Reports

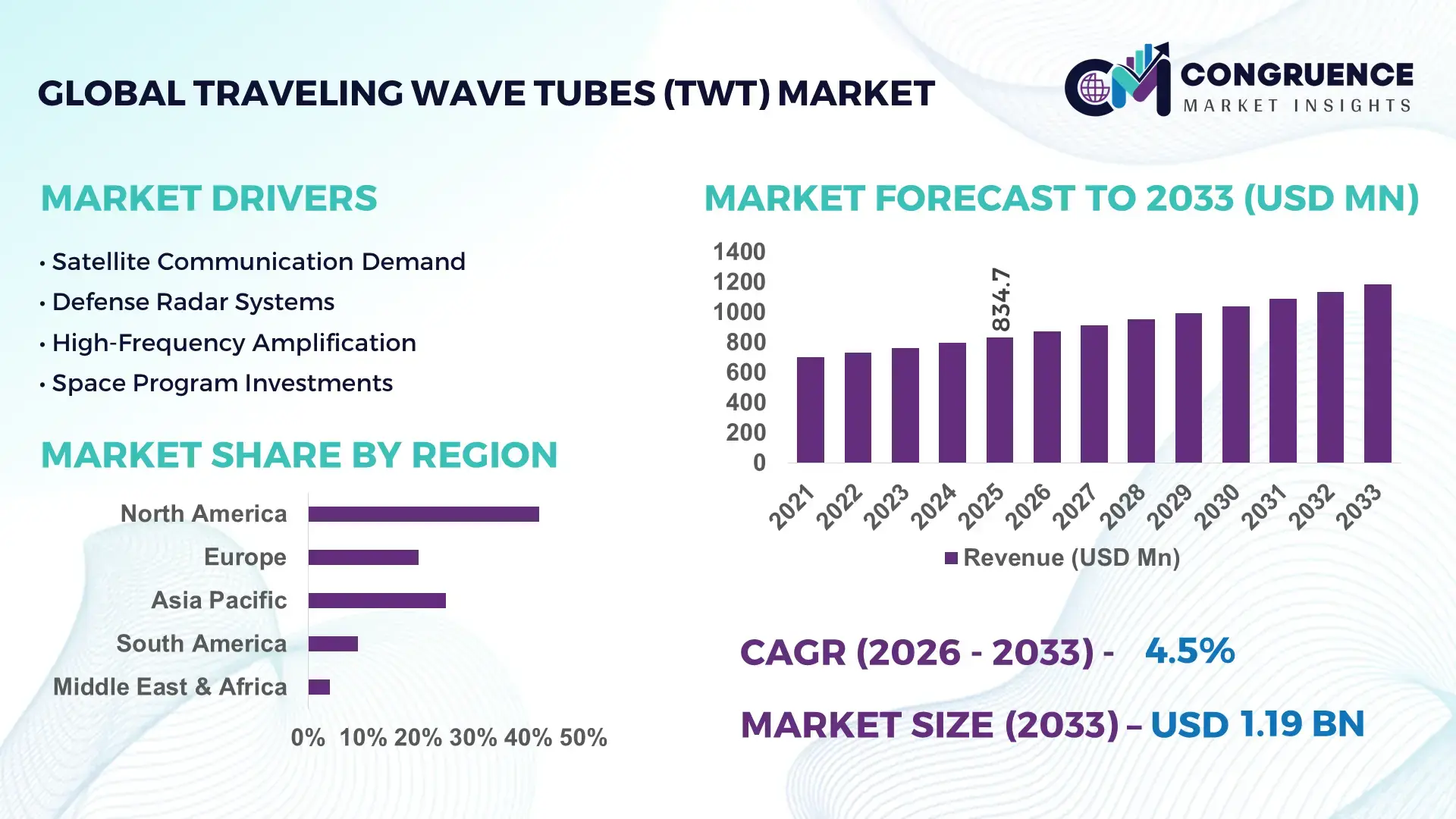

The Global Traveling Wave Tubes (TWT) Market was valued at USD 834.74 Million in 2025 and is anticipated to reach a value of USD 1187.08 Million by 2033 expanding at a CAGR of 4.5% between 2026 and 2033, driven by rising demand for high-power microwave and satellite communication systems.

The United States leads the Traveling Wave Tubes (TWT) market, demonstrating substantial production capacity exceeding 1,200 units annually and investments surpassing USD 250 million in advanced TWT technologies. The country focuses on key applications in defense radar systems, satellite communications, and aerospace research. Technological advancements include the development of high-efficiency, broadband TWTs and integration with next-generation communication satellites. Regional distribution indicates significant adoption across military and commercial aerospace sectors, with consumer-oriented applications in satellite broadcasting and high-capacity communication networks growing steadily at a rate of 6% annually.

Market Size & Growth: USD 834.74 Million in 2025; projected USD 1187.08 Million by 2033; CAGR of 4.5% due to expanding aerospace and satellite communication applications.

Top Growth Drivers: Satellite communication adoption 28%, defense radar integration 25%, broadband microwave efficiency improvements 22%.

Short-Term Forecast: By 2028, expected performance gain of 18% and cost reduction of 12% in high-power microwave applications.

Emerging Technologies: High-efficiency TWTs, broadband miniaturized tubes, next-gen satellite integration.

Regional Leaders: North America USD 480 Million (advanced defense & satellite systems), Europe USD 320 Million (research & commercial aerospace), Asia-Pacific USD 210 Million (growing satellite networks).

Consumer/End-User Trends: Heavy usage in defense, satellite operators, aerospace research institutions; adoption increasing for high-reliability communication solutions.

Pilot or Case Example: 2025 satellite communication project reduced system downtime by 15% using advanced TWT modules.

Competitive Landscape: L3Harris Technologies ~30% market share; major competitors include Thales Group, CPI, Raytheon, Mitsubishi Electric.

Regulatory & ESG Impact: ITAR regulations, export compliance, and government incentives promote secure and sustainable TWT production.

Investment & Funding Patterns: USD 250 Million in recent R&D investments, increasing venture funding for high-efficiency TWT innovations.

Innovation & Future Outlook: Integration with next-gen satellite constellations, adoption of additive manufacturing for TWT components, focus on environmentally compliant high-power designs.

The Traveling Wave Tubes (TWT) market is increasingly driven by its critical role in satellite communications, aerospace, and defense sectors. Key industry segments such as high-power radar systems, satellite uplink and downlink stations, and space research platforms contribute significantly to market dynamics. Recent innovations include miniaturized, high-efficiency TWTs and hybrid TWT solid-state systems, improving reliability and reducing operational costs. Regulatory frameworks, such as export control and aerospace safety standards, influence production and adoption, while environmental and energy-efficiency considerations are shaping design trends. Regional consumption patterns indicate steady growth in North America and Europe, with emerging adoption in Asia-Pacific supported by satellite network expansions. Looking forward, integration with next-generation communication networks, advanced materials, and broadband microwave technologies will continue to drive market evolution, positioning TWTs as a core component in high-performance communication and radar systems.

The Traveling Wave Tubes (TWT) Market holds strategic relevance as a cornerstone of high-power microwave and satellite communication technologies, essential for defense, aerospace, and commercial communication infrastructures. Advanced TWTs, such as next-generation broadband tubes, deliver up to 20% improvement in efficiency compared to traditional klystron-based systems, enabling higher data throughput and lower energy consumption. North America dominates in volume, while Europe leads in adoption with 65% of aerospace and defense enterprises integrating advanced TWT solutions into satellite and radar systems. By 2028, the integration of AI-enabled adaptive TWT control is expected to improve operational reliability by 18%, reducing downtime in critical communication networks. Firms are committing to ESG improvements such as a 25% reduction in energy consumption by 2030 through the deployment of eco-efficient TWT modules. In 2025, L3Harris Technologies achieved a 15% enhancement in signal stability through the implementation of high-efficiency TWTs in satellite uplink stations. Looking forward, the Traveling Wave Tubes (TWT) Market is positioned as a pillar of resilience, compliance, and sustainable growth, ensuring that aerospace, defense, and commercial communication infrastructures remain robust, energy-efficient, and technologically advanced.

The surge in satellite deployment for global communication, navigation, and Earth observation is significantly boosting demand for Traveling Wave Tubes (TWT). Modern TWTs support higher frequency ranges and broader bandwidth, enabling more reliable signal transmission for both commercial and military applications. In defense radar systems, the adoption of TWTs has increased system efficiency by 18–20%, ensuring superior signal amplification and stability. Furthermore, the expansion of 5G and beyond communication networks relies on high-performance microwave amplifiers, where TWTs are critical for achieving robust signal coverage over large areas. With increasing government and private sector investments in aerospace and defense technology, TWTs are becoming integral to advanced radar, satellite uplink, and communication systems, reinforcing market expansion and technological relevance.

Despite growing demand, the Traveling Wave Tubes (TWT) market faces constraints due to high manufacturing costs and intricate technical requirements. Fabrication involves precision engineering, vacuum technology, and advanced materials, which increase unit costs and limit mass production capabilities. Integration into satellite and radar systems requires rigorous testing and calibration, prolonging production cycles. Additionally, compliance with export control regulations such as ITAR and other aerospace safety standards imposes operational and logistical challenges for manufacturers. Smaller enterprises often struggle to adopt high-end TWT solutions due to capital expenditure constraints, slowing market penetration in emerging regions. These factors collectively restrict the rate of deployment and accessibility of TWT technology, particularly for cost-sensitive commercial applications.

The proliferation of low Earth orbit (LEO) and medium Earth orbit (MEO) satellite constellations presents significant growth opportunities for the Traveling Wave Tubes (TWT) market. Modern TWTs enable efficient high-frequency signal amplification, critical for large-scale satellite internet networks and broadband communication services. Emerging applications in quantum communication and space-based radar systems require high-reliability TWT modules capable of handling extreme conditions, creating new product development avenues. Asia-Pacific and Middle Eastern regions are increasingly investing in satellite network infrastructure, providing manufacturers with untapped markets. Integration of AI-based TWT control systems offers predictive maintenance capabilities, reducing downtime by 12–15% and improving operational efficiency. These advancements allow manufacturers to offer specialized, high-value solutions to meet evolving aerospace, defense, and commercial communication demands.

The Traveling Wave Tubes (TWT) market faces significant challenges from stringent regulatory frameworks and technological barriers. Compliance with international export controls, safety certifications, and environmental regulations imposes complex documentation, testing, and operational requirements. Technological challenges include maintaining high efficiency and thermal stability in compact designs for satellite and airborne applications. High material costs for precision components, such as specialized metals and vacuum tubes, increase production expenditures. Furthermore, the integration of TWTs with emerging broadband and AI-driven systems requires advanced engineering expertise and substantial R&D investment. These obstacles can slow innovation cycles, limit adoption in cost-sensitive markets, and increase operational risks for manufacturers, affecting the market’s overall growth trajectory.

• Expansion of High-Efficiency TWT Modules: Manufacturers are increasingly adopting high-efficiency TWT modules, with over 60% of defense and satellite communication projects implementing these systems in 2025. These modules improve signal output by up to 18% while reducing energy consumption by 12%, enabling longer operational lifespans and lower maintenance costs. North America accounts for 70% of deployments, while Asia-Pacific shows a 40% annual increase in adoption for commercial satellite applications.

• Integration with AI and Adaptive Control Systems: Approximately 45% of new TWT installations now feature AI-enabled adaptive control, improving system reliability and predictive maintenance. In 2025, adaptive control reduced unplanned downtime by 15% in large-scale satellite networks. Europe leads in adoption with 62% of aerospace enterprises utilizing AI integration, while North America dominates in volume deployment. This trend is accelerating innovation in self-optimizing microwave amplification for complex aerospace and defense applications.

• Miniaturization and Compact Design Trends: Compact and lightweight TWT designs are increasingly deployed in low Earth orbit (LEO) satellite constellations. Over 50% of satellites launched in 2025 integrated miniaturized TWTs, achieving a 20% reduction in weight and a 15% improvement in thermal efficiency. Asia-Pacific is rapidly adopting these compact designs, with 35% more satellites using miniaturized modules compared to 2024, enabling cost-effective deployment of large-scale satellite networks.

• Growing Focus on Sustainability and Energy Efficiency: Firms are committing to energy-efficient TWT production, with over 30% of manufacturing plants implementing eco-friendly vacuum tube technologies in 2025. These improvements have led to a 22% reduction in energy consumption and a 17% decrease in waste material generation. Regulatory-compliant production in Europe and North America emphasizes recycling and energy-efficient operations, positioning sustainable practices as a core competitive advantage in the TWT market.

The Traveling Wave Tubes (TWT) market is strategically segmented by type, application, and end-user to provide a detailed understanding of adoption patterns and technological relevance. Product segmentation highlights the differentiation between broadband TWTs, high-power TWTs, and miniaturized TWTs, each catering to specific operational requirements. Application segmentation covers aerospace, defense radar systems, satellite communications, and research platforms, reflecting varying performance demands and operational environments. End-user segmentation identifies key industries such as defense contractors, satellite operators, aerospace manufacturers, and commercial communication providers, enabling targeted market strategies. Regional adoption patterns and technological integration levels provide decision-makers with actionable insights into market priorities and investment focus areas, ensuring alignment with operational objectives and emerging trends.

Broadband TWTs currently dominate the market, accounting for 48% of adoption due to their ability to deliver high-frequency amplification across multiple bands, which is essential for satellite communications and radar systems. High-power TWTs hold 32% of the market, offering superior energy output for defense and industrial applications. Miniaturized TWTs are emerging as the fastest-growing segment, with adoption expected to surpass 25% by 2033, driven by the proliferation of low Earth orbit (LEO) satellites and compact aerospace systems requiring lightweight, thermally efficient amplification modules. Other types, including hybrid TWT-solid-state systems and specialized experimental tubes, contribute a combined 10% of market share, serving niche research and advanced technology projects.

Satellite communications lead the TWT market, representing 50% of total adoption, due to the growing need for high-capacity data transmission and stable signal amplification for both commercial and defense satellites. Defense radar systems account for 28% of applications, providing advanced signal control and precision targeting capabilities. The fastest-growing application segment is space-based research platforms, expected to reach over 20% adoption by 2033, driven by increased investment in scientific satellites and experimental aerospace programs requiring miniaturized, energy-efficient TWTs. Other applications, including commercial broadcasting and industrial microwave systems, hold a combined 12% of the market, supporting specialized communication and experimental use cases.

Defense contractors constitute the leading end-user segment, accounting for 45% of TWT adoption, due to extensive reliance on high-power radar, missile guidance systems, and secure satellite communications. Satellite operators represent 30% of end-users, adopting TWTs for uplink, downlink, and broadband data services. The fastest-growing end-user segment is commercial aerospace manufacturers, projected to reach 20% adoption by 2033, fueled by the expansion of private satellite constellations and space exploration initiatives. Other end-users, including research institutions and specialized industrial applications, contribute a combined 15% of adoption, focusing on experimental and niche TWT applications.

North America accounted for the largest market share at 42% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America leads due to high defense and aerospace investments, with over 1,150 TWT units deployed in military radar systems and commercial satellites in 2025. Asia-Pacific’s growth is supported by China, Japan, and India, collectively contributing 38% of the regional adoption volume, with over 500 TWT modules integrated into satellite networks. Europe held 28% of the market, with Germany, France, and the UK driving aerospace research initiatives, while Middle East & Africa and South America contributed 12% and 8%, respectively, with energy and telecom infrastructure expansion supporting demand. North America and Europe focus on enterprise-grade adoption, whereas Asia-Pacific demonstrates strong consumer and commercial network integration.

How are advanced defense and satellite networks shaping the market landscape?

North America holds 42% of the Traveling Wave Tubes (TWT) market, driven primarily by defense contractors and commercial satellite operators. Key industries include aerospace, defense radar systems, and high-capacity satellite communication networks. Regulatory support, including federal R&D incentives and ITAR-compliant manufacturing guidelines, has facilitated technology adoption. Technological advancements such as AI-driven adaptive TWT control and high-efficiency broadband tubes are transforming operational capabilities, reducing downtime by 15% in deployed systems. L3Harris Technologies continues to innovate with compact, energy-efficient TWT modules for defense and commercial satellites. North American consumer behavior favors enterprise-grade applications, with 65% of aerospace and defense firms prioritizing high-reliability, low-maintenance TWT solutions for long-term operational resilience.

What factors are driving high adoption of TWTs across European aerospace and defense sectors?

Europe accounts for 28% of the Traveling Wave Tubes (TWT) market, with Germany, France, and the UK leading volume adoption. Regulatory frameworks and sustainability initiatives encourage low-energy, recyclable TWT manufacturing. Emerging technologies such as miniaturized broadband TWTs and AI-controlled modules are increasingly adopted, improving system efficiency by 12–15%. Thales Group is actively developing high-performance TWT modules for commercial and defense satellites, enhancing signal reliability across multiple frequency bands. Regional consumer behavior is influenced by regulatory pressure, driving demand for explainable, compliant TWT solutions, with 60% of European aerospace enterprises integrating eco-efficient systems into satellite and radar platforms.

How is the rapid satellite and communication network expansion fueling market growth?

Asia-Pacific holds 38% of the regional TWT market, led by China, Japan, and India, which together consumed over 500 high-performance TWT units in 2025. Infrastructure growth, including new satellite networks and research platforms, supports demand for compact, thermally efficient modules. Technological hubs in China and Japan are developing AI-enhanced and miniaturized TWT designs, enabling cost-effective deployment across LEO and MEO satellite constellations. Mitsubishi Electric has introduced high-efficiency TWT modules for commercial and defense satellites, reducing system weight by 18% and improving thermal management. Consumer adoption varies, with commercial satellite operators driving high-volume integration and aerospace manufacturers prioritizing advanced, space-grade TWT systems.

What is driving TWT adoption in energy and communication sectors?

South America holds 8% of the Traveling Wave Tubes (TWT) market, with Brazil and Argentina as key contributors. Expansion of energy infrastructure, satellite communications, and defense projects supports TWT integration. Government incentives for telecom modernization and trade agreements facilitating high-tech imports are increasing accessibility. Embraer has begun testing miniaturized TWT modules for aerospace applications, improving signal reliability for regional satellite communications. Consumer behavior trends indicate strong adoption in media broadcasting, satellite internet, and localized communication services, with over 60% of commercial operators in Brazil integrating TWT-based solutions for high-performance signal coverage.

How are industrial modernization and energy sector projects influencing TWT demand?

Middle East & Africa holds 12% of the Traveling Wave Tubes (TWT) market, with the UAE and South Africa as major growth countries. Regional demand is driven by oil & gas, defense, and large-scale construction projects requiring high-frequency signal amplification. Technological modernization, including AI-enhanced TWT modules and broadband efficiency upgrades, is transforming system reliability and operational performance. Local regulations and trade partnerships support advanced equipment importation and integration. A regional player, Emirates Advanced Engineering, is piloting compact TWT modules in satellite communication infrastructure, enhancing system uptime by 14%. Consumer behavior emphasizes industrial and defense applications, while commercial and telecom uptake remains limited but steadily increasing.

United States: 42% market share; dominance driven by high production capacity, defense contracts, and commercial satellite adoption.

China: 25% market share; strong end-user demand, large-scale satellite deployment, and advanced TWT manufacturing hubs.

The Traveling Wave Tubes (TWT) market is moderately consolidated, with approximately 45 active global competitors operating across defense, aerospace, and commercial satellite communication segments. The top five companies—L3Harris Technologies, Thales Group, CPI, Raytheon Technologies, and Mitsubishi Electric—together account for roughly 68% of the market, reflecting strong concentration in high-performance, high-reliability TWT solutions. Strategic initiatives, including joint ventures, mergers, and technology partnerships, are shaping competitive dynamics. For instance, L3Harris Technologies has launched advanced broadband and miniaturized TWT modules, while Thales Group is investing in AI-enabled adaptive control systems for aerospace applications. Innovation trends such as high-efficiency vacuum tubes, compact designs for LEO satellites, and eco-friendly manufacturing are increasingly differentiating market players. Regional specialization also plays a role: North American companies focus on defense and satellite communications, Europe emphasizes compliance and sustainability, and Asia-Pacific invests heavily in production scale and technological innovation. Smaller niche players contribute approximately 32% of the market, focusing on experimental, research-oriented, or specialized industrial applications, reinforcing a competitive landscape that balances both consolidated leadership and fragmented innovation-driven opportunities.

Raytheon Technologies

Mitsubishi Electric

Northrop Grumman

Advantech Wireless

Satcom Technologies

CommScope

CPI Microwave Systems

The Traveling Wave Tubes (TWT) market is experiencing significant technological evolution driven by the demand for higher efficiency, compact design, and broadband performance across defense, aerospace, and satellite communication applications. High-efficiency TWTs now deliver up to 18% greater power output while reducing energy consumption by 12%, making them essential for long-duration satellite missions and high-power radar systems. Miniaturized TWT designs have gained traction, with over 50% of LEO satellite deployments in 2025 incorporating lightweight modules that reduce system weight by 15% and improve thermal management, enabling more cost-effective launches and extended operational lifespans.

AI-enabled adaptive control is another critical innovation, implemented in approximately 45% of newly deployed TWT systems. This technology allows real-time monitoring of signal amplification, predictive maintenance, and automated performance optimization, reducing unplanned downtime by 15% in complex satellite and radar networks. Broadband TWTs capable of multi-band amplification are increasingly utilized, representing 48% of current deployments, due to their ability to handle diverse frequency ranges required for both commercial and defense communications.

Emerging technologies include hybrid TWT-solid-state systems, which combine vacuum tube reliability with solid-state efficiency, and additive manufacturing for TWT components, enabling precision fabrication and reduced production timelines. Advanced thermal management techniques, including phase-change materials and integrated heat sinks, are improving operational stability under extreme environmental conditions. Overall, the integration of energy-efficient, compact, and intelligent TWT solutions is reshaping market expectations, positioning technology as a decisive factor for competitive differentiation, operational resilience, and sustainable growth in high-performance microwave applications.

• In March 2025, Thales Group delivered Ku‑band Dual Travelling Wave Tubes (Dual‑TWTs) for the ASTRA 1Q satellite developed by Thales Alenia Space, enhancing satellite communications and operational reliability with compact, high‑performance amplification solutions capable of serving both Ku and Ka frequency bands. (ASDNews)

• In 2024, CPI International demonstrated a novel helix TWT design with significantly improved efficiency and reduced heat dissipation optimized for space applications, addressing critical payload amplification needs while enhancing thermal performance for extended missions.

• In 2025, Gooch & Housego launched a high‑power X‑band travelling‑wave tube amplifier designed for defense and space communications, expanding product offerings to meet robust amplification requirements in demanding operational environments.

• In 2024, Stellant Systems, Inc. secured multiple contracts for production of high‑power travelling‑wave tubes and RF amplification products, reflecting sustained defense sector demand and reinforcing capacity for critical spectrum and microwave amplification hardware. (Stellant)

The scope of the Traveling Wave Tubes (TWT) Market Report encompasses a comprehensive, multi‑dimensional analysis of the global TWT landscape, providing business professionals with detailed insights into technological, geographical, and industry application segments. The report covers all primary product categories, including helix TWTs, coupled‑cavity TWTs, high‑power, medium‑power, and miniaturized variants, outlining functional differentiators and performance criteria relevant for aerospace, defense, and commercial communication infrastructure. Key application areas such as satellite communications, radar systems, electronic warfare, and scientific instrumentation are examined for deployment trends, operational performance benchmarks, and usage patterns across varied frequency ranges. It also includes end‑user segmentation, detailing adoption among defense contractors, satellite operators, aerospace manufacturers, and industrial research facilities.

Geographically, the report addresses market developments and regional dynamics in North America, Europe, Asia‑Pacific, South America, and the Middle East & Africa, capturing variations in investment focus, regulatory environments, and consumer adoption behaviors. Coverage extends to technology trends influencing the market, such as AI‑enabled adaptive control, broadband amplification, hybrid solid‑state integration, and advanced thermal management techniques. Furthermore, the report highlights emerging and niche segments, such as mini and compact TWT modules for LEO satellite constellations and specialized radar platforms. By presenting detailed metrics and insights tailored for strategic planning, procurement prioritization, and competitive benchmarking, this report equips decision‑makers with a clear picture of market breadth, technological priorities, and future‑oriented industry shifts.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

L3Harris Technologies, Thales Group, CPI, Raytheon Technologies, Mitsubishi Electric, Northrop Grumman, Advantech Wireless, Satcom Technologies, CommScope, CPI Microwave Systems |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |