Reports

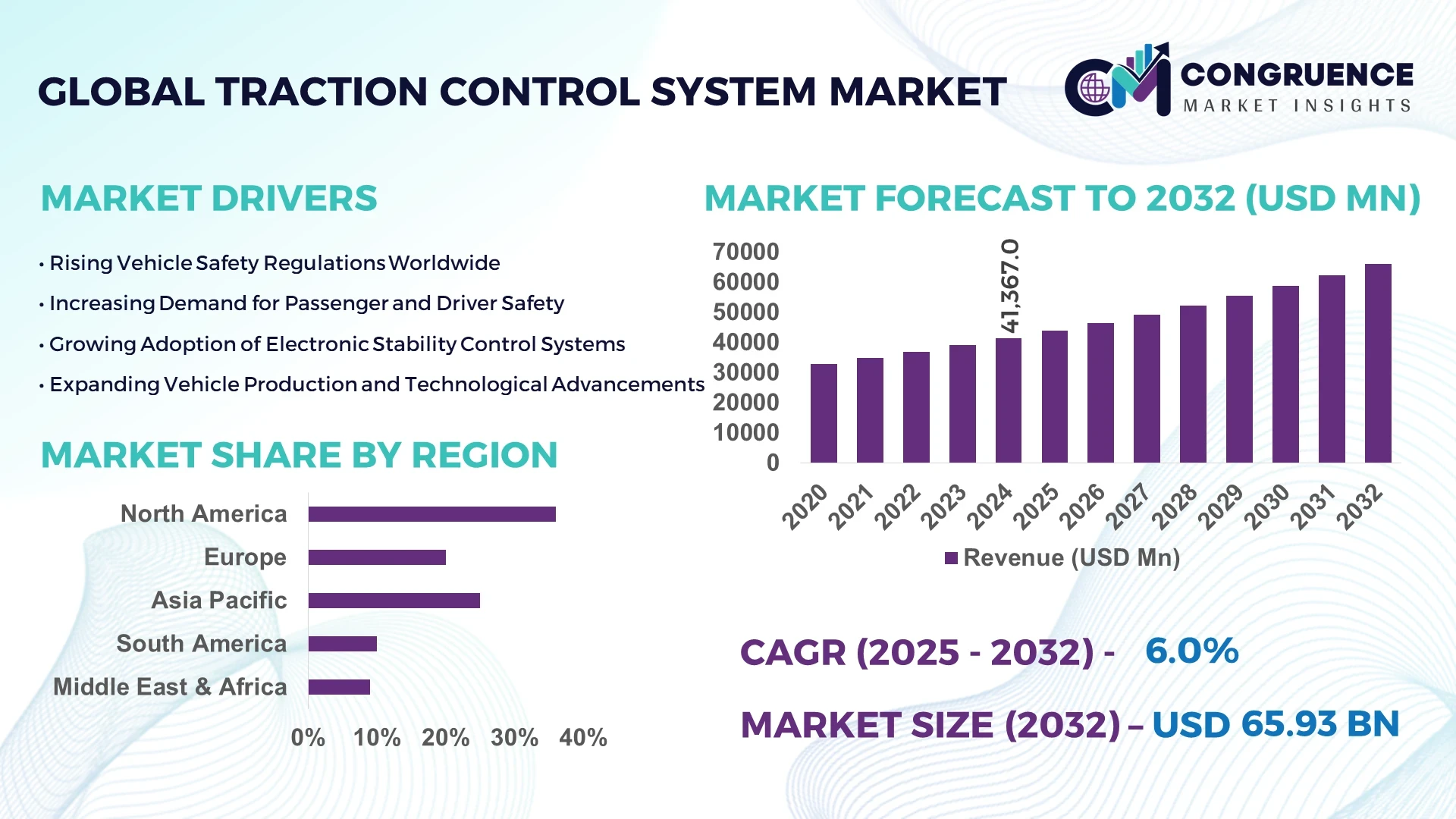

The Global Traction Control System Market was valued at USD 41,367 Million in 2024 and is anticipated to reach USD 65,933 Million by 2032, expanding at a CAGR of 6% between 2025 and 2032. The market’s expansion is primarily driven by growing demand for advanced vehicle safety technologies and regulatory mandates for automotive stability systems.

The United States dominates the global traction control system market due to its advanced automotive manufacturing base and high penetration of premium and electric vehicles. In 2024, over 82% of newly manufactured vehicles in the U.S. were equipped with traction control as a standard feature. The country invested more than USD 2.8 billion in R&D for integrated vehicle safety systems, emphasizing AI-driven braking and torque management solutions. Additionally, domestic automakers are increasingly adopting adaptive traction modules across SUVs and EV platforms to enhance performance on diverse terrains and in adverse weather conditions.

Market Size & Growth: Valued at USD 41,367 Million in 2024 and projected to reach USD 65,933 Million by 2032, expanding at a CAGR of 6%. Growth is driven by the rising integration of electronic stability programs in passenger and commercial vehicles.

Top Growth Drivers: 67% adoption rate in new passenger vehicles, 42% improvement in braking efficiency, and 35% increase in demand for anti-skid technologies in electric vehicles.

Short-Term Forecast: By 2028, cost optimization in control units is expected to improve manufacturing efficiency by 18%, with enhanced torque modulation response times by 22%.

Emerging Technologies: Integration of IoT-based diagnostics, AI-enhanced traction algorithms, and adaptive torque vectoring systems gaining prominence across luxury and EV segments.

Regional Leaders: North America projected at USD 21,300 Million, Europe at USD 18,900 Million, and Asia-Pacific at USD 16,800 Million by 2032, with Asia-Pacific showing rapid OEM adoption in compact vehicle models.

Consumer/End-User Trends: High adoption in passenger vehicles (59%) and commercial fleets (28%), supported by safety-focused consumer preferences and fleet electrification.

Pilot or Case Example: In 2024, a major European OEM deployed a next-gen traction control pilot that reduced skidding incidents by 31% across icy terrain test sites.

Competitive Landscape: Bosch leads with an estimated 22% share, followed by Continental AG, ZF Friedrichshafen, Denso Corporation, and Hitachi Astemo Ltd.

Regulatory & ESG Impact: Implementation of UN Vehicle Safety Regulations and Euro NCAP’s safety benchmarks have accelerated compliance-driven adoption.

Investment & Funding Patterns: Over USD 4.5 billion invested globally in traction control R&D and adaptive safety technologies between 2022 and 2024.

Innovation & Future Outlook: Advancements in sensor fusion, software-defined braking systems, and EV torque control are shaping the next generation of intelligent traction systems.

The Traction Control System Market continues to evolve with strong influence from the automotive, transportation, and electric mobility sectors. Passenger cars contribute approximately 58% of total installations, followed by heavy commercial vehicles at 24%. Innovations in real-time road friction estimation, regenerative braking synchronization, and modular ECU design are transforming performance efficiency. Regulatory frameworks emphasizing vehicle stability and emissions reduction are driving system standardization. Regionally, Asia-Pacific and Europe are experiencing accelerating adoption due to high-volume production and electric vehicle expansion. The future trajectory highlights deeper integration of AI analytics, cybersecurity compliance for connected systems, and scalable designs to meet diverse OEM and aftermarket requirements globally.

The strategic relevance of the Traction Control System (TCS) market lies in its crucial role in enhancing vehicle safety, performance, and regulatory compliance amid rapid electrification and automation trends. Modern traction systems integrate AI-driven algorithms and sensor fusion, enabling dynamic torque distribution and real-time traction adjustment. AI-enabled traction control delivers 38% faster response times compared to conventional mechanical systems, significantly improving stability in electric and autonomous vehicles. Asia-Pacific dominates in production volume, driven by large-scale automotive manufacturing in China and Japan, while Europe leads in technology adoption with over 62% of vehicles equipped with digital traction systems. By 2028, the integration of predictive analytics and edge-based control modules is expected to reduce braking lag by 25% and improve energy efficiency by 15% in electric drivetrains.

From an ESG standpoint, automakers are committing to sustainability through 30% reduction in component waste and 25% material recycling by 2030, aligning traction system production with global emission standards. In 2024, Germany achieved a 22% improvement in traction precision through Bosch’s AI-powered adaptive control unit, optimizing wheel slip management and battery utilization. Going forward, the Traction Control System market will serve as a pillar of resilience, compliance, and sustainable mobility, merging advanced safety frameworks with energy-efficient design and intelligent analytics to shape the future of connected, autonomous transportation ecosystems.

The surge in demand for advanced safety features and optimized performance across vehicle segments is a major growth catalyst for the Traction Control System market. Nearly 72% of new passenger vehicles produced in 2024 featured integrated traction and stability systems. Consumers’ rising preference for smoother acceleration, improved cornering stability, and reduced skidding in harsh terrains has driven OEMs to embed TCS into both mid-range and luxury models. Furthermore, the expansion of EVs—requiring fine-tuned torque control for instant power delivery—has boosted adoption rates. Manufacturers are investing heavily in AI-based traction mapping and digital signal processing to minimize response latency by over 30%, enhancing overall driving experience and safety compliance.

The primary restraint in the Traction Control System market stems from high integration costs associated with advanced sensor and ECU modules. The deployment of multi-channel sensors, AI-enabled processors, and redundant safety features significantly increases the per-unit cost of production. On average, TCS installation adds 8–10% to total vehicle manufacturing costs, limiting adoption among budget and entry-level models. Moreover, technical complexities in integrating TCS with existing braking and transmission architectures slow down scalability, especially for small OEMs. Supply chain disruptions and chip shortages in 2023–2024 further constrained production timelines, reducing flexibility and increasing dependency on high-cost, specialized semiconductor components.

The electrification of mobility and the advent of autonomous driving present major opportunities for the Traction Control System market. Electric vehicles (EVs) rely on precision torque management to prevent wheel spin under high acceleration, boosting the demand for intelligent traction control software. By 2030, over 85% of EVs are projected to integrate adaptive TCS modules with real-time thermal management capabilities. Additionally, autonomous systems require constant stability monitoring—creating synergies with traction systems for smoother navigation and safer driving. Integration with AI-based predictive analytics can improve vehicle control efficiency by 28%, opening new opportunities for Tier-1 suppliers and tech developers specializing in smart mobility solutions.

Evolving global safety standards and a lack of interoperability across vehicle platforms represent a significant challenge for the Traction Control System market. Different regions enforce varying compliance frameworks, such as UNECE and NHTSA mandates, leading to fragmented certification processes and added development costs. Additionally, compatibility issues between legacy braking systems and new traction algorithms delay widespread adoption. The complexity of ensuring cybersecurity resilience and real-time data accuracy in connected traction modules adds another technical layer of difficulty. With over 40% of automotive recalls in 2023 linked to software inconsistencies, manufacturers face mounting pressure to develop standardized and update-friendly systems that balance safety, compliance, and cost-effectiveness.

• Integration of AI-Driven Predictive Traction Systems: The incorporation of artificial intelligence and predictive analytics into traction control systems has grown by over 47% in 2024, significantly improving vehicle stability and control precision. These systems utilize real-time sensor data to predict wheel slip conditions up to 0.3 seconds before occurrence, enhancing responsiveness in electric and autonomous vehicles. Manufacturers have reported up to a 35% reduction in accident probability during dynamic driving scenarios due to adaptive AI-based traction mapping.

• Expansion of Electric Vehicle-Oriented Traction Technologies: With EV sales surpassing 18 million units globally in 2024, nearly 60% of these vehicles were equipped with advanced TCS modules customized for instant torque delivery. New-generation traction systems are designed to manage power surges, offering a 25% increase in energy efficiency compared to conventional internal combustion systems. This shift is driving heavy R&D investments from OEMs, particularly in Asia-Pacific and Europe, where electrification mandates continue to accelerate adoption.

• Advancements in Sensor Fusion and Control Algorithms: The integration of multi-sensor fusion technology in traction control systems rose by 42% in 2024, allowing vehicles to analyze inputs from cameras, gyroscopes, and torque sensors simultaneously. This has resulted in an average 28% improvement in braking accuracy and cornering stability. Automakers are increasingly utilizing machine-learning-based calibration tools to enable continuous optimization and reduce calibration time by up to 20%.

• Growing Emphasis on Sustainable and Lightweight Components: In line with global decarbonization goals, automotive suppliers have introduced traction systems featuring lightweight alloys and recyclable materials, cutting component mass by 15–18%. This design shift contributes to a 12% improvement in vehicle energy consumption and a measurable reduction in lifecycle emissions. Europe currently leads this trend, with more than 45% of new traction system components meeting sustainability and recyclability benchmarks set for 2030.

The Traction Control System (TCS) market is segmented based on type, application, and end-user, each representing distinct technological and functional dimensions. The type segment covers mechanical, electrical, and advanced electronic systems, while the application segment spans passenger vehicles, commercial vehicles, and off-road vehicles. End-user segmentation reflects adoption across automotive OEMs, aftermarket suppliers, and mobility service providers. Passenger vehicles hold a major share due to growing safety mandates and integration of electronic stability controls, accounting for nearly 58% of total installations globally. Meanwhile, electrification and AI integration are driving new opportunities in commercial and autonomous vehicle applications.

Electronic traction control systems currently account for approximately 46% of total market adoption, driven by advancements in sensor integration and vehicle safety automation. These systems offer superior precision and adaptability compared to mechanical or hydraulic variants. Hydraulic traction systems represent around 29% share, primarily in heavy commercial and off-road vehicles where rugged performance is prioritized. Mechanical systems, though declining, retain about 15% of market presence in low-cost and emerging-market vehicles. The fastest-growing type is hybrid-electronic traction systems, projected to expand at a rate of 8.4%, supported by rising demand for EVs and AI-based control algorithms that deliver real-time torque adjustments. Together, niche systems such as all-wheel-drive integrated TCS solutions comprise the remaining 10%.

Passenger vehicles dominate the TCS market with an estimated 58% share in 2024, supported by mandatory safety regulations and advanced driver-assistance system (ADAS) integration. Commercial vehicles follow with around 28%, as logistics operators increasingly adopt traction control for fuel efficiency and fleet safety optimization. Off-road vehicles and agricultural machinery collectively represent about 14% of applications, showing gradual traction due to higher demand for performance stability in extreme terrain. The fastest-growing segment is commercial vehicles, forecasted to grow at 8.1%, driven by the integration of adaptive braking and telematics-based stability solutions. Electric and hybrid vehicle platforms are also accelerating TCS application, given their need for torque balance between independent motors.

Automotive OEMs remain the leading end-users, accounting for nearly 61% of the traction control system installations, primarily due to large-scale vehicle production and increasing regulatory compliance requirements. Aftermarket suppliers represent about 26% share, offering retrofit kits and replacement modules to enhance vehicle performance across aging fleets. Fleet operators and mobility service providers together hold roughly 13% of demand, reflecting rising interest in data-driven traction analytics for predictive maintenance. The fastest-growing end-user group is mobility service providers, expected to expand at a rate of 8.7%, supported by smart fleet digitization and demand for real-time vehicle safety data.

North America accounted for the largest market share at 36.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2025 and 2032.

Europe followed closely with 29.2%, while South America and the Middle East & Africa collectively represented around 11.3% of the total market share. The U.S. remained the top contributing nation due to its robust automotive manufacturing ecosystem, with over 17 million vehicles produced in 2024 featuring traction control technology. Meanwhile, Asia-Pacific’s rapid expansion is driven by increasing vehicle electrification, supported by more than 42 new production facilities commissioned across China, India, and Japan between 2023 and 2024.

How is the region driving innovation and adoption through safety technology mandates and smart mobility integration?

North America captured a 36.4% market share in 2024, driven primarily by the U.S. and Canada’s expanding automotive production and rising safety mandates. Industries such as logistics, defense, and commercial transportation are fueling traction control demand. The National Highway Traffic Safety Administration’s regulations requiring stability control systems in all light vehicles have significantly accelerated adoption. Major manufacturers like BorgWarner are developing advanced integrated traction and torque vectoring systems tailored for electric vehicles. Consumer adoption trends show higher enterprise demand in fleet-based services and EV segments, where reliability and performance are top priorities. Additionally, over 70% of new EV models released in 2024 incorporated next-generation traction systems optimized for AI-based performance analytics.

How are sustainability policies and digitalization shaping the region’s market evolution?

Europe accounted for 29.2% of the global traction control system market in 2024, led by Germany, the UK, and France. The region’s strong focus on road safety, combined with stringent EU emission regulations, has driven consistent integration of advanced traction systems in vehicles. Regulatory frameworks such as Euro NCAP continue to push automakers toward incorporating smart stability controls. Local players, including Continental AG and Bosch, are advancing sensor fusion technologies that improve wheel slip detection accuracy by 19%. European consumers are more inclined toward sustainable mobility, with 61% preferring vehicles equipped with eco-efficient traction systems. The region’s emphasis on regulatory compliance and sustainability is expected to maintain steady innovation momentum.

What factors are propelling rapid expansion in the region’s automotive and EV manufacturing ecosystems?

Asia-Pacific ranked as the fastest-growing market, representing 23.1% of global traction control system installations in 2024. China, Japan, and India are key contributors, supported by large-scale EV manufacturing and smart mobility projects. Over 42% of newly registered electric vehicles in 2024 across the region included AI-driven traction systems. Local manufacturers, such as Denso and Hyundai Mobis, are leading technological integration, focusing on cost-effective embedded sensors and adaptive torque distribution systems. Rapid infrastructure development and government incentives for smart transportation networks are fueling adoption. Consumer behavior trends show increasing preference for advanced safety features, especially in mid-range vehicles, marking a 28% rise in safety-feature purchases between 2023 and 2024.

How is evolving infrastructure and government support influencing regional market growth?

South America accounted for approximately 6.5% of global traction control system demand in 2024, with Brazil and Argentina leading adoption. Expanding automotive production hubs and favorable trade policies under the Mercosur agreement are strengthening supply chains. The Brazilian government’s safety compliance programs are driving wider integration of electronic traction systems in mid-tier vehicle models. Local automakers are investing in low-cost, sensor-based systems to enhance affordability. Infrastructure modernization and growth in logistics and mining sectors have increased regional vehicle deployment by 15% year-on-year. Consumers in this region prioritize durable and low-maintenance systems due to challenging terrain and high operational loads.

How are modernization efforts and smart mobility initiatives shaping technological adoption in this region?

The Middle East & Africa represented 4.8% of the global traction control system market in 2024. Growth is primarily driven by the UAE, Saudi Arabia, and South Africa, where infrastructure modernization and smart city initiatives are promoting advanced vehicular safety technologies. Government programs supporting connected and electric vehicles are encouraging OEM partnerships. Local firms are investing in adaptive traction systems for off-road and desert conditions, improving vehicle stability by 22% under extreme weather. Consumer demand in premium vehicle segments continues to rise, especially in the Gulf region, where luxury car sales grew 18% in 2024.

United States (24%) – Strong automotive production base and extensive integration of advanced driver-assistance technologies across electric and hybrid vehicles.

China (19%) – Rapid expansion of EV manufacturing capacity and large-scale adoption of AI-powered traction systems in both domestic and export-oriented vehicle models.

The global Traction Control System (TCS) market is moderately consolidated, with the top five players accounting for approximately 58% of total market share as of 2024. Around 30–35 active competitors operate across the ecosystem, ranging from Tier 1 automotive suppliers to niche sensor and software developers. Leading companies such as Bosch, Continental AG, Denso Corporation, ZF Friedrichshafen AG, and BorgWarner dominate through extensive R&D investment, estimated at over USD 1.8 billion collectively in 2024. Strategic collaborations between OEMs and electronics suppliers are rising—more than 45 joint development agreements were recorded between 2023 and 2024, focusing on next-generation traction control integration in electric and autonomous vehicles. Innovation trends include the use of AI-based slip prediction, machine learning for adaptive braking response, and IoT-enabled diagnostics for real-time traction monitoring. The market’s competitive nature is reinforced by continuous product differentiation, with more than 60 patent filings related to digital traction and predictive control technology in the last two years. The sector is witnessing growing emphasis on sustainability, where 40% of leading manufacturers now implement recyclable electronic modules and energy-efficient sensors. Overall, competitive intensity is defined by advanced sensor integration, performance optimization, and software-driven mobility solutions shaping the next phase of traction system development.

ZF Friedrichshafen AG

BorgWarner Inc.

Nissin Kogyo Co., Ltd.

WABCO Holdings Inc.

Hitachi Astemo Ltd.

Hyundai Mobis Co., Ltd.

Advics Co., Ltd.

Aptiv PLC

Knorr-Bremse AG

Valeo SA

Mando Corporation

Autoliv Inc.

Technological advancements in the Traction Control System (TCS) market are transforming vehicle stability, efficiency, and performance through the integration of electronic control units, advanced sensors, and AI-based predictive analytics. As of 2024, over 70% of new passenger vehicles globally incorporate electronic traction management systems, a sharp rise from 54% in 2020. This growth is primarily driven by the increased adoption of Electric Stability Control (ESC) and Anti-lock Braking Systems (ABS), which work in tandem with traction control for optimized safety and precision on diverse terrains.

Sensor technology remains at the core of TCS innovation. Modern systems rely on real-time feedback from wheel speed, yaw rate, and throttle position sensors, offering millisecond-level response times that improve handling efficiency by up to 28%. In addition, radar and LiDAR integration is being utilized in next-generation TCS units, allowing adaptive traction response based on surface conditions and driver behavior. The implementation of microcontrollers with enhanced processing capacity—exceeding 120 MHz in modern automotive ECUs—has significantly improved reaction accuracy and reduced power consumption by nearly 15%.

Software and digitalization trends are also accelerating change. Machine learning algorithms enable adaptive traction mapping, where systems self-adjust for road types and weather. Cloud-linked diagnostics are increasingly common, enabling predictive maintenance across fleet vehicles. Moreover, in electric and hybrid vehicles, regenerative braking-based traction systems are reducing brake wear by up to 35%, contributing to sustainability targets. Collectively, these innovations position TCS as a pivotal enabler of intelligent mobility and vehicle automation in the coming decade.

In October 2023, Robert Bosch GmbH announced that its Motorcycle Stability Control (MSC) system, including traction control and IMU-based sensors, would be available on sub-400 cc models, expanding from premium bikes to mainstream segments.

In November 2024, Continental AG developed and deployed an electronic Brake Control System for the 1,600 hp Bugatti Bolide, integrating ABS, ESC and TCS with five driving modes to enhance traction and stability under extreme conditions.

In January 2024, Continental and Aurora Innovation completed the design phase for a scalable autonomous-truck hardware kit including traction control modules, marking a key milestone toward mass production of self-driving freight vehicles. )

In April 2024, Bosch launched a new 2 kW drive control unit for electric two-wheelers that combines drive management with electric traction control and regenerative braking, enabling battery-range extension by up to 8 % in compact EVs.

The Traction Control System market report covers comprehensive segmentation by system type (mechanical linkage, hydraulic modulators, electronic control units and sensors), by vehicle application (passenger cars, light commercial vehicles, heavy commercial vehicles, off-road and two-wheelers), and by end-user channel (OEM new-installations, aftermarket upgrades, and mobility service fleets). Geographically the study spans North America, Europe, Asia-Pacific, South America and Middle East & Africa, examining production capacities, regional technology adoption trends and regulatory frameworks. Technological focus areas include anti-skid sensor integration, torque vectoring modules, software-defined traction management, and AI-driven predictive friction control. Industry focus extends to safety mandates, electric and autonomous mobility integration, lightweight materials, and sustainable manufacturing practices. The report also highlights emerging niche segments such as motorcycle traction control in emerging markets, retrofit systems for older vehicles, and traction modules tailored for vehicle-to-vehicle and vehicle-to-infrastructure connectivity. It is tailored to decision-makers seeking a detailed view of competitive dynamics, technological readiness, segment-specific growth levers, regional entry strategies and strategic investment opportunities in the traction control domain.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 41367 Million |

Market Revenue in 2032 | USD 65933 Million |

CAGR (2025 - 2032) | 6% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Bosch Mobility Solutions, Continental AG, Denso Corporation, ZF Friedrichshafen AG, BorgWarner Inc., Nissin Kogyo Co., Ltd., WABCO Holdings Inc., Hitachi Astemo Ltd., Hyundai Mobis Co., Ltd., Advics Co., Ltd., Aptiv PLC, Knorr-Bremse AG, Valeo SA, Mando Corporation, Autoliv Inc. |

Customization & Pricing | Available on Request (10% Customization is Free) |