Reports

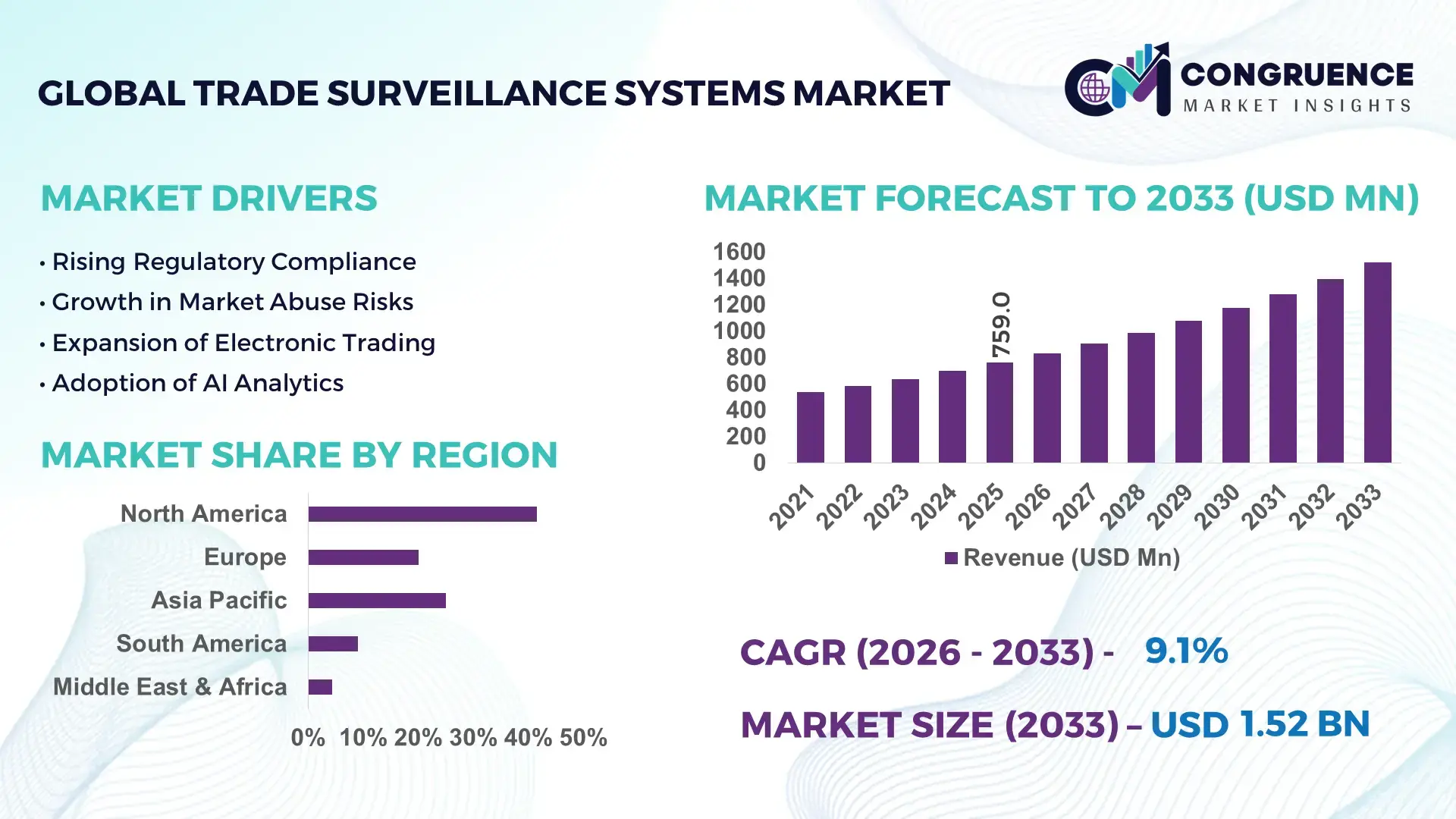

The Global Trade Surveillance Systems Market was valued at USD 759.04 Million in 2025 and is anticipated to reach a value of USD 1523.57 Million by 2033 expanding at a CAGR of 9.1% between 2026 and 2033. This growth is driven by rising regulatory scrutiny across financial markets and the accelerated adoption of automated compliance and monitoring platforms by trading institutions.

The United States represents the most advanced ecosystem for trade surveillance systems, supported by a mature financial services infrastructure and large-scale technology deployment. Over 65% of Tier-1 investment banks operating in the U.S. have implemented multi-asset surveillance platforms covering equities, derivatives, FX, and fixed income trading. Annual investments in financial compliance technologies exceeded USD 4.8 billion in 2024, with a significant portion allocated to AI-based monitoring tools. High-frequency trading environments process billions of transactions daily, driving demand for real-time analytics, pattern recognition, and cloud-based surveillance architectures. Advanced machine learning models capable of analyzing over 100 million events per day are increasingly deployed to detect market abuse, insider trading, and spoofing activities across regulated exchanges and dark pools.

Market Size & Growth: USD 759.04 Million in 2025, projected to reach USD 1523.57 Million by 2033 at a CAGR of 9.1%, supported by automation of regulatory compliance and cross-asset trade monitoring

Top Growth Drivers: Regulatory reporting automation adoption at 42%, AI-driven anomaly detection efficiency improvement of 35%, cloud-based deployment penetration increase of 38%

Short-Term Forecast: By 2028, average compliance operational costs are expected to decline by 22% through workflow automation and centralized surveillance platforms

Emerging Technologies: Artificial intelligence and machine learning analytics, cloud-native surveillance platforms, real-time behavioral analytics

Regional Leaders: North America projected at USD 612 Million by 2033 with multi-asset surveillance adoption, Europe at USD 418 Million driven by MiFID II compliance expansion, Asia-Pacific at USD 327 Million supported by exchange modernization initiatives

Consumer/End-User Trends: Investment banks, broker-dealers, and exchanges increasingly favor integrated, multi-regulation surveillance solutions over standalone tools

Pilot or Case Example: A 2024 pilot deployment at a global investment bank reduced false-positive alerts by 31% and improved investigation turnaround time by 27%

Competitive Landscape: NICE Actimize holding approximately 22% share, followed by Nasdaq, FIS, Refinitiv, and SIA

Regulatory & ESG Impact: Expansion of market abuse regulations, enhanced transaction transparency mandates, and governance-focused compliance investments

Investment & Funding Patterns: Over USD 2.1 Billion invested globally between 2022–2024, with increased venture funding in AI-driven RegTech platforms

Innovation & Future Outlook: Integration of cross-market data lakes, predictive surveillance models, and real-time regulatory reporting frameworks

The Trade Surveillance Systems Market is shaped by strong demand from capital markets, investment banking, asset management, and exchange operators, with these sectors collectively accounting for over 70% of system deployments. Recent innovations include AI-powered alert optimization, cross-venue trade correlation engines, and cloud-scalable compliance architectures. Regulatory frameworks such as market abuse regulations, transaction reporting mandates, and data retention requirements continue to influence adoption decisions. Regionally, North America and Europe lead in system maturity, while Asia-Pacific exhibits the fastest growth due to expanding electronic trading volumes and regulatory reforms. Emerging trends point toward fully automated surveillance ecosystems, deeper integration with risk management platforms, and predictive analytics capabilities designed to anticipate compliance breaches before execution.

The strategic relevance of the Trade Surveillance Systems Market is closely tied to its role in safeguarding market integrity, ensuring regulatory compliance, and enabling operational resilience across global capital markets. As trading volumes grow in both traditional and digital asset classes, surveillance platforms have become a core component of enterprise risk and compliance strategies. Artificial intelligence–based behavioral analytics now serve as a strategic differentiator; for example, machine learning–driven surveillance delivers nearly 35% improvement in anomaly detection accuracy compared to rule-based legacy monitoring systems. This shift allows institutions to manage exponentially larger datasets while reducing investigation backlogs and compliance costs.

From a regional perspective, North America dominates in transaction volume due to high-frequency and multi-asset trading environments, while Europe leads in adoption with approximately 68% of regulated financial institutions deploying advanced, multi-regulation surveillance platforms aligned with MiFID II and MAR requirements. In the short term, by 2028, real-time AI-driven alert prioritization is expected to improve compliance investigation efficiency by nearly 25%, enabling faster response to potential market abuse and reducing manual review workloads.

Compliance and ESG considerations are increasingly intertwined, as firms commit to governance transparency and operational efficiency. Many institutions are targeting a 30% reduction in redundant data storage and processing emissions by 2030 through cloud optimization and centralized surveillance architectures. In a measurable micro-scenario, in 2024, a U.S.-based exchange operator achieved a 28% reduction in false-positive alerts through the deployment of natural language processing and cross-market correlation analytics. Looking forward, the Trade Surveillance Systems Market is positioned as a foundational pillar supporting resilient financial infrastructure, proactive compliance, and sustainable, technology-driven market growth.

Regulatory authorities are increasing the scope, depth, and frequency of market monitoring obligations, directly stimulating demand for advanced trade surveillance systems. Frameworks such as MiFID II, MAR, SEC Rule 613, and global transaction reporting mandates require firms to capture, analyze, and retain massive volumes of trading data across asset classes. More than 70% of large financial institutions now monitor trades across at least four asset classes, compared to fewer than 45% a decade ago. This expansion has made manual or fragmented monitoring impractical. Automated surveillance platforms enable real-time detection of spoofing, layering, wash trades, and insider activity, supporting faster regulatory reporting and internal escalation. As enforcement actions and penalties for non-compliance increase, institutions are prioritizing robust surveillance infrastructures to reduce regulatory exposure and reputational risk.

Despite strong demand, implementation complexity remains a key restraint in the Trade Surveillance Systems Market. Integrating surveillance platforms with existing trading, order management, and data warehouses requires significant customization and technical expertise. Large institutions often operate dozens of legacy systems, creating fragmented data environments that complicate normalization and real-time analysis. Initial deployment timelines can extend beyond 12 months for multi-asset implementations, increasing operational disruption. Smaller firms, in particular, face challenges due to limited budgets and in-house compliance technology resources. Additionally, ongoing model tuning, regulatory updates, and data quality management demand continuous investment. These factors can delay adoption decisions, especially among mid-sized brokerages and regional exchanges, slowing uniform market penetration.

The growing adoption of AI-driven cross-asset surveillance represents a significant opportunity for the Trade Surveillance Systems Market. As trading strategies increasingly span equities, derivatives, FX, and digital assets, demand is rising for platforms capable of correlating activity across venues and instruments in real time. Advanced machine learning models can analyze millions of events per second, identifying complex behavioral patterns that were previously undetectable. Institutions deploying cross-market analytics report up to 30% reductions in investigation time due to improved alert relevance. Emerging opportunities also exist in surveillance for crypto-assets and decentralized finance platforms, where regulatory frameworks are still evolving. Vendors offering flexible, modular solutions that adapt to new asset classes and regulations are well positioned to capture untapped demand.

The exponential growth of trading data presents an ongoing challenge for the Trade Surveillance Systems Market. High-frequency trading, algorithmic strategies, and expanded reporting obligations generate billions of daily data points, straining processing and storage infrastructures. Without advanced analytics, surveillance systems can produce excessive false positives, overwhelming compliance teams and diluting investigative focus. In some institutions, over 60% of alerts are initially deemed non-actionable, increasing labor costs and response times. Managing data privacy, retention requirements, and cross-border data transfer regulations further complicates operations. Addressing these challenges requires continuous investment in scalable architectures, model optimization, and skilled compliance personnel, making efficient alert management a critical success factor for market participants.

• Accelerated Adoption of AI-Driven Behavioral Analytics: Advanced behavioral analytics powered by artificial intelligence is becoming a core capability within modern trade surveillance systems. More than 62% of Tier-1 financial institutions have shifted from static rule-based monitoring to machine learning–based models capable of analyzing trader behavior across multiple asset classes. These AI models process over 80 million trade and order events per day in large exchanges, improving suspicious pattern detection accuracy by nearly 33%. Institutions report a 29% reduction in manual review workloads as adaptive algorithms continuously recalibrate thresholds based on historical and real-time data, enabling more precise identification of market abuse activities.

• Expansion of Cloud-Native and SaaS Surveillance Platforms: Cloud-native trade surveillance platforms are rapidly replacing on-premise deployments due to scalability and operational efficiency advantages. Approximately 58% of new surveillance implementations in 2024 were cloud-based, enabling firms to scale processing capacity by more than 45% during peak trading periods without infrastructure expansion. SaaS-based models have reduced average system deployment times from 9 months to under 4 months. Additionally, centralized cloud architectures have helped organizations lower system maintenance efforts by 27%, while improving cross-venue data consolidation across equities, derivatives, FX, and digital assets.

• Growing Focus on False-Positive Reduction and Alert Optimization: Alert optimization has emerged as a measurable priority as institutions seek to improve compliance efficiency. Nearly 65% of compliance teams cite false positives as their primary operational challenge, prompting increased investment in alert-ranking and prioritization engines. Advanced surveillance platforms now achieve false-positive reductions of 30–38% through predictive scoring and contextual data enrichment. These improvements shorten investigation cycles by an average of 24% and allow compliance analysts to handle 20% more cases per month without additional staffing, strengthening overall regulatory responsiveness.

• Integration of Cross-Asset and Cross-Market Surveillance Capabilities: The convergence of trading strategies across asset classes is driving demand for unified surveillance systems capable of monitoring activity across multiple markets. Over 57% of global banks now operate cross-asset surveillance frameworks covering equities, fixed income, derivatives, and FX within a single platform. These integrated systems analyze correlations across venues and instruments, increasing detection of complex manipulation schemes by nearly 28%. As electronic and algorithmic trading volumes continue to rise, cross-market surveillance adoption is expected to expand further, particularly among exchanges processing more than 1 billion transactions annually.

The Trade Surveillance Systems Market is segmented based on type, application, and end-user, reflecting the diverse operational needs of global financial ecosystems. By type, solutions range from rule-based surveillance to advanced AI-driven platforms, with clear differentiation in scalability, automation, and analytical depth. Application-wise, market demand spans market abuse detection, transaction monitoring, risk management, and regulatory reporting, each shaped by evolving compliance mandates and trading complexity. From an end-user perspective, investment banks, exchanges, broker-dealers, and asset managers represent the core adopters, while emerging participation from fintech platforms and digital asset venues is reshaping adoption patterns. Across segments, institutions increasingly prioritize integrated, real-time, and cross-asset capabilities, signaling a shift from fragmented compliance tools toward enterprise-wide surveillance infrastructures.

The Trade Surveillance Systems Market by type includes rule-based surveillance systems, AI and machine learning–based surveillance platforms, hybrid surveillance systems, and cloud-native surveillance solutions. AI and machine learning–based platforms currently lead the segment, accounting for approximately 46% of total adoption, due to their ability to analyze complex trading behaviors across millions of daily transactions and significantly reduce false positives. Rule-based systems still represent around 28% of deployments, particularly among smaller firms, but their limitations in handling high-frequency and cross-asset trading are increasingly evident. Hybrid systems, combining rules with adaptive analytics, along with fully cloud-native platforms, collectively contribute about 26%, serving firms transitioning from legacy architectures.

AI-driven surveillance is also the fastest-growing type, expanding at an estimated CAGR of 13.8%, fueled by rising algorithmic trading volumes and regulatory expectations for proactive market abuse detection. Growth is further supported by improvements in natural language processing and pattern recognition models.

By application, market abuse detection represents the leading segment, holding approximately 41% share, as regulators prioritize prevention of insider trading, spoofing, layering, and cross-venue manipulation. Transaction monitoring follows with about 27% adoption, particularly for real-time oversight of high-frequency and algorithmic trades. Regulatory reporting and compliance management account for roughly 19%, driven by stringent reporting timelines and data retention requirements, while risk analytics and other niche applications collectively contribute the remaining 13%.

Real-time market abuse detection is also the fastest-growing application, advancing at an estimated CAGR of 12.6%, supported by the shift toward continuous monitoring rather than post-trade reviews. Increased use of multi-asset trading strategies and off-exchange venues is accelerating demand for real-time analytics.

Investment banks are the dominant end-user group in the Trade Surveillance Systems Market, accounting for nearly 38% of total adoption, driven by high trading volumes, multi-asset exposure, and stringent regulatory oversight. Exchanges and trading venues follow closely with around 26%, reflecting their responsibility for real-time market integrity across millions of daily transactions. Broker-dealers represent approximately 18%, while asset management firms contribute about 11%, increasingly adopting surveillance to monitor internal trading conduct and outsourced execution. Other users, including fintech trading platforms and digital asset exchanges, collectively hold about 7% but are gaining visibility.

Digital asset exchanges and fintech trading platforms are the fastest-growing end-user segment, expanding at an estimated CAGR of 15.2%, fueled by regulatory formalization and rapid growth in electronic trading participation. Adoption rates among major crypto and alternative trading platforms exceeded 60% for automated surveillance tools by 2025.

North America accounted for the largest market share at 41.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.8% between 2026 and 2033.

North America continues to lead due to high electronic trading volumes exceeding 65% of global algorithmic transactions and widespread adoption of multi-asset surveillance platforms across equities, derivatives, and FX markets. Europe follows closely with a 32.4% share, supported by stringent regulatory enforcement and harmonized compliance frameworks across more than 30 regulated exchanges. Asia-Pacific currently represents 19.1% of the market but is rapidly expanding as exchange digitization initiatives increase monitored transaction volumes by over 45% across major markets. South America and Middle East & Africa together account for approximately 6.9%, driven by modernization of capital markets, rising foreign investment flows, and gradual regulatory alignment with global best practices.

How are advanced analytics and regulatory rigor reshaping enterprise-level compliance ecosystems?

North America holds the largest regional share at approximately 41.6%, driven primarily by the United States and Canada. Financial services, capital markets, and exchange operators represent over 70% of regional demand, supported by strict oversight frameworks governing equities, derivatives, and alternative trading systems. Regulatory enhancements focusing on real-time monitoring and cross-venue transparency have increased enterprise adoption rates to nearly 68% among Tier-1 institutions. Technological transformation is evident, with more than 60% of deployments utilizing AI-driven analytics and cloud-native architectures. Local players such as Nasdaq are actively expanding real-time surveillance solutions capable of processing over 100 million events daily. Regional consumer behavior shows significantly higher enterprise adoption within finance and capital markets compared to other industries, emphasizing accuracy, latency reduction, and audit-ready analytics.

How does regulatory harmonization influence demand for explainable and auditable surveillance platforms?

Europe accounts for nearly 32.4% of the Trade Surveillance Systems Market, led by the UK, Germany, and France. Regulatory bodies overseeing market abuse, transaction transparency, and cross-border trading have driven adoption rates above 65% among regulated institutions. Explainable AI and audit-friendly analytics are particularly emphasized, with over 55% of new deployments incorporating model transparency features. Sustainability and governance initiatives further influence technology selection, as firms align compliance tools with long-term risk management objectives. A prominent regional exchange group has recently upgraded its surveillance stack to support multi-market correlation analysis across more than 25 trading venues. Consumer behavior reflects strong preference for compliant, explainable systems capable of meeting evolving regulatory scrutiny.

What role do digital exchanges and innovation hubs play in accelerating surveillance adoption?

Asia-Pacific ranks third by market share at approximately 19.1%, yet leads global growth momentum. China, Japan, India, and Australia collectively account for over 75% of regional demand. Exchange digitization programs have increased electronic trading penetration to more than 58% across major markets. Innovation hubs in Singapore, Tokyo, and Hong Kong are advancing AI-enabled surveillance, with regional platforms processing transaction volumes growing by 40% year-over-year. Local technology providers are developing scalable, multilingual surveillance systems tailored for diverse regulatory environments. Consumer behavior in this region is shaped by rapid growth in mobile trading and digital asset platforms, accelerating demand for real-time, automated monitoring solutions.

How are emerging capital markets strengthening oversight through technology adoption?

South America represents around 4.2% of the global market, with Brazil and Argentina as primary contributors. Financial market modernization initiatives have expanded electronic trading volumes by nearly 35% over the past three years. Government-backed reforms focusing on transparency and foreign investor confidence are encouraging adoption of automated surveillance platforms. Energy and commodities trading plays a significant role, accounting for over 30% of monitored transactions in the region. A leading regional exchange recently implemented centralized surveillance capable of monitoring equities and derivatives on a unified platform. Consumer behavior indicates growing institutional demand tied to cross-border trading and regulatory alignment with global standards.

Why is financial modernization driving demand for compliance technologies?

The Middle East & Africa holds approximately 2.7% of the market, led by the UAE and South Africa. Financial diversification strategies and capital market expansion initiatives are increasing monitored trade volumes by over 28% across regional exchanges. Technology modernization programs emphasize cloud adoption and centralized compliance platforms. Regulatory cooperation agreements with international markets are strengthening demand for globally compatible surveillance systems. A major Gulf exchange has deployed real-time monitoring tools supporting both equities and commodities trading. Regional consumer behavior reflects growing institutional focus on governance, transparency, and cross-border investment readiness.

United States – 36.8% market share: Dominance driven by high-frequency trading volumes, advanced regulatory enforcement, and large-scale enterprise adoption of AI-based surveillance platforms.

United Kingdom – 14.2% market share: Strong position supported by dense financial market activity, regulatory leadership, and early adoption of explainable, multi-asset trade surveillance systems.

The Trade Surveillance Systems market exhibits a moderately consolidated competitive structure, characterized by the presence of approximately 25–30 active global and regional vendors offering specialized compliance and monitoring solutions. The top five companies collectively account for nearly 55–60% of total deployments, reflecting strong brand recognition, long-term regulatory relationships, and deep integration with exchange and banking infrastructures. Market leaders differentiate through advanced analytics, cross-asset surveillance capabilities, and scalable cloud-native architectures capable of processing 80–120 million trade events per day.

Strategic initiatives remain central to competition. Over 40% of leading vendors have entered technology partnerships with cloud service providers and data analytics firms to enhance real-time monitoring and AI-driven alert optimization. Product launches increasingly focus on reducing false positives, with newer platforms reporting 30–35% improvement in alert accuracy compared to earlier generations. Mergers and acquisitions have been selective rather than aggressive, primarily aimed at acquiring niche capabilities such as crypto-asset surveillance, behavioral analytics, or natural language processing for communications monitoring.

Innovation trends shaping competition include explainable AI, unified cross-market surveillance dashboards, and modular compliance frameworks aligned with evolving regulations. While large vendors dominate Tier-1 banks and exchanges, smaller specialized providers remain competitive in regional markets and fintech segments, contributing to ongoing innovation and preventing full market consolidation.

NICE Actimize

Nasdaq

FIS

Refinitiv

SIA

ACA Group

Aquis Technologies

b-next

Eventus Systems

Software AG

Technology evolution is fundamentally reshaping the Trade Surveillance Systems Market, enabling institutions to manage rapidly increasing trading complexity, data volumes, and regulatory expectations. Artificial intelligence and machine learning technologies now underpin more than 60% of newly deployed surveillance platforms, allowing real-time analysis of trading behavior across equities, derivatives, foreign exchange, and digital assets. Advanced pattern-recognition models can process over 100 million trade and order events per day, improving detection accuracy for market abuse scenarios such as spoofing, layering, and insider trading by approximately 30–35% compared to legacy rule-based systems.

Natural language processing has emerged as a critical capability, particularly for monitoring trader communications across emails, chat platforms, and voice transcripts. Institutions integrating NLP modules report a 25% improvement in identifying collusive behavior when trade data is correlated with unstructured communications. Cloud-native architectures are another major technological shift, with nearly 58% of new implementations leveraging cloud or hybrid-cloud models to scale computing resources dynamically during peak trading periods. These deployments have reduced system latency by 20–28% while supporting centralized data governance across multiple trading venues.

Explainable AI is gaining traction as regulators demand transparency into decision-making logic. Approximately 45% of large financial institutions now require model interpretability features to support audits and regulatory reviews. Additionally, real-time cross-asset correlation engines are enabling surveillance teams to detect complex, multi-market manipulation patterns, increasing cross-venue detection effectiveness by 27%. Emerging technologies such as graph analytics, real-time streaming data pipelines, and API-driven modular surveillance components are expected to further enhance adaptability, interoperability, and compliance resilience across global financial markets.

• In July 2025, Nasdaq enhanced its trade surveillance offering with a real-time multi-asset monitoring module to detect suspicious trading patterns more accurately across equities, derivatives, and crypto asset markets, improving cross-venue anomaly detection capacity significantly.

• In June 2025, NICE Actimize rolled out a machine learning-powered auto-tuning capability in its SURVEIL-X platform, designed to identify emerging market abuse scenarios faster by reducing alert noise and accelerating downstream compliance investigations.

• In May 2025, BAE Systems introduced an integrated trade surveillance and communications monitoring solution, unifying oversight of both trade activity and internal communications within a single compliance platform for enhanced risk detection across financial institutions.

• In March 2025, Fenergo embedded trade surveillance screening rules directly into its KYC and onboarding workflows, enabling proactive monitoring of trading behaviors during client onboarding to mitigate risks before execution.

The scope of the Trade Surveillance Systems Market Report encompasses a comprehensive examination of surveillance solutions and services deployed by financial institutions, capital markets, exchanges, and digital trading platforms worldwide. The report analyzes diverse market segments such as deployment types — including on-premise, cloud, and hybrid environments — and organizational size categories spanning small and medium enterprises to large multinational banks. It delineates application areas that include market abuse detection, transaction monitoring, risk and compliance management, alert handling, and regulatory reporting. Geographic coverage includes major global regions — North America, Europe, Asia-Pacific, South America, Middle East & Africa — with detailed market profiles for key countries within these regions, capturing adoption patterns, technology preferences, and regulatory impacts.

Technological focus areas within the report highlight AI and machine learning integration, natural language processing (NLP) for communications surveillance, real-time analytics engines, and cross-asset, cross-venue correlation platforms. The analysis also considers emerging sectors, such as trade surveillance tailored for crypto and digital asset markets, multi-regulated environments, and decentralized finance (DeFi) trading infrastructures. End-user insights, such as adoption rates among investment banks, broker-dealers, exchanges, and fintech trading platforms, provide depth in understanding how different segments leverage surveillance technologies. The report further examines innovation trends — including explainable AI, modular architectures, and API-driven integrations — as well as competitive positioning of leading solution providers. Overall, the scope is designed to equip decision-makers with actionable intelligence on market dimensions, technological evolution, adoption drivers, and emerging opportunities across the global Trade Surveillance Systems landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

9.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

NICE Actimize, Nasdaq, FIS, Refinitiv, SIA, ACA Group, Aquis Technologies, b-next, Eventus Systems, Software AG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |