Reports

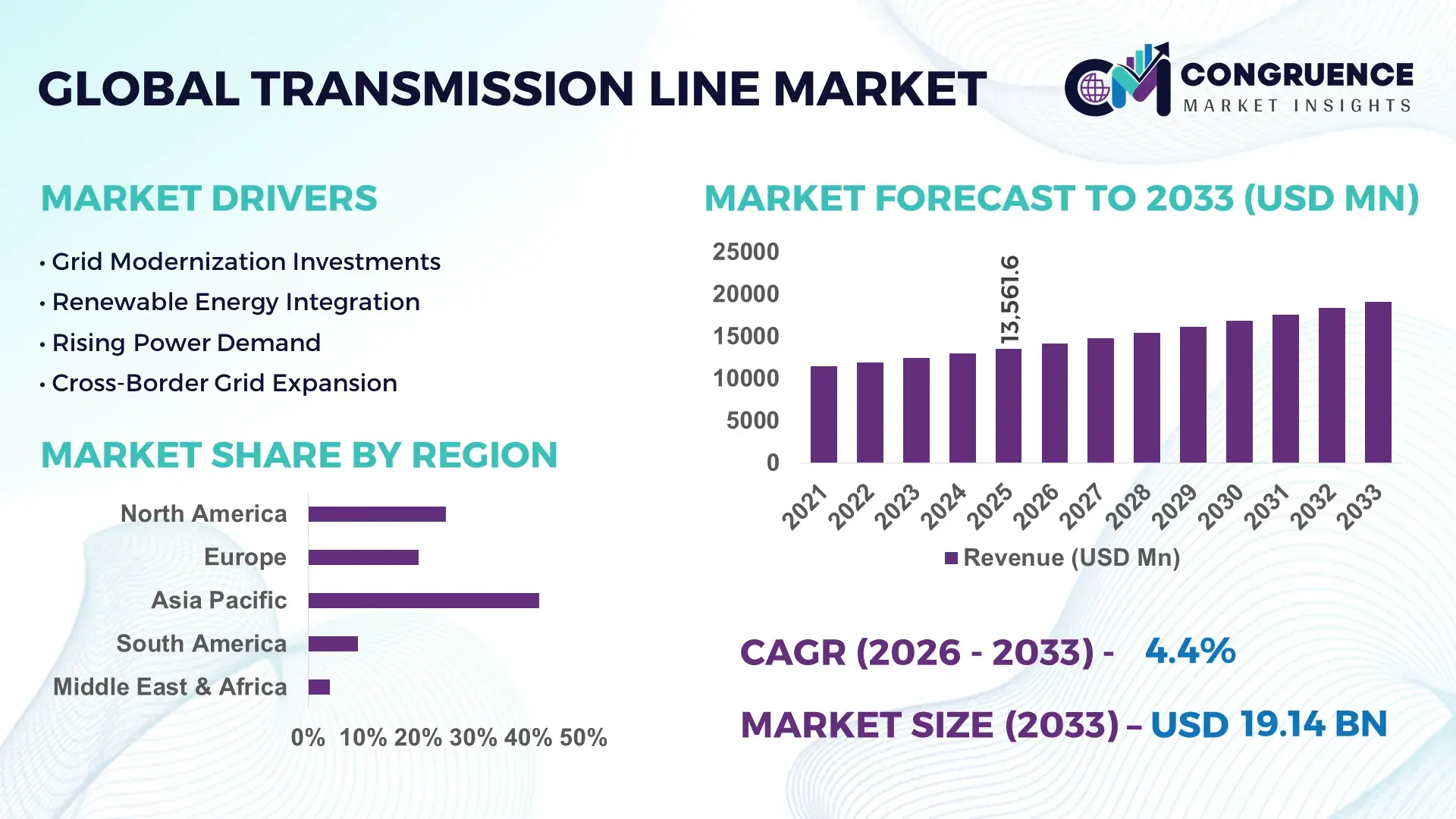

The Global Transmission Line Market was valued at USD 13561.56 Million in 2025 and is anticipated to reach a value of USD 19138.75 Million by 2033 expanding at a CAGR of 4.4% between 2026 and 2033. Market expansion is being driven by accelerated high-voltage transmission corridor deployment, cross-border grid interconnections, renewable energy evacuation projects, and large-scale grid modernization investments supporting energy security objectives.

