Reports

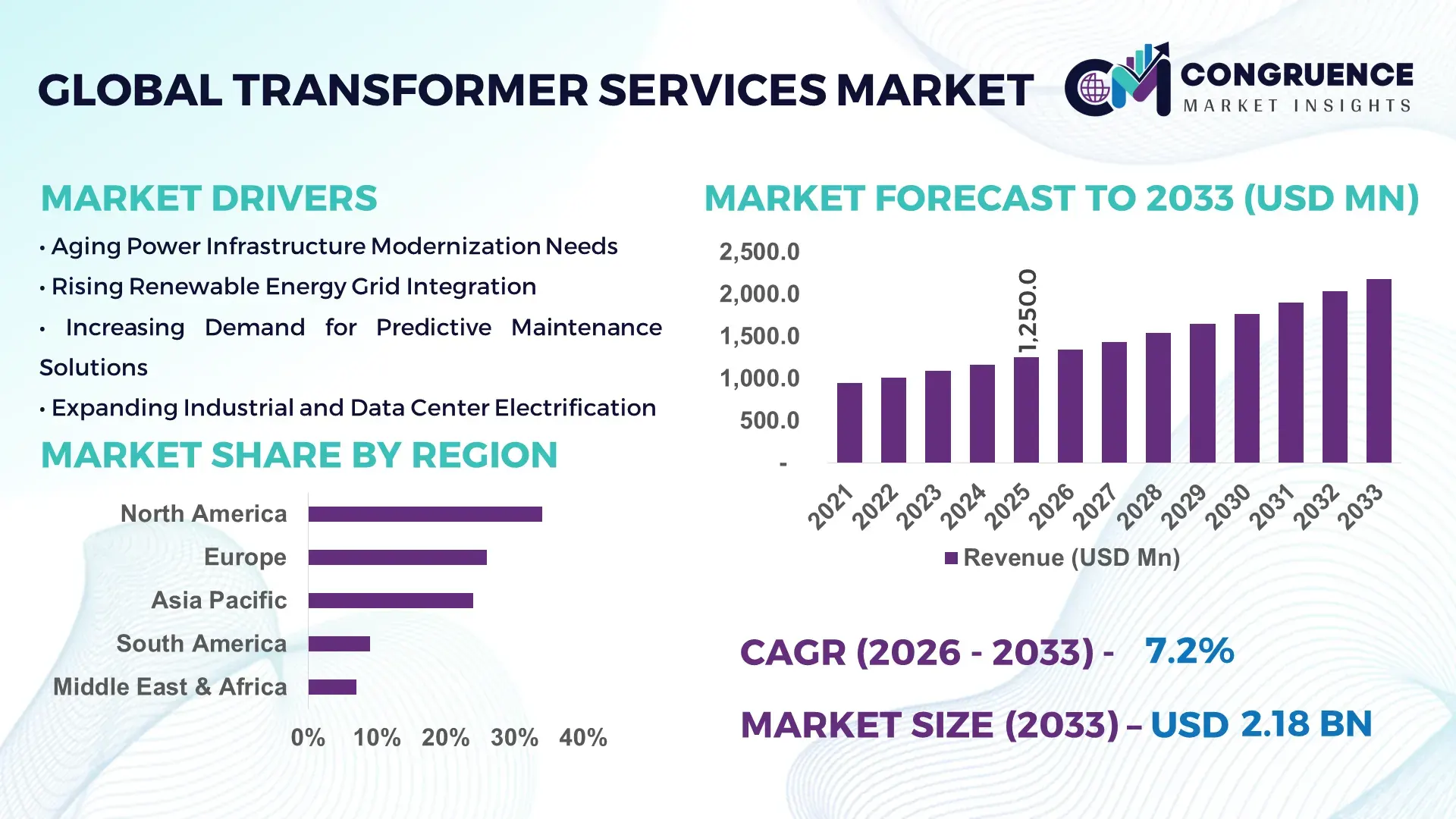

The Global Transformer Services Market was valued at USD 1,250.0 Million in 2025 and is anticipated to reach a value of USD 2,180.1 Million by 2033 expanding at a CAGR of 7.2% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by aging power infrastructure, grid modernization programs, and increasing renewable energy integration requiring continuous transformer maintenance and lifecycle management services.

The United States stands at the forefront of the Transformer Services Market with over 60% of its installed power transformers aged more than 25 years, creating sustained demand for refurbishment, oil testing, retrofitting, and predictive diagnostics. The country operates more than 7,000 utility-scale power plants and over 160,000 miles of high-voltage transmission lines, necessitating continuous service contracts. Annual grid modernization investments exceed USD 20 billion, with utilities increasingly adopting digital monitoring systems. Industrial sectors such as oil & gas, data centers, and manufacturing collectively account for over 45% of service demand, while smart grid deployments have surpassed 70 million smart meter installations, reinforcing transformer service requirements.

Market Size & Growth: Valued at USD 1,250.0 Million in 2025, projected to reach USD 2,180.1 Million by 2033, expanding at 7.2% CAGR between 2026 and 2033, driven by aging grid assets and renewable integration.

Top Growth Drivers: 65% aging infrastructure upgrades, 48% renewable grid interconnections, 37% increase in industrial electrification demand.

Short-Term Forecast: By 2028, predictive maintenance adoption is expected to reduce transformer downtime by 30% across utility networks.

Emerging Technologies: AI-based fault diagnostics, IoT-enabled condition monitoring sensors, and digital twin modeling for asset lifecycle optimization.

Regional Leaders: North America projected at USD 780 Million by 2033 with strong grid modernization; Asia-Pacific USD 720 Million driven by industrial expansion; Europe USD 410 Million supported by renewable grid compliance upgrades.

Consumer/End-User Trends: Utilities account for nearly 55% of service contracts, followed by industrial facilities at 30%, with long-term maintenance agreements rising 25% annually.

Pilot or Case Example: In 2024, a U.S. utility pilot integrating AI diagnostics achieved 28% reduction in unplanned outages and 18% maintenance cost savings.

Competitive Landscape: ABB holds approximately 16% share, followed by Siemens Energy, Schneider Electric, General Electric, and Mitsubishi Electric.

Regulatory & ESG Impact: Carbon neutrality targets mandate 40% grid efficiency improvements by 2030, accelerating transformer retrofits and eco-friendly insulation adoption.

Investment & Funding Patterns: Over USD 35 billion committed globally toward grid upgrades between 2023–2025, with rising public-private partnerships.

Innovation & Future Outlook: Integration of digital substations, remote diagnostics platforms, and biodegradable transformer oils shaping resilient and sustainable service ecosystems.

Utility applications contribute nearly 55% of total service demand, followed by heavy industry at 30% and renewable power plants at 15%. Digital oil analysis systems have improved fault detection accuracy by 35%, while eco-friendly ester-based insulating fluids are gaining 22% adoption in new retrofits. Regulatory mandates on grid reliability and emissions reduction are accelerating modernization, particularly in North America and Asia-Pacific, positioning lifecycle extension services as a core operational priority for utilities.

The Transformer Services Market holds strategic relevance as power infrastructure across developed and emerging economies faces accelerated aging and rising electrification loads. More than 40% of global transformers in operation today exceed 20 years of service life, intensifying demand for refurbishment, condition monitoring, and asset life-extension programs. Digital transformer monitoring systems now enable real-time diagnostics, reducing catastrophic failure risks by measurable margins. AI-driven predictive maintenance delivers 30% improvement compared to traditional time-based maintenance schedules, significantly lowering unplanned outage rates and operational expenditures.

North America dominates in volume due to extensive legacy grid networks, while Asia-Pacific leads in adoption with over 52% of utilities implementing smart monitoring platforms. By 2028, AI-enabled transformer health analytics are expected to cut emergency repair incidents by 25% across digitally enabled substations. Firms are committing to ESG metrics such as 35% reduction in transformer oil waste and 20% increase in recyclable component usage by 2030.

In 2024, a leading U.S. utility achieved 26% reduction in service response time through deployment of IoT-enabled transformer sensors and centralized analytics dashboards. Such measurable operational gains underscore the market’s transformation from reactive servicing to predictive asset management. Going forward, integration of digital twins, remote asset inspection drones, and smart grid automation will position the Transformer Services Market as a pillar of resilience, regulatory compliance, and sustainable energy infrastructure growth.

The Transformer Services Market dynamics are shaped by aging transmission infrastructure, expanding renewable integration, rising industrial electrification, and increasing regulatory scrutiny on grid reliability. Utilities worldwide are prioritizing preventive and predictive maintenance strategies to avoid large-scale outages, as transformer failures can account for up to 30% of substation downtime incidents. Growing renewable installations, which surpassed 3,500 GW globally, require step-up and distribution transformer servicing to ensure voltage stability. Industrial expansion in Asia-Pacific and data center proliferation in North America further intensify transformer loading cycles, increasing maintenance frequency. Additionally, digitization of substations and deployment of IoT sensors are transforming service models from manual inspection-based approaches to real-time condition-based monitoring frameworks.

Globally, more than 50% of installed power transformers are over two decades old, increasing susceptibility to insulation degradation, overheating, and oil contamination. In the United States alone, approximately 60% of large power transformers exceed 25 years in service. Aging equipment requires frequent oil analysis, bushings replacement, thermal imaging diagnostics, and complete refurbishments. Utilities report that preventive servicing can extend transformer life by 15–20 years, significantly reducing replacement frequency. Additionally, electrification growth in transport and industry has increased transformer load utilization rates by nearly 18% over the past decade. These structural factors collectively intensify scheduled maintenance cycles and long-term service agreements across transmission and distribution networks.

Comprehensive transformer refurbishment projects can cost up to 40% of a new transformer’s capital expense, creating budgetary pressures for utilities with constrained funding. Skilled labor shortages further increase operational costs, as certified high-voltage maintenance technicians remain limited in supply across several regions. Lead times for specialized components such as bushings and tap changers often exceed 6–9 months, delaying service execution. Additionally, utilities operating in remote areas face logistical expenses that raise service costs by nearly 15%. These financial and operational constraints may defer non-critical maintenance, limiting immediate service expansion despite long-term infrastructure needs.

Global renewable capacity additions surpassed 500 GW in a single year, requiring new grid interconnections and transformer installations. Each solar or wind farm requires step-up transformers and periodic insulation testing to maintain voltage consistency. Offshore wind installations alone are projected to increase maintenance demand by over 20% due to harsh marine environments. Energy storage systems integrated into substations further increase transformer cycling frequency, intensifying monitoring requirements. Digital substations equipped with IoT sensors can improve fault detection rates by 35%, presenting service providers with opportunities in data analytics, remote diagnostics, and lifecycle management contracts across rapidly expanding clean energy infrastructure.

Transformer servicing depends on specialized insulating oils, copper windings, and electronic monitoring modules, many of which experienced supply delays of 20–30% during recent global disruptions. High-voltage transformers above 400 kV require technically complex diagnostics and outage coordination, limiting the number of qualified service providers. Environmental regulations on oil disposal and hazardous waste handling add compliance costs of up to 12% per project. Additionally, unexpected load surges from renewable intermittency can accelerate component wear, complicating predictive maintenance accuracy. These operational and regulatory complexities require advanced planning and capital allocation, creating execution challenges for service vendors and utilities alike.

32% Increase in Predictive Maintenance Adoption: Utilities worldwide have reported a 32% rise in AI-based transformer monitoring deployments over the past three years. IoT-enabled dissolved gas analysis (DGA) systems now detect incipient faults with 35% higher accuracy compared to periodic manual testing. More than 45% of newly commissioned substations include remote monitoring dashboards, reducing on-site inspections by 28% and improving response time efficiency.

27% Growth in Renewable-Linked Service Contracts: Transformer service demand linked to solar and wind installations has expanded by 27%, driven by over 500 GW annual renewable additions. Offshore wind substations experience maintenance cycles 20% more frequently due to marine exposure, while battery-integrated grids increase transformer load variability by 18%, requiring advanced thermal management diagnostics.

22% Adoption of Eco-Friendly Insulating Fluids: Ester-based biodegradable transformer oils now account for 22% of retrofitted units in developed markets. These fluids reduce fire risk probability by 15% and extend insulation life expectancy by nearly 10%. Regulatory mandates targeting 30% hazardous waste reduction by 2030 are accelerating sustainable service retrofits.

30% Reduction in Downtime via Digital Substations: Digital substation integration has delivered up to 30% downtime reduction through automated alerts and condition-based maintenance scheduling. Over 50% of large utilities in North America and Europe are transitioning toward hybrid or fully digital asset management platforms, improving maintenance productivity by 25% and enabling centralized performance analytics across multi-site transformer fleets.

The Transformer Services Market is segmented by type, application, and end-user, each reflecting distinct operational priorities and infrastructure maturity levels. Service types range from routine maintenance and testing to advanced monitoring and full-scale refurbishment. Applications are concentrated across power generation, transmission, and distribution networks, with additional demand emerging from renewable integration and industrial electrification. End-user demand is primarily driven by utilities, followed by industrial facilities and renewable energy operators. Over 50% of installed transformers globally are more than 20 years old, influencing a higher share of maintenance and retrofitting services. Utilities increasingly favor long-term service agreements, with nearly 58% of grid operators adopting condition-based maintenance strategies. Meanwhile, digital monitoring penetration has crossed 45% among newly commissioned substations, reshaping service delivery models. Segmentation trends indicate a clear transition from reactive repair services to predictive, technology-driven lifecycle management across both developed and emerging economies.

Transformer services are categorized into maintenance & testing, repair & refurbishment, monitoring & diagnostics, and other specialized services such as oil management and spare parts replacement. Maintenance & testing currently account for approximately 38% of total service demand, driven by mandatory periodic inspections, dissolved gas analysis (DGA), and thermal imaging requirements across high-voltage assets. Repair & refurbishment hold around 27%, primarily supporting aging transformers exceeding 25 years of operation. However, monitoring & diagnostics services are expanding fastest, projected to grow at approximately 9.1% CAGR, fueled by digital sensor integration and AI-based predictive analytics that reduce unexpected failures by nearly 30%. Oil management, retrofilling with biodegradable fluids, and emergency breakdown services collectively contribute nearly 35% of the remaining segment share, serving niche yet critical operational needs. While traditional preventive maintenance remains dominant, utilities are shifting toward real-time diagnostics platforms to extend transformer lifespan by up to 20%.

In 2024, the U.S. Department of Energy reported expanded deployment of advanced grid monitoring technologies across multiple states, enabling real-time transformer condition assessment in over 200 substations and improving early fault detection accuracy by more than 25%.

By application, transmission & distribution (T&D) networks represent the largest segment, accounting for nearly 46% of service demand due to extensive grid infrastructure and high-voltage transformer concentration. Power generation facilities contribute around 24%, particularly thermal and hydroelectric plants requiring periodic transformer overhauls. Renewable energy integration applications currently account for approximately 18%, while industrial and commercial facilities collectively represent about 12%. While T&D networks lead in adoption, renewable energy applications are expanding fastest with an estimated 8.7% CAGR, driven by over 500 GW of annual renewable capacity additions and increased grid interconnections. Offshore wind substations require 20% more frequent servicing due to harsh environmental exposure. In 2025, nearly 41% of utilities globally reported piloting AI-enabled transformer analytics for renewable grid stability. Additionally, over 35% of large industrial operators have implemented predictive maintenance systems to minimize production downtime linked to transformer faults.

In 2024, the International Energy Agency highlighted large-scale grid reinforcement initiatives supporting renewable integration across more than 70 countries, accelerating demand for transformer testing and voltage stabilization services in high-capacity transmission corridors.

Utilities remain the dominant end-user segment, accounting for approximately 55% of total service contracts due to expansive transmission and distribution responsibilities. Industrial manufacturing facilities represent nearly 23%, including oil & gas, metals, mining, and heavy engineering sectors that rely on uninterrupted power supply. Renewable energy operators contribute about 15%, while commercial infrastructure and data centers make up the remaining 7%. Although utilities lead overall demand, renewable energy operators represent the fastest-growing end-user segment, expanding at approximately 9.4% CAGR as new solar and wind farms require specialized transformer servicing. Industrial facilities report that predictive maintenance adoption has reduced transformer-related production losses by 22%. In 2025, more than 38% of energy-intensive enterprises globally indicated deployment of digital monitoring systems to enhance asset reliability. Data center operators, managing facilities with power loads exceeding 50 MW, are increasingly adopting thermal diagnostics to ensure redundancy compliance.

In 2024, the U.S. Energy Information Administration noted continued expansion of utility-scale renewable plants integrated into transmission networks, prompting accelerated transformer inspection and lifecycle extension programs across major grid operators.

North America accounted for the largest market share at 34% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.9% between 2026 and 2033.

Europe followed with a 26% share, while Asia-Pacific held approximately 24%, South America 9%, and Middle East & Africa 7%. North America’s leadership is supported by more than 160,000 miles of high-voltage transmission lines and over 70 million installed smart meters. Europe operates cross-border interconnections exceeding 400 GW capacity, intensifying transformer monitoring demand. Asia-Pacific manages over 45% of global electricity consumption, with China and India adding more than 250 GW of combined grid capacity upgrades in recent years. In South America, Brazil alone accounts for nearly 55% of regional electricity generation capacity. Meanwhile, the Middle East & Africa region continues expanding substation capacity, with grid investments exceeding 20 GW annually across major energy-exporting economies.

North America holds approximately 34% share of the Transformer Services Market, driven by aging infrastructure and large-scale grid modernization initiatives. Over 60% of installed power transformers are older than 25 years, requiring systematic maintenance and refurbishment. Key demand drivers include utilities, oil & gas facilities, manufacturing plants, and hyperscale data centers exceeding 50 MW load capacity. Regulatory programs such as federal grid resilience funding and state-level clean energy mandates are accelerating transformer retrofits and digital monitoring deployments. Nearly 52% of utilities have integrated condition-based monitoring platforms to reduce unplanned outages by over 25%. Companies like General Electric are expanding digital transformer diagnostic solutions, deploying AI-enabled monitoring systems across multiple substations to enhance predictive accuracy. Regional consumer behavior indicates higher enterprise adoption of predictive analytics in energy-intensive sectors, with nearly 40% of industrial operators implementing asset health dashboards to ensure operational continuity.

Europe represents nearly 26% of the global market share, with Germany, the UK, and France leading in transformer servicing activities. The region’s energy transition strategy emphasizes grid reliability to integrate over 40% renewable power into electricity mixes across several countries. Regulatory frameworks under EU decarbonization initiatives require enhanced grid efficiency and emissions reduction targets by 2030, prompting retrofitting with biodegradable insulating fluids and advanced diagnostics. Approximately 48% of transmission operators have adopted remote monitoring solutions to ensure compliance with cross-border grid stability requirements. ABB, headquartered in Switzerland, continues investing in eco-efficient transformer retrofills and digital substation solutions across continental grids. European consumer behavior reflects strong regulatory compliance focus, where utilities prioritize explainable diagnostics, transparent maintenance reporting, and lifecycle sustainability metrics to meet strict environmental benchmarks.

Asia-Pacific accounts for around 24% of the global market share and ranks first in electricity consumption volume globally. China, India, and Japan are the top consuming countries, collectively operating thousands of gigawatts of installed generation capacity. Infrastructure expansion, including ultra-high-voltage (UHV) transmission lines exceeding 30,000 km in China, significantly boosts transformer servicing requirements. Industrial manufacturing growth and renewable capacity additions exceeding 500 GW annually further intensify service frequency. Mitsubishi Electric has enhanced smart transformer monitoring deployments across Japanese and Southeast Asian substations, improving operational diagnostics accuracy by nearly 28%. Regional consumer behavior indicates rapid digital adoption, with over 45% of utilities in developed Asia integrating IoT-based grid monitoring. Growth is driven by expanding urbanization, e-mobility infrastructure, and industrial automation demands across emerging economies.

South America holds approximately 9% of global market share, with Brazil and Argentina as leading contributors. Brazil alone accounts for more than half of regional electricity generation capacity, supported by hydroelectric infrastructure exceeding 100 GW. Ongoing grid reinforcement projects and renewable wind capacity expansions are increasing demand for transformer inspection and refurbishment services. Government-backed infrastructure financing programs and regional trade partnerships facilitate import of advanced diagnostic equipment. Local utilities are increasingly deploying condition-based maintenance strategies to reduce outage durations by nearly 18%. Regional consumer behavior is closely tied to energy reliability in mining and heavy industry sectors, where transformer downtime directly impacts export-driven production cycles. Industrial operators are progressively adopting oil analysis and thermal monitoring to prevent service interruptions in energy-intensive zones.

The Middle East & Africa region contributes about 7% of global market share, supported by oil & gas infrastructure, rapid urban construction, and expanding renewable projects. Major growth countries include the UAE and South Africa, where grid expansion projects exceed 15 GW combined annually. Utilities are modernizing substations with digital relay protection and online monitoring to improve outage response efficiency by nearly 20%. Regional trade partnerships and infrastructure investment programs support modernization of aging distribution networks. In the UAE, smart grid initiatives aim to integrate over 50% clean energy by 2050, necessitating advanced transformer diagnostics. Consumer behavior reflects growing reliance on uninterrupted industrial power supply, particularly in petrochemical complexes and mining operations, where preventive servicing programs are increasingly standardized.

United States – 29% Market Share: Strong transformer services demand supported by aging grid infrastructure exceeding 25 years in over 60% of installations and large-scale modernization investments.

China – 21% Market Share: High transformer services demand driven by ultra-high-voltage transmission expansion, large industrial base, and extensive renewable energy integration projects.

The Transformer Services Market exhibits a moderately fragmented competitive structure, with more than 120 active regional and global service providers operating across maintenance, refurbishment, monitoring, and lifecycle management domains. The top five companies collectively account for approximately 48% of total market share, indicating the presence of strong global leaders alongside numerous specialized regional contractors. Major multinational players leverage integrated service portfolios combining digital diagnostics, spare parts manufacturing, and long-term maintenance contracts, often spanning 5–15 years.

Competition is increasingly centered on digitalization capabilities, with over 55% of leading vendors offering AI-enabled predictive maintenance platforms integrated with IoT sensors. Strategic initiatives between 2023 and 2025 included more than 25 partnership agreements between utilities and technology providers to deploy digital substation monitoring systems. Mergers and acquisitions activity remains active, with at least 10 notable consolidation transactions recorded globally over the past two years aimed at strengthening transformer retrofitting and renewable grid servicing capabilities.

Vendors are investing heavily in eco-efficient technologies, including biodegradable insulating fluids and advanced dissolved gas analysis (DGA) tools, with digital monitoring accuracy improving by nearly 30% compared to legacy inspection methods. Market positioning increasingly depends on lifecycle extension expertise, rapid-response service networks covering over 80 countries, and compliance with evolving grid reliability standards. As utilities prioritize resilience and decarbonization, competitive differentiation is shifting from reactive repairs to predictive, performance-based service agreements supported by advanced analytics platforms.

General Electric

Mitsubishi Electric

Eaton Corporation

Toshiba Energy Systems & Solutions

Hyundai Electric

Hitachi Energy

WEG S.A.

CG Power and Industrial Solutions

SPX Transformer Solutions

Hyosung Heavy Industries

ERMCO (Electric Research and Manufacturing Cooperative)

SGB-SMIT Group

Technological advancement is fundamentally reshaping the Transformer Services Market, transitioning from manual inspection-driven models to predictive and analytics-based service ecosystems. Over 45% of newly commissioned substations globally now integrate digital monitoring platforms, enabling real-time transformer health assessment. Dissolved Gas Analysis (DGA) sensors equipped with IoT connectivity improve incipient fault detection accuracy by nearly 35%, significantly reducing catastrophic failure risks.

Artificial intelligence algorithms are increasingly applied to thermal modeling and load forecasting, delivering up to 30% improvement in maintenance planning accuracy compared to time-based schedules. Digital twin technology enables simulation of transformer behavior under fluctuating renewable loads, enhancing lifecycle optimization and reducing emergency repair incidents by approximately 20%. More than 50% of large utilities in developed markets have begun integrating centralized asset performance dashboards across multiple substations.

Eco-efficient insulation technologies are gaining prominence, with biodegradable ester-based fluids extending insulation lifespan by nearly 10% while lowering fire risk probability by 15%. Drone-assisted visual inspection systems reduce manual inspection time by approximately 40%, particularly for high-voltage transformers exceeding 400 kV. Furthermore, remote partial discharge monitoring solutions provide early anomaly detection across ultra-high-voltage networks spanning over 30,000 km in advanced grid systems.

Blockchain-based asset documentation and automated compliance reporting tools are also emerging, streamlining regulatory reporting cycles by 25%. As electrification expands and grid loads intensify, integration of AI-driven diagnostics, sensor fusion platforms, and cloud-based analytics is positioning transformer servicing as a data-centric, performance-driven infrastructure function rather than a reactive maintenance task.

• In September 2025, Hitachi Energy announced a historic investment of more than $1 billion USD to expand production of critical transformers and grid infrastructure in the United States, including a $457 million USD facility in South Boston, Virginia that will create over 800 jobs and strengthen domestic power transformer manufacturing capacity to support growing electricity demand. Source: www.hitachienergy.com

• In March 2025, Hitachi Energy expanded its global production commitment with an additional $250 million USD investment to address ongoing transformer shortages, strengthen key component manufacturing across the U.S., and support global electrification demand through 2027. Source: www.hitachienergy.com

• In September 2025, Hitachi Energy announced a $270 million CAD (≈ $195 million USD) expansion of its large power transformer manufacturing facility in Varennes, Quebec, Canada, aiming to nearly triple production capacity and create around 500 new jobs as part of its broader global manufacturing build-out. Source: www.hitachienergy.com

• In February 2024, Schneider Electric launched the EcoStruxure™ Transformer Expert service in the UK & Ireland to extend oil-transformer lifespans and reduce downtime through condition monitoring and risk assessment analytics, enhancing lifecycle management for utility and industrial customers. Source: www.se.com

The Transformer Services Market Report provides comprehensive coverage of service types including maintenance & testing, repair & refurbishment, monitoring & diagnostics, oil management, and emergency breakdown services. It evaluates application segments spanning transmission & distribution networks, power generation facilities, renewable energy integration sites, heavy industrial operations, and commercial infrastructure. The report examines more than 15 major national markets across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, collectively representing over 90% of global electricity infrastructure capacity.

Technological coverage includes AI-based predictive maintenance systems, IoT-enabled dissolved gas analysis tools, digital twin simulations, eco-friendly insulating fluids, and drone-assisted inspections. The study further analyzes asset age distribution, noting that over 50% of installed transformers globally exceed 20 years, influencing maintenance frequency and refurbishment demand. Regulatory landscapes covering grid reliability mandates, environmental compliance standards, and renewable interconnection requirements are incorporated into the assessment framework.

End-user analysis encompasses utilities, renewable energy operators, oil & gas companies, heavy manufacturing facilities, mining operations, and hyperscale data centers. The report also evaluates competitive dynamics among more than 100 active market participants, highlighting innovation strategies, partnership models, and geographic service coverage spanning over 80 countries. Additionally, emerging niches such as offshore wind transformer servicing, ultra-high-voltage diagnostics, and digital substation analytics are addressed, offering decision-makers a structured understanding of evolving service priorities and infrastructure modernization pathways within the Transformer Services Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,250.0 Million |

| Market Revenue (2033) | USD 2,180.1 Million |

| CAGR (2026–2033) | 7.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | ABB; Siemens Energy; Schneider Electric; General Electric; Mitsubishi Electric; Eaton Corporation; Toshiba Energy Systems & Solutions; Hyundai Electric; Hitachi Energy; WEG S.A.; CG Power and Industrial Solutions; SPX Transformer Solutions; Hyosung Heavy Industries; ERMCO (Electric Research and Manufacturing Cooperative); SGB-SMIT Group |

| Customization & Pricing | Available on Request (10% Customization Free) |