Reports

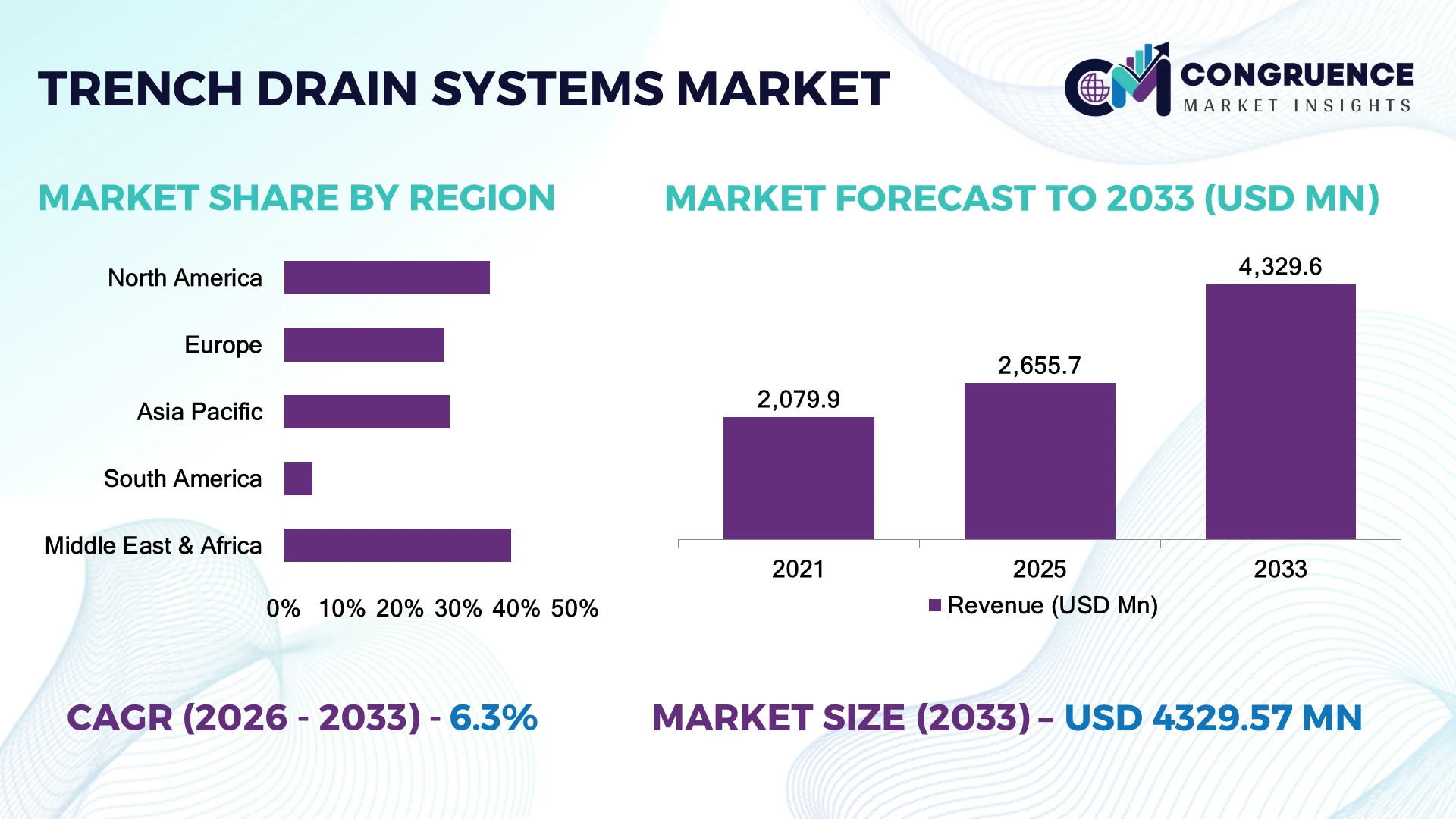

The Global Trench Drain Systems Market was valued at USD 2,655.7 Million in 2025 and is anticipated to reach a value of USD 4,329.6 Million by 2033 expanding at a CAGR of 6.3% between 2026 and 2033. Rapid investments in stormwater infrastructure, industrial facility modernization, airport expansion, and stricter urban drainage regulations are accelerating demand for advanced trench drain systems with higher hydraulic capacity and corrosion resistance.

The United States leads the global market with an estimated 28% share, supported by multi-billion-dollar transportation upgrades, warehouse construction, and municipal stormwater rehabilitation programs. Adoption of polymer concrete and stainless-steel drainage systems exceeds 46% across new commercial developments, compared with Germany's stronger focus on industrial process drainage. Continued infrastructure investment under post-2025 public funding programs reinforces replacement demand while resilient drainage design gains strategic importance amid increasing climate-related flood risks.

Manufacturers prioritizing high-capacity modular drainage solutions, sustainable materials, and rapid-installation systems are positioned to capture long-term infrastructure opportunities.

Market Size & Growth: USD 2,655.7 Million in 2025, reaching USD 4,329.6 Million by 2033 at 6.3% CAGR, driven by resilient infrastructure investments.

Top Growth Drivers: Urban drainage upgrades contribute nearly 34%, industrial expansion 29%, and airport infrastructure projects 18% of demand momentum.

Short-Term Forecast: By 2028, installation time declines 16% through modular trench drain systems and prefabricated channel designs.

Emerging Technologies: Polymer concrete, recycled composites, and digital hydraulic modeling improve drainage efficiency by approximately 20%.

Regional Leaders: North America, Europe, and Asia-Pacific remain dominant with strong transportation, logistics, and municipal infrastructure deployment.

Consumer/End-User Trends: Nearly 58% of commercial construction projects specify corrosion-resistant trench drainage solutions.

Pilot/Case Example: A 2026 logistics park drainage upgrade improved surface water removal efficiency by 27% while reducing maintenance frequency.

Competitive Landscape: Leading manufacturers collectively control roughly 49% market share through engineering capabilities and customized drainage systems.

Regulatory & ESG Impact: Sustainable drainage initiatives reduce runoff impact by approximately 22% in compliant developments.

Investment & Funding: Infrastructure modernization programs continue supporting large-scale transportation and industrial drainage expansion worldwide.

Innovation & Future Outlook: Smart monitoring integration and modular channel systems strengthen lifecycle performance and maintenance efficiency.

The Trench Drain Systems Market is expanding across airports, logistics parks, food processing facilities, manufacturing plants, and urban infrastructure where efficient surface water management is becoming operationally essential. Polymer concrete channels and corrosion-resistant composite materials now account for nearly 42% of new premium installations. Increasing adoption of sustainable urban drainage standards and resilient infrastructure planning is accelerating technology upgrades, setting the stage for broader strategic market transformation.

Modern trench drain systems have become a strategic infrastructure component as governments, industrial operators, and commercial developers prioritize resilient stormwater management, operational safety, and regulatory compliance. Infrastructure modernization and climate adaptation initiatives are shifting procurement toward engineered drainage systems capable of handling higher hydraulic loads while reducing lifecycle maintenance requirements. Manufacturers are increasingly localizing production to improve delivery reliability and respond to evolving construction specifications.

Advanced polymer concrete and composite drainage channels deliver approximately 18% greater hydraulic efficiency while reducing installed weight by nearly 30% compared with conventional cast-in-place concrete systems. North America emphasizes transportation and warehouse infrastructure, whereas Asia-Pacific continues expanding industrial manufacturing parks and smart city developments with higher deployment volumes. Over the next two to three years, modular drainage systems are expected to represent more than 45% of new commercial installations because of faster construction schedules and lower maintenance demands.

Large logistics hubs increasingly deploy prefabricated trench drainage networks that shorten installation periods and simplify future maintenance access. Manufacturers are strengthening competitive positions through engineered product portfolios, regional manufacturing expansion, and integrated design partnerships with infrastructure contractors. Companies combining durable materials, hydraulic optimization, and installation efficiency will establish long-term leadership as resilient infrastructure becomes a core investment priority.

Climate-resilient infrastructure investment and stricter stormwater management regulations are accelerating adoption of advanced trench drain systems across transportation, industrial, and commercial projects. Nearly 61% of new logistics parks now specify modular surface drainage systems, while polymer concrete installations have increased by approximately 34% due to superior durability and hydraulic performance. The United States continues expanding federally supported transportation upgrades, driving demand for engineered drainage solutions with higher load ratings. This structural shift improves flood resilience, lowers lifecycle maintenance costs, and shortens construction schedules. Manufacturers are responding through regional production expansion, engineered modular product portfolios, and partnerships with civil engineering contractors, while integrating high-capacity grating systems for faster installation and greater infrastructure standardization.

Fluctuating prices for stainless steel, ductile iron, and polymer resins continue pressuring trench drain manufacturers and infrastructure contractors. Material procurement costs for premium drainage components have fluctuated by nearly 18%, while imported specialty grating products account for approximately 27% of procurement in several developed construction markets. Supply disruptions affecting metal casting and resin availability complicate production planning and extend project timelines. Higher input costs reduce bidding competitiveness and compress contractor margins, particularly on public infrastructure projects with fixed-price contracts. Companies are mitigating these pressures through localized sourcing strategies, long-term procurement agreements, recycled material integration, and expanded composite product offerings that reduce dependence on volatile raw material supply chains.

Digital infrastructure is creating new opportunities for intelligent trench drain systems equipped with embedded monitoring technologies and predictive maintenance capabilities. Approximately 36% of large smart-city drainage projects are evaluating sensor-enabled water flow monitoring, while remote asset management can reduce maintenance inspections by nearly 25%. Japan and Singapore continue incorporating digital stormwater infrastructure into urban resilience programs, encouraging manufacturers to develop connected drainage platforms. Beyond flood prevention, operational analytics improve municipal maintenance planning and reduce emergency repair costs. Companies are increasing investment in IoT-enabled channel systems, digital twins, and integrated monitoring partnerships, positioning trench drainage as a long-term infrastructure management solution rather than a passive construction component.

Retrofitting trench drain systems into aging transportation corridors, industrial facilities, and urban streets remains a significant execution challenge. Nearly 32% of drainage rehabilitation projects require customized channel dimensions, while project timelines can extend by approximately 20% because of underground utility conflicts and site-specific engineering constraints. Older municipal infrastructure in Germany and the United Kingdom frequently requires phased installation to maintain operational continuity. These complexities increase engineering costs, reduce deployment consistency, and complicate long-term asset management. Manufacturers must strengthen BIM integration, prefabricated modular designs, engineering support services, and contractor training programs to improve installation precision while ensuring compatibility with evolving infrastructure standards and sustainable drainage requirements.

Modular Installation Expansion Modular trench drain systems now represent nearly 48% of new commercial installations, reducing installation time by approximately 22% and labor requirements by 18%. Accelerated warehouse construction and labor shortages are encouraging manufacturers to expand prefabricated product lines while strengthening partnerships with infrastructure contractors for faster project execution.

Composite Material Adoption Polymer concrete and fiber-reinforced composite drainage channels account for nearly 41% of premium project specifications because they reduce structural weight by approximately 30% while improving corrosion resistance. Infrastructure owners increasingly prioritize lifecycle performance, prompting manufacturers to restructure production around advanced material technologies and sustainable product portfolios.

Higher Hydraulic Capacity Designs Airport expansions, logistics hubs, and industrial manufacturing plants increasingly require drainage systems with 25% greater hydraulic capacity to manage intense rainfall events. Updated stormwater engineering standards are driving larger channel profiles, while manufacturers are introducing optimized grate geometries and computational hydraulic design tools to improve operational efficiency.

Digital Asset Management Integration Smart drainage infrastructure incorporating flow sensors and predictive maintenance platforms has grown by nearly 19% across municipal pilot projects. Utilities are adopting digital inspection workflows to reduce maintenance costs and improve response times, leading manufacturers to integrate monitoring technologies, cloud-based maintenance platforms, and automation capabilities into premium trench drainage systems.

Polymer concrete trench drain systems account for approximately 42% of the market, making them the dominant segment because of their exceptional compressive strength, corrosion resistance, low water absorption, and long service life under heavy traffic conditions. Airports, logistics parks, highways, and industrial facilities increasingly specify polymer concrete channels to minimize maintenance costs and improve hydraulic performance. Municipal infrastructure projects also favor this material because modular channel systems reduce installation time by nearly 20% while supporting standardized construction practices. Stainless steel systems continue serving hygiene-sensitive environments, while conventional concrete remains relevant for budget-driven public works. Manufacturers are expanding polymer concrete production capacity and introducing engineered modular solutions to strengthen long-term infrastructure partnerships.

Composite trench drain systems represent the fastest-growing segment as contractors prioritize lightweight materials that simplify handling and reduce installation costs. Composite channels are nearly 30% lighter than conventional concrete alternatives while maintaining high chemical resistance in industrial environments. HDPE and fiberglass systems continue gaining traction across landscape drainage and utility projects where corrosion resistance and installation flexibility are critical. Companies are investing in advanced composite formulations, localized manufacturing, and modular product portfolios to improve project efficiency and expand specification opportunities across commercial infrastructure.

Industry observations released during 2025 by leading civil engineering associations indicate that modular polymer concrete drainage systems are increasingly specified for high-load transportation and logistics infrastructure because of superior lifecycle durability and reduced maintenance requirements.

Transportation infrastructure represents the largest application, accounting for approximately 36% of global demand. Airports, highways, ports, and railway facilities require high-capacity trench drainage systems capable of managing heavy axle loads and increasing stormwater volumes. Long operational lifecycles, stringent engineering standards, and continuous infrastructure upgrades reinforce sustained demand across this segment. Commercial buildings remain a significant application through retail complexes, office developments, and parking structures, while municipal stormwater projects continue replacing aging drainage networks. Manufacturers are strengthening engineering support, customized hydraulic designs, and modular installation systems to meet increasingly complex infrastructure specifications.

Industrial facilities are the fastest-growing application as manufacturing expansion, warehouse construction, and distribution center investments accelerate globally. Industrial installations have increased by nearly 26% across newly developed logistics facilities, while corrosion-resistant trench drainage solutions account for approximately 44% of new food and beverage processing projects. Residential developments continue supporting steady demand for compact drainage systems, particularly in premium housing and urban redevelopment. Companies are expanding automated manufacturing capacity, integrated drainage portfolios, and contractor partnerships to support evolving industrial and commercial construction requirements.

Enterprise surveys conducted during 2026 across commercial construction firms indicate that high-capacity modular drainage systems are increasingly selected to accelerate installation while lowering long-term maintenance requirements for transportation and industrial developments.

Municipal authorities account for approximately 39% of global trench drain system demand, supported by extensive investments in urban stormwater management, road rehabilitation, flood mitigation, and public infrastructure modernization. Their large procurement volumes, long asset lifecycles, and regulatory compliance requirements make municipalities the dominant buyer group. Industrial enterprises continue representing a substantial share because manufacturing plants require durable drainage systems for operational safety and wastewater control. Commercial developers remain important purchasers for logistics parks, airports, retail developments, and mixed-use construction. Manufacturers increasingly provide customized hydraulic designs, long-term maintenance support, and modular installation solutions to strengthen public-sector relationships.

Industrial enterprises are the fastest-growing end-user segment as warehouse automation, advanced manufacturing, and distribution infrastructure expand globally. Industrial demand has increased by nearly 24%, while modular drainage adoption exceeds 47% across newly developed logistics facilities requiring rapid construction schedules. Transportation authorities continue upgrading airport and highway drainage networks, whereas institutional buyers such as universities and healthcare campuses increasingly specify corrosion-resistant systems. Companies are strengthening engineering partnerships, value-added installation services, and localized production capabilities to address evolving procurement requirements and improve competitive positioning.

According to infrastructure procurement findings published during 2025 by leading public works organizations, municipal stormwater upgrades and transportation rehabilitation projects remain the largest procurement channel for engineered trench drainage systems, with lifecycle durability becoming a primary purchasing criterion.

North America accounted for the largest market share at 35.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

Infrastructure Renewal and High-Performance Drainage Deployment

North America maintains its leadership through sustained investments in transportation infrastructure, logistics facilities, industrial manufacturing, and municipal stormwater modernization. Large-scale highway rehabilitation, airport upgrades, and warehouse construction continue driving demand for polymer concrete and modular trench drainage systems capable of supporting heavy traffic loads and extreme weather conditions. Approximately 52% of premium commercial projects specify corrosion-resistant drainage materials, while modular installations reduce project timelines by nearly 18%. Engineering firms increasingly integrate hydraulic modeling into drainage design, improving lifecycle performance. Manufacturers are expanding regional production capacity and collaborating with infrastructure contractors to deliver customized systems aligned with evolving public infrastructure standards.

United States Market Outlook: The United States represents the largest national market owing to continuous transportation upgrades, expanding logistics corridors, and municipal flood mitigation initiatives. More than 46% of new commercial infrastructure projects specify modular trench drainage solutions to improve installation efficiency and long-term maintenance performance. Strong investment across airports, distribution centers, manufacturing facilities, and public infrastructure supports sustained procurement, while manufacturers continue strengthening domestic production and engineering partnerships to improve project execution and supply reliability.

Sustainable Urban Drainage Shapes Infrastructure Modernization

Europe remains a mature market supported by stringent stormwater regulations, sustainable urban drainage initiatives, and extensive rehabilitation of aging public infrastructure. Industrial modernization and transportation upgrades continue driving replacement demand for corrosion-resistant drainage systems with longer operational lifecycles. Approximately 43% of municipal drainage projects now prioritize modular systems that simplify installation and maintenance. Manufacturers continue introducing recycled composite materials and advanced polymer concrete technologies while strengthening engineering collaboration with infrastructure developers to meet increasingly demanding environmental performance requirements.

Germany Market Outlook: Germany leads the regional market through its advanced civil engineering sector, industrial manufacturing base, and continuous transportation infrastructure investment. Industrial facilities increasingly specify chemically resistant trench drainage systems to improve operational safety, while nearly 48% of large logistics developments incorporate modular drainage designs for accelerated construction schedules. Domestic manufacturers continue investing in material innovation and automated production to strengthen competitiveness across infrastructure and industrial applications.

Manufacturing Expansion Accelerates Infrastructure Deployment

Asia-Pacific is the fastest-growing regional market as rapid urbanization, industrial expansion, airport development, and smart city programs increase demand for engineered drainage infrastructure. China, India, and Southeast Asian economies continue investing heavily in logistics parks, manufacturing zones, and transportation corridors requiring high-capacity drainage systems. Nearly 58% of newly developed industrial parks specify modular drainage products to improve installation efficiency, while production of polymer concrete channels continues expanding to support domestic infrastructure demand. Manufacturers are increasing localized manufacturing, automation, and regional distribution capabilities to serve rapidly growing construction activity.

China Market Outlook: China dominates regional demand through extensive industrial development, transportation expansion, and large-scale municipal infrastructure projects. More than 50% of newly commissioned logistics and manufacturing facilities incorporate engineered trench drainage systems designed for heavy-duty operational environments. Domestic manufacturers continue expanding production capacity, improving material technology, and strengthening project partnerships to support infrastructure modernization while reducing dependence on imported drainage components.

Industrial Construction Supports Emerging Demand

South America is witnessing steady market expansion through investments in mining operations, logistics infrastructure, food processing facilities, and urban drainage modernization. Infrastructure replacement remains gradual because of budget limitations, yet industrial developments increasingly specify corrosion-resistant trench drainage systems capable of operating under demanding environmental conditions. Approximately 31% of new industrial construction projects now incorporate modular drainage solutions to improve installation speed and reduce maintenance requirements. Manufacturers continue strengthening distributor networks and localized inventory management to improve product availability across expanding infrastructure markets.

Brazil Market Outlook: Brazil remains the largest regional market due to its extensive industrial base, transportation infrastructure investments, and growing logistics sector. Food processing plants, manufacturing facilities, and commercial developments increasingly deploy polymer concrete drainage systems to improve operational reliability. Nearly 38% of new logistics projects include engineered trench drainage networks, encouraging suppliers to expand regional partnerships and customized product offerings for infrastructure contractors.

Mega Infrastructure Projects Strengthen Market Potential

The Middle East & Africa market is expanding through airport construction, industrial diversification, commercial real estate development, and large-scale urban infrastructure investments. Governments continue prioritizing resilient drainage systems capable of supporting high-capacity transportation facilities and rapidly growing metropolitan areas. Approximately 35% of major infrastructure developments now specify modular trench drainage products that accelerate construction and improve long-term maintenance efficiency. Manufacturers are expanding regional partnerships, engineering support, and project-specific product customization to capitalize on increasing infrastructure investment.

Saudi Arabia Market Outlook: Saudi Arabia leads regional demand through large-scale urban development, industrial diversification, and transportation infrastructure expansion. Mega projects increasingly incorporate engineered trench drainage systems to improve stormwater management and infrastructure resilience. Nearly 42% of newly awarded commercial infrastructure packages specify high-capacity modular drainage solutions, encouraging manufacturers to establish stronger regional distribution, technical support, and localized project engineering capabilities.

The market is led by global drainage specialists including ACO Group, HAURATON, MEA Group, and Zurn Elkay, competing against regional precast concrete manufacturers and cost-focused local suppliers. The top five companies collectively account for approximately 49% of global market share, with competition centered on hydraulic performance, material durability, installation speed, and engineering support rather than price alone. Premium manufacturers achieve nearly 20% faster installation through modular systems and deliver up to 30% lower lifecycle maintenance than conventional cast-in-place alternatives. Companies are expanding polymer concrete production, strengthening contractor partnerships, and vertically integrating grate, channel, and stormwater solutions to secure specification-driven projects. Competitive momentum is shifting toward intelligent drainage design, sustainable materials, and integrated water management portfolios, raising technical entry barriers for commodity suppliers. Success increasingly depends on engineering expertise, certified product performance, resilient supply chains, customized project support, and rapid delivery across major infrastructure developments.

ACO Group

HAURATON GmbH & Co. KG

MEA Group

Zurn Elkay Water Solutions

NDS, Inc.

ULMA Architectural Solutions

Wade Drains

MIFAB, Inc.

Josam Company

Watts Water Technologies

Kent Stainless

Hubbell Drainage Systems

Polymer concrete continues replacing conventional reinforced concrete because it provides approximately 18% higher hydraulic efficiency while reducing structural weight by nearly 30%. Nearly 48% of premium infrastructure projects now specify modular drainage systems that accelerate installation and improve long-term maintenance access. Advanced finite element engineering and computational hydraulic modeling optimize channel geometry, delivering greater flow capacity and enhanced structural durability under heavy traffic conditions. Manufacturers adopting automated casting and precision molding achieve stronger dimensional consistency and shorter production cycles, strengthening competitiveness in transportation and industrial infrastructure projects.

Emerging technologies focus on embedded IoT sensors, predictive maintenance platforms, and digital stormwater monitoring. Smart drainage solutions can reduce inspection frequency by approximately 25%, while remote flow monitoring improves maintenance planning across airports, logistics parks, and municipal infrastructure. Compared with conventional passive drainage systems, digitally monitored installations improve maintenance efficiency by nearly 22%. Infrastructure operators and municipalities benefit most because predictive maintenance minimizes emergency repairs and extends asset life while improving operational resilience.

Between 2026 and 2028, digital asset management, recycled composite materials, and prefabricated modular systems will reshape procurement priorities. Manufacturers investing in connected infrastructure, advanced material science, and integrated stormwater solutions will strengthen specification rates across transportation, industrial, and smart city developments. Companies that combine engineering support, digital monitoring, and sustainable product innovation will secure long-term competitive advantages as resilient infrastructure spending continues accelerating.

June 2025 – Zurn Elkay Water Solutions launched its 6-inch Ductile Iron Frame Trench Drain System featuring DIN F load-rated grates and an optimized radiused channel design that improves flow performance while reducing sediment buildup. The launch strengthens heavy-duty transportation infrastructure offerings. Source: zurn.com

March 2024 – ACO Drain expanded its sustainability focus by promoting eco-friendly drainage solutions and resilient stormwater management practices supporting climate-adaptive infrastructure projects. The initiative reinforces growing adoption of polymer concrete drainage technologies across commercial developments. Source: acodrain.com.au

December 2025 – ACO Drain highlighted safer pavement design initiatives supporting walkable urban infrastructure and advanced surface drainage integration for public environments. The program strengthens demand for engineered trench drainage solutions within municipal redevelopment projects. Source: ACO Drain News

2026 – Infrastructure developers increasingly integrated AI-assisted drainage inspection and predictive maintenance technologies into stormwater asset management, improving defect detection accuracy while reducing inspection workloads for large municipal drainage networks. Source: Institutional research publication.

This report provides comprehensive analysis of the global Trench Drain Systems Market across material types, applications, end-user industries, and major regional markets. The assessment covers polymer concrete, composite, stainless steel, concrete, and related drainage technologies deployed across transportation infrastructure, industrial facilities, commercial buildings, municipal projects, and residential developments. Regional evaluation examines deployment patterns, procurement priorities, material adoption, and infrastructure modernization trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The study evaluates technology adoption, competitive positioning, engineering innovation, modular installation trends, and evolving stormwater management requirements. It incorporates operational indicators including approximate segment shares, deployment concentrations, modular system penetration, and manufacturer participation across key infrastructure projects. The report supports investment planning, product development, regional expansion, competitive benchmarking, and strategic decision-making while identifying emerging opportunities expected to influence the market between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2,655.7 Million |

|

Market Revenue in 2033 |

USD 4,329.6 Million |

|

CAGR (2026 - 2033) |

6.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ACO Group, HAURATON GmbH & Co. KG, MEA Group, Zurn Elkay Water Solutions, NDS, Inc., ULMA Architectural Solutions, Wade Drains, MIFAB, Inc., Josam Company, Watts Water Technologies, Kent Stainless, Hubbell Drainage Systems |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |