Reports

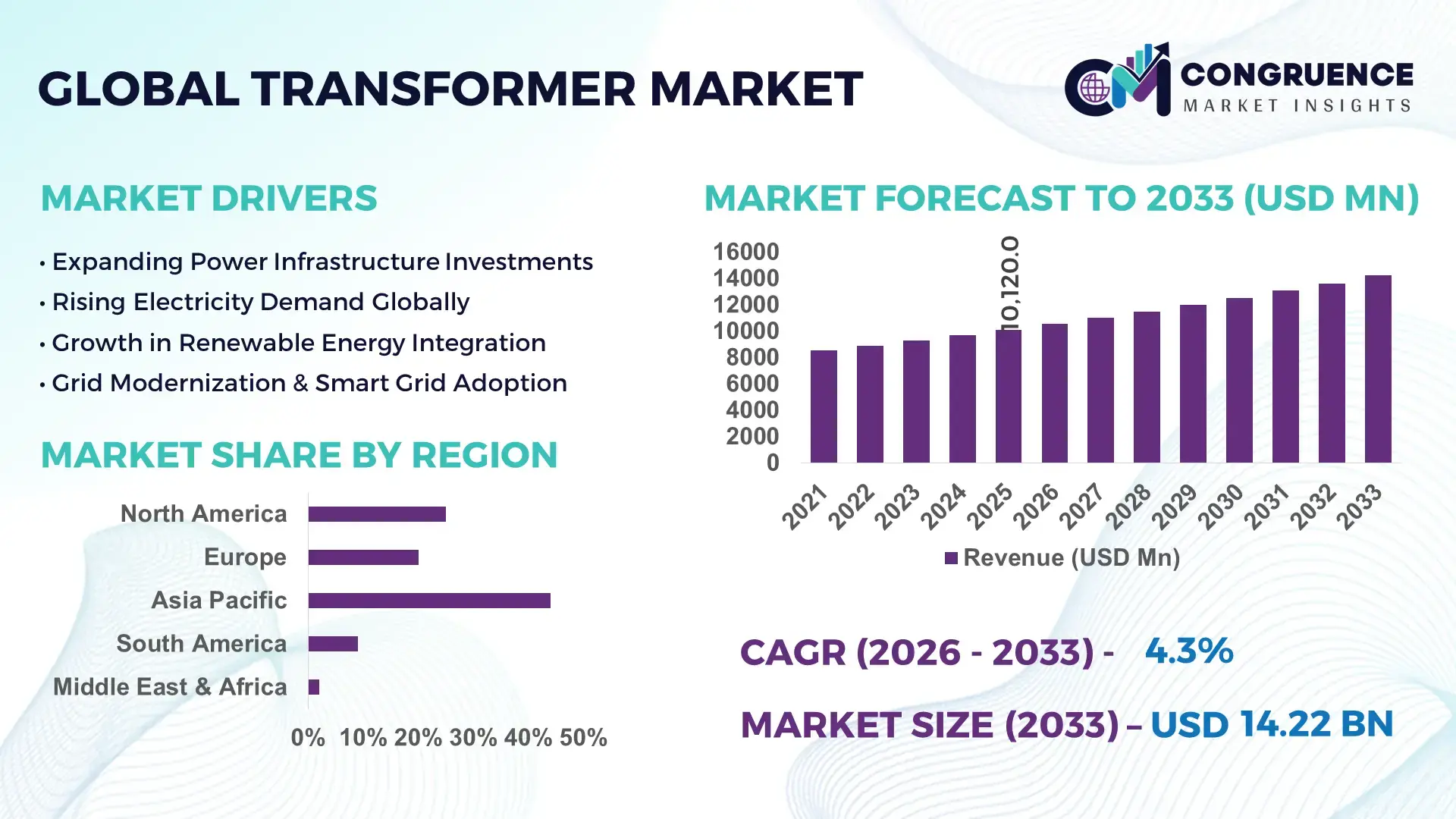

The Global Transformer Market was valued at USD 10120 Million in 2025 and is anticipated to reach a value of USD 14216.31 Million by 2033 expanding at a CAGR of 4.34% between 2026 and 2033. This growth is primarily driven by the accelerating expansion of power transmission and distribution infrastructure across developing and developed economies.

China continues to lead the transformer market with significant production capacity and large-scale grid modernization initiatives. The country manufactures over 40% of global power transformers annually, supported by strong domestic demand and export-oriented production. Investments exceeding USD 70 billion have been directed toward ultra-high-voltage (UHV) transmission networks, requiring advanced transformers with capacities above 1000 kV. Industrial applications, including renewable energy integration and heavy manufacturing, account for over 55% of transformer usage. Additionally, China’s smart grid deployment has surpassed 65% coverage in urban areas, accelerating the adoption of digitally monitored transformers with real-time diagnostics and predictive maintenance capabilities.

Market Size & Growth: USD 10120 Million in 2025, projected to reach USD 14216.31 Million by 2033, growing at 4.34% due to grid modernization and renewable energy integration.

Top Growth Drivers: Renewable energy adoption (35%), urban electrification expansion (28%), smart grid investments (22%).

Short-Term Forecast: By 2028, smart transformer deployment is expected to improve grid efficiency by 18% and reduce transmission losses by 12%.

Emerging Technologies: Digital transformers with IoT integration, solid-state transformers, AI-based predictive maintenance systems.

Regional Leaders: Asia-Pacific projected at USD 6200 Million by 2033 with infrastructure expansion; North America at USD 3200 Million driven by grid upgrades; Europe at USD 2800 Million with renewable integration focus.

Consumer/End-User Trends: Utilities account for over 60% usage, followed by industrial and commercial sectors adopting energy-efficient transformer solutions.

Pilot or Case Example: In 2024, a smart grid project in India achieved a 15% reduction in outage duration using AI-enabled transformers.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players including Siemens Energy, Hitachi Energy, General Electric, Schneider Electric, and Toshiba.

Regulatory & ESG Impact: Governments are mandating energy-efficient transformers with up to 20% lower losses and promoting eco-friendly insulating materials.

Investment & Funding Patterns: Over USD 50 billion invested globally in grid modernization projects, with rising public-private partnerships.

Innovation & Future Outlook: Increasing integration of digital monitoring, modular transformer designs, and hybrid energy systems is shaping long-term market evolution.

The transformer market is significantly influenced by power generation, transmission, and industrial sectors, which collectively account for over 70% of total demand. Technological innovations such as amorphous core transformers have reduced energy losses by up to 70% compared to conventional silicon steel cores. Environmental regulations promoting biodegradable insulating oils and reduced carbon emissions are reshaping manufacturing standards. Regionally, Asia-Pacific dominates consumption due to rapid electrification, while Europe focuses on sustainable energy integration. Emerging trends include the adoption of solid-state transformers, enhanced grid resilience solutions, and increased deployment in electric vehicle charging infrastructure, indicating a progressive shift toward smarter and more efficient power systems.

The transformer market holds strategic importance in ensuring reliable electricity distribution, supporting renewable energy integration, and enabling digital grid transformation. With global electricity demand expected to rise by over 25% by 2030, advanced transformer solutions are becoming critical for maintaining grid stability and efficiency. Smart transformers integrated with IoT sensors deliver up to 30% improvement in operational monitoring compared to traditional analog systems, allowing utilities to reduce maintenance costs and enhance asset lifespan.

Asia-Pacific dominates in volume due to extensive infrastructure projects, while North America leads in adoption with over 60% of utilities implementing digital transformer technologies. By 2028, AI-driven predictive maintenance is expected to reduce transformer failure rates by 20% and improve operational efficiency by 15%. Firms are committing to ESG targets, including reducing transformer energy losses by 25% and increasing the use of recyclable materials by 2030.

In 2024, India achieved a 12% reduction in transmission losses through the deployment of smart transformers under national grid modernization programs. Similarly, European utilities have reported up to 18% efficiency gains by integrating advanced monitoring systems. The market is also witnessing the adoption of solid-state transformers, which deliver 40% faster voltage regulation compared to conventional designs. The transformer market is evolving as a critical pillar of resilient energy infrastructure, enabling sustainable growth, regulatory compliance, and efficient power management across global economies.

The increasing adoption of renewable energy sources such as solar and wind power is a major driver of the transformer market. Renewable installations have grown by over 50% in the past five years, requiring specialized transformers capable of managing fluctuating power inputs. Grid-connected solar farms utilize step-up transformers to transmit electricity efficiently over long distances, while wind farms depend on high-capacity transformers for stable power conversion. The integration of distributed energy systems has increased demand for compact and efficient transformers in both urban and rural areas. Additionally, energy storage systems and hybrid grids are creating new requirements for advanced transformer technologies with enhanced load-handling capabilities. Governments are also incentivizing renewable energy projects, leading to increased deployment of transformers in both utility-scale and decentralized applications.

The transformer market faces significant constraints due to high capital investment and ongoing maintenance requirements. Large power transformers can cost upwards of several million dollars, making them a substantial financial commitment for utilities and industrial operators. Maintenance challenges, including insulation degradation and thermal stress, contribute to operational costs and downtime. Additionally, the complexity of installation, particularly in urban areas with space constraints, further increases expenses. Supply chain disruptions and fluctuating raw material prices, especially for copper and steel, have added cost pressures, with material costs rising by over 20% in recent years. These factors limit adoption, particularly in developing regions where budget constraints and infrastructure limitations hinder large-scale deployment of advanced transformer technologies.

The rapid expansion of smart grids presents significant opportunities for the transformer market. Smart grid technologies rely on digitally enabled transformers that provide real-time monitoring, fault detection, and automated control capabilities. Over 40% of global utilities are expected to adopt smart grid solutions by 2030, creating strong demand for intelligent transformer systems. These transformers enable improved energy efficiency, reducing transmission losses by up to 15% and enhancing grid reliability. Additionally, the rise of electric vehicles and charging infrastructure is driving demand for distribution transformers with higher load capacities. Emerging markets are investing heavily in digital grid infrastructure, offering untapped growth potential. The integration of artificial intelligence and data analytics further enhances operational efficiency, making smart transformers a key component of future energy systems.

The transformer market faces challenges related to stringent regulatory requirements and environmental concerns. Governments are enforcing strict energy efficiency standards, requiring manufacturers to develop transformers with lower losses and reduced environmental impact. Compliance with these regulations often involves higher production costs and extended development timelines. Additionally, the use of traditional insulating oils poses environmental risks, prompting a shift toward biodegradable alternatives, which are more expensive and less widely available. Disposal and recycling of aging transformers also present logistical and environmental challenges, as improper handling can lead to hazardous waste issues. Furthermore, the need to meet evolving international standards adds complexity for manufacturers operating in multiple regions. These factors collectively increase operational burdens and create barriers to market expansion.

• Accelerated Adoption of Digital and Smart Transformers Enhancing Grid Intelligence: Utilities are rapidly deploying digital transformers integrated with IoT and AI capabilities, with over 60% of newly installed transformers in developed markets featuring real-time monitoring systems. These advanced systems reduce unplanned outages by up to 25% and improve asset lifespan by nearly 30%. Grid operators are increasingly relying on predictive analytics, with fault detection accuracy improving by 40% compared to conventional systems. Additionally, smart transformer deployment in urban grids has increased by 35% over the last three years, supporting efficient load balancing and minimizing transmission losses.

• Surge in Renewable Energy-Linked Transformer Installations: The global push toward renewable energy integration has led to a 50% increase in transformer installations for solar and wind projects. Step-up transformers used in utility-scale solar farms have witnessed a 45% rise in demand, while offshore wind projects are driving a 38% increase in high-capacity transformer deployment. Renewable energy systems now account for approximately 30% of total transformer demand, reflecting a structural shift in power infrastructure. Enhanced transformer designs are enabling up to 20% better efficiency in handling variable power loads from intermittent energy sources.

• Rising Demand for Energy-Efficient and Eco-Friendly Transformer Designs: Regulatory mandates and ESG commitments are accelerating the adoption of energy-efficient transformers, with low-loss transformer installations growing by 28% globally. Amorphous core transformers, which reduce energy losses by up to 70%, are gaining traction, particularly in Asia-Pacific markets. Biodegradable insulating fluids are being adopted in over 22% of new installations, reducing environmental risk and improving safety standards. Manufacturers are also reporting a 15% improvement in thermal performance through advanced materials and cooling technologies.

• Expansion of Modular and Prefabricated Transformer Solutions in Infrastructure Projects: The adoption of modular and prefabricated transformer systems is reshaping project execution, with 55% of new infrastructure projects reporting cost savings and reduced installation timelines. Prefabricated transformer units enable up to 40% faster deployment compared to traditional on-site assembly. Demand for compact, high-efficiency transformers has increased by 33% in urban and industrial applications where space optimization is critical. Europe and North America are leading this trend, with over 45% of large-scale grid projects incorporating modular transformer solutions to enhance operational flexibility and scalability.

The transformer market segmentation is primarily structured across type, application, and end-user categories, each contributing distinctively to overall industry performance. By type, power transformers dominate due to their critical role in long-distance electricity transmission, while distribution transformers support widespread electrification at the local level. Instrument transformers, though smaller in share, are essential for measurement and protection systems. In terms of application, power generation and transmission sectors collectively account for over 65% of total deployment, driven by increasing electricity demand and grid expansion. Industrial applications contribute significantly, particularly in manufacturing and energy-intensive sectors. From an end-user perspective, utilities remain the largest consumers, representing more than 60% of total demand, followed by industrial and commercial sectors. Regional consumption patterns highlight strong adoption in Asia-Pacific due to infrastructure growth, while North America and Europe emphasize modernization and efficiency upgrades. This structured segmentation reflects evolving energy needs and technological advancements shaping transformer deployment globally.

The transformer market by type includes power transformers, distribution transformers, and instrument transformers, each serving specific roles in the electricity value chain. Power transformers hold the leading position, accounting for approximately 48% of total adoption, primarily due to their extensive use in high-voltage transmission networks and large-scale renewable energy projects. Distribution transformers follow with nearly 35% share, enabling efficient electricity delivery to residential and commercial users. Instrument transformers, including current and voltage transformers, collectively contribute around 17%, playing a crucial role in monitoring and protection systems. While power transformers dominate in volume, distribution transformers are emerging as the fastest-growing segment, expanding at an estimated CAGR of 5.2%, driven by rapid urbanization, rural electrification, and increasing electricity consumption in emerging economies. Compact designs and improved efficiency standards are further accelerating their adoption.

Other specialized transformer types, including isolation and auto-transformers, collectively account for about 12% of niche applications, particularly in industrial and commercial settings where voltage regulation and safety are critical.

The transformer market by application is categorized into power generation, transmission and distribution, industrial, and commercial applications. Transmission and distribution represent the leading application segment, accounting for approximately 52% of total usage, as expanding grid infrastructure and cross-border electricity networks require robust transformer deployment. Power generation applications contribute around 28%, driven by the increasing integration of renewable energy sources such as solar and wind. Industrial applications, including manufacturing, oil and gas, and mining, account for nearly 12% of transformer demand, while commercial applications contribute approximately 8%, supporting infrastructure such as data centers and commercial buildings.

Among these, renewable energy integration within power generation is the fastest-growing application, with an estimated CAGR of 6.1%, supported by global investments in clean energy and decentralized power systems. The rise of electric vehicle charging infrastructure is also boosting transformer demand in both industrial and commercial sectors.

The transformer market by end-user is dominated by utilities, industrial enterprises, commercial establishments, and residential sectors. Utilities represent the largest segment, accounting for approximately 62% of total adoption, due to their responsibility for power generation, transmission, and distribution infrastructure. Industrial users follow with nearly 20% share, driven by high electricity consumption in sectors such as manufacturing, chemicals, and heavy engineering. Commercial end-users, including data centers, hospitals, and office complexes, contribute around 10%, while residential applications account for approximately 8%, primarily through distribution networks. The fastest-growing end-user segment is the commercial sector, expanding at an estimated CAGR of 6.5%, fueled by the rapid growth of data centers and digital infrastructure. Data centers alone have increased transformer demand by over 25% in the past three years due to rising cloud computing and digital services.

Other emerging end-users, including electric vehicle charging networks and renewable energy developers, collectively account for nearly 15% of evolving demand, reflecting diversification in transformer applications.

Region Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

Asia-Pacific’s dominance is supported by large-scale electrification projects and grid expansion, with over 65% of new transformer installations occurring in China, India, and Southeast Asia. North America, holding approximately 24% share, is witnessing rapid modernization of aging grid infrastructure, with over 70% of utilities investing in smart grid technologies. Europe accounts for nearly 20% of the global transformer market, driven by renewable energy integration and strict energy efficiency regulations, with more than 55% of installations focused on eco-efficient transformers. South America contributes around 6%, supported by hydropower and rural electrification programs, while the Middle East & Africa region holds close to 4%, with increasing investments in power infrastructure and urban development. Across regions, digital transformer adoption has surpassed 40% in developed markets, while emerging economies are seeing over 30% annual growth in distribution transformer installations, reflecting strong global demand diversification.

How are advanced grid modernization initiatives reshaping demand patterns across industrial power networks?

North America holds approximately 24% of the global transformer market, driven by extensive investments in upgrading aging electrical infrastructure. Key industries such as utilities, data centers, and renewable energy projects account for over 65% of regional demand. Regulatory frameworks emphasizing energy efficiency, including mandates requiring up to 20% reduction in transformer losses, are accelerating the adoption of advanced technologies. Smart transformers equipped with IoT sensors now represent over 58% of new installations, enhancing real-time monitoring and predictive maintenance capabilities. Digital transformation trends have improved operational efficiency by nearly 18% across utility networks. A notable regional player has focused on expanding production of high-efficiency transformers, increasing output capacity by 25% to meet rising demand. Consumer behavior in this region reflects strong enterprise-level adoption, particularly in sectors such as healthcare and finance, where uninterrupted power supply and reliability are critical performance requirements.

What role do sustainability mandates play in accelerating innovation across energy infrastructure systems?

Europe accounts for nearly 20% of the transformer market, with Germany, the United Kingdom, and France leading in deployment and technological advancement. Over 60% of transformer installations in the region are aligned with renewable energy projects, particularly offshore wind and solar power integration. Regulatory bodies have introduced strict energy efficiency standards, pushing manufacturers to develop transformers with up to 25% lower energy losses. The adoption of biodegradable insulating fluids has increased by 30%, reflecting strong environmental compliance requirements. Digital transformer solutions are gaining traction, with more than 50% of utilities implementing advanced monitoring systems. A leading regional manufacturer has introduced eco-efficient transformers with enhanced cooling systems, improving performance by 15%. Consumer behavior in Europe is strongly influenced by regulatory pressure, resulting in high demand for energy-efficient and environmentally sustainable transformer technologies.

How is rapid industrial expansion influencing large-scale electrification and power distribution systems?

Asia-Pacific dominates the global transformer market in terms of volume, accounting for over 46% of total consumption. China, India, and Japan are the top consuming countries, collectively contributing more than 70% of regional demand. Massive infrastructure investments, including over 100,000 km of new transmission lines, are driving transformer deployment across urban and rural areas. Manufacturing output in the region has increased by 35% over the past five years, supported by strong domestic production capabilities. Technological advancements include widespread adoption of smart grid systems, with digital transformer penetration exceeding 40% in urban centers. A key regional player has expanded its manufacturing facilities, increasing annual production capacity by 20% to meet both domestic and export demand. Consumer behavior in Asia-Pacific is largely driven by rapid urbanization, industrial growth, and increasing electricity consumption across residential and commercial sectors.

What infrastructure modernization trends are shaping energy distribution efficiency across emerging economies?

South America represents approximately 6% of the global transformer market, with Brazil and Argentina as key contributors. The region’s demand is heavily influenced by hydropower generation, which accounts for nearly 45% of electricity production, requiring efficient transformer systems for transmission. Infrastructure development projects have increased transformer installations by 22% over the past three years. Government incentives promoting rural electrification and renewable energy adoption are further boosting demand. Trade policies supporting local manufacturing have led to a 15% increase in domestic transformer production capacity. A regional manufacturer has focused on developing cost-effective transformers tailored for rural applications, improving energy access in remote areas. Consumer behavior in this region is closely tied to infrastructure expansion and localized energy needs, with a growing emphasis on reliable and affordable power distribution solutions.

How are energy diversification and large-scale construction projects driving advanced power solutions?

The Middle East & Africa region holds around 4% of the global transformer market, with significant growth driven by oil and gas, construction, and renewable energy sectors. Countries such as the UAE and South Africa are leading in infrastructure investments, with over 30% of new projects focused on energy diversification. Transformer demand has increased by 18% due to large-scale urban development and industrial expansion. Technological modernization is evident through the adoption of digital monitoring systems, with approximately 35% of new installations incorporating smart technologies. Regional trade partnerships have facilitated a 20% increase in transformer imports to support infrastructure projects. A local player has introduced high-capacity transformers designed for extreme environmental conditions, improving operational reliability by 12%. Consumer behavior reflects a strong focus on large-scale industrial applications and long-term infrastructure resilience.

China – 32% share in the Transformer market, supported by large-scale manufacturing capacity and extensive grid infrastructure expansion.

United States – 18% share in the Transformer market, driven by advanced grid modernization initiatives and high demand from utilities and data centers.

The transformer market exhibits a moderately consolidated competitive structure, with the top five companies accounting for approximately 45% of the total market share. Over 120 active global and regional players operate within the industry, ranging from large multinational corporations to specialized local manufacturers. Market leaders are focusing on strategic initiatives such as mergers, acquisitions, and partnerships to strengthen their technological capabilities and geographic presence. For instance, recent collaborations between technology providers and utilities have improved transformer efficiency by up to 20% through digital integration.

Product innovation remains a key competitive factor, with over 35% of new product launches centered on smart transformers and eco-efficient designs. Companies are increasingly investing in research and development, allocating nearly 8% of their annual budgets toward advanced materials and digital technologies. The rise of modular transformer solutions has intensified competition, with manufacturers reporting a 25% increase in demand for compact and prefabricated units.

Additionally, regional players are gaining traction by offering cost-effective solutions tailored to local requirements, particularly in emerging markets. Competitive differentiation is also driven by after-sales services, predictive maintenance solutions, and lifecycle management offerings, which have improved customer retention rates by over 15%. Overall, the competitive landscape is evolving rapidly, with innovation and digital transformation shaping long-term market positioning.

Siemens Energy

Hitachi Energy

General Electric

Schneider Electric

Toshiba Corporation

Mitsubishi Electric Corporation

Hyundai Electric & Energy Systems

Bharat Heavy Electricals Limited

CG Power and Industrial Solutions

Eaton Corporation

ABB Ltd

Fuji Electric Co., Ltd.

Technological advancements are significantly transforming the operational efficiency, reliability, and sustainability of the transformer market. One of the most impactful innovations is the integration of digital monitoring systems, with over 60% of newly installed transformers in developed regions now equipped with IoT-enabled sensors. These systems enable real-time data collection on temperature, load conditions, and insulation health, improving fault detection accuracy by up to 40% and reducing maintenance costs by nearly 25%. Predictive maintenance powered by artificial intelligence is further enhancing asset lifecycle management, extending transformer lifespan by approximately 20%.

Solid-state transformer (SST) technology is emerging as a disruptive innovation, offering up to 35% reduction in size and weight compared to conventional transformers. SSTs also enable faster voltage regulation, improving grid responsiveness by nearly 40%, making them particularly suitable for renewable energy integration and electric vehicle charging infrastructure. Additionally, high-efficiency core materials such as amorphous steel are gaining traction, reducing no-load losses by up to 70% compared to traditional silicon steel cores.

Eco-friendly insulating materials are another key technological trend, with biodegradable insulating fluids now used in over 25% of new installations to minimize environmental impact. Advanced cooling technologies, including forced air and liquid cooling systems, have improved thermal performance by approximately 15%, enabling higher load capacities and operational stability.

Furthermore, the adoption of modular and prefabricated transformer solutions is accelerating, with deployment times reduced by up to 40%. Digital twin technology is also being implemented by over 30% of utilities, allowing virtual simulation of transformer performance and enabling proactive decision-making. These innovations collectively position the transformer market toward enhanced efficiency, sustainability, and intelligent grid integration.

• In March 2025, Hitachi Energy announced the expansion of its transformer manufacturing facility in India, increasing production capacity by over 20% to meet rising demand for grid modernization and renewable energy integration. The expansion focuses on high-voltage and eco-efficient transformers. Source: www.hitachienergy.com

• In October 2024, Siemens Energy launched a new range of blue transformers utilizing clean air insulation technology, eliminating the use of SF6 gas. These transformers reduce greenhouse gas emissions by up to 100% and support sustainable grid infrastructure development. Source: www.siemens-energy.com

• In June 2025, ABB Ltd introduced advanced digital distribution transformers equipped with integrated IoT sensors and cloud-based monitoring systems, improving operational efficiency by 15% and reducing downtime through predictive maintenance capabilities. Source: www.abb.com

• In January 2024, Toshiba Corporation developed a next-generation power transformer with enhanced insulation materials, achieving a 10% improvement in energy efficiency and improved resistance to extreme weather conditions, supporting grid resilience initiatives. Source: www.global.toshiba

The Transformer Market Report provides a comprehensive analysis of the global industry, covering multiple dimensions including product types, applications, end-user industries, and regional dynamics. The report evaluates key transformer categories such as power transformers, distribution transformers, and instrument transformers, which collectively account for over 90% of market deployment across transmission and distribution networks. It also includes emerging segments such as solid-state transformers and smart digital transformers, which are gaining traction due to increasing demand for intelligent grid solutions.

From an application perspective, the report examines power generation, transmission and distribution, industrial operations, and commercial infrastructure, with transmission and distribution accounting for more than 50% of total usage. The study further explores end-user segments including utilities, industrial enterprises, commercial establishments, and residential sectors, highlighting that utilities contribute over 60% of overall demand.

Geographically, the report spans key regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, capturing diverse consumption patterns and infrastructure development trends. Asia-Pacific alone represents over 45% of global transformer deployment, driven by rapid urbanization and industrial expansion.

Additionally, the report covers technological advancements such as IoT-enabled transformers, AI-driven predictive maintenance, eco-efficient materials, and modular designs. It also addresses regulatory frameworks, environmental considerations, and investment trends shaping the industry. With detailed segmentation and data-driven insights, the report serves as a strategic resource for stakeholders seeking to understand market dynamics, identify growth opportunities, and make informed business decisions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.34% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens Energy, Hitachi Energy, General Electric, Schneider Electric, Toshiba Corporation, Mitsubishi Electric Corporation, Hyundai Electric & Energy Systems, Bharat Heavy Electricals Limited , CG Power and Industrial Solutions, Eaton Corporation, ABB Ltd, Fuji Electric Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |