Reports

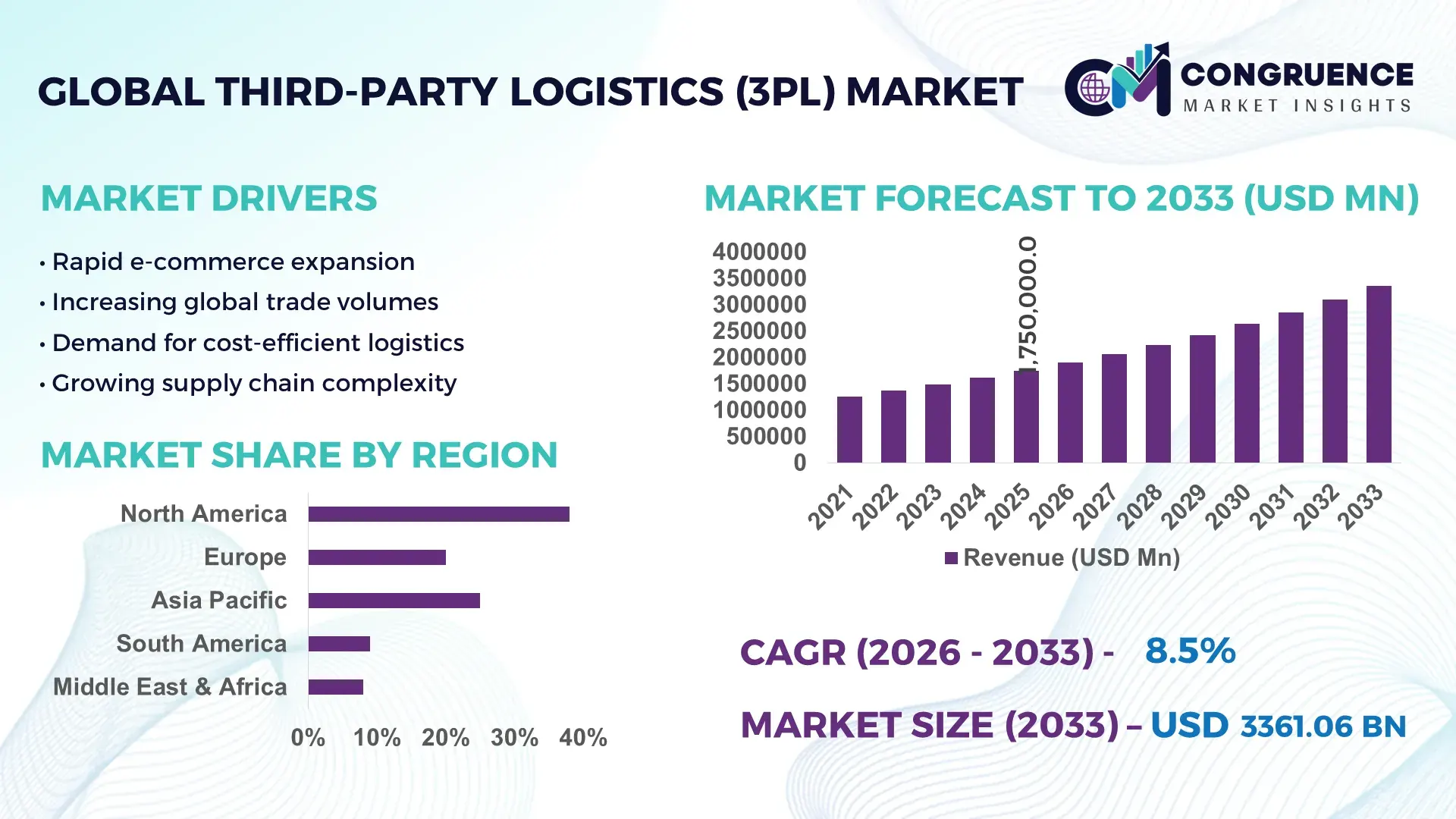

The Global Third-Party Logistics (3PL) Market was valued at USD 1750000 Million in 2025 and is anticipated to reach a value of USD 3361057 Million by 2033 expanding at a CAGR of 8.5% between 2026 and 2033. This growth is primarily driven by increasing global trade volumes and the rapid expansion of e-commerce fulfillment networks.

The United States continues to demonstrate strong operational scale in the Third-Party Logistics (3PL) market, supported by over 20 billion square feet of warehousing space and advanced transportation infrastructure. Investments in automated fulfillment centers have exceeded USD 30 billion over recent years, enabling faster order processing and improved supply chain visibility. Key industry applications span retail, healthcare, and manufacturing, with e-commerce accounting for over 35% of logistics demand. Technological advancements such as robotics integration, AI-powered route optimization, and real-time tracking systems have improved delivery accuracy by nearly 25% and reduced transit times by up to 20%, reinforcing the country’s leadership in operational efficiency and innovation.

Market Size & Growth: Valued at USD 1750000 Million in 2025 and projected to reach USD 3361057 Million by 2033 at 8.5% CAGR, driven by rising e-commerce logistics demand and global supply chain outsourcing.

Top Growth Drivers: E-commerce expansion (45%), supply chain cost optimization (30%), digital logistics adoption (25%).

Short-Term Forecast: By 2028, automation and AI integration are expected to reduce operational costs by 18% and improve delivery speed by 22%.

Emerging Technologies: AI-based route optimization, warehouse robotics, blockchain-enabled supply chain transparency.

Regional Leaders: North America to reach USD 1100000 Million by 2033 with strong tech adoption; Asia-Pacific projected at USD 950000 Million driven by manufacturing hubs; Europe expected at USD 800000 Million with sustainability-led logistics transformation.

Consumer/End-User Trends: Retail and e-commerce dominate with over 50% usage, followed by healthcare and automotive sectors adopting specialized logistics solutions.

Pilot or Case Example: In 2024, a global logistics firm achieved 28% efficiency improvement through AI-powered warehouse automation deployment.

Competitive Landscape: Market leader holds approximately 12% share, followed by major players including global integrated logistics providers and regional specialists.

Regulatory & ESG Impact: Increasing adoption of green logistics practices targeting 30% carbon emission reduction by 2030.

Investment & Funding Patterns: Over USD 120 billion invested globally in logistics infrastructure, automation, and digital platforms.

Innovation & Future Outlook: Growth in autonomous delivery systems, smart warehouses, and integrated digital supply chain platforms shaping next-generation logistics ecosystems.

The Third-Party Logistics (3PL) market is heavily influenced by sectors such as retail, manufacturing, automotive, and healthcare, contributing over 70% of demand collectively. Recent innovations include automated guided vehicles, predictive analytics platforms, and cloud-based transportation management systems that enhance supply chain agility. Regulatory frameworks focusing on carbon emissions and sustainable packaging are reshaping operational strategies, particularly in Europe and North America. Asia-Pacific is witnessing rapid consumption growth due to expanding manufacturing exports and urbanization trends. Emerging trends such as last-mile delivery optimization, cold chain logistics expansion, and omnichannel distribution models are expected to redefine the competitive landscape and operational priorities for logistics providers.

The Third-Party Logistics (3PL) market plays a strategically critical role in modern supply chains by enabling enterprises to enhance efficiency, reduce costs, and improve service delivery through outsourced logistics expertise. Advanced technologies such as AI-driven logistics platforms deliver up to 30% improvement in route optimization compared to traditional manual planning systems, significantly enhancing delivery timelines and operational precision. North America dominates in logistics volume due to extensive infrastructure, while Asia-Pacific leads in adoption with over 60% of enterprises integrating digital logistics solutions into their operations.

By 2028, AI-powered demand forecasting and predictive analytics are expected to improve inventory accuracy by 35% and reduce stockouts by nearly 25%. Sustainability is becoming a core focus, with firms committing to ESG metrics such as achieving 40% reduction in transportation emissions and increasing recyclable packaging usage by 50% by 2030. In 2024, a leading logistics operator in Germany achieved a 20% reduction in fuel consumption through the implementation of smart fleet management systems and electric vehicle integration, demonstrating measurable gains from technology-driven initiatives.

The market is also witnessing a shift toward integrated supply chain ecosystems where real-time data sharing and digital platforms enable seamless coordination among stakeholders. These advancements position the Third-Party Logistics (3PL) market as a foundational pillar for resilient, compliant, and sustainable global trade systems, capable of adapting to evolving economic and environmental challenges.

The exponential growth of e-commerce has significantly increased demand for efficient logistics and fulfillment services, directly driving the expansion of the Third-Party Logistics (3PL) market. Online retail sales now account for over 20% of global retail transactions, requiring scalable warehousing and rapid delivery solutions. 3PL providers are enabling same-day and next-day delivery capabilities through strategically located fulfillment centers and advanced inventory systems. Automation technologies have improved order processing speeds by nearly 40%, while last-mile delivery innovations have reduced delivery times by up to 25%. The surge in cross-border e-commerce has also increased the need for customs handling, freight forwarding, and international logistics expertise, further strengthening the role of 3PL providers in global trade ecosystems.

The Third-Party Logistics (3PL) market faces challenges due to the high capital investment required for infrastructure development, including warehouses, transportation fleets, and digital systems. Establishing automated warehouses can require investments exceeding USD 50 million per facility, limiting entry for smaller providers. Additionally, operational complexities such as managing multi-modal transportation, regulatory compliance, and fluctuating fuel costs create financial and logistical pressures. Labor shortages in warehousing and transportation sectors further exacerbate operational inefficiencies, with vacancy rates in logistics roles exceeding 10% in several developed markets. These factors collectively hinder scalability and profitability, particularly for small and mid-sized logistics providers.

Digital transformation presents significant opportunities for the Third-Party Logistics (3PL) market by enabling enhanced efficiency, transparency, and scalability. The adoption of cloud-based logistics platforms and AI-driven analytics allows companies to optimize routes, reduce fuel consumption by up to 15%, and improve delivery accuracy by over 20%. Emerging technologies such as blockchain enhance supply chain transparency and reduce fraud risks, while IoT-enabled devices provide real-time tracking of goods. The growing demand for cold chain logistics in pharmaceuticals and perishable goods is also creating new revenue streams. Additionally, the integration of autonomous vehicles and drones for last-mile delivery is expected to revolutionize logistics operations, offering faster and cost-effective delivery solutions.

The Third-Party Logistics (3PL) market is increasingly challenged by stringent regulatory frameworks and sustainability requirements. Governments worldwide are implementing stricter emission standards and environmental regulations, requiring logistics providers to invest in cleaner technologies such as electric vehicles and energy-efficient warehouses. Compliance with these regulations can increase operational costs by 10% to 20%, impacting profitability. Additionally, varying international trade regulations and customs procedures complicate cross-border logistics operations. The pressure to achieve carbon neutrality and adopt sustainable practices also necessitates significant investment in green technologies and infrastructure. These challenges require continuous adaptation and innovation, placing additional strain on logistics providers striving to balance cost efficiency with regulatory compliance.

• Rapid Adoption of AI-Driven Logistics Optimization:

Artificial intelligence is transforming operational efficiency across the Third-Party Logistics (3PL) market, with over 65% of large logistics providers deploying AI-based route optimization and predictive analytics tools. These technologies have reduced delivery delays by nearly 28% and improved fleet utilization by approximately 35%. AI-enabled demand forecasting has enhanced inventory accuracy by over 30%, minimizing stockouts and excess inventory. Additionally, machine learning algorithms are helping reduce fuel consumption by 12% to 18%, directly impacting cost efficiency and sustainability goals.

• Expansion of Smart Warehousing and Automation Technologies:

Automation in warehousing is accelerating, with nearly 58% of logistics facilities integrating robotics and automated storage systems. Automated guided vehicles (AGVs) and robotic picking systems have improved order processing speeds by up to 40% and reduced labor dependency by around 25%. Smart warehouses equipped with IoT sensors are enabling real-time inventory tracking, increasing operational visibility by over 50%. Adoption is particularly strong in North America and Europe, where over 60% of new warehouse developments incorporate automation-first designs.

• Surge in Last-Mile Delivery Innovations and Urban Logistics:

Last-mile delivery continues to evolve with increasing urbanization, accounting for nearly 45% of total logistics costs. Over 70% of logistics firms are investing in micro-fulfillment centers and urban distribution hubs to reduce delivery times. Electric delivery vehicles now represent approximately 20% of urban fleets, contributing to a 15% reduction in carbon emissions. Drone and autonomous delivery pilots have demonstrated delivery time reductions of up to 35% in controlled environments, highlighting the shift toward faster and more sustainable logistics models.

• Rising Demand for Sustainable and Green Logistics Solutions:

Sustainability is becoming a central focus, with more than 50% of logistics companies committing to carbon neutrality targets by 2030. Adoption of eco-friendly packaging solutions has increased by 32%, while energy-efficient warehouses have reduced operational emissions by up to 25%. Renewable energy integration in logistics facilities has grown by 20%, particularly in Europe. Additionally, reverse logistics systems for recycling and returns management have expanded by over 27%, reflecting the increasing importance of circular economy practices in the 3PL ecosystem.

The Third-Party Logistics (3PL) market segmentation reflects a diverse and highly specialized industry structure, categorized by service types, application areas, and end-user industries. Transportation services, warehousing, and value-added logistics form the core segmentation by type, each contributing significantly to operational efficiency. Application-wise, sectors such as retail, manufacturing, healthcare, and automotive dominate demand due to their complex supply chain requirements. End-user insights reveal strong adoption among large enterprises, while small and medium-sized businesses are increasingly leveraging outsourced logistics to enhance scalability. Technological integration, regional demand variations, and industry-specific requirements continue to influence segmentation dynamics, with digital transformation and sustainability emerging as key differentiators across all segments.

The Third-Party Logistics (3PL) market is segmented into transportation, warehousing and distribution, dedicated contract carriage, and value-added logistics services. Transportation services currently lead the segment, accounting for approximately 40% of total adoption due to their critical role in freight movement and supply chain connectivity. Warehousing and distribution follow closely with around 30% share, driven by the surge in e-commerce and the need for efficient inventory management. However, value-added logistics services are the fastest-growing segment, expanding at an estimated CAGR of 9.8%, supported by increasing demand for packaging, labeling, and customization services that enhance supply chain flexibility. Dedicated contract carriage and other niche services collectively contribute nearly 30%, serving specialized logistics requirements across industries.

Application segmentation in the Third-Party Logistics (3PL) market is dominated by retail and e-commerce, which account for approximately 50% of total demand due to high-volume order fulfillment and rapid delivery expectations. Manufacturing applications represent around 25%, driven by the need for efficient raw material and finished goods transportation. Healthcare logistics is emerging as the fastest-growing application segment, expanding at an estimated CAGR of 10.5%, fueled by rising demand for cold chain logistics and pharmaceutical distribution. Automotive and other industrial applications collectively contribute nearly 25%, supporting complex global supply chains and just-in-time delivery systems.

End-user segmentation in the Third-Party Logistics (3PL) market highlights retail and e-commerce companies as the leading segment, contributing approximately 45% of total demand due to high shipment volumes and the need for efficient last-mile delivery. Manufacturing industries account for around 30%, relying heavily on logistics providers for supply chain optimization and inventory management. Small and medium-sized enterprises (SMEs) represent the fastest-growing end-user segment, with an estimated CAGR of 11.2%, driven by increasing adoption of outsourced logistics to reduce operational costs and improve scalability. Other sectors, including healthcare, automotive, and consumer goods, collectively contribute nearly 25%, reflecting diverse logistics requirements across industries.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.6% between 2026 and 2033.

North America’s dominance is supported by over 25,000 logistics service providers and more than 20 billion square feet of warehousing capacity, with automation penetration exceeding 60% in major distribution hubs. Europe holds approximately 26% share, driven by strong cross-border trade volumes exceeding 3.5 billion tons annually and sustainability-focused logistics investments. Asia-Pacific accounts for nearly 28% share, supported by high manufacturing output and over 45% of global e-commerce transactions originating from the region. South America contributes around 5%, while the Middle East & Africa collectively account for nearly 3%, with growing investments in logistics infrastructure and trade corridors. Increasing digital adoption, infrastructure expansion, and regional trade agreements are reshaping competitive positioning and accelerating logistics transformation across all regions.

North America holds approximately 38% of the Third-Party Logistics (3PL) market share, driven by strong demand from retail, healthcare, and manufacturing sectors. The region processes over 20 billion shipments annually, supported by highly developed transportation and warehousing infrastructure. Government initiatives promoting supply chain resilience and infrastructure modernization have increased logistics efficiency by nearly 18%. Technological advancements such as AI-driven route optimization and warehouse robotics are adopted by over 65% of logistics providers, significantly improving operational accuracy. A leading regional player has implemented automated fulfillment systems across more than 200 facilities, improving order processing speed by 30%. Consumer behavior in this region shows high enterprise adoption, particularly in healthcare and finance sectors, where precision logistics and real-time tracking are critical.

Europe accounts for approximately 26% of the Third-Party Logistics (3PL) market, with key countries such as Germany, the United Kingdom, and France leading logistics demand. The region handles over 3 billion cross-border shipments annually, supported by integrated transport networks. Regulatory frameworks focusing on carbon neutrality have driven over 55% of logistics companies to adopt green technologies. Electric delivery fleets now represent nearly 18% of urban logistics vehicles. Advanced technologies such as blockchain and IoT tracking systems are used by more than 50% of providers to enhance transparency and compliance. A major regional logistics provider has deployed electric delivery fleets across 120 cities, reducing emissions by 22%. Consumer behavior reflects strong demand for sustainable and transparent logistics solutions, driven by regulatory pressure and environmental awareness.

Asia-Pacific ranks as the fastest-growing region in the Third-Party Logistics (3PL) market, contributing approximately 28% of global demand. Key countries including China, India, and Japan collectively generate over 45% of global e-commerce shipments, driving logistics expansion. The region processes more than 15 billion parcels annually, supported by large-scale manufacturing and export activities. Infrastructure development projects exceeding 1,000 logistics hubs are underway to improve connectivity and efficiency. Technological adoption is rapidly increasing, with over 58% of logistics companies implementing digital platforms and automation tools. A prominent regional logistics provider has introduced AI-powered delivery systems, reducing delivery times by 25%. Consumer behavior is heavily influenced by e-commerce growth and mobile-based purchasing, with over 70% of transactions initiated through digital platforms.

South America holds approximately 5% share of the Third-Party Logistics (3PL) market, with Brazil and Argentina as key contributors. The region manages over 1 billion shipments annually, driven by agriculture, mining, and retail sectors. Infrastructure investments in logistics corridors and port modernization have improved transportation efficiency by nearly 15%. Government trade policies promoting exports have increased cross-border logistics demand by over 12%. Technological adoption remains moderate, with around 35% of providers integrating digital logistics platforms. A regional logistics company has expanded its distribution network by 20% to improve last-mile delivery coverage. Consumer behavior is influenced by growing urbanization and increasing demand for localized delivery services, particularly in metropolitan areas.

The Middle East & Africa region accounts for approximately 3% of the Third-Party Logistics (3PL) market, with the UAE and South Africa leading demand. The region handles over 500 million shipments annually, supported by expanding trade routes and logistics hubs. Investments in smart logistics infrastructure and free trade zones have increased operational efficiency by nearly 20%. Oil & gas, construction, and retail sectors are primary demand drivers. Digital transformation is accelerating, with over 40% of logistics providers adopting automation and tracking technologies. A leading regional logistics provider has implemented smart warehouse systems, improving inventory accuracy by 18%. Consumer behavior reflects increasing demand for fast and reliable delivery services, particularly in urban centers with rising e-commerce penetration.

United States – 32% share: Strong infrastructure, high e-commerce demand, and advanced technology adoption drive dominance in the Third-Party Logistics (3PL) market.

China – 22% share: Large manufacturing base and high-volume e-commerce shipments position China as a key leader in the Third-Party Logistics (3PL) market.

The Third-Party Logistics (3PL) market is highly competitive and moderately fragmented, with more than 10,000 active logistics providers operating globally. The top five companies collectively account for approximately 28% of the market, indicating the presence of numerous regional and specialized players. Large multinational providers dominate through extensive global networks, advanced technological capabilities, and integrated service offerings. Strategic initiatives such as mergers, acquisitions, and partnerships have increased by over 15% in recent years, enabling companies to expand geographic reach and service portfolios. Investment in digital transformation, including AI, IoT, and automation technologies, has become a key differentiator, with over 60% of leading firms deploying smart logistics solutions. Innovation trends such as autonomous delivery systems, blockchain integration, and predictive analytics are reshaping competitive dynamics. Additionally, companies are increasingly focusing on sustainability initiatives, with more than 50% implementing carbon reduction strategies and green logistics practices to align with regulatory requirements and customer expectations.

DHL Supply Chain

Kuehne + Nagel

DB Schenker

XPO Logistics

C.H. Robinson

Nippon Express

DSV A/S

CEVA Logistics

Expeditors International

Ryder System

UPS Supply Chain Solutions

FedEx Logistics

Technology is fundamentally transforming the Third-Party Logistics (3PL) market, with digital integration and automation becoming central to operational efficiency. Over 65% of logistics providers have adopted AI-based systems for route optimization and demand forecasting, enabling delivery time reductions of up to 28% and fuel savings of nearly 15%. Machine learning algorithms are increasingly used to predict shipment delays, improving on-time delivery performance by more than 20%. Additionally, AI-driven warehouse management systems have enhanced inventory accuracy levels to above 98%, significantly reducing stock discrepancies.

Automation technologies such as robotics and automated guided vehicles (AGVs) are deployed in nearly 58% of modern warehouses, improving picking efficiency by up to 40% and reducing labor costs by approximately 25%. Internet of Things (IoT) devices are widely implemented for real-time tracking, with over 70% of shipments now monitored using sensor-based technologies that provide location, temperature, and condition data. Blockchain technology is also gaining traction, with adoption rates exceeding 35% among large logistics firms to enhance transparency and reduce fraud risks in supply chains.

Cloud-based transportation management systems (TMS) are used by more than 60% of logistics providers, enabling centralized data access and improving operational visibility by over 45%. Emerging technologies such as autonomous delivery vehicles and drones are undergoing pilot testing, demonstrating delivery time reductions of up to 35% in controlled environments. Digital twin technology is also being introduced to simulate logistics operations, improving planning efficiency by nearly 30%. These technological advancements are enabling scalable, data-driven logistics ecosystems that enhance efficiency, resilience, and customer satisfaction.

• In March 2025, DHL Supply Chain expanded its robotics deployment across North America and Europe by adding over 2,000 collaborative robots to its warehouse operations, increasing picking productivity by 25% and improving order accuracy across more than 150 fulfillment centers. Source: www.dhl.com

• In September 2024, Kuehne + Nagel launched an advanced digital logistics platform integrating AI-driven predictive analytics, enabling customers to improve supply chain visibility by 40% and reduce shipment delays by approximately 18% across global operations. Source: www.kuehne-nagel.com

• In January 2025, DSV A/S completed the integration of automated warehouse systems in key distribution hubs, enhancing processing capacity by 30% and reducing manual handling requirements across its European logistics network. Source: www.dsv.com

• In July 2024, FedEx Logistics introduced a new real-time shipment tracking solution leveraging IoT sensors, improving tracking accuracy to over 95% and enabling proactive issue resolution for temperature-sensitive shipments. Source: www.fedex.com

The Third-Party Logistics (3PL) Market Report provides a comprehensive analysis of the global logistics ecosystem, covering a wide range of service types, applications, and end-user industries. The report evaluates key segments including transportation services, warehousing and distribution, value-added services, and dedicated contract carriage, collectively representing over 90% of logistics operations. It also examines application-specific demand across retail, manufacturing, healthcare, automotive, and industrial sectors, which together account for more than 75% of total logistics usage.

Geographically, the report spans major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing regional consumption patterns, infrastructure development, and trade dynamics. The study includes insights into over 25 major countries that collectively contribute to global logistics demand, supported by data on shipment volumes, warehouse capacity, and digital adoption rates.

The report further explores technological advancements such as AI, IoT, robotics, blockchain, and cloud-based logistics platforms, which are now adopted by over 60% of leading logistics providers. Emerging segments such as cold chain logistics, last-mile delivery solutions, and reverse logistics are also analyzed, reflecting their growing importance in modern supply chains. Additionally, the report addresses regulatory frameworks, sustainability initiatives, and environmental compliance measures impacting logistics operations.

Overall, the scope encompasses more than 15 key market segments and over 50 performance indicators, offering a detailed and structured view of industry trends, operational benchmarks, and strategic opportunities for stakeholders across the global Third-Party Logistics (3PL) market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

DHL Supply Chain, Kuehne + Nagel, DB Schenker, XPO Logistics, C.H. Robinson, Nippon Express, DSV A/S, CEVA Logistics, Expeditors International, Ryder System, UPS Supply Chain Solutions, FedEx Logistics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |