Reports

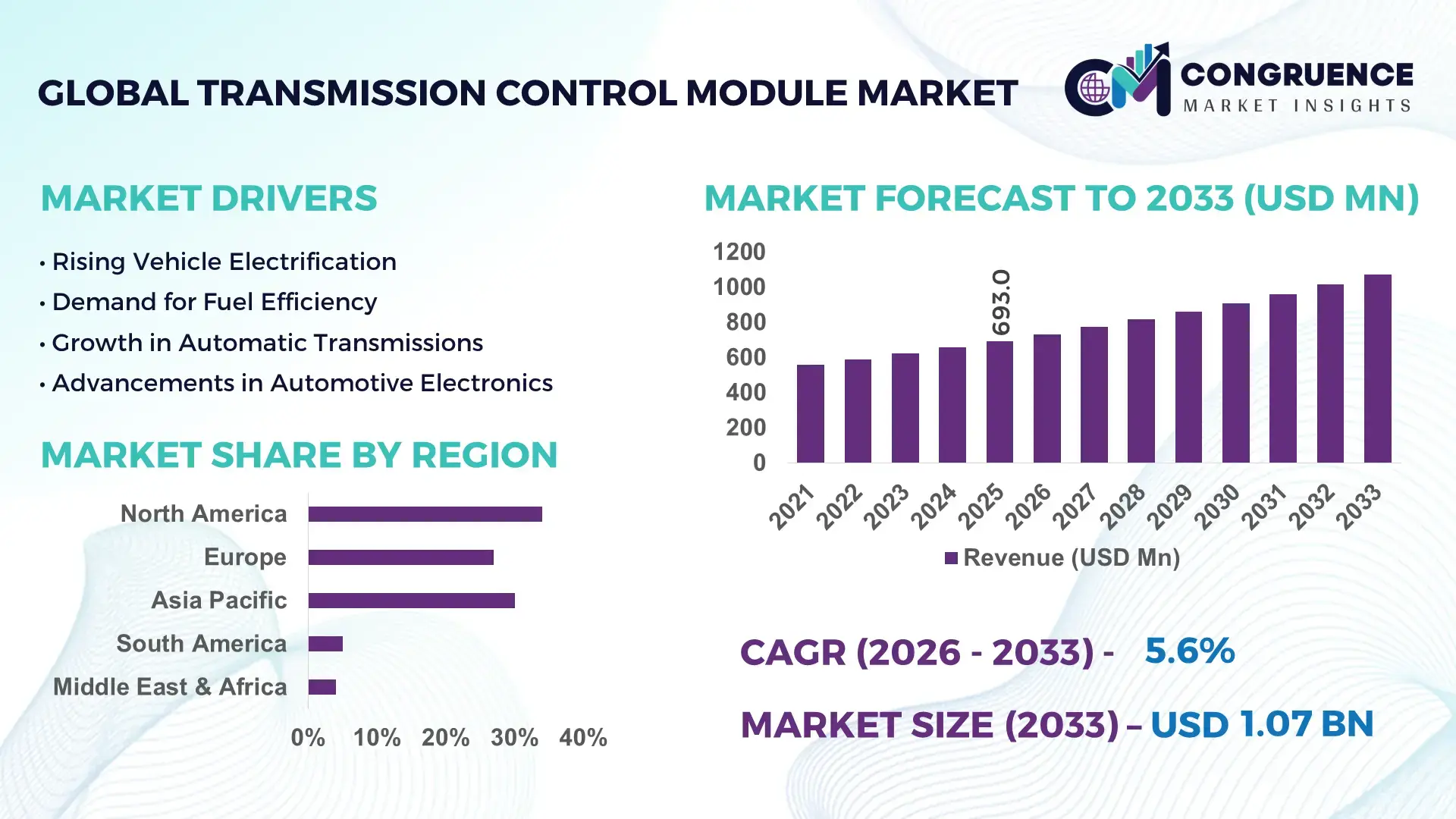

The Global Transmission Control Module Market was valued at USD 693.0 Million in 2025 and is anticipated to reach a value of USD 1,071.6 Million by 2033 expanding at a CAGR of 5.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market is expanding steadily due to rising electronic content per vehicle and the accelerating shift toward advanced automatic and hybrid transmission systems.

The United States remains the dominant country in the Transmission Control Module (TCM) Market, supported by annual vehicle production exceeding 10 million units and automotive electronics penetration above 40% of total vehicle component value. Over 65% of new passenger vehicles sold in the country are equipped with automatic transmissions, directly increasing TCM integration. Investments in automotive semiconductor manufacturing have surpassed USD 50 billion between 2022 and 2025, strengthening domestic ECU and module production capacity. Advanced driver-assistance system (ADAS) integration in over 60% of new vehicles further enhances demand for high-performance transmission control architectures.

Market Size & Growth: USD 693.0 Million in 2025, projected to reach USD 1,071.6 Million by 2033 at 5.6% CAGR, driven by 70%+ automatic transmission penetration in new vehicles globally.

Top Growth Drivers: 68% automatic vehicle adoption rate, 35% improvement in fuel efficiency via optimized shifting, 40% increase in hybrid vehicle production.

Short-Term Forecast: By 2028, AI-enabled shift calibration is expected to improve drivetrain efficiency by 18% and reduce maintenance incidents by 12%.

Emerging Technologies: AI-based adaptive shift algorithms, over-the-air (OTA) software updates, and integration with 48V mild-hybrid architectures.

Regional Leaders: North America projected at USD 340 Million by 2033 with high SUV adoption; Asia-Pacific at USD 410 Million driven by 55% passenger vehicle output; Europe at USD 250 Million supported by emission-focused transmission optimization.

Consumer/End-User Trends: Passenger vehicles account for over 60% of installations, while commercial fleet electrification adoption has risen by 22% since 2022.

Pilot or Case Example: In 2024, an OEM pilot program achieved 15% shift response improvement using AI-enhanced TCM calibration.

Competitive Landscape: Market leader holds approximately 24% share, followed by Bosch, Continental, Denso, ZF Friedrichshafen, and Aisin.

Regulatory & ESG Impact: Emission norms targeting 30% CO₂ reduction by 2030 are accelerating demand for precision shift-control electronics.

Investment & Funding Patterns: Over USD 6 billion invested globally in automotive electronics manufacturing upgrades since 2023.

Innovation & Future Outlook: Increasing consolidation of powertrain ECUs and software-defined vehicle platforms is shaping next-generation TCM integration.

Passenger vehicles contribute nearly 62% of installations, commercial vehicles 28%, and hybrid/electric platforms 10%. Advanced 8-speed and dual-clutch systems now represent over 45% of new transmission deployments. Regulatory pressure for 30% lower emissions and rising fuel-efficiency mandates are accelerating digital shift optimization. Asia-Pacific accounts for over 50% of global vehicle production, supporting sustained TCM demand. Future growth centers on AI-integrated calibration and software-defined vehicle architectures.

The Transmission Control Module Market plays a strategic role in automotive electrification, efficiency optimization, and vehicle intelligence integration. Modern vehicles rely heavily on precision-controlled transmissions to achieve fuel efficiency gains exceeding 20% compared to legacy hydraulic-only systems. AI-based adaptive shift control delivers 18% improvement in shift timing accuracy compared to conventional rule-based calibration standards.

North America dominates in volume production, while Europe leads in advanced adoption, with over 72% of new vehicles integrating electronically optimized multi-speed automatic transmissions. Asia-Pacific demonstrates the fastest production scaling, supported by high passenger vehicle assembly rates exceeding 30 million units annually.

By 2028, AI-driven predictive drivetrain diagnostics are expected to reduce unexpected transmission-related downtime by 25% across commercial fleets. ESG commitments are accelerating innovation, with automakers targeting 30% lifecycle emission reductions by 2030 through lightweight transmission systems and optimized electronic controls.

In 2024, a leading Japanese OEM implemented AI-enhanced TCM software upgrades that improved fuel economy by 14% across hybrid models. Over-the-air (OTA) updates reduced recall-related service visits by 20%.

Strategically, the Transmission Control Module Market is transitioning toward centralized domain controllers within software-defined vehicles. Integration with electrified powertrains, hybrid architectures, and real-time vehicle analytics positions the market as a pillar of operational resilience, regulatory compliance, and sustainable mobility transformation.

The Transmission Control Module Market dynamics are shaped by increasing vehicle electrification, automatic transmission penetration, and stringent emission standards. Over 75% of new passenger vehicles globally are equipped with automatic or semi-automatic transmissions, intensifying demand for electronic shift management. The proliferation of hybrid systems, which require synchronized powertrain coordination, further strengthens reliance on advanced TCM units.

Automotive electronics now account for nearly 40% of total vehicle manufacturing costs, compared to 18% two decades ago, underscoring the growing importance of embedded control systems. Semiconductor advancements, 32-bit microcontrollers, and integrated communication protocols such as CAN and LIN are redefining module architecture. Additionally, regulatory mandates targeting 25–35% emission reductions over the next decade are compelling OEMs to invest in precision-controlled drivetrain systems.

Global automatic vehicle penetration has surpassed 70% in developed markets and is expanding rapidly in emerging economies. Hybrid vehicle production increased by over 40% between 2021 and 2024, requiring advanced TCM systems for synchronized engine-motor power distribution. Modern 8-speed and 10-speed transmissions rely entirely on electronic control logic, improving fuel efficiency by up to 20% compared to traditional 5-speed systems. Additionally, dual-clutch transmissions reduce shift time by nearly 30%, demanding high-speed processing TCM hardware. Fleet operators adopting automated manual transmissions report 12–15% operational efficiency gains, reinforcing demand for advanced modules.

TCM units depend heavily on automotive-grade semiconductors, where supply shortages between 2021 and 2023 disrupted production across over 8 million vehicles globally. Advanced microcontrollers and power management chips account for nearly 35% of TCM component costs. Increasing integration with ADAS and hybrid systems raises R&D expenses by approximately 18% per platform upgrade. Smaller OEMs face barriers due to compliance testing requirements exceeding 1,000 validation hours per model. Additionally, cybersecurity compliance standards add nearly 10% additional development overhead to embedded control systems.

Software-defined vehicles (SDVs) are projected to represent over 50% of new vehicle platforms by 2030. Centralized computing reduces wiring complexity by 20% and enhances processing efficiency. Over-the-air updates can extend TCM software lifecycle by 5–7 years without hardware replacement. AI-based predictive analytics improves gear selection precision by 18%, while reducing maintenance events by 15%. Emerging EV platforms integrating multi-speed gearboxes are opening new electronic control segments, particularly in performance EVs where torque optimization improves acceleration by 10–12%.

With more than 60% of new vehicles connected via telematics, TCM cybersecurity risks have intensified. ISO 26262 functional safety compliance demands rigorous validation protocols exceeding 500 test scenarios per transmission type. Cybersecurity regulations require encrypted communication, increasing processor utilization by 8–12%. OTA-enabled modules must maintain 99.9% software integrity reliability, demanding redundant architecture. Compliance audits and homologation procedures can extend product launch cycles by 6–9 months, increasing development costs and slowing rapid deployment of next-generation modules.

AI-Driven Adaptive Shift Control Improving Efficiency by 18%: Automotive OEMs are deploying AI-based algorithms in TCM systems that enhance shift timing precision by 18% compared to fixed-rule calibration. Nearly 45% of premium vehicle models launched in 2024 feature adaptive learning transmission software. Fleet operators report 12% fuel savings after deploying AI-enabled shift optimization modules, while hybrid vehicles achieve 10% torque synchronization improvements.

Over-the-Air (OTA) Software Updates Reducing Service Visits by 20%: More than 60% of connected vehicles now support OTA powertrain software updates. OEM case studies show a 20% reduction in dealership service visits due to remote recalibration of transmission software. Update deployment time has decreased by 35%, improving customer satisfaction metrics by 15%.

Integration with Hybrid and 48V Architectures Growing 40% Annually: 48V mild-hybrid systems adoption has increased by 40% since 2022. These systems require integrated TCM-ECU coordination, reducing fuel consumption by up to 12%. Approximately 55% of European hybrid models now deploy electronically synchronized multi-speed transmissions.

Shift Toward Centralized Domain Controllers Reducing Wiring by 22%: Automotive manufacturers are consolidating standalone ECUs into domain controllers, reducing wiring harness complexity by 22% and lowering vehicle weight by 8%. Centralized transmission control improves data processing speed by 25% and enhances predictive maintenance accuracy by 17%, strengthening long-term reliability and system integration efficiency.

The Transmission Control Module Market is segmented by type, application, and end-user, reflecting the increasing complexity of automotive powertrain electronics. By type, the market spans standalone TCM units, integrated transmission control within powertrain control modules (PCM), and centralized domain-based controllers. Integration trends are accelerating as over 55% of newly launched vehicle platforms now adopt consolidated electronic architectures.

By application, passenger vehicles represent the most substantial installation base due to automatic transmission penetration exceeding 70% in developed economies. Commercial vehicles, including light-duty trucks and heavy-duty fleets, are rapidly integrating advanced shift logic to improve fuel efficiency by 10–15%. Hybrid and electric platforms require synchronized torque and regenerative coordination, expanding the need for high-performance control software.

From an end-user perspective, OEMs dominate demand generation, while Tier-1 suppliers are strengthening software development capabilities. Aftermarket retrofits and performance tuning segments remain niche but strategically relevant, especially in regions with high vehicle parc exceeding 250 million units.

The Transmission Control Module Market by type includes standalone TCM units, integrated PCM/TCM systems, and centralized domain controller-based transmission control systems. Standalone TCM units currently account for approximately 48% of adoption, widely used in mid-range and legacy automatic transmission vehicles due to modular replacement advantages and simplified validation cycles. Integrated PCM/TCM systems hold around 34% share, offering reduced wiring complexity and 15–20% weight optimization compared to discrete modules. However, centralized domain controller systems are rising fastest, projected to grow at a CAGR of 8.2%, supported by the shift toward software-defined vehicle (SDV) platforms and zonal electronic architectures. While standalone systems remain dominant due to compatibility with 6-speed and 8-speed automatic transmissions, integrated architectures are gaining preference in hybrid vehicles where synchronized engine-motor coordination improves shift precision by 18%. The remaining niche configurations, including performance-oriented programmable modules, collectively contribute nearly 18% of installations, particularly in motorsports and premium vehicles.

Passenger vehicles represent the leading application, accounting for approximately 62% of total installations, driven by high automatic transmission penetration and rising SUV production. Commercial vehicles hold about 28%, benefiting from automated manual transmission (AMT) adoption that improves fuel economy by 12–15%. Hybrid and electrified vehicle applications currently account for 10%, yet this segment is expanding fastest with a projected CAGR of 9.1%, fueled by increasing multi-speed EV gearbox deployment and torque vectoring optimization requirements. Passenger vehicles dominate due to global production volumes exceeding 60 million units annually. However, hybrid platforms are witnessing accelerated integration, expected to surpass 18% of installations by 2033 as electrified drivetrains expand. The remaining specialized applications, including performance and off-highway vehicles, contribute a combined 10–12%, serving construction and agricultural machinery segments. In 2025, more than 44% of fleet operators globally reported piloting predictive transmission diagnostics to minimize downtime. Additionally, over 58% of new hybrid vehicle buyers prefer models equipped with adaptive shift optimization features.

OEMs constitute the leading end-user segment, accounting for nearly 68% of total demand, as transmission control modules are factory-installed during vehicle assembly. Tier-1 automotive electronics suppliers contribute approximately 22%, primarily through system integration, software calibration, and component manufacturing. The aftermarket segment represents around 10%, focusing on replacement modules and performance upgrades in mature automotive markets. OEM integration dominates due to rising embedded electronics penetration exceeding 40% of vehicle manufacturing value. However, the fastest-growing end-user category is Tier-1 suppliers, expanding at a CAGR of 7.4%, driven by increased outsourcing of software development and domain controller manufacturing. The aftermarket segment remains strategically relevant in regions with vehicle fleets exceeding 15 years average age, particularly in North America and Europe. In 2025, over 52% of automotive OEMs globally reported investing in centralized powertrain control platforms to streamline ECU consolidation. Additionally, nearly 37% of independent repair centers have upgraded diagnostic tools to support OTA-enabled transmission software recalibration.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of7.9% between 2026 and 2033.

North America’s dominance is supported by automatic transmission penetration exceeding 75% of new vehicle sales and annual vehicle production of over 15 million units. Europe follows with approximately 27% share, driven by strong hybrid vehicle adoption where over 55% of new registrations in select markets include electrified drivetrains requiring advanced transmission control logic. Asia-Pacific holds nearly 30% share, supported by passenger vehicle production surpassing 35 million units annually, with China alone contributing more than 25 million units. South America represents about 5%, primarily concentrated in Brazil and Argentina, while the Middle East & Africa collectively account for 4%, driven by commercial fleet imports and infrastructure expansion. Electrification mandates, ECU consolidation trends, and over 60% connected vehicle penetration in developed economies are reshaping regional demand patterns.

North America holds approximately 34% of the global Transmission Control Module Market, supported by high SUV and pickup production volumes exceeding 8 million units annually. The automotive sector, commercial fleet operations, and performance vehicle segments are key demand drivers. More than 72% of new vehicles sold feature automatic or semi-automatic transmissions, ensuring strong OEM integration rates. Regulatory frameworks targeting 30% fleet-wide emission reduction by 2030 are accelerating adoption of electronically optimized transmission systems. Digital transformation trends include OTA-enabled software calibration, now integrated in over 65% of connected vehicles. A leading regional supplier has expanded silicon-carbide-based power control module production, improving drivetrain response time by 14%. Consumer behavior reflects strong preference for performance and towing capability, increasing demand for 8-speed and 10-speed electronically controlled transmissions. Fleet operators show 48% adoption of predictive maintenance tools to reduce downtime.

Europe accounts for nearly 27% of the global market share, with Germany, the UK, and France representing over 65% of regional installations. Hybrid vehicle registrations exceed 50% of new passenger car sales in several Western European markets, significantly boosting demand for synchronized transmission control modules. Regulatory oversight from sustainability-focused automotive frameworks compels OEMs to implement precision shift systems that reduce CO₂ emissions by up to 12%. Electrification mandates and Euro 7 emission readiness are pushing OEMs toward integrated domain controllers. Over 58% of new vehicles feature advanced multi-speed automatic or dual-clutch systems. A major European automotive technology firm recently introduced AI-driven TCM software capable of reducing shift shock by 16%, enhancing passenger comfort metrics. Consumers in this region prioritize fuel efficiency and environmental compliance, resulting in 60% preference for electrified drivetrains equipped with optimized control electronics.

Asia-Pacific contributes close to 30% of global market volume, ranking second in share but first in production growth momentum. China, Japan, and India collectively manufacture over 40 million vehicles annually, driving large-scale integration of electronic transmission systems. Manufacturing localization initiatives and semiconductor investments exceeding USD 70 billion across the region strengthen supply chain resilience. Nearly 62% of passenger vehicles in Japan feature CVT or electronically controlled automatic transmissions. Innovation hubs in China are advancing AI-based drivetrain software, improving torque optimization by 15%. A leading regional supplier has deployed next-generation 48V-compatible TCM platforms supporting hybrid expansion. Consumer trends show growing preference for compact SUVs and hybrid sedans, contributing to over 35% increase in electronically controlled transmission installations across emerging Southeast Asian markets.

South America accounts for roughly 5% of the global Transmission Control Module Market, with Brazil contributing nearly 60% of regional vehicle output, followed by Argentina. Annual vehicle production in the region exceeds 3 million units, with automatic transmission adoption approaching 45% of new passenger vehicles. Infrastructure upgrades and logistics sector expansion are increasing demand for automated manual transmissions in light commercial vehicles. Trade agreements within MERCOSUR encourage component localization, supporting regional electronics assembly growth. A regional automotive manufacturer recently upgraded production lines to incorporate electronically controlled 6-speed transmissions, improving fuel efficiency by 10%. Consumer demand is shifting toward fuel-efficient compact vehicles, while fleet operators demonstrate 28% higher adoption of predictive maintenance diagnostics compared to 2022 levels.

The Middle East & Africa region holds approximately 4% of global market share, with the UAE and South Africa leading demand. Commercial vehicle imports account for over 55% of electronically controlled transmission installations in the region. Oil & gas, construction, and logistics sectors drive fleet procurement, where automated transmissions improve fuel efficiency by 8–12%. Modernization initiatives in Gulf economies are accelerating connected vehicle adoption, now present in 40% of newly registered premium vehicles. A regional distributor partnership recently expanded ECU diagnostic capabilities across service centers, reducing maintenance turnaround time by 18%. Consumer behavior indicates preference for durable SUVs and utility vehicles, increasing multi-speed automatic transmission demand aligned with harsh climate performance requirements.

United States – 29% Market Share: The leadership is driven by high automatic vehicle penetration exceeding 75% and strong domestic OEM production capacity.

China – 24% Market Share: The growth is supported by annual vehicle production surpassing 25 million units and rapid hybrid vehicle integration across domestic manufacturers.

The Transmission Control Module Market is moderately consolidated, with the top five companies collectively accounting for approximately 58% of global market share. The competitive landscape includes more than 35 active global and regional competitors, ranging from Tier-1 automotive electronics suppliers to specialized ECU manufacturers. Market leaders differentiate through vertical integration, proprietary calibration software, and semiconductor partnerships.

Strategic initiatives between 2023 and 2025 have included over 20 publicly announced collaborations focused on software-defined vehicle (SDV) architecture and centralized domain controller development. Product innovation cycles have shortened to 18–24 months, compared to 36 months a decade ago, reflecting faster integration of AI-based shift logic and cybersecurity frameworks.

More than 60% of leading players are investing in 48V and hybrid-compatible TCM platforms to align with electrification targets. Mergers and technology licensing agreements have increased by nearly 15% year-over-year, primarily targeting embedded software capabilities. Competitive intensity is also influenced by semiconductor supply agreements, with long-term wafer contracts covering up to 70% of production requirements among top OEM suppliers. The market increasingly emphasizes OTA-enabled calibration, ISO 26262 compliance, and encrypted communication protocols, creating high entry barriers for smaller firms.

ZF Friedrichshafen AG

Aisin Corporation

Magna International Inc.

BorgWarner Inc.

Hitachi Astemo Ltd.

Valeo SA

Hyundai Mobis

Schaeffler AG

Mitsubishi Electric Corporation

Infineon Technologies AG

NXP Semiconductors N.V.

Aptiv PLC

Technological transformation within the Transmission Control Module Market is centered on software-defined vehicle platforms, AI-based calibration, and semiconductor miniaturization. Modern TCM units utilize 32-bit and 64-bit automotive-grade microcontrollers capable of processing over 300 million instructions per second, enabling real-time torque and shift optimization.

AI-driven adaptive shift algorithms enhance shift timing precision by up to 18%, improving fuel efficiency and drivetrain longevity. Over 65% of newly launched premium vehicles now integrate OTA-enabled TCM software updates, reducing physical recall interventions by nearly 20%.

Cybersecurity integration aligned with ISO/SAE 21434 standards is embedded in over 60% of new TCM architectures, incorporating encrypted CAN-FD communication and secure boot authentication. Transition toward centralized domain controllers reduces ECU count by approximately 20–25%, lowering wiring harness weight by up to 8%.

Electrification is another major technological catalyst. 48V mild-hybrid compatibility has increased by 40% since 2022, requiring advanced synchronization between battery management systems and transmission modules. Silicon carbide-based power electronics are improving energy efficiency by 10–12% in hybrid drivetrain control systems. Additionally, predictive maintenance analytics embedded within TCM firmware can reduce unexpected fleet downtime by 25%, enhancing commercial vehicle uptime and lifecycle performance.

• In June 2025, ZF Friedrichshafen AG entered a strategic partnership with a leading Indian commercial vehicle OEM to supply several thousand manual and automated 9-speed transmission systems — including advanced control and modular TCM-enabled solutions — at its Chakan manufacturing plant, supporting heavy-duty (over 25 t) truck applications with high torque (1500 Nm and beyond). Source: www.press.zf.com

• In May 2025, Bosch announced an expanded portfolio of software-defined vehicle solutions tailored for the Chinese automotive market, including customizable hardware and software control units that align with electrified powertrains and driver assistance control architectures, highlighting strong demand for integrated control systems. Source: www.boschmediaservice.hu

• On September 8, 2025 at IAA Mobility, Robert Bosch GmbH emphasized its role in enabling software-driven vehicle control, including integrated vehicle motion management systems that coordinate braking, steering, and powertrain electronics — signaling deeper emphasis on centralized control modules in modern automotive ECUs. Source: www.us.bosch-press.com

• In March 2025, Continental AG held its Annual Press Conference outlining strategic realignment and improvement in its Automotive Group sector performance, reinforcing the company’s focus on advanced control unit technologies and electronics segments as part of its value-creation strategy in a challenging automotive market. Source: www.continental.com

The Transmission Control Module Market Report provides comprehensive coverage across product types, applications, technologies, and geographic regions. The scope includes standalone TCM units, integrated PCM/TCM systems, and centralized domain controller-based transmission management platforms. It evaluates deployment across passenger vehicles, commercial vehicles, hybrid platforms, and performance vehicles, which collectively account for over 90% of electronically controlled transmission installations.

Geographically, the report analyzes five major regions and more than 20 key countries, representing over 95% of global automotive production volume. It examines automatic transmission penetration exceeding 70% in developed markets and hybrid adoption surpassing 50% in select European economies.

Technological coverage includes AI-enabled adaptive shift algorithms, 48V mild-hybrid integration, silicon carbide-based power electronics, OTA software calibration, and cybersecurity-compliant architectures aligned with ISO standards. The report also assesses supply chain dynamics involving over 35 global competitors and highlights semiconductor integration trends influencing module design.

In addition, the scope addresses regulatory compliance requirements, fleet modernization programs, predictive maintenance integration, and ECU consolidation trends reducing hardware complexity by up to 25%. The analysis is structured to support strategic decision-making, investment evaluation, technology benchmarking, and competitive positioning within the evolving automotive electronics ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 693.0 Million |

| Market Revenue (2033) | USD 1,071.6 Million |

| CAGR (2026–2033) | 5.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Bosch; Continental AG; Denso Corporation; ZF Friedrichshafen AG; Aisin Corporation; Magna International Inc.; BorgWarner Inc.; Hitachi Astemo Ltd.; Valeo SA; Hyundai Mobis; Schaeffler AG; Mitsubishi Electric Corporation; Infineon Technologies AG; NXP Semiconductors N.V.; Aptiv PLC |

| Customization & Pricing | Available on Request (10% Customization Free) |