China remains the dominant country in the transmission line sector, accounting for approximately 32% of global installed transmission infrastructure capacity, supported by multi-billion-dollar ultra-high-voltage network investments and rapid renewable integration programs. The country operates more than 45 GW of UHV transmission capacity, significantly ahead of India, where national grid expansion and renewable energy corridors continue to accelerate. Rising electrification, industrial consumption, and strategic energy resilience initiatives linked to evolving geopolitical energy security priorities are strengthening transmission network deployment across both markets, with China maintaining a capacity advantage exceeding 2.5 times that of India.

Strategic focus on advanced transmission technologies, localized manufacturing capabilities, and long-distance grid connectivity projects will determine competitive positioning and infrastructure investment returns through 2033.

Market Size & Growth: USD 13,561.56 million in 2025 reaching USD 19,138.75 million by 2033 at 4.4% CAGR, supported by renewable energy evacuation networks and grid modernization programs.

Top Growth Drivers: Renewable integration (+28%), grid reliability upgrades (+24%), and cross-border interconnection projects (+18%) are driving capital deployment.

Short-Term Forecast: By 2028, advanced transmission projects improve power transfer efficiency by 12% while reducing line losses by nearly 8%.

Emerging Technologies: AI-based grid monitoring, digital substations, and advanced composite conductors increase operational efficiency by 10–15%.

Regional Leaders: Asia-Pacific exceeds USD 8.5 billion, North America approaches USD 3.7 billion, and Europe surpasses USD 3.1 billion, driven by smart-grid adoption.

Consumer/End-User Trends: More than 65% of utility operators prioritize high-capacity transmission upgrades to accommodate renewable power flows.

Pilot/Case Example: A 2026 HVDC corridor deployment demonstrated approximately 14% lower transmission losses and 11% higher network utilization.

Competitive Landscape: Top players collectively hold around 38% market share, with leading positions maintained by major global transmission equipment and EPC providers.

Regulatory & ESG Impact: Grid decarbonization initiatives support over 20% reduction in transmission-related energy losses across modernization programs.

Investment & Funding: Annual infrastructure investments exceed USD 70 billion globally, supported by strategic partnerships and regional expansion initiatives.

Innovation & Future Outlook: Next-generation HVDC systems, dynamic line rating, and digital grid analytics improve asset utilization by over 15% while strengthening network resilience.

The Transmission Line Market is experiencing strong demand from renewable energy integration, industrial electrification, and long-distance power transfer applications. Utilities are increasingly deploying advanced conductors, digital monitoring systems, and high-voltage direct current technologies that improve transmission efficiency by approximately 10–15%. A notable trend is the growing adoption of dynamic line rating solutions, enabling higher network utilization under evolving grid conditions. Concurrent supply-chain localization efforts and grid resilience regulations are reshaping procurement strategies, setting the stage for deeper strategic evaluation of competitive and investment opportunities.

Transmission line infrastructure has become a strategic asset for energy security, industrial competitiveness, and large-scale renewable integration. Utilities and grid operators are prioritizing network expansion as power demand from data centers, electrified manufacturing, and clean energy projects accelerates. A major market shift is the restructuring of transmission equipment supply chains, with countries increasing domestic manufacturing capacity to reduce dependency on imported components. More than 40% of newly announced grid investments are now linked to modernization and resilience objectives, strengthening the market’s long-term strategic relevance.

Technology upgrades are reshaping operational economics. High-voltage direct current (HVDC) systems reduce transmission losses by approximately 30–40% compared with conventional long-distance AC networks, while advanced conductors increase power-carrying capacity by nearly 20%. China continues to lead large-scale deployment through ultra-high-voltage corridors, whereas India is emphasizing renewable energy evacuation networks and digital grid integration. Over the next two to three years, utilities are expected to expand dynamic line monitoring deployments by more than 25%, improving asset utilization and network reliability.

A practical example is the deployment of renewable energy corridors connecting remote generation assets to industrial demand centers, reducing congestion and improving grid stability. Companies are responding through technology partnerships, conductor manufacturing expansion, and digital grid investments. Organizations that secure advanced transmission capabilities, localized supply networks, and grid intelligence platforms will strengthen competitive positioning and gain a durable operational advantage as power systems become increasingly interconnected.

The strongest driver for the transmission line market is the rapid expansion of renewable energy capacity and the modernization of aging grid infrastructure. More than 35% of new utility investments are being directed toward transmission upgrades, while advanced conductor adoption improves network capacity by up to 20% and reduces technical losses by nearly 10%. India’s Green Energy Corridor programs and China's ultra-high-voltage projects illustrate how renewable integration requirements are reshaping transmission priorities. The direct impact is higher demand for long-distance power transfer infrastructure and digital monitoring systems. In response, manufacturers and EPC contractors are expanding production facilities, forming technology partnerships, and investing in higher-capacity conductor solutions. A notable strategic insight is that grid operators increasingly prioritize transmission efficiency gains over new generation additions, improving overall system economics and network utilization.

Transmission line deployment continues to face pressure from conductor material cost fluctuations, land acquisition challenges, and lengthy approval procedures. Aluminum and steel account for a significant share of project costs, with input price movements of 15–20% affecting procurement budgets and project scheduling. In several countries, transmission projects can experience permitting delays exceeding 25% of planned timelines due to environmental reviews and right-of-way constraints. These factors directly impact deployment scalability, contractor margins, and capital allocation efficiency. To reduce exposure, companies are localizing supply chains, securing long-term material contracts, and diversifying supplier networks. A key operational insight is that procurement resilience is increasingly becoming a competitive differentiator, as stable material sourcing often determines project execution performance more than engineering capability alone.

A significant opportunity lies in the convergence of transmission infrastructure with digital grid technologies. Utilities deploying real-time monitoring and dynamic line rating systems report asset utilization improvements of 10–15%, while predictive maintenance platforms reduce outage-related costs by nearly 20%. India and Saudi Arabia are accelerating smart-grid investments to improve network visibility and renewable integration efficiency. Emerging technologies such as AI-enabled grid analytics and digital twins are creating new value pools beyond conventional infrastructure deployment. Companies are positioning through software partnerships, R&D programs, and integrated transmission management platforms. A unique strategic insight is that future competitive advantage will increasingly depend on data-driven network optimization rather than solely on physical transmission capacity, creating opportunities for technology providers alongside traditional infrastructure players.

As transmission networks become more digital and interconnected, integration complexity is emerging as a major execution challenge. More than 30% of utilities report shortages of specialized engineering and grid automation talent, while digital system integration can increase project implementation timelines by approximately 15%. The growing use of connected sensors, advanced substations, and automated control systems also expands cybersecurity exposure across critical infrastructure networks. These pressures affect deployment consistency, operational resilience, and long-term competitiveness. Companies are addressing the issue through workforce development programs, technology partnerships, and investments in cyber-resilient grid architectures. A critical strategic insight is that organizations capable of integrating physical infrastructure, digital intelligence, and cybersecurity frameworks simultaneously will achieve stronger operational reliability and maintain a sustainable competitive edge.

Dynamic Line Rating Expansion: Utilities are increasing dynamic line rating deployments by nearly 25%, enabling existing corridors to carry 10–15% more power without major infrastructure additions. Rising grid congestion and renewable energy variability are accelerating adoption. Operators in India and Australia are integrating sensor-based monitoring into transmission workflows, reducing curtailment events and improving asset utilization. Companies are responding through analytics partnerships and grid digitalization programs that shorten upgrade cycles and improve operational flexibility.

Localized Supply Chain Realignment: Transmission equipment manufacturers are restructuring procurement networks as localization requirements strengthen. Domestic sourcing of conductors, towers, and hardware has increased by approximately 20% in several key markets, while project lead times have declined by 8–12%. Supply-chain resilience is becoming a competitive metric rather than a procurement function. Companies are expanding regional manufacturing footprints, securing long-term material agreements, and developing multi-country supplier ecosystems to improve delivery consistency.

Advanced Conductor Adoption Rising: High-capacity conductors are replacing legacy solutions across network upgrade projects, improving transmission efficiency by 10% and increasing line capacity by up to 20%. Rather than constructing entirely new routes, utilities are prioritizing reconductoring strategies to accelerate deployment and reduce permitting complexity. Manufacturers are expanding specialized conductor portfolios and collaborating with grid operators to support faster modernization programs.

HVDC Corridor Development Accelerates: Long-distance power transfer projects are increasingly utilizing HVDC technology, reducing transmission losses by 30–40% compared with conventional long-distance AC systems. Growing renewable energy integration requirements and cross-border electricity exchanges are driving deployment. Transmission developers are forming technology alliances, standardizing project architectures, and increasing investment in converter infrastructure to improve scalability and network stability.

Overhead Lines remain the leading segment due to lower installation costs, easier maintenance access, and suitability for large-scale transmission expansion projects. They account for an estimated 60% of transmission infrastructure deployment globally and continue to dominate utility-scale grid expansion programs in China, India, and the United States. HVAC Lines maintain strong adoption because of their compatibility with existing networks and established operational frameworks. Underground Lines are gaining traction in densely populated urban corridors where right-of-way constraints and reliability requirements are increasing infrastructure complexity.

HVDC Lines represent the fastest-growing segment as utilities prioritize long-distance renewable energy transmission and interregional power exchange. Compared with conventional HVAC systems, HVDC technology can reduce transmission losses by 30–40% over extended distances. Submarine Cables are also witnessing increased deployment for offshore wind integration and island-grid connectivity projects. Companies are expanding HVDC manufacturing capabilities, investing in advanced conductor technologies, and strengthening technology partnerships to capture high-value infrastructure contracts. Investment priorities are gradually shifting from traditional expansion toward efficiency-focused transmission architectures capable of supporting higher renewable penetration.

Power Transmission remains the dominant application because national grids continue to require extensive network reinforcement, capacity expansion, and reliability upgrades. This segment accounts for approximately 45% of transmission infrastructure utilization, supported by growing electricity consumption and aging grid replacement programs. Grid Interconnection projects are also expanding as countries pursue stronger energy security and network balancing capabilities. Urban Electrification remains strategically important, particularly in rapidly growing metropolitan areas where transmission reliability directly affects economic activity.

Renewable Energy Integration is the fastest-growing application segment, driven by large-scale solar and wind deployment requiring dedicated evacuation infrastructure. Renewable-linked transmission projects have increased by nearly 30% in several major energy markets, while advanced monitoring technologies improve grid balancing efficiency by approximately 15%. Industrial Power Supply applications continue to expand around manufacturing clusters, mining operations, and data center developments. Companies are responding through network automation, transmission corridor expansion, and renewable-focused infrastructure partnerships. Demand is increasingly concentrating around applications that support grid flexibility and high-volume power movement across geographically dispersed generation assets.

Utility Companies remain the largest end-user group because they manage the majority of transmission assets and lead national grid modernization initiatives. Utilities account for more than 50% of transmission infrastructure procurement activity, supported by reliability targets, capacity expansion programs, and digital grid investments. Government Agencies continue to influence demand through infrastructure funding mechanisms and strategic energy security programs. Infrastructure Developers also play an important role by supporting large transmission corridor construction and interconnection projects.

Renewable Energy Developers represent the fastest-growing end-user segment as utility-scale wind and solar projects increasingly require dedicated transmission connectivity. Transmission demand associated with renewable projects has expanded by approximately 25%, while grid connection requirements continue to intensify. Power Generation Companies are investing in transmission partnerships to improve market access, while Industrial Facilities are strengthening procurement activity to secure reliable high-capacity power supply. Companies are targeting these segments through customized transmission solutions, integrated service offerings, and long-term partnership models. Competitive positioning increasingly depends on the ability to align infrastructure deployment with evolving energy transition requirements and grid modernization priorities.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 5.8% rate between 2026 and 2033.

Grid Reliability Investments Accelerate Network Upgrades

North America represents a significant share of the transmission line market, supported by aging grid replacement programs, renewable energy integration requirements, and increasing electricity demand from data centers and industrial facilities. The region accounts for approximately 24% of global transmission infrastructure activity, with the United States leading large-scale grid modernization efforts. Utilities are increasingly deploying advanced conductors and digital monitoring systems to improve network efficiency and reduce transmission losses. Recent transmission corridor expansion projects have increased long-distance power transfer capability by more than 12% across several utility networks. Companies are prioritizing grid resilience investments, transmission automation, and strategic partnerships to strengthen operational performance and improve asset utilization.

United States Market Outlook: The United States remains the region’s most influential market due to extensive transmission infrastructure, large-scale renewable integration programs, and ongoing grid modernization initiatives. Utility operators are expanding high-voltage transmission corridors to support growing electricity demand from manufacturing facilities and hyperscale data centers. More than 70% of major utility investment plans include transmission upgrades, while advanced grid monitoring deployments continue to improve operational visibility. Strong regulatory support for infrastructure modernization and domestic manufacturing expansion reinforces long-term market positioning.

Cross-Border Interconnection Reshapes Transmission Priorities

Europe maintains a strong market position through extensive grid interconnection projects, renewable energy integration requirements, and transmission modernization initiatives. The region accounts for nearly 22% of global transmission deployment activity and continues to prioritize energy security through enhanced network connectivity. High-voltage and subsea transmission projects are expanding to support offshore wind developments and cross-border electricity exchange. Several interconnection projects have improved transfer capacity by approximately 15%, strengthening network stability and operational flexibility. Companies are investing in smart-grid technologies, digital substations, and advanced transmission equipment to improve efficiency and support evolving energy transition objectives.

Germany Market Outlook: Germany serves as the region’s strategic transmission hub due to its industrial scale, renewable energy deployment, and grid balancing requirements. The country continues expanding north-to-south transmission corridors to connect offshore wind generation with industrial demand centers. Utilities are accelerating deployment of digital grid technologies and advanced transmission infrastructure, improving network management efficiency. Strong engineering expertise, regulatory support, and transmission planning capabilities position Germany as a key market influencing infrastructure investment decisions across Europe.

Massive Infrastructure Scale Drives Market Leadership

Asia-Pacific leads the global transmission line market, accounting for approximately 42% of total market activity. Large-scale grid expansion, industrial electrification, and renewable energy deployment continue to support transmission infrastructure demand across China, India, and Southeast Asia. The region benefits from extensive manufacturing capabilities and strong investment in high-voltage transmission technologies. Multiple national transmission projects have expanded network capacity by more than 20% in key markets, supporting long-distance power transfer requirements. Companies are strengthening domestic production, expanding EPC capabilities, and accelerating deployment of advanced conductors and grid automation solutions to support growing electricity demand.

China Market Outlook: China remains the largest individual market due to its ultra-high-voltage transmission leadership, extensive manufacturing ecosystem, and large-scale renewable integration programs. The country operates one of the world's most advanced transmission networks, with continuous investment in long-distance power transfer infrastructure. Transmission equipment manufacturers are expanding production capacity while utilities continue deploying digital monitoring technologies. Strong policy alignment, industrial demand, and grid modernization initiatives provide sustained momentum for transmission infrastructure development.

Renewable Connectivity Expands Infrastructure Demand

South America is experiencing increasing transmission investment as governments and utilities seek to improve grid reliability and connect renewable generation assets. The region accounts for roughly 7% of global transmission activity, with Brazil leading infrastructure deployment. Long-distance transmission projects are becoming essential for connecting hydropower, solar, and wind resources to major consumption centers. Several grid expansion programs have improved regional transmission capacity by approximately 10%, although permitting processes and financing constraints remain execution challenges. Companies are focusing on strategic partnerships, localized engineering expertise, and phased infrastructure deployment to improve project delivery and operational performance.

Brazil Market Outlook: Brazil dominates regional transmission activity through its extensive electricity network, renewable energy resources, and large-scale infrastructure projects. Transmission operators continue expanding long-distance corridors connecting renewable generation zones with urban and industrial demand centers. Grid reinforcement initiatives have improved network reliability and operational efficiency across several states. Strong public-private collaboration and ongoing infrastructure development programs support the country’s position as South America's most influential transmission market.

Energy Diversification Spurs Network Expansion

The Middle East & Africa region is emerging as the fastest-expanding transmission line market due to large-scale infrastructure investment, grid modernization programs, and energy diversification strategies. Countries across the Gulf region are strengthening transmission networks to support renewable energy projects and growing electricity demand. Regional transmission investments have increased by approximately 18% in recent development cycles, supporting higher-capacity interconnections and network resilience. Utilities are adopting advanced transmission technologies and digital monitoring platforms to improve operational performance. Companies are entering strategic partnerships and expanding project execution capabilities to capture infrastructure opportunities.

Saudi Arabia Market Outlook: Saudi Arabia is the region’s leading transmission market due to extensive energy infrastructure investments, utility modernization programs, and large renewable energy deployment targets. National grid expansion initiatives continue strengthening long-distance transmission connectivity between generation and consumption centers. Utilities are implementing advanced monitoring systems and high-capacity transmission technologies to improve network reliability. The country's focus on energy diversification, industrial expansion, and infrastructure modernization positions it as a critical driver of regional transmission demand.

The transmission line market is characterized by competition between global technology leaders such as Hitachi Energy, Siemens Energy, GE Vernova, Prysmian Group, and Nexans, and regional infrastructure specialists focused on cost-efficient deployment and localized manufacturing. The top five participants collectively account for approximately 35–40% of market activity. Competition centers on transmission efficiency, project execution speed, supply-chain control, and technology differentiation. Advanced conductor and HVDC solutions deliver efficiency improvements of 10–20%, while localized production strategies reduce project lead times by nearly 15%. Global leaders compete through grid modernization technologies, digital monitoring platforms, and integrated EPC capabilities, whereas regional players emphasize procurement flexibility and lower installation costs. Strategic partnerships between utilities, equipment manufacturers, and engineering firms are becoming increasingly important as transmission projects grow in scale and complexity. The competitive landscape is shifting toward vertically integrated business models and digital grid solutions. Success increasingly depends on technology leadership, execution reliability, resilient supply chains, and the ability to support large-scale transmission modernization programs.

Hitachi Energy

Siemens Energy

GE Vernova

Prysmian Group

Nexans

Sumitomo Electric Industries

LS Cable & System

NKT A/S

Southwire Company

Sterlite Power

KEC International

Quanta Services

NR Electric Co., Ltd.

Toshiba Energy Systems & Solutions Corporation

Transmission line operators are increasingly deploying advanced conductors, digital substations, and real-time monitoring systems to improve network performance. High-temperature low-sag conductors increase transmission capacity by approximately 15–20% compared with conventional conductor technologies while reducing corridor expansion requirements. By 2026, more than 45% of newly approved grid modernization projects incorporate digital monitoring platforms that improve fault detection accuracy by nearly 10%. Utilities benefit through lower maintenance costs, higher asset utilization, and faster operational decision-making across large transmission networks.

Emerging technologies are shifting investment priorities toward intelligent and flexible transmission systems. Dynamic line rating solutions improve line utilization by 10–15% through continuous environmental monitoring, while AI-driven predictive maintenance reduces unplanned outages by approximately 20%. Digital twin technology is gaining adoption across major transmission operators, with deployment levels exceeding 25% among large utility modernization programs. Companies integrating these technologies achieve stronger grid reliability and operational efficiency, creating measurable advantages in project execution and infrastructure management.

Disruptive innovation is centered on HVDC transmission, grid analytics, and autonomous inspection systems. Modern HVDC networks reduce long-distance transmission losses by 30–40% compared with traditional HVAC alternatives. Drone-based inspections shorten asset assessment times by nearly 50%, improving maintenance productivity. Between 2026 and 2028, utilities, renewable developers, and transmission EPC firms that accelerate digital grid integration and HVDC deployment will strengthen competitive positioning as grid complexity, renewable penetration, and electricity demand continue increasing.

April 2025 – Hitachi Energy secured a contract for a ±800 kV, 6 GW, 950 km HVDC transmission system connecting Rajasthan and Uttar Pradesh in India, supporting renewable power evacuation and grid stability. The project strengthens long-distance transmission capabilities and large-scale renewable integration. Source: hitachienergy.com

March 2024 – Siemens Energy entered a strategic partnership with China's Huadian Group to expand collaboration in offshore wind power transmission, smart grid technologies, and low-carbon energy infrastructure. The agreement supports transmission network modernization and strengthens technology deployment across utility-scale projects. Source: reuters.com

March 2024 – Siemens Energy and BAM signed a major agreement with SSEN Transmission under the UK's Pathway to 2030 program to deliver critical transmission infrastructure supporting energy security and low-carbon power transport. The initiative targets network expansion through 2030 and strengthens transmission capacity development. Source: bam.com

October 2025 – Nexans reported a 27% increase in its transmission project backlog, driven primarily by subsea and power transmission infrastructure demand. The development reflects accelerating grid electrification investments and strengthens the company’s position in high-capacity transmission network deployment. Source: nexans.com

This report provides comprehensive analysis of the transmission line market across major infrastructure categories including Overhead Lines, Underground Lines, HVAC Lines, HVDC Lines, and Submarine Cables. The study evaluates key applications such as Power Transmission, Renewable Energy Integration, Grid Interconnection, Urban Electrification, and Industrial Power Supply while assessing demand patterns across Utility Companies, Power Generation Companies, Renewable Energy Developers, Government Agencies, Infrastructure Developers, and Industrial Facilities. The report examines deployment trends, technology adoption rates, infrastructure modernization activity, and evolving transmission network requirements across global markets.

The assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed country-level operational insights. More than 40% of market activity is concentrated in large-scale grid modernization and renewable integration projects, while digital monitoring, advanced conductors, and HVDC technologies continue expanding deployment. The report supports investment planning, competitive benchmarking, expansion strategies, partnership evaluation, technology prioritization, and long-term infrastructure decision-making across the 2026–2033 planning horizon.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 13561.56 Million |

|

Market Revenue in 2033 |

USD 19138.75 Million |

|

CAGR (2026 - 2033) |

4.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Hitachi Energy, Siemens Energy, GE Vernova, Prysmian Group, Nexans, Sumitomo Electric Industries, LS Cable & System, NKT A/S, Southwire Company, Sterlite Power, KEC International, Quanta Services, NR Electric Co., Ltd., Toshiba Energy Systems & Solutions Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |