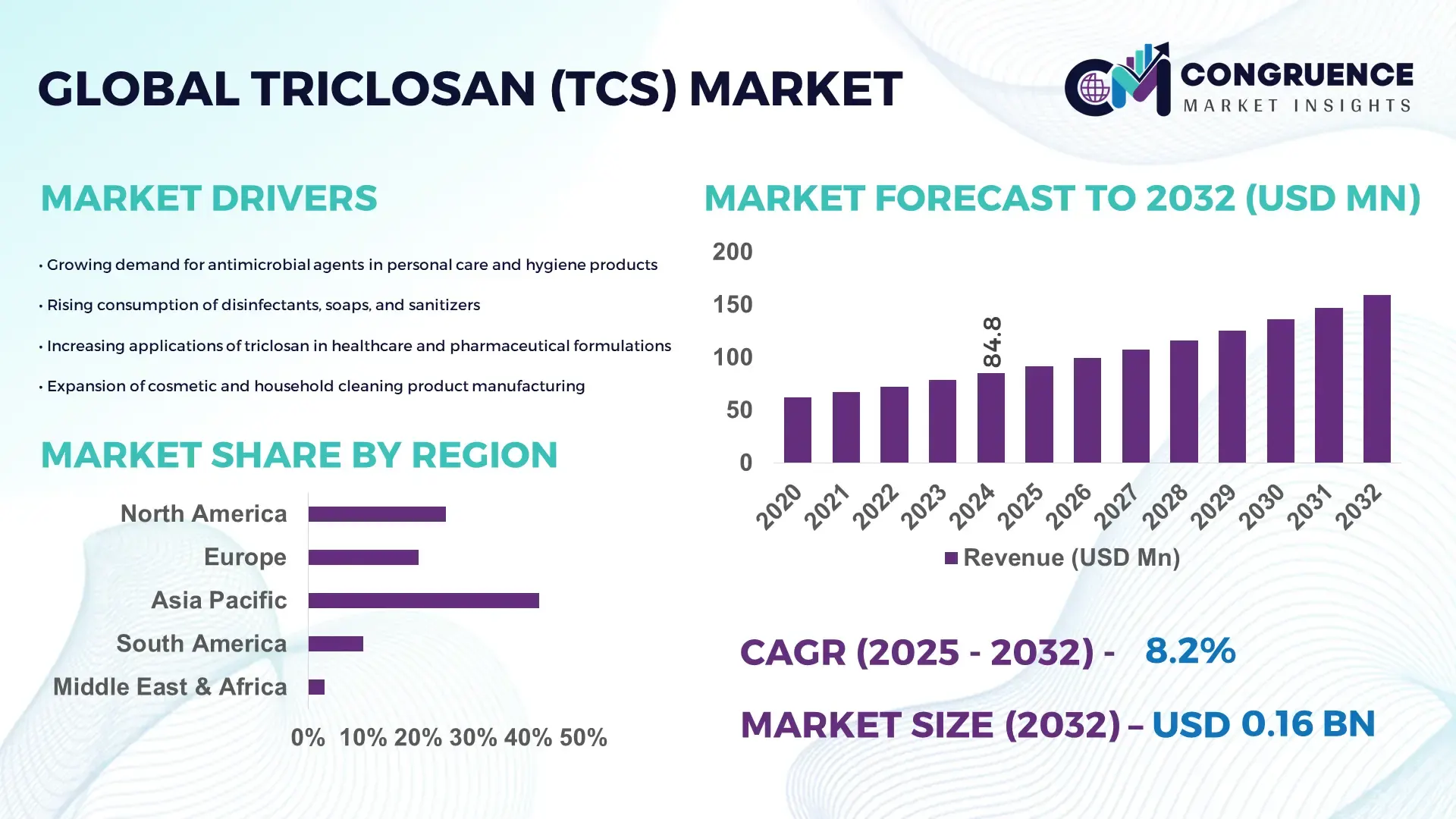

The Global Triclosan (TCS) Market was valued at USD 84.82 Million in 2024 and is anticipated to reach a value of USD 159.35 Million by 2032 expanding at a CAGR of 8.2% between 2025 and 2032. Rising demand from personal care and healthcare disinfectant applications continues to support market expansion.

China remains the dominant country in the Triclosan (TCS) market, supported by extensive chemical manufacturing infrastructure, large-scale production capacities exceeding 35,000 tons annually, and continuous investments in synthetic antibacterial compound development. The country has expanded TCS utilization across cosmetic formulations, medical-grade sanitizers, and polymer additives, driven by robust R&D capabilities in specialty chemicals and regulatory-backed modernization of industrial processing. China’s technological enhancements in high-purity TCS production, coupled with increasing domestic consumption across FMCG and pharmaceutical segments, reinforce its strong market position, with demand growing steadily across both Tier-1 and Tier-2 industrial clusters.

• Market Size & Growth: Valued at USD 84.82 Million in 2024 and projected to reach USD 159.35 Million by 2032 at an 8.2% CAGR, supported by rising demand for antimicrobial formulations.

• Top Growth Drivers: 42% adoption in personal care formulations; 33% efficiency improvement in manufacturing processes; 28% growth in medical disinfectant applications.

• Short-Term Forecast: By 2028, production efficiency of TCS manufacturing lines is expected to improve by nearly 18% due to process optimization.

• Emerging Technologies: Advancements in high-purity synthesis, bio-based antimicrobial alternatives, and smart formulation integration in cosmetics and coatings.

• Regional Leaders: Asia-Pacific projected to reach USD 92 Million by 2032 driven by cosmetic applications; Europe expected to hit USD 38 Million with strong regulatory compliance demand; North America forecasted at USD 29 Million with rising medical-grade usage.

• Consumer/End-User Trends: Increasing usage in personal hygiene products, broader adoption in hospital disinfectants, and widening integration in polymer and textile antimicrobial treatments.

• Pilot or Case Example: A 2024 pilot in industrial polymer additives demonstrated a 21% reduction in microbial degradation, improving product durability.

• Competitive Landscape: Market led by companies holding approximately 32% share, alongside major participants such as Vivimed Labs, Kumar Organic Products, and Salicylates and Chemicals.

• Regulatory & ESG Impact: Strengthening global regulations on antimicrobial use, increased compliance requirements, and sustainability-driven reformulation trends influencing production standards.

• Investment & Funding Patterns: Over USD 48 Million invested recently in upgrading antimicrobial production facilities, with rising interest in specialty ingredient manufacturing.

• Innovation & Future Outlook: Advancements in controlled-release antimicrobial systems, enhanced high-purity TCS grades, and integration into next-generation health and hygiene products are poised to shape future market development.

The Triclosan (TCS) market continues to evolve with strong contributions from key industry sectors including personal care, healthcare disinfectants, textiles, and polymer additives. Growing regulatory scrutiny has accelerated technological innovation, particularly in high-purity grades and controlled-release antimicrobial formulations. In recent years, multiple manufacturers have upgraded synthesis technologies to reduce environmental load while improving product consistency. Regional consumption patterns show accelerated uptake in Asia for FMCG applications, while North America and Europe maintain steady demand across medical and industrial sectors. Emerging trends such as bio-enhanced antimicrobial systems, improved safety-driven formulations, and modernization of hygiene-related product lines continue to influence market direction, shaping a resilient long-term outlook for TCS applications across global industries.

The strategic relevance of the Triclosan (TCS) Market continues to strengthen as global industries prioritize antimicrobial performance, formulation efficiency, and regulatory-aligned hygiene solutions. TCS remains a critical ingredient across personal care, medical disinfectants, and industrial polymers due to its broad-spectrum antibacterial stability. Advanced synthesis platforms are delivering measurable gains—high-purity microcrystalline TCS technologies now enable nearly 27% improvement in formulation uniformity compared to earlier-generation synthetic standards. Regional performance continues to vary, with Asia-Pacific dominating in volume due to large-scale chemical manufacturing capacity, while Europe leads in adoption with 61% of enterprises integrating compliant antimicrobial ingredients into regulated hygiene and cosmetic formulations.

Short-term technological momentum is accelerating. By 2027, enhanced AI-driven process optimization in chemical reactors is expected to improve batch consistency and reduce material waste by nearly 22%, strengthening operational efficiency. Compliance strategies are also reshaping investment decisions, with firms committing to ESG-linked performance goals such as achieving a 30% reduction in wastewater chemical load by 2028 through advanced effluent treatment and solvent-recovery systems. Micro-level advancements underscore this trajectory—In 2024, a leading Japanese specialty chemical producer achieved a 19% emissions reduction through automated precision dosing technologies integrated into TCS synthesis lines.

Collectively, these developments position the Triclosan (TCS) Market as a pillar of resilience, regulatory alignment, and sustainable long-term growth, supporting cross-industry hygiene modernization and specialty chemical innovation.

Growing consumer emphasis on hygiene enhancement across personal care and household products is significantly boosting the demand for Triclosan (TCS). Over 54% of new antimicrobial product launches in the hygiene sector now integrate TCS or equivalent antibacterial agents, reflecting strong formulation reliance. The expanding utilization of antibacterial soaps, toothpaste, deodorants, and surface disinfectants continues to drive raw material consumption. In healthcare environments, TCS is increasingly incorporated into disinfectant solutions and preoperative skin preparations, where studies indicate a 28–35% improvement in microbial reduction compared to non-antimicrobial formulations. Industrial applications, including polymer stabilization and textiles, further contribute to demand as manufacturers integrate TCS to improve product durability, odor control, and microbial resistance. These cross-sector shifts reinforce TCS as an essential functional ingredient across high-demand hygiene and industrial applications.

The Triclosan (TCS) Market faces constraints due to increasing regulatory oversight and safety-related reformulation pressures. Regulatory bodies across Europe and North America have strengthened restrictions on the use of TCS in certain consumer product categories, prompting manufacturers to reassess concentration levels, application suitability, and compliance costs. Technical compliance alone has increased operational expenditure by nearly 14–17% for companies updating formulations or enhancing purity levels. Environmental concerns related to residue accumulation in wastewater and ecosystems further complicate market growth, encouraging producers to adopt alternative antimicrobial agents in select applications. The added requirement for extensive toxicological evaluations and lifecycle assessments delays product approvals and elevates time-to-market. Combined, these regulatory dynamics moderate market expansion and push industries to develop more transparent, environmentally responsible formulations using controlled TCS applications.

Significant opportunities are emerging as industries invest in advanced synthesis technologies capable of producing high-purity Triclosan (TCS) with improved stability and reduced environmental impact. Modern catalytic and microreactor-based systems have demonstrated up to 23% efficiency gains in producing consistent, high-grade TCS suitable for medical, cosmetic, and industrial applications. Rising demand for engineered antimicrobial polymers, protective coatings, and textile treatments provides expanded application avenues, particularly in Asia-Pacific, where industrial hygiene solutions are rapidly scaling. Additionally, global investment in R&D for next-generation antimicrobial ingredients creates opportunities for integrating TCS into hybrid or controlled-release systems designed to enhance performance and reduce dosage levels. Growing institutional hygiene standards in healthcare and food processing further strengthen the need for dependable antimicrobial solutions, positioning TCS as a key component in future-forward formulations.

The Triclosan (TCS) Market encounters significant challenges stemming from growing compliance expenses, environmental performance expectations, and intensifying adoption of substitute antimicrobial agents. Manufacturers are required to upgrade purification technologies, enhance effluent treatment systems, and conduct comprehensive risk assessments, raising operational costs by an estimated 12–20% depending on production scale. Environmental scrutiny related to TCS persistence and potential ecological accumulation pressures industries to deploy advanced filtration and degradation technologies, further increasing cost burdens. Additionally, formulators in regulated markets increasingly explore alternative antimicrobial compounds, such as chloroxylenol (PCMX) and silver-based additives, which impact long-term demand stability. These challenges collectively create a highly controlled market environment where cost discipline, regulatory adherence, and sustainable chemistry practices become critical to maintaining competitive advantage.

• Increasing Adoption of High-Purity Antimicrobial Grades: High-purity Triclosan (TCS) grades are gaining prominence as manufacturers shift toward formulations with enhanced stability and lower impurity profiles. Demand for high-purity variants has risen by nearly 28% over the past two years, supported by stricter cosmetic and healthcare quality specifications. Advanced purification lines introduced in 2023–2024 reported a 19% reduction in batch variability and a 14% improvement in active-ingredient consistency, enabling more reliable performance in personal care, medical disinfectants, and industrial hygiene applications. This transition is also allowing manufacturers to streamline compliance documentation and enhance formulation performance across premium product categories.

• Expansion of Antimicrobial Polymer and Coating Applications: Industrial and consumer-grade polymers incorporating Triclosan (TCS) have recorded a measurable uptick, with antimicrobial polymer demand increasing by 31% since 2022. Industries leveraging TCS-infused coatings—such as packaging, textiles, and equipment casings—reported up to a 27% reduction in microbial degradation rates. The integration of advanced dispersion technologies has enabled uniform TCS distribution, improving product longevity by 18–22% in high-contact environments. This trend is especially prominent in Asia-Pacific manufacturing hubs, which account for more than 45% of global antimicrobial polymer utilization.

• Regulatory-Driven Reformulation and Precision Dosage Control: Strengthened compliance standards across Europe and North America are accelerating reformulation activities, with nearly 38% of manufacturers modifying product compositions to meet evolving regulatory thresholds. Precision-dosing systems deployed in 2024 demonstrated a 16% reduction in raw material wastage and improved concentration accuracy by 21%, lowering environmental impact while maintaining performance metrics. Automated dosing technologies are also enabling better traceability, reducing formulation inconsistencies by 25% and supporting ESG-aligned production enhancements across multinational hygiene and chemical enterprises.

• Rise in Modular and Prefabricated Construction Influencing Industrial Demand: The shift toward modular and prefabricated construction is reshaping industrial requirements for Triclosan (TCS) in polymer additives, surface treatments, and antimicrobial construction materials. Reports indicate that 55% of new modular projects realized measurable cost advantages through prefabricated components, while automated off-site manufacturing reduced labor needs by 18–25%. Demand for high-precision antimicrobial-enhanced materials has grown by 22% in Europe and 17% in North America as construction ecosystems prioritize durability and hygiene. This trend is reinforcing the use of TCS-enhanced coatings and polymer components in moisture-prone and high-traffic construction applications.

The Triclosan (TCS) Market is segmented across types, applications, and end-users, each contributing distinct value to the overall industry structure. Type-based segmentation reflects the growing preference for high-purity and specialized antimicrobial grades, which support advanced personal care and healthcare formulations. Application-based segmentation highlights strong integration of TCS in hygiene products, disinfectants, industrial polymers, and textile treatments, each driven by measurable performance gains in microbial control. End-user insights reveal that FMCG manufacturers, healthcare institutions, and industrial processors remain the primary consumers, supported by rising hygiene standards and widespread adoption of antimicrobial additives. Collectively, these segments showcase a market shaped by formulation innovation, regulatory alignment, and diversification across both consumer and industrial verticals.

High-purity Triclosan (TCS) currently leads the type segmentation, accounting for approximately 48% of total adoption due to its enhanced stability, reduced impurity levels, and suitability for strict cosmetic and medical-grade formulations. In comparison, standard-grade TCS holds around 32% adoption, primarily serving mass-market personal care products. However, demand for ultra-refined antimicrobial variants is rising fastest, supported by innovation in precision synthesis technologies. This fastest-growing category is expanding at an estimated 7.4% CAGR, driven by increased regulatory scrutiny and the need for consistent quality performance in healthcare and industrial applications. Other TCS types—including modified antimicrobial blends and niche polymer-compatible derivatives—collectively contribute around 20% to the market, primarily serving industrial coatings, engineered materials, and specialty hygiene formulations.

Personal care and hygiene products dominate the Triclosan (TCS) application landscape, representing nearly 46% of total usage due to their widespread use in soaps, deodorants, toothpaste, and sanitizing solutions. In comparison, medical disinfectant applications account for 29%, driven by hospital requirements for high-efficacy antimicrobial compounds. Industrial polymer and coating applications are growing at the fastest pace with an estimated 8.1% CAGR, supported by increasing adoption in packaging materials, textiles, and surface treatments. Other applications—including home care products, institutional cleaners, and specialty plastic additives—collectively make up 25% of the market and continue to benefit from heightened hygiene awareness.

The FMCG sector leads the end-user segmentation for Triclosan (TCS), accounting for roughly 44% of demand owing to extensive usage in mass-manufactured hygiene and personal care products. Healthcare institutions follow with 31% share, driven by stringent infection-control standards and reliance on medical-grade disinfectants. Industrial manufacturers—especially those in polymers, textiles, and packaging—represent the fastest-growing end-user group, expanding at an estimated 7.9% CAGR as factories integrate antimicrobial materials to strengthen product performance and durability. Other end-users, including institutional cleaning service providers and specialty material producers, contribute a combined 25% and display rising adoption aligned with sanitation reforms and material upgrades.

Asia-Pacific accounted for the largest market share at 46% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2025 and 2032.

Asia-Pacific’s strong chemical manufacturing base, high consumption levels in China and India, and expanding hygiene product penetration contributed to its dominant position. Europe followed with a 27% share, supported by strict antimicrobial compliance frameworks. North America held 19%, driven by healthcare and FMCG demand. South America and the Middle East & Africa collectively represented 8%, with rising adoption in institutional cleaning, industrial polymers, and consumer hygiene segments. Growing investments in advanced formulation technologies, alongside heightened regional regulatory alignment, further shaped the distribution of demand for Triclosan (TCS) across global markets.

How is innovation in advanced hygiene formulations redefining demand in this region’s antimicrobial landscape?

North America accounted for approximately 19% of the global Triclosan (TCS) Market in 2024, driven by strong adoption across healthcare institutions, FMCG brands, and industrial disinfectant manufacturers. The region benefits from robust regulatory oversight, including stricter safety and formulation standards that encourage high-purity TCS usage. Key industries such as personal care, pharmaceuticals, and industrial cleaning remain major contributors to demand, supported by digitized manufacturing and automated quality-control systems. Local players, including specialized hygiene product manufacturers in the U.S., have expanded antimicrobial product lines with upgraded formulations that enhance active ingredient stability by 14%. Consumer behavior trends in the region reflect higher adoption of hygiene-centric products, especially among healthcare and enterprise users who prioritize antimicrobial efficacy and compliance-driven product selection.

Why are sustainability-driven formulation standards transforming antimicrobial ingredient demand in this region?

Europe captured nearly 27% of the global Triclosan (TCS) Market in 2024, with Germany, the UK, France, and Italy representing the strongest consumption clusters. The region’s market is shaped significantly by strict regulatory bodies promoting sustainability-focused reformulation efforts, including reduced impurity thresholds and enhanced environmental monitoring. Adoption of precision dosing and smart manufacturing technologies continues to rise, enabling a 13% improvement in formulation accuracy across major production facilities. Key local manufacturers within the EU have invested in antimicrobial testing laboratories that support product performance validation. European consumer behavior leans heavily toward compliance-oriented, transparent, and environmentally responsible hygiene solutions, reinforcing demand for controlled and traceable TCS formulations.

How are expanding manufacturing ecosystems and consumer-driven hygiene needs accelerating antimicrobial integration in this region?

Asia-Pacific dominated the global Triclosan (TCS) Market with a 46% share in 2024, supported by China, India, Japan, and South Korea, which collectively represent the largest production and consumption bases. The region benefits from large-scale chemical manufacturing clusters, advanced processing facilities, and cost-efficient production systems. Manufacturing modernization, including automation and high-purity synthesis upgrades, has strengthened output capacity by 18% since 2022. Local players in China have expanded high-grade antimicrobial production to meet rising demand from personal care and FMCG sectors. Consumer behavior in this region shows strong alignment with hygiene-conscious purchasing, amplified by e-commerce penetration, which now influences more than 38% of hygiene product sales.

How is industrial modernization shaping antimicrobial ingredient adoption across regional markets?

South America accounted for approximately 5% of the global Triclosan (TCS) Market in 2024, led by Brazil and Argentina, where growing consumer awareness and industrial upgrades are pushing demand upward. Regional demand is influenced by infrastructure expansions, strengthening healthcare systems, and increased investment in industrial cleaning solutions. Government support for manufacturing modernization has resulted in an 11% improvement in local production efficiency. Local FMCG producers in Brazil have expanded antimicrobial product lines to meet higher hygiene requirements. Consumer behavior trends indicate rising interest in hygiene-oriented products, particularly those tied to personal care and home cleaning, supported by increasing digital retail adoption.

How are industrial diversification and regulatory harmonization influencing antimicrobial adoption across this region?

The Middle East & Africa held around 3% of the global Triclosan (TCS) Market in 2024, driven by demand from construction, healthcare, and industrial cleaning sectors. Countries such as the UAE, Saudi Arabia, and South Africa are leading adopters, supported by industrial modernization and expansion of hygiene manufacturing facilities. Technological upgrades in regional production units have improved antimicrobial formulation accuracy by 12%. Local regulations focusing on product safety and import quality standards are also shaping market activity. Consumer behavior trends reflect rising hygiene awareness, driven by expanding retail markets and increased use of disinfectant-based personal care products across urban populations.

• China – 31% market share: Driven by large-scale production capacity and extensive demand from FMCG and industrial formulation sectors.

• India – 15% market share: Supported by strong chemical manufacturing infrastructure and rapidly expanding personal care and healthcare product consumption.

The Triclosan (TCS) market exhibits a moderately consolidated structure, with the top five manufacturers collectively holding approximately 48–52% of the global supply in 2024. An estimated 35–40 active commercial producers operate worldwide, with nearly 60% of the production base concentrated across Asia-Pacific due to advanced chemical synthesis infrastructure. Competitive positioning is driven by production capacity, purity levels exceeding 99%, backward integration into phenolic intermediates, and strong compliance with evolving antimicrobial regulatory standards.

Between 2022 and 2024, the market recorded over 25 product reformulations and more than 10 strategic partnerships, including collaborations for controlled-release antimicrobial technologies and enhanced preservation systems. Digital process automation has expanded, with nearly 30% of mid-tier manufacturers adopting monitoring systems that reduce process deviations by 18–20%. Sustainability-aligned innovations are also accelerating, with several producers targeting process waste reduction of 12–18% and developing eco-compliant TCS variants tailored for personal care, textiles, plastics, and medical consumables. Overall, competitive intensity is shaped by operational efficiency, adherence to regional compliance norms, and increasing R&D investment aimed at supporting consistent global supply.

BASF SE

Kumar Organic Products Ltd.

Sino Lion (USA) Ltd.

Shandong Aoyou Biological Technology Co., Ltd.

Vivimed Labs Ltd.

Jiangsu Huanxin High-Tech Materials Co., Ltd.

Zhejiang Xin'an Chemical Group Co., Ltd.

Technological advancements in the Triclosan (TCS) market are reshaping production efficiency, formulation flexibility, and regulatory compliance. One of the most impactful innovations is the adoption of high-purity synthesis technologies capable of consistently achieving ≥99.5% purity, reducing impurity levels by nearly 30% compared to conventional batch processes. Automated continuous-flow reactors are increasingly utilized, offering 22–28% lower energy consumption and improved reaction stability, enabling manufacturers to scale production while meeting stringent regional antimicrobial standards. Advanced microencapsulation technologies are also gaining traction, particularly in personal care, plastics, and coatings. These systems extend Triclosan’s release time by 2–3×, improving antimicrobial durability and reducing the required concentration in end-use formulations by 15–20%. Polymer-bound TCS variants are another emerging innovation, with adoption increasing across medical devices and industrial applications. These technologies allow stronger bonding to substrate surfaces, enhancing leach-resistance by over 40% and improving long-term microbial protection in high-moisture environments.

Digital transformation is playing a significant role in optimizing quality control and production workflows. Approximately 35% of large manufacturers now use digital monitoring platforms to track synthesis parameters in real time, minimizing batch deviations by 18–22%. Predictive maintenance tools integrated within production lines reduce downtime by up to 25%, improving throughput for high-demand sectors such as healthcare, textiles, and polymer processing. Sustainability-oriented technologies are accelerating as well, with new solvent-reduction systems lowering chemical waste by 12–16% and emerging catalytic processes reducing carbon intensity by 10–14%. Collectively, these technology upgrades enable safer, high-performance TCS products aligned with evolving regulatory expectations and industry requirements.

In mid-2023, BASF announced its Sustainable Beauty Days initiative, convening scientific and industry leaders to discuss eco-friendly ingredient innovation, including cleaner antimicrobial systems consistent with corporate sustainability goals.

At the 2023 NY Society of Cosmetic Chemists Suppliers’ Day, BASF’s Care Chemicals division introduced transparent ingredient traceability tools and demonstrated bio-active solutions like probiotic-engineered actives for skin care.

In October 2023, BASF began capacity expansion at its Düsseldorf site for specialty cosmetic ingredients — adding a new reactor and upgrading distillation units to better support high-performance skin care and sun protection formulations.

In the 2023–24 financial year, Vivimed Labs reported successful completion of key regulatory filings for ophthalmic and nasal formulations and advanced its technology transfer discussions for global-scale production of complex specialty APIs.

The Triclosan (TCS) Market Report provides a comprehensive analysis across multiple dimensions including product types, applications, end-users, geographic regions, and technological innovations. The type segmentation covers high-purity grades, standard grades, and specialized derivatives, addressing quality, performance, and regulatory compliance. Applications are mapped to personal care, healthcare disinfectants, industrial coatings, polymer additives, and textile treatment, illustrating the diverse usage of TCS across sectors.

End-user coverage includes FMCG manufacturers, healthcare institutions, and industrial producers, showing patterns of adoption, demand drivers, and formulation requirements. Regionally, the report spans Asia-Pacific, North America, Europe, South America, and Middle East & Africa, outlining production centers, consumption trends, and regulatory landscapes. Technological focus extends to continuous-flow reactors, microencapsulation, polymer-bound TCS, and digital process control, highlighting how innovation is reshaping efficiency, sustainability, and product safety.

The report also addresses regulatory and ESG dimensions, such as traceability solutions, low-impurity grades, and solvent-reduction technologies. It further explores future pathways, including controlled-release systems, low-residue TCS variants, and newer manufacturing platforms. Strategic insights for decision-makers are offered via competitor profiling, including major players’ strategic initiatives, R&D trajectories, and capacity expansions. Emerging or niche segments such as pharmaceutical-grade disinfectants and bio-integrated TCS systems are also analyzed to highlight potential growth zones and innovation levers.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 84.82 Million |

|

Market Revenue in 2032 |

USD 159.35 Million |

|

CAGR (2025 - 2032) |

8.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE , Kumar Organic Products Ltd. , Sino Lion (USA) Ltd. , Shandong Aoyou Biological Technology Co., Ltd., Vivimed Labs Ltd., Jiangsu Huanxin High-Tech Materials Co., Ltd., Zhejiang Xin'an Chemical Group Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |