Reports

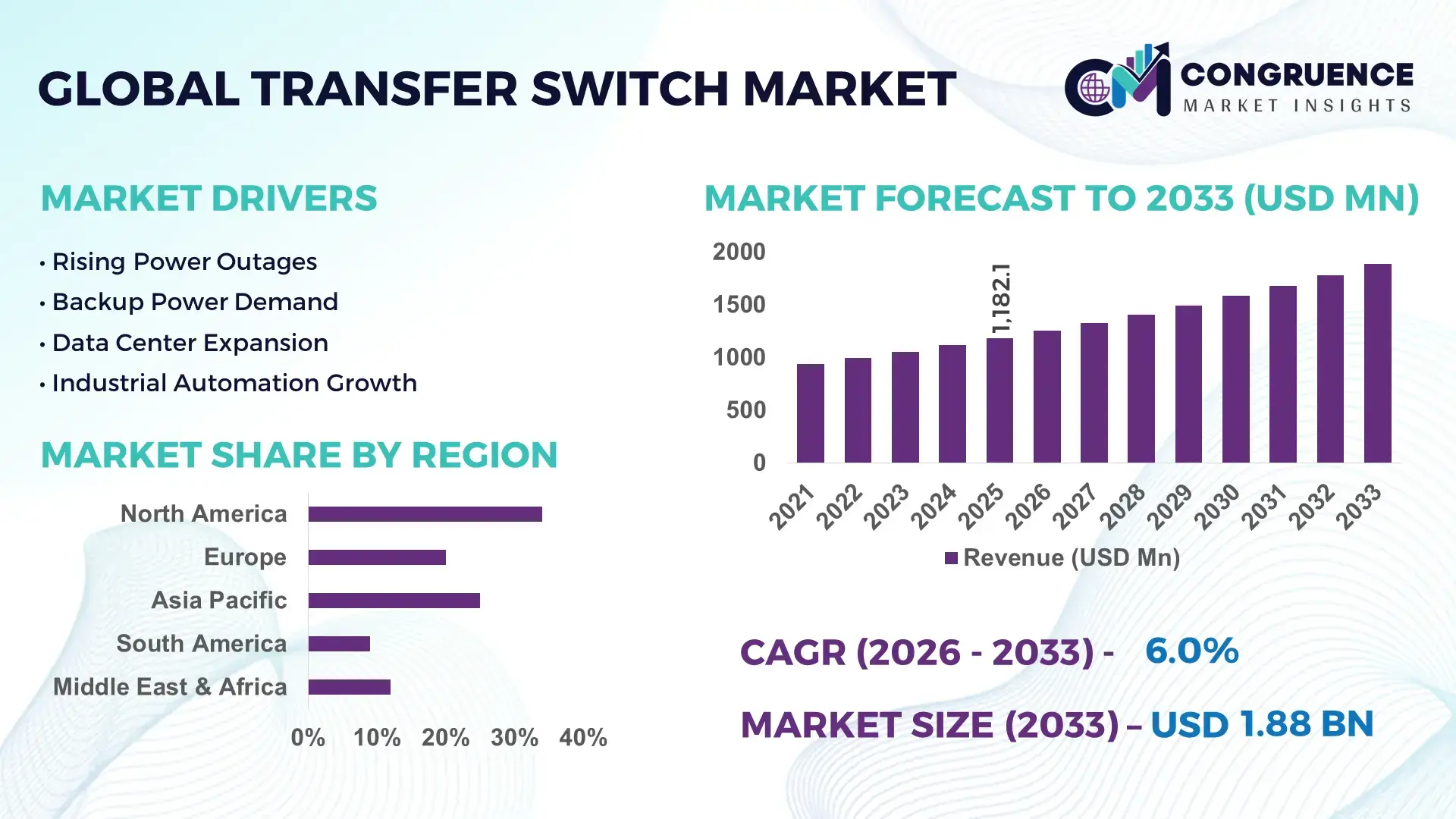

The Global Transfer Switch Market was valued at USD 1182.13 Million in 2025 and is anticipated to reach a value of USD 1884.15 Million by 2033 expanding at a CAGR of 6% between 2026 and 2033.

Rising grid instability and the rapid expansion of distributed energy systems are accelerating demand for advanced transfer switches, with automated switching solutions improving power continuity efficiency by over 30% compared to manual systems. The 2024–2026 period is defined by energy resilience policies and infrastructure modernization, particularly influenced by geopolitical energy disruptions and grid security investments across North America and Asia-Pacific.

The United States dominates the global transfer switch market with an estimated 32% share, supported by large-scale investments exceeding USD 18 billion in grid resilience and backup power infrastructure. Industrial sectors such as data centers, healthcare, and manufacturing account for over 55% of national demand, with automatic transfer switch adoption exceeding 68% in mission-critical applications. In comparison, China holds approximately 27% share, driven by rapid industrial electrification and smart grid expansion, while India is emerging with over 12% annual capacity additions in backup power systems due to frequent grid variability.

Automatic transfer switches now represent nearly 62% of installations globally, compared to 38% for manual systems, reflecting a clear shift toward automation and reliability. This structural transition, combined with rising electrification intensity, is positioning the market as a critical component in energy security strategies. Businesses must align investments toward intelligent switching solutions to remain competitive in an increasingly resilience-driven power ecosystem.

Market Size & Growth: USD 1182.13M (2025) to USD 1884.15M (2033) at 6% CAGR, driven by rising demand for automated power backup in data centers and industrial operations.

Top Growth Drivers: Grid instability (+28%), data center expansion (+35%), renewable integration (+22%) are accelerating adoption globally.

Short-Term Forecast: By 2028, automated transfer switch deployment increases system uptime by 25% while reducing downtime costs by 18%.

Emerging Technologies: AI-enabled monitoring, IoT-integrated switches, and predictive maintenance systems improve operational efficiency by 20–30%.

Regional Leaders: North America (~USD 520M) leads in automation adoption; Asia-Pacific (~USD 610M) drives volume growth; Europe (~USD 390M) advances smart grid integration.

Consumer/End-User Trends: Over 68% of industrial facilities and 72% of data centers prefer automatic transfer switches for uninterrupted operations.

Pilot/Case Example: In 2025, a hyperscale data center project improved power reliability by 32% using intelligent transfer switching systems.

Competitive Landscape: Top players hold ~45% combined share, with leading companies focusing on digital switchgear and modular solutions.

Regulatory & ESG Impact: Energy efficiency mandates reduce operational losses by 15% while accelerating adoption of low-emission backup systems.

Investment & Funding: Over USD 2.5B invested in grid resilience and backup power technologies, with strong focus on regional expansion and smart infrastructure.

Innovation & Future Outlook: Next-gen hybrid transfer switches and cloud-based diagnostics are reshaping competitive positioning and enabling 24/7 energy continuity.

Industrial applications contribute nearly 48% of total demand, followed by commercial infrastructure at 32% and residential usage at 20%, reflecting strong reliance on uninterrupted power systems. Recent innovations such as AI-integrated transfer switches and modular hybrid systems have improved fault detection accuracy by over 25%. Asia-Pacific accounts for over 40% of incremental demand, driven by rapid infrastructure expansion, while North America leads in technology adoption. Increasing supply chain localization and component standardization are further optimizing production efficiency, setting the stage for accelerated strategic investments.

The transfer switch market is rapidly transforming into a critical infrastructure layer as industries prioritize uninterrupted power, operational resilience, and energy optimization. With rising dependence on digital infrastructure, even milliseconds of power disruption translate into measurable financial losses, forcing organizations to invest aggressively in advanced switching systems. A major structural shift is unfolding as supply chain localization and grid decentralization reshape procurement and deployment strategies, particularly after recent global energy disruptions. Intelligent transfer switches integrated with real-time monitoring are redefining performance benchmarks. AI-enabled transfer switches improve efficiency by 28% while reducing maintenance costs by 22% compared to legacy electromechanical systems. This technological shift is accelerating adoption across sectors requiring high uptime reliability.

Regionally, North America leads in volume due to mature infrastructure, while Asia-Pacific leads in adoption acceleration with over 35% increase in smart switch installations driven by industrial expansion and grid modernization. In the next 2–3 years, automated transfer switch penetration is expected to exceed 70% in critical infrastructure, improving system uptime by over 30% and reducing outage-related costs by nearly 20%. ESG alignment is emerging as a competitive advantage, with energy-efficient switching systems lowering power loss by 12–15%, directly impacting operational costs and regulatory compliance.

A real-world example includes a 2025 manufacturing facility deployment where smart transfer switches improved operational continuity by 27% and reduced manual intervention by 40%. Companies are shifting capital allocation toward digital switchgear, predictive maintenance, and integrated energy management platforms. This market is no longer a passive component segment but a strategic enabler of resilience, forcing companies to optimize technology adoption, accelerate investments, and position themselves for a digitally controlled power ecosystem.

Increasing grid volatility, combined with the explosive growth of data centers and industrial automation, is forcing rapid adoption of transfer switch systems. Power outage frequency has increased by nearly 18% in key industrial regions, directly impacting productivity and operational continuity. Simultaneously, data center capacity expansion has surged by over 30%, creating a critical need for uninterrupted power solutions. A key global trigger is the ongoing restructuring of energy infrastructure following geopolitical supply disruptions, pushing governments to prioritize energy resilience investments. This has led to a 25% increase in funding for backup power systems and smart grid technologies. The cause is clear: unstable grids and high digital dependency. The impact is measurable: downtime costs rising by up to 20% annually in critical sectors. Businesses are responding by accelerating deployment of automatic transfer switches, expanding manufacturing capacity, and forming strategic partnerships with energy solution providers. This shift is not optional but essential for maintaining operational continuity and competitive positioning.

The transfer switch market faces significant constraints due to raw material cost volatility and supply chain concentration. Copper and semiconductor component prices have fluctuated by over 22% in recent years, directly increasing manufacturing costs. Additionally, nearly 60% of key electronic components are sourced from a limited number of suppliers, creating supply risk. A major real-world constraint is the global semiconductor shortage, which has delayed production cycles by up to 15% in certain regions. These disruptions are increasing lead times and limiting scalability, particularly for advanced automatic transfer switches. The direct business impact includes higher capital costs, delayed project timelines, and reduced deployment speed. Companies are mitigating these risks by diversifying supplier networks, securing long-term procurement contracts, and investing in alternative materials and localized production. However, cost pressures remain a critical barrier to widespread adoption, particularly in price-sensitive markets.

The emergence of smart grids and decentralized energy systems is unlocking high-value opportunities for advanced transfer switch technologies. Integration with renewable energy systems has increased by over 35%, creating demand for hybrid transfer switches capable of managing multiple power sources efficiently. A key innovation shift is the development of IoT-enabled and AI-driven transfer switches, improving predictive maintenance accuracy by 30% and reducing unexpected failures by 25%. These capabilities are opening new demand pockets in sectors such as renewable energy, electric vehicle infrastructure, and smart cities. An important future signal is the rise of microgrids, with deployment increasing by over 28% globally. These systems require highly responsive and intelligent switching solutions, creating a strong growth avenue. Companies are positioning for dominance by investing in R&D, expanding digital capabilities, and building integrated energy ecosystems. The non-obvious advantage lies in long-term operational savings and enhanced system reliability, making advanced transfer switches a strategic investment rather than a cost component.

Despite strong demand, the market faces execution challenges related to infrastructure limitations and integration complexity. Over 40% of existing power infrastructure is not fully compatible with modern automated transfer switch systems, requiring costly upgrades. A significant real-world pressure is the limited grid capacity in emerging economies, where power distribution networks struggle to support advanced switching technologies. This creates adoption barriers and slows deployment timelines. Performance consistency is another concern, with system integration failures reported in nearly 12% of complex installations, impacting reliability and customer confidence. Additionally, high upfront investment costs, often 20–25% higher for advanced systems, limit adoption among small and medium enterprises. These challenges directly affect scalability and long-term growth consistency. Companies must invest in infrastructure modernization, develop standardized integration frameworks, and strengthen technical expertise. Strategic partnerships and innovation in cost-efficient solutions will be essential to overcome these barriers and sustain competitive advantage in a rapidly evolving market.

The transfer switch market is segmented across types, applications, and end-users, with demand increasingly concentrated in high-reliability and automation-driven segments. Automatic and closed transition switches dominate installations due to their ability to ensure uninterrupted power flow, collectively accounting for over 60% of deployments. Applications are heavily skewed toward industrial power supply and data center power, which together contribute nearly 55% of demand, reflecting the rising dependency on continuous operations. End-user demand is led by industrial facilities and data centers, where uptime requirements exceed 99%, forcing adoption of advanced switching systems. Demand is shifting toward intelligent, integrated solutions, particularly in renewable integration and healthcare, where reliability and compliance are critical. This segmentation trend highlights a clear movement from basic backup systems to high-performance, automated infrastructure, requiring companies to align product development and market strategies with evolving operational needs.

Automatic transfer switches dominate the market with approximately 62% share, driven by their ability to deliver seamless power transitions, minimize downtime, and integrate with digital monitoring systems. Their structural advantage lies in automation, scalability, and compatibility with critical infrastructure, making them the preferred choice across industrial and commercial applications. Closed transition switches are emerging as the fastest-growing segment, with adoption increasing by over 24%, as they enable zero-interruption switching, particularly valuable in data centers and healthcare environments. In comparison, manual transfer switches, holding around 18% share, are gradually declining due to operational inefficiencies and reliance on human intervention, limiting their scalability in high-demand environments. Static transfer switches, known for ultra-fast switching speeds, are gaining niche traction in sensitive applications but remain limited to specialized use cases. Open transition switches, along with static systems, collectively account for nearly 20% of the market, maintaining relevance in cost-sensitive and less critical operations.

Demand is clearly shifting toward automated and intelligent systems, prompting companies to expand production of digital transfer switches and invest in advanced control technologies. This transition signals a strong business implication: investment is increasingly directed toward high-performance, automation-driven solutions, while legacy systems are steadily losing strategic relevance.

Industrial power supply leads the application segment with approximately 34% share, driven by continuous production requirements and high dependency on uninterrupted electricity. The concentration of demand in this segment is due to rising automation and the need to prevent costly downtime. Data center power is the fastest-growing application, expanding at over 27%, fueled by hyperscale infrastructure expansion and increasing digital workloads. Emergency power systems, accounting for nearly 22% share, remain critical in healthcare and public infrastructure, but are comparatively mature. In contrast, renewable integration is rapidly gaining traction, supported by over 25% increase in hybrid energy system deployments, as organizations seek to manage multiple power sources efficiently. Backup power applications, along with emergency systems, collectively represent around 44% of demand, reflecting stable but slower growth patterns.

The comparison highlights a clear shift from traditional backup systems toward high-performance, continuous power applications such as data centers and renewable systems. Companies are responding by tailoring solutions for high-load environments, enhancing system intelligence, and expanding deployment capabilities. The business implication is clear: demand is moving toward sectors where uptime and energy optimization are mission-critical, requiring strategic repositioning.

Industrial facilities dominate the end-user segment with approximately 38% share, driven by high energy consumption and the need for uninterrupted production cycles. Their demand concentration is rooted in operational intensity and the financial impact of downtime. Data centers represent the fastest-growing end-user group, with adoption rising by over 30%, supported by digital transformation and cloud infrastructure expansion. In comparison, healthcare facilities, accounting for around 16% share, require highly reliable power systems but operate within regulated frameworks that slow rapid expansion. Commercial buildings and utilities, together contributing nearly 46% of demand, show steady adoption driven by urban infrastructure growth and grid reliability requirements.

The contrast between industrial facilities and data centers highlights a shift from traditional heavy-load users to digitally driven environments requiring near-zero downtime. Buying behavior is evolving, with large enterprises prioritizing intelligent, automated solutions and long-term service contracts. Companies are responding through customized solutions, flexible pricing models, and strategic partnerships with infrastructure developers.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

North America leads in demand concentration, driven by high automation penetration exceeding 65% in critical infrastructure, while Asia-Pacific commands over 40% of global installation volume, reflecting rapid industrial expansion and electrification. Europe holds approximately 24% share, leading in innovation with over 55% adoption of energy-efficient and compliant switching systems. A key structural shift is the global push for grid resilience and localized manufacturing, reshaping supply chains and accelerating regional investments. While North America dominates scale and reliability, Asia-Pacific leads expansion, and Europe drives regulatory innovation, prompting companies to prioritize Asia-Pacific for growth while maintaining technology leadership in developed markets.

How are high-reliability power systems redefining enterprise infrastructure investments?

North America holds approximately 34% market share, with demand heavily concentrated in data centers, healthcare, and industrial automation sectors where uptime requirements exceed 99%. A major structural force is the ongoing grid modernization push, increasing investment in resilient infrastructure by over 25%. Execution is shifting toward AI-integrated transfer switches, with over 60% of new installations featuring real-time monitoring and predictive maintenance. A measurable shift includes a 30% increase in deployment across hyperscale data centers. Enterprises prioritize reliability and automation, favoring premium, high-performance systems over cost-driven alternatives. Companies are expanding digital product lines and forming partnerships with energy solution providers, signaling that this region remains critical for technology leadership and high-margin innovation.

How is compliance-driven innovation reshaping power continuity solutions?

Europe accounts for nearly 24% of the market, with strong contributions from Germany, France, and the UK. Strict energy efficiency regulations and carbon reduction targets are driving adoption, with over 55% of installations aligned with low-loss, energy-efficient standards. ESG mandates are forcing a shift toward smart and hybrid transfer switches, improving operational efficiency by nearly 18%. Companies are integrating advanced monitoring systems to meet compliance and reporting requirements. A key measurable trend includes a 20% increase in adoption of closed transition switches for uninterrupted operations. Enterprises prioritize quality and compliance over cost, pushing manufacturers to innovate continuously. This region compels companies to adapt through sustainable design and regulatory alignment to remain competitive.

What is driving rapid scaling in power infrastructure deployment?

Asia-Pacific represents over 40% of global demand volume, led by China, India, and Southeast Asia. The region benefits from strong manufacturing capacity and large-scale infrastructure development, with industrial electrification projects increasing by over 30%. Execution is shifting toward mass deployment of automated transfer switches, with adoption rates rising by 35% in industrial zones. Localized production has grown by nearly 28%, reducing costs and improving supply efficiency. A key strategic move includes large-scale capacity expansions to support rising export demand. Enterprises prioritize cost-efficiency and scalability, driving bulk procurement and standardized solutions. This region is critical for volume-driven growth, making it the primary focus for expansion and supply chain optimization strategies.

How are infrastructure gaps influencing power continuity investments?

South America contributes approximately 8% of the market, with Brazil and Argentina leading demand due to industrial and commercial infrastructure needs. Frequent power disruptions, increasing by nearly 15% in key regions, are driving demand for backup power solutions. However, structural constraints such as limited grid infrastructure and cost sensitivity restrict rapid adoption. Execution is shifting toward localized, cost-effective transfer switch solutions, with adoption rising by 18% in mid-scale industries. A measurable trend includes increased deployment in manufacturing and mining sectors. Enterprises prioritize affordability and reliability, often opting for hybrid or manual systems. This region presents a balanced opportunity, where growth potential exists but requires cost-focused strategies and localized adaptation.

What role does infrastructure expansion play in accelerating adoption?

The Middle East & Africa region accounts for approximately 10% of demand, driven by large-scale infrastructure and energy projects in countries such as the UAE, Saudi Arabia, and South Africa. Oil & gas, construction, and utilities sectors contribute over 60% of regional demand. A key transformation driver is government-led investment in smart infrastructure, increasing deployment of advanced transfer switches by nearly 22%. Execution is shifting toward integration with modern power systems, particularly in urban development projects. A strategic move includes expanding partnerships for technology deployment in mega projects. Enterprises prioritize reliability and long-term performance, making this region a strategic growth frontier for infrastructure-driven demand.

United States – 32% share; dominance driven by advanced grid infrastructure, high data center density, and strong adoption of automated transfer systems.

China – 27% share; leadership supported by rapid industrial electrification, large-scale manufacturing capacity, and expanding smart grid deployment.

The transfer switch market is defined by competition between global technology leaders, regional manufacturers, and specialized system integrators. Major players such as Schneider Electric, ABB, Siemens, Eaton, and Vertiv collectively hold approximately 45% market share, competing primarily against regional cost-focused manufacturers and niche technology providers. Competition is driven by technology innovation, pricing strategies, and supply chain efficiency. Advanced players are leveraging digital switchgear and AI-enabled monitoring, improving operational efficiency by over 25%, while cost-focused competitors are reducing product pricing by nearly 15% to capture emerging markets. Companies are actively expanding manufacturing footprints, forming strategic partnerships, and investing in R&D to enhance product capabilities. A significant competitive shift is the move toward integrated energy management solutions, where transfer switches are bundled with digital platforms. Entry barriers remain high due to certification requirements, technology complexity, and capital investment. To succeed, companies must combine technological differentiation with scalable production and strong regional distribution networks.

Schneider Electric

ABB

Siemens

Eaton Corporation

Vertiv Group Corp.

General Electric

Mitsubishi Electric

Cummins Inc.

Generac Power Systems

Socomec Group

Legrand

Fuji Electric

Toshiba Corporation

Digital and automated transfer switch technologies are reshaping operational reliability, with automatic systems now used in over 62% of installations globally. These systems improve switching response time by 35% and reduce manual intervention by nearly 40%, directly enhancing uptime in critical infrastructure. Integration with IoT-enabled monitoring platforms is enabling real-time diagnostics, cutting maintenance costs by approximately 18% while improving system visibility and control.

Emerging technologies such as AI-driven predictive maintenance and cloud-based energy management are gaining rapid traction, with adoption levels crossing 30% in large-scale industrial and data center environments. These systems enhance fault detection accuracy by 25% and reduce unexpected outages by 20%, allowing enterprises to shift from reactive to proactive maintenance models. The integration trend is moving toward centralized control systems, enabling multi-site energy optimization and operational standardization.

Disruptive advancements in static and hybrid transfer switches are redefining performance benchmarks, particularly in high-sensitivity applications. Static switches deliver switching speeds under 5 milliseconds, improving performance by over 50% compared to conventional electromechanical systems. In comparison, new digital transfer switches improve efficiency by 28% while reducing lifecycle costs by 22% compared to legacy systems, signaling a decisive shift toward intelligent infrastructure.

From a competitive perspective, companies investing in smart, connected switching solutions are gaining a clear advantage, particularly in data center and renewable integration segments. Between 2026 and 2028, over 70% of new deployments are expected to include intelligent control features, forcing manufacturers to accelerate innovation cycles and embed advanced analytics capabilities to remain relevant in a rapidly digitizing power ecosystem.

March 2026 – Schneider Electric launched an advanced digital transfer switch platform integrating real-time monitoring, improving fault detection accuracy by 30% and reducing downtime risks in industrial systems. This strengthens its smart infrastructure portfolio and enhances competitive positioning in high-reliability segments. [Digital Expansion] Source: (https://www.se.com)

November 2025 – ABB expanded its low-voltage product manufacturing capacity by 20% to support rising demand for automated transfer switches across Asia-Pacific. This move improves regional supply efficiency and shortens delivery timelines, reinforcing ABB’s position in high-growth industrial and infrastructure markets. [Capacity Scaling] Source: (https://global.abb)

July 2025 – Eaton partnered with a data center operator to deploy intelligent transfer switching systems, achieving a 25% improvement in uptime reliability and a 15% reduction in energy losses. This highlights the growing role of integrated power management solutions in digital infrastructure. [Strategic Partnership] Source: (https://www.eaton.com)

February 2024 – Siemens introduced a closed transition transfer switch solution designed for uninterrupted power transfer, reducing switching delays by 40% in healthcare and mission-critical applications. This innovation supports compliance-driven demand and strengthens Siemens’ presence in high-performance segments. [Product Innovation] Source: (https://www.siemens.com)

The report provides comprehensive coverage of the transfer switch market across key segments, including types such as automatic, manual, static, closed transition, and open transition systems; applications spanning emergency power, industrial supply, data centers, and renewable integration; and end-users including industrial facilities, commercial buildings, utilities, and healthcare. It evaluates demand across five major regions, capturing over 95% of global deployment activity, while also analyzing emerging technologies such as AI-enabled monitoring, IoT integration, and hybrid switching systems. Notably, automatic transfer switches account for over 60% of installations, while data center applications contribute nearly 25% of demand, reflecting a strong shift toward high-reliability infrastructure.

The analytical depth includes evaluation of more than 12 major companies, alongside detailed insights into adoption patterns, with over 70% of critical infrastructure facilities prioritizing automated switching solutions. The report also examines niche growth areas such as microgrid integration and decentralized energy systems, where adoption is increasing by over 25%. Covering the 2026–2033 period, it provides forward-looking insights into technology evolution, regional expansion strategies, and competitive positioning. This enables decision-makers to identify investment priorities, optimize market entry strategies, and align with high-impact growth segments in a rapidly transforming energy ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1182.13 Million |

|

Market Revenue in 2033 |

USD 1884.15 Million |

|

CAGR (2026 - 2033) |

6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Schneider Electric, ABB, Siemens, Eaton Corporation, Vertiv Group Corp., General Electric, Mitsubishi Electric, Cummins Inc., Generac Power Systems, Socomec Group, Legrand, Fuji Electric, Toshiba Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |