Reports

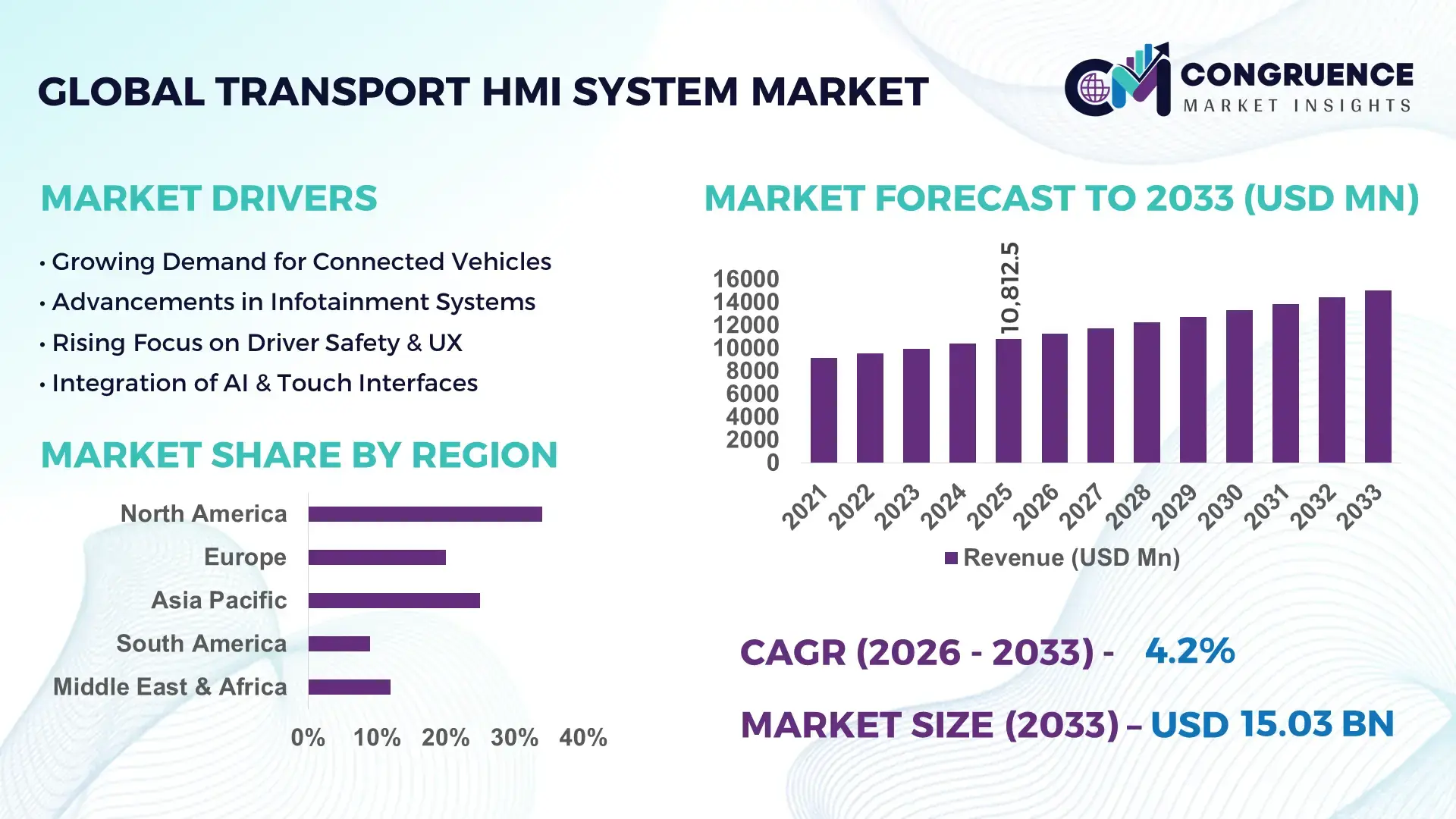

The Global Transport HMI System Market was valued at USD 10812.46 Million in 2025 and is anticipated to reach a value of USD 15026.79 Million by 2033 expanding at a CAGR of 4.2% between 2026 and 2033. This growth is primarily driven by increasing integration of digital cockpit systems and intelligent human-machine interfaces across modern transportation platforms.

The United States continues to exhibit strong dominance in the Transport HMI System market, supported by advanced automotive and aerospace manufacturing ecosystems. The country produces over 10 million vehicles annually, with more than 65% of new vehicles equipped with advanced infotainment and HMI solutions. Investment in intelligent transportation systems exceeded USD 12 billion in recent years, focusing on connected mobility, autonomous driving interfaces, and railway digitization. Major applications include automotive dashboards, aviation control panels, and railway command interfaces, with over 70% of commercial aircraft integrating next-generation HMI displays. Additionally, consumer adoption of touchscreen-based and voice-enabled interfaces has surpassed 75% in premium vehicle segments, reflecting rapid technological evolution and strong industrial demand.

Market Size & Growth: Valued at USD 10812.46 Million in 2025, projected to reach USD 15026.79 Million by 2033, growing at 4.2% CAGR due to rising demand for connected and automated transportation systems.

Top Growth Drivers: 68% adoption of digital cockpit systems, 55% efficiency improvement in transport monitoring, 48% increase in autonomous vehicle interface integration.

Short-Term Forecast: By 2028, HMI optimization is expected to improve system response time by 30% and reduce driver distraction incidents by 25%.

Emerging Technologies: AI-powered voice recognition, augmented reality (AR) dashboards, and haptic feedback systems are reshaping user interaction.

Regional Leaders: North America projected at USD 4.8 Billion by 2033 with high automotive innovation; Europe at USD 4.1 Billion with strong regulatory adoption; Asia-Pacific at USD 5.3 Billion driven by mass production and urban mobility demand.

Consumer/End-User Trends: Over 72% of users prefer touch-based interfaces, while 60% demand integrated smartphone connectivity in transport systems.

Pilot or Case Example: In 2024, a European railway project achieved 28% operational efficiency improvement using AI-based HMI dashboards.

Competitive Landscape: Leading players hold approximately 22% share, followed by key competitors focusing on automotive electronics and smart mobility solutions.

Regulatory & ESG Impact: Emission reduction mandates and safety compliance standards are driving 40% increase in smart HMI adoption.

Investment & Funding Patterns: Over USD 9 Billion invested globally in intelligent transport interface technologies with rising venture funding in AI-driven HMI.

Innovation & Future Outlook: Integration of IoT-enabled displays, predictive analytics, and adaptive UI systems is shaping future transport ecosystems.

The Transport HMI System market is increasingly influenced by diverse industry sectors including automotive, aviation, marine, and railways, each contributing significantly to overall demand. Automotive applications account for over 60% of system deployment due to rising digital cockpit integration, while aviation contributes nearly 20% with advanced avionics displays. Regulatory mandates related to driver safety and emission monitoring are accelerating adoption rates, particularly in Europe and North America. Technological innovations such as gesture control interfaces, multi-display clusters, and AI-enabled predictive user interfaces are transforming user experiences. Asia-Pacific is witnessing rapid consumption growth driven by urbanization and rising vehicle production exceeding 50 million units annually. The future outlook indicates strong emphasis on personalization, real-time data visualization, and seamless connectivity across transport systems.

The strategic relevance of the Transport HMI System market lies in its critical role in enhancing operational efficiency, safety, and user experience across modern transportation ecosystems. With over 70% of new vehicles integrating advanced digital interfaces, businesses are prioritizing investments in intelligent HMI solutions to remain competitive. AI-powered interfaces deliver 35% faster response times compared to conventional analog systems, significantly improving driver interaction and reducing cognitive load. Similarly, augmented reality dashboards provide up to 40% better situational awareness compared to traditional display panels.

Regionally, Asia-Pacific dominates in volume due to large-scale vehicle production, while Europe leads in adoption with over 65% of enterprises implementing advanced HMI technologies in transportation infrastructure. In the short term, by 2028, AI-driven predictive interfaces are expected to reduce operational errors by 30% and improve system efficiency by 25%. Companies are aligning with ESG goals, committing to reduce electronic waste by 20% and enhance energy-efficient display technologies by 2027.

A notable micro-scenario includes a 2024 initiative in Japan where automotive manufacturers achieved a 32% improvement in driver response time through integration of voice-controlled HMI systems and adaptive UI technologies. The increasing convergence of IoT, AI, and real-time analytics is enabling highly personalized and responsive transport interfaces. Looking ahead, the Transport HMI System market is positioned as a foundational pillar supporting resilient transportation infrastructure, regulatory compliance, and sustainable mobility transformation across global markets.

The increasing adoption of connected and autonomous vehicles is a primary driver of the Transport HMI System market. More than 60% of new vehicles are now equipped with connected features, requiring advanced HMI solutions for seamless interaction. Autonomous driving technologies depend heavily on real-time data visualization, increasing demand for high-resolution displays and intuitive interfaces. Studies indicate that advanced HMI systems can reduce driver reaction time by up to 35%, enhancing safety outcomes. Additionally, the integration of voice recognition and gesture control technologies has improved user engagement by over 40%. Governments worldwide are also promoting smart mobility initiatives, further accelerating the deployment of sophisticated HMI systems across transport networks.

High implementation costs and system complexity remain significant barriers to widespread adoption of Transport HMI systems. Advanced HMI solutions require integration of multiple technologies including AI, sensors, and high-performance computing, increasing overall system costs by up to 25%. Small and mid-sized manufacturers often face challenges in adopting these systems due to limited capital resources. Additionally, the complexity of integrating HMI with existing vehicle architectures can extend development timelines by 20–30%. Maintenance and software updates also add to operational costs. Furthermore, cybersecurity concerns associated with connected interfaces are rising, with over 45% of transport operators identifying data security as a critical challenge, thereby slowing adoption rates.

The rapid expansion of smart transportation infrastructure presents significant growth opportunities for the Transport HMI System market. Global smart city initiatives are increasing investments in intelligent transport systems, with over 100 cities deploying advanced mobility solutions. These developments require sophisticated HMI interfaces for traffic management, public transport monitoring, and passenger information systems. Railway networks are increasingly adopting digital control panels, improving operational efficiency by up to 30%. Additionally, the rise of electric vehicles is creating demand for specialized HMI systems focused on battery management and energy efficiency visualization. Emerging markets in Asia and the Middle East are also investing heavily in modern transport infrastructure, providing new avenues for market expansion.

Regulatory compliance and interoperability challenges pose significant obstacles to the Transport HMI System market. Different regions have varying safety and operational standards, requiring manufacturers to customize systems for each market, increasing development costs and time. Compliance with stringent safety regulations can extend product certification timelines by up to 18 months. Interoperability between different hardware and software platforms is another critical issue, as over 50% of transport systems operate on legacy infrastructure. Ensuring seamless integration across diverse platforms requires extensive testing and standardization efforts. Additionally, the lack of unified global standards for HMI systems complicates cross-border deployments, limiting scalability and hindering market growth.

• Rapid Adoption of AI-Powered Voice and Gesture Interfaces: The integration of AI-driven voice recognition and gesture control technologies is transforming transport HMI systems. Over 62% of newly manufactured vehicles now incorporate voice-enabled controls, improving driver interaction efficiency by nearly 35%. Gesture-based systems have reduced manual touch interactions by 28%, particularly in premium vehicle segments. In aviation, more than 40% of next-generation cockpits are integrating AI-assisted command systems, enhancing pilot response times by 22% and reducing operational errors significantly.

• Expansion of Augmented Reality (AR) and Head-Up Displays (HUDs): AR-based HMI solutions are gaining momentum, with over 48% of high-end vehicles equipped with head-up displays that project real-time navigation and hazard alerts. These systems have improved situational awareness by approximately 37% and reduced driver distraction rates by 25%. In railway systems, AR-enabled dashboards are being adopted in over 30% of modern control rooms, enabling faster decision-making and real-time monitoring of network conditions across large-scale operations.

• Increased Integration of IoT and Cloud-Connected Interfaces: IoT-enabled HMI systems are now present in over 58% of smart transport networks, facilitating seamless communication between vehicles and infrastructure. Cloud integration has enabled real-time data synchronization, improving fleet management efficiency by 33%. Public transportation systems leveraging connected HMI platforms have reported a 27% improvement in passenger information accuracy and operational coordination, especially in densely populated urban regions.

• Growth in Multi-Display and Personalized User Interfaces: Multi-display cockpit systems are being adopted in nearly 55% of newly produced vehicles, offering enhanced customization and real-time data visualization. Personalized HMI interfaces, powered by machine learning, have increased user satisfaction levels by 30% by adapting to driver preferences and usage patterns. Additionally, over 45% of transport operators are investing in adaptive UI technologies to improve user engagement and reduce cognitive load, particularly in autonomous and semi-autonomous vehicles.

The Transport HMI System market segmentation is structured across product types, application areas, and end-user industries, each contributing distinctively to market expansion. Display-based interfaces, voice recognition systems, and control panels form the core product categories, with display technologies accounting for a significant portion due to their widespread use in automotive dashboards and aviation systems. Application-wise, automotive remains the dominant segment, representing over 60% of total deployment, followed by aviation and railway sectors that rely heavily on advanced HMI systems for operational control and safety monitoring. End-user insights indicate strong adoption among automotive manufacturers, public transport authorities, and logistics providers, with increasing penetration in emerging economies. The segmentation reflects a growing shift toward integrated, intelligent, and user-centric interface solutions across global transportation ecosystems.

The Transport HMI System market by type includes display interfaces, voice control systems, gesture-based systems, and control panels. Display interfaces dominate the segment, accounting for approximately 46% of total adoption, driven by widespread deployment in automotive digital dashboards and aircraft cockpit displays. These systems provide high-resolution visualization and real-time data integration, making them essential for modern transportation. Voice control systems hold around 24% share, offering hands-free operation and improved safety, especially in connected vehicles. Gesture-based interfaces, while currently representing nearly 12%, are emerging rapidly with a projected growth rate exceeding 8.5% annually, supported by advancements in sensor technologies and user experience optimization.

Control panels and other conventional interface systems collectively contribute about 18% of the market, maintaining relevance in legacy transport systems and industrial applications. The fastest growth is observed in gesture-based systems due to increasing demand for contactless interaction and enhanced safety features.

By application, the Transport HMI System market is categorized into automotive, aviation, railway, and marine sectors. Automotive leads with over 62% share, attributed to the rapid integration of digital cockpits, infotainment systems, and driver assistance technologies. Aviation follows with approximately 18% adoption, where advanced HMI systems are critical for flight navigation, control systems, and pilot interaction. Railway applications account for nearly 12%, focusing on control room dashboards, signaling systems, and passenger information displays.

Marine and other niche applications contribute the remaining 8%, primarily involving navigation systems and vessel monitoring interfaces. The fastest-growing application segment is railway, expanding at an estimated rate of over 9% annually due to increasing investments in smart rail infrastructure and digital control systems.

End-user segmentation in the Transport HMI System market includes automotive manufacturers, transportation authorities, aerospace companies, and logistics providers. Automotive manufacturers dominate with approximately 58% share, driven by increasing production of connected and autonomous vehicles equipped with advanced HMI systems. Transportation authorities represent around 20% of adoption, utilizing HMI solutions for traffic management, public transport monitoring, and smart city integration.

Aerospace companies account for nearly 14%, leveraging high-performance HMI systems in aircraft control and navigation. Logistics and fleet management companies contribute the remaining 8%, focusing on real-time tracking and operational optimization. The fastest-growing end-user segment is transportation authorities, with an estimated growth rate exceeding 8.8% annually, supported by global smart city initiatives and infrastructure modernization projects.

Region North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2026 and 2033.

North America’s dominance is supported by over 70% integration of advanced digital cockpit systems in newly manufactured vehicles and more than 60% adoption of AI-enabled HMI interfaces across aviation and rail sectors. Europe follows with approximately 28% share, driven by stringent safety regulations and over 55% penetration of advanced driver assistance systems. Asia-Pacific holds nearly 30% share, with vehicle production exceeding 50 million units annually and over 65% of urban transit systems adopting digital control interfaces. South America contributes around 5%, supported by increasing smart mobility investments, while the Middle East & Africa accounts for nearly 3%, driven by infrastructure modernization and smart city initiatives. Across all regions, more than 58% of transport systems now rely on connected HMI platforms, reflecting a global shift toward intelligent and integrated transport ecosystems.

How are advanced digital cockpit innovations transforming transport interface adoption?

North America holds approximately 34% of the Transport HMI System market share, supported by strong demand from automotive, aerospace, and railway industries. Over 68% of vehicles produced in the region feature advanced infotainment and HMI systems, while aviation adoption exceeds 60% in commercial fleets. Regulatory frameworks emphasizing driver safety and digital compliance have accelerated the deployment of intelligent interfaces. Government initiatives supporting connected vehicle infrastructure have increased investment in smart mobility solutions by over 20% in recent years. Technological advancements include widespread use of AI-powered voice interfaces, augmented reality dashboards, and cloud-connected systems. A leading regional player has focused on integrating multi-display cockpit solutions, improving user interaction efficiency by 30%. Consumer behavior reflects high preference for seamless connectivity, with over 72% of users demanding smartphone-integrated HMI systems and personalized digital experiences across transport platforms.

Why is regulatory-driven innovation accelerating intelligent interface adoption?

Europe accounts for approximately 28% of the Transport HMI System market, with key markets including Germany, the UK, and France leading adoption. Over 58% of vehicles in these countries are equipped with advanced HMI systems, driven by strict safety and environmental regulations. Regional policies promoting emission reduction and road safety have resulted in a 40% increase in demand for intelligent driver assistance interfaces. The adoption of emerging technologies such as AR-based displays and AI-powered predictive interfaces is expanding rapidly, with nearly 45% of new vehicles incorporating these features. Local manufacturers are investing heavily in digital transformation, with one major automotive supplier deploying next-generation HMI platforms that enhanced driver response times by 27%. Consumer behavior in the region is influenced by regulatory compliance, with over 65% of enterprises prioritizing transparent and explainable interface technologies.

What factors are driving large-scale adoption of intelligent transport interfaces?

Asia-Pacific ranks as the fastest-growing region in the Transport HMI System market, contributing nearly 30% of global volume. Major consuming countries such as China, India, and Japan collectively produce over 50 million vehicles annually, with more than 60% incorporating digital HMI systems. Rapid urbanization and infrastructure expansion have led to over 70% of metro and rail networks adopting advanced control interfaces. The region is a hub for manufacturing innovation, with increasing investments in AI-driven HMI technologies and IoT-enabled transport systems. A prominent regional manufacturer has implemented smart cockpit solutions across its vehicle lineup, improving system responsiveness by 33%. Consumer behavior is heavily influenced by mobile-first ecosystems, with over 75% of users preferring touchscreen and app-integrated interfaces, reflecting strong alignment with digital lifestyles and smart mobility trends.

How are infrastructure modernization efforts influencing transport interface demand?

South America holds approximately 5% share in the Transport HMI System market, with Brazil and Argentina being the primary contributors. Infrastructure development and modernization of public transport systems have increased adoption of digital HMI platforms by over 35% in recent years. Government initiatives aimed at improving urban mobility and reducing traffic congestion have accelerated investments in intelligent transport solutions. The energy and logistics sectors are also contributing to demand, particularly in fleet management and monitoring systems. A regional player has introduced advanced HMI dashboards for commercial fleets, resulting in a 22% improvement in operational efficiency. Consumer behavior reflects growing demand for localized and language-specific interfaces, with over 60% of users preferring regionally customized digital solutions that enhance usability and accessibility.

How is smart infrastructure development reshaping intelligent transport interfaces?

The Middle East & Africa region accounts for nearly 3% of the Transport HMI System market, driven by increasing investments in smart city and infrastructure projects. Countries such as the UAE and South Africa are leading adoption, with over 40% of new transport systems integrating digital HMI solutions. The oil and gas sector, along with construction and logistics industries, is contributing to demand for advanced monitoring and control interfaces. Technological modernization efforts have resulted in over 30% improvement in system efficiency through the deployment of AI-enabled dashboards. Trade partnerships and government-backed initiatives are supporting the adoption of intelligent transport solutions. A regional technology provider has implemented integrated HMI platforms across urban transit networks, enhancing operational performance by 25%. Consumer behavior shows rising preference for high-performance, multilingual interfaces tailored to diverse user groups.

United States Transport HMI System Market – 34% share: Strong automotive production exceeding 10 million units annually and high adoption of advanced digital cockpit technologies.

China Transport HMI System Market – 28% share: Large-scale vehicle manufacturing and rapid integration of smart mobility and connected transport systems.

The Transport HMI System market is moderately fragmented, with over 45 active global and regional competitors operating across automotive, aerospace, and industrial segments. The top five companies collectively account for approximately 38% of the market, indicating a competitive yet innovation-driven landscape. Leading players are focusing on strategic partnerships, product innovation, and expansion into emerging markets to strengthen their positions. Over 60% of major companies have increased their investment in research and development, particularly in AI-driven interfaces, augmented reality displays, and connected mobility platforms.

Recent years have witnessed more than 25 strategic collaborations between automotive manufacturers and technology providers aimed at developing next-generation HMI solutions. Product launches have increased by 30%, with a strong emphasis on multi-display systems, voice-controlled interfaces, and predictive analytics integration. Mergers and acquisitions activity has also intensified, with over 15 notable deals focused on expanding technological capabilities and geographic presence. Additionally, companies are leveraging cloud computing and IoT technologies to enhance system scalability and performance. Competitive differentiation is increasingly based on user experience, system reliability, and integration capabilities, making innovation a key driver in sustaining market leadership.

Continental AG

Robert Bosch GmbH

Denso Corporation

Panasonic Corporation

Visteon Corporation

Valeo SA

HARMAN International

Mitsubishi Electric Corporation

Siemens AG

Thales Group

Garmin Ltd.

Alpine Electronics Inc.

Clarion Co., Ltd.

Delphi Technologies

Nippon Seiki Co., Ltd.

The Transport HMI System market is undergoing rapid technological transformation, driven by advancements in artificial intelligence, augmented reality, and connected vehicle ecosystems. AI-powered interfaces are now embedded in over 65% of modern transport systems, enabling predictive analytics, voice recognition, and adaptive user interfaces. These systems improve driver response time by nearly 35% and reduce operational errors by approximately 28%. Machine learning algorithms are increasingly used to personalize interface layouts based on user behavior, with over 50% of premium vehicles offering adaptive dashboard configurations.

Augmented reality (AR) and head-up display (HUD) technologies are gaining widespread adoption, particularly in automotive and aviation sectors. Over 48% of high-end vehicles now incorporate AR-enabled displays, enhancing situational awareness by projecting navigation, hazard alerts, and real-time data directly onto windshields. In aviation, next-generation cockpit displays integrate multi-layered data visualization systems, improving pilot efficiency by over 30%. Gesture recognition and haptic feedback technologies are also expanding, reducing physical interaction with controls by up to 25% and enhancing safety in high-speed environments.

The integration of Internet of Things (IoT) and cloud computing is further redefining transport HMI capabilities. More than 58% of transport networks now utilize cloud-connected HMI systems for real-time data synchronization and remote diagnostics. Edge computing is emerging as a critical enabler, reducing data processing latency by nearly 40% and supporting real-time decision-making in autonomous systems. Additionally, cybersecurity technologies are becoming essential, with over 45% of manufacturers implementing advanced encryption and intrusion detection systems to protect connected interfaces. These technological advancements are collectively shaping a highly intelligent, responsive, and secure HMI ecosystem across global transportation platforms.

• In January 2025, Continental AG introduced an advanced 3D curved display system for automotive cockpits, integrating real-time driver monitoring and AI-based interface adaptation. The system enhances visual depth perception and reduces driver distraction by over 20%, improving overall user interaction efficiency. Source: www.continental.com

• In March 2025, HARMAN International launched its next-generation Ready Vision QVUE augmented reality head-up display, capable of projecting information up to 15 meters ahead. The system improves situational awareness and reduces cognitive load by nearly 30% in complex driving environments. Source: www.harman.com

• In September 2024, Visteon Corporation expanded its SmartCore cockpit domain controller platform, enabling integration of up to 6 displays and advanced driver assistance systems. The platform supports high-speed data processing and enhances system performance by over 25% in connected vehicles. Source: www.visteon.com

• In November 2024, Bosch introduced an AI-powered voice assistant for automotive HMI systems, capable of understanding natural language commands with over 95% accuracy. The solution improves driver interaction speed by 30% and supports multilingual functionality across global markets. Source: www.bosch.com

The Transport HMI System Market Report provides a comprehensive evaluation of industry dynamics, covering multiple dimensions including product types, applications, technologies, and regional distribution. The report analyzes key segments such as display interfaces, voice-controlled systems, gesture recognition technologies, and integrated control panels, which collectively account for over 80% of system deployments across transportation platforms. It also examines application areas including automotive, aviation, railway, and marine sectors, with automotive contributing more than 60% of total installations due to the rapid integration of digital cockpit systems and connected vehicle technologies.

Geographically, the report encompasses major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing over 95% of global demand patterns. Asia-Pacific is highlighted for its large-scale manufacturing output exceeding 50 million vehicles annually, while North America and Europe are analyzed for their advanced technological adoption and regulatory frameworks. The report further explores emerging technologies such as AI-driven interfaces, AR-based displays, IoT-enabled connectivity, and edge computing solutions, which are collectively influencing over 70% of new system developments.

In addition, the scope includes evaluation of end-user industries such as automotive manufacturers, transportation authorities, aerospace companies, and logistics providers, each contributing distinct adoption patterns. The report also addresses niche segments including electric vehicle-specific HMI systems and autonomous transport interfaces, which are gaining traction with adoption rates increasing by over 40% in pilot deployments. Overall, the report offers a structured, data-driven perspective designed to support strategic decision-making, technology investments, and market entry planning for stakeholders across the global transport ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Continental AG, Robert Bosch GmbH, Denso Corporation, Panasonic Corporation, Visteon Corporation, Valeo SA, HARMAN International, Mitsubishi Electric Corporation, Siemens AG, Thales Group, Garmin Ltd., Alpine Electronics Inc., Clarion Co., Ltd., Delphi Technologies, Nippon Seiki Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |