Reports

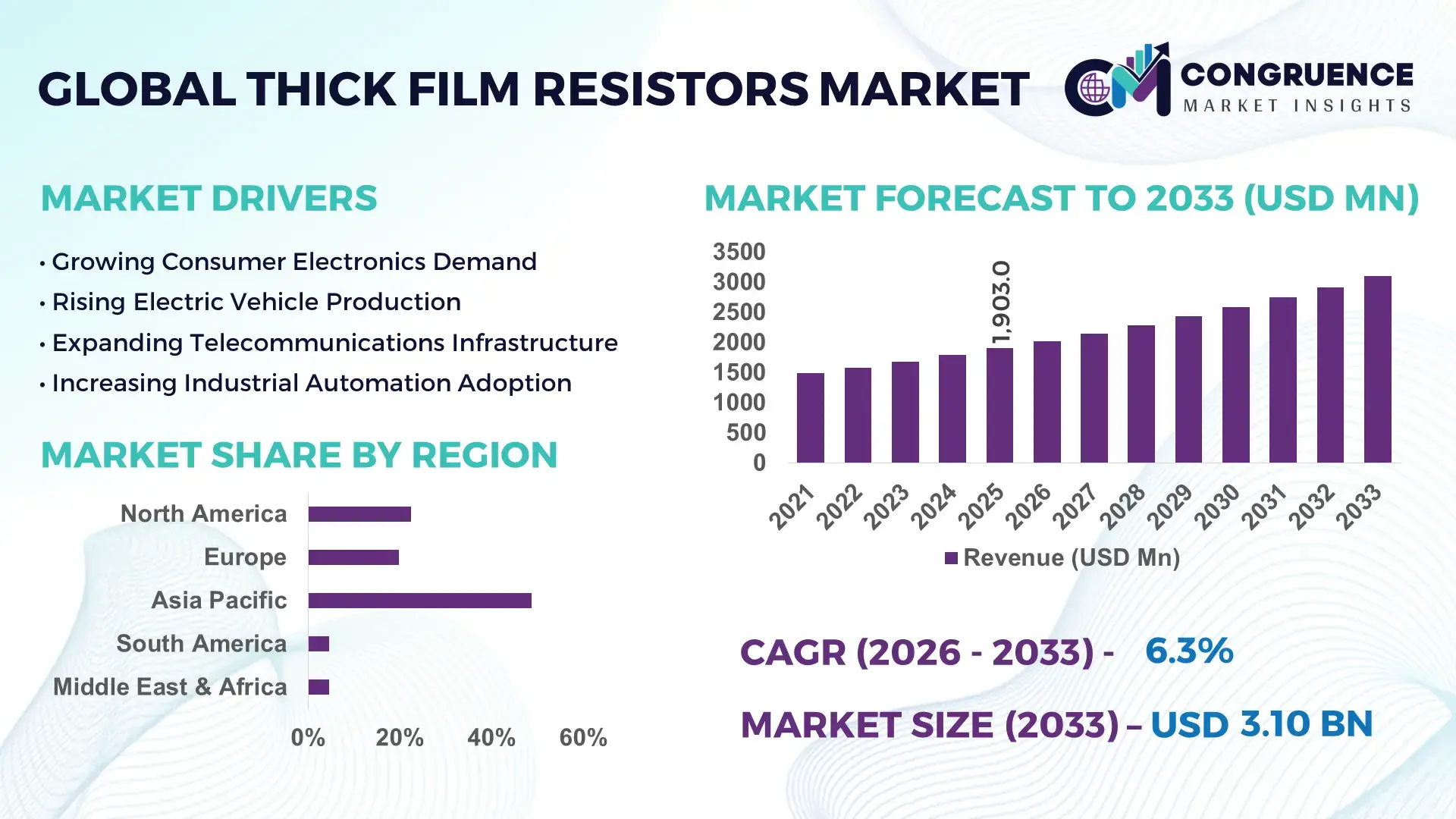

The Global Thick Film Resistors Market was valued at USD 1,903.0 Million in 2025 and is anticipated to reach a value of USD 3,102.5 Million by 2033 expanding at a CAGR of 6.3% between 2026 and 2033. Growth is being accelerated by rising deployment of automotive electronics, EV power control systems, industrial automation modules, and high-density consumer electronics requiring compact, thermally stable resistance components.

China remains the dominant country in the global thick film resistors ecosystem, accounting for nearly 38% of worldwide electronics manufacturing output and over 45% of passive component production capacity. Supported by investments exceeding USD 20 billion in semiconductor and electronic component expansion programs, the country supplies major automotive, telecom, and consumer electronics industries. In comparison, Japan maintains leadership in precision resistor technology with defect rates below 0.5%, while China leads large-scale production efficiency and component integration volumes. Ongoing electronics supply-chain realignment following U.S.-China technology restrictions continues to reshape sourcing strategies across Asia.

Strategically, manufacturers prioritizing automotive-grade reliability, localized production networks, and advanced miniaturization capabilities are positioned to secure stronger long-term procurement contracts.

Market Size & Growth: Valued at USD 1,903.0 million in 2025 and projected to reach USD 3,102.5 million by 2033, supported by a 6.3% CAGR and accelerating EV electronics integration.

Top Growth Drivers: EV electronics adoption (+22%), industrial automation deployment (+18%), and smart consumer device production (+15%) remain the strongest demand catalysts.

Short-Term Forecast: By 2028, automated resistor manufacturing lines are expected to reduce production defects by nearly 20% and improve throughput by 15%.

Emerging Technologies: AI-driven quality inspection, laser trimming systems, and advanced conductive paste materials are improving precision by over 25%.

Regional Leaders: Asia Pacific exceeds USD 1.4 billion demand value, North America approaches USD 520 million, and Europe surpasses USD 430 million, driven by automotive and industrial digitization.

Consumer/End-User Trends: More than 65% of next-generation automotive control units incorporate thick film resistor architectures for power management applications.

Pilot/Case Example: In 2024, a leading electronics manufacturer reported a 17% reduction in component failure rates after implementing AI-assisted resistor inspection systems.

Competitive Landscape: Yageo holds approximately 12% market share, alongside Vishay, KOA, Panasonic, Bourns, and Rohm competing through portfolio expansion.

Regulatory & ESG Impact: Energy-efficiency standards have increased adoption of high-reliability passive components by nearly 14% across industrial equipment platforms.

Investment & Funding: More than USD 8 billion has been committed globally to electronics component manufacturing expansion amid supply-chain diversification initiatives.

Innovation & Future Outlook: Ultra-miniature chip resistors, automotive-grade high-power variants, and smart manufacturing platforms are reshaping competitive differentiation.

The Thick Film Resistors Market is experiencing robust demand across electric vehicles, industrial control systems, telecommunications infrastructure, and advanced consumer electronics. Recent innovations include high-power compact resistor architectures, laser-trimmed precision designs, and enhanced conductive paste formulations that improve thermal stability by over 20%. Manufacturers are also responding to ongoing electronics supply-chain localization efforts and stricter automotive reliability standards, creating new opportunities for value-added component development and strategic ecosystem partnerships.

Thick film resistors have become strategically important as electronics manufacturers pursue higher component density, improved thermal management, and cost-efficient circuit architectures across automotive, industrial, and communications applications. The market is increasingly influenced by semiconductor ecosystem restructuring, regional manufacturing localization, and growing demand for reliable passive components in electrification projects. As global OEMs diversify sourcing networks, resistor suppliers with advanced production capabilities are gaining stronger negotiating power and long-term supply agreements.

Technological improvements are reinforcing competitiveness across the value chain. Modern laser-trimmed thick film resistors achieve resistance tolerances up to 30% tighter than conventional designs while lowering calibration and assembly costs by approximately 15%. China leads production scale and manufacturing capacity, whereas Japan and South Korea maintain advantages in precision engineering and advanced materials expertise. Over the next two to three years, automotive-grade resistor adoption is expected to expand substantially as electric vehicle platforms integrate larger numbers of power management modules and electronic control units.

A practical example is the deployment of high-reliability thick film resistors in battery management systems, where improved thermal performance supports longer component life and greater operational stability. Companies are increasing investments in automation, strategic partnerships, and localized manufacturing facilities to strengthen resilience against geopolitical disruptions. Organizations that combine precision manufacturing, supply-chain flexibility, and application-specific innovation will secure stronger competitive positioning and sustainable long-term relevance.

The strongest growth catalyst is the rapid integration of electronics into electric vehicles, industrial automation equipment, and intelligent consumer devices. Modern electric vehicles contain 20–30% more electronic content than conventional vehicles, while industrial automation investments continue expanding at double-digit rates across major manufacturing hubs. Automotive electronics now account for nearly 40% of passive component consumption in several advanced manufacturing markets. Continued supply-chain restructuring following global semiconductor shortages has encouraged OEMs to secure diversified component sourcing and higher inventory visibility. In response, leading resistor manufacturers are expanding automotive-grade production capacity, investing in automated quality-control systems, and developing high-power miniaturized designs. A notable strategic outcome is the shift toward application-specific resistor platforms that improve design efficiency while strengthening supplier differentiation in increasingly competitive procurement environments.

Fluctuating prices of conductive metals, ceramic substrates, and specialized resistor pastes continue to create operational pressure across the value chain. Material cost swings of 12–18% have periodically compressed margins for component manufacturers, particularly those serving fixed-price automotive contracts. More than 60% of global electronics component production remains concentrated within a limited number of Asian manufacturing corridors, increasing exposure to logistics disruptions and trade-related uncertainties. Recent export-control measures affecting technology and advanced manufacturing equipment have further complicated sourcing decisions. To mitigate these challenges, companies are localizing production footprints, negotiating long-term procurement agreements, and increasing dual-sourcing strategies. The key operational insight is that supply-chain resilience has become as important as manufacturing efficiency when competing for strategic OEM contracts.

Emerging opportunities are being created by advanced vehicle architectures, industrial digitalization, and smart energy infrastructure. Electric vehicle production volumes are expected to represent more than 25% of global vehicle output within the next decade, creating substantial demand for high-reliability passive components. Advanced factory automation deployments have improved equipment productivity by 15–20%, increasing requirements for precision electronic control systems. New conductive materials and enhanced resistor formulations are delivering thermal performance improvements exceeding 20%, supporting wider deployment in demanding operating environments. Manufacturers are responding through R&D partnerships, specialized automotive product lines, and localized engineering support centers. A less obvious opportunity lies in energy storage systems and battery management platforms, where reliability requirements create premium-value component segments with stronger long-term margins.

Maintaining consistent quality across expanding production networks remains a significant execution challenge. Automotive and industrial customers increasingly require defect rates below 1%, tighter resistance tolerances, and extended product traceability throughout the supply chain. At the same time, production automation investments can increase facility upgrade costs by 15–25%, creating pressure on smaller manufacturers. Geopolitical tensions, evolving compliance requirements, and workforce shortages in advanced electronics manufacturing further complicate global scaling strategies. Companies must invest in digital quality-management systems, AI-enabled inspection platforms, and workforce development programs to maintain competitiveness. The critical strategic challenge is balancing cost efficiency with precision manufacturing excellence while ensuring consistent product performance across multiple facilities and international customer programs.

Automotive Electronics Content Expansion Modern electric vehicle platforms now incorporate 25–35% more passive electronic components than conventional vehicles, increasing thick film resistor integration across battery management, power distribution, and thermal monitoring systems. Automotive-grade resistor demand has risen by nearly 18% over the past two years as OEMs prioritize reliability and miniaturization. In response to stricter vehicle safety and functional performance requirements, manufacturers are expanding AEC-qualified product portfolios, automating quality validation workflows, and strengthening partnerships with Tier-1 suppliers to secure long-term design wins.

Precision Miniaturization Accelerates Adoption Electronics manufacturers are rapidly shifting toward compact resistor formats to support high-density PCB architectures. Sub-miniature resistor deployments have increased by approximately 22%, while board-space utilization improvements of 15–20% are being achieved in smartphones, wearables, and industrial controllers. A less obvious outcome is lower assembly complexity and improved thermal distribution within constrained designs. Companies are scaling laser-trimming technologies, investing in advanced conductive materials, and expanding ultra-compact component production to support next-generation electronic device roadmaps.

Supply Chain Localization Strategies Ongoing technology restrictions and logistics disruptions have prompted major OEMs to diversify component sourcing. More than 30% of electronics manufacturers have expanded secondary supplier programs, while localized procurement initiatives have increased by nearly 20% across strategic manufacturing hubs. Countries such as India and Vietnam are attracting new passive-component investments as enterprises seek operational resilience. Companies are restructuring procurement networks, establishing regional manufacturing partnerships, and increasing inventory visibility through digital supply-chain platforms.

Smart Manufacturing Process Integration AI-enabled inspection systems and automated production lines are transforming resistor manufacturing efficiency. Advanced visual inspection platforms have reduced defect detection times by nearly 40%, while production yield improvements exceeding 12% are being reported in highly automated facilities. Labor availability constraints and rising quality expectations are accelerating adoption of these technologies. Manufacturers are investing in machine-learning quality control, predictive maintenance systems, and factory digitization programs to improve throughput, consistency, and operational scalability.

Thick Film Chip Resistors remain the leading segment due to their broad deployment across consumer electronics, automotive control units, industrial automation systems, and telecommunications equipment. The segment accounts for an estimated 55–60% of overall demand, supported by low manufacturing costs, compact form factors, and seamless integration into high-volume surface-mount production environments. Their scalability and compatibility with automated assembly lines make them the preferred choice for OEMs seeking cost-effective circuit protection and signal management. Manufacturers continue expanding production capacity and introducing smaller package sizes to address increasing board-density requirements. Shunt Thick Film Resistors represent the fastest-growing type as electric vehicles, battery systems, and industrial power electronics require more precise current-sensing capabilities. Adoption of shunt variants has increased by approximately 18% as power management architectures become more sophisticated. Meanwhile, Thick Film Power Resistors retain strong relevance in industrial equipment and energy infrastructure, while High Voltage Thick Film Resistors support specialized applications in medical, telecom, and power distribution systems. Companies are prioritizing product innovation, thermal-performance enhancements, and automotive-grade certifications to strengthen positioning across both mature and emerging applications.

Automotive Electronics represents the leading application segment, accounting for approximately 35–40% of global thick film resistor utilization. Increasing electronic content per vehicle, advanced driver assistance systems, battery management platforms, and onboard power electronics continue to expand resistor deployment intensity. Automotive manufacturers are integrating higher volumes of precision passive components to support safety, energy efficiency, and thermal management objectives. Component suppliers are responding through expanded automotive-grade portfolios, localized engineering support, and dedicated qualification programs to meet strict reliability requirements. Electric Vehicles constitute the fastest-growing application area, with resistor content per vehicle increasing by nearly 25% compared with conventional internal combustion platforms. Consumer Electronics remains a mature yet highly significant segment, benefiting from device miniaturization and increasing circuit density. Industrial Equipment applications continue expanding as automation investments rise, while Telecommunications Infrastructure supports stable demand through network modernization initiatives. Companies are scaling production capabilities, optimizing product footprints, and developing application-specific resistor solutions to address evolving operational requirements across these sectors.

Consumer Electronics Manufacturers remain the dominant end-user group, generating nearly 40% of overall procurement demand due to large-scale production of smartphones, computing devices, wearables, and smart home equipment. Their purchasing power is driven by continuous product refresh cycles, compact component requirements, and highly automated assembly operations. To secure supply continuity and cost competitiveness, leading manufacturers increasingly rely on strategic sourcing agreements and long-term supplier partnerships. Component vendors are responding through volume-based production expansion and enhanced miniaturization capabilities. Automotive OEMs represent the fastest-growing end-user category as electrification programs and software-defined vehicle architectures increase demand for advanced passive components. Procurement volumes from automotive buyers have expanded by approximately 18%, supported by rising deployment of battery management and power control systems. Industrial Equipment Manufacturers maintain stable demand linked to automation investments, while Telecommunications Equipment Providers continue upgrading network infrastructure requiring reliable circuit protection and signal management. Companies are targeting these segments through customized product designs, application engineering support, and ecosystem partnerships focused on long-term integration opportunities.

Asia-Pacific accounted for the largest market share at 48.7% in 2025 however, South America is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

North America represents approximately 22.4% of global thick film resistor demand, supported by strong adoption across automotive electronics, aerospace systems, industrial automation equipment, and telecommunications infrastructure. The United States and Mexico continue strengthening regional electronics manufacturing capabilities as supply-chain diversification remains a strategic priority. More than 30% of advanced industrial control systems deployed across the region utilize precision resistor technologies for monitoring and power management applications. Recent investments in semiconductor ecosystem development and electronic component localization have accelerated supplier qualification programs. Manufacturers are increasingly integrating automated testing platforms and digital quality-control systems to improve production consistency while meeting stringent reliability requirements for automotive and industrial customers.

United States Market Outlook: The United States remains the most influential market due to its leadership in aerospace electronics, electric vehicle development, industrial automation, and defense technology. More than 70% of regional electronics R&D spending originates from U.S.-based enterprises, supporting continuous innovation in passive component design and reliability engineering. Growing investments in semiconductor manufacturing facilities and advanced packaging technologies are creating stronger domestic sourcing opportunities for resistor suppliers. Companies are expanding partnerships with automotive OEMs and industrial equipment manufacturers to secure long-term procurement agreements.

Europe accounts for nearly 19.8% of global market activity, supported by strong demand from automotive manufacturing, industrial automation, renewable energy infrastructure, and advanced medical electronics. The region maintains a strategic position in high-reliability component adoption, particularly in Germany, France, and Italy. More than 35% of industrial automation upgrades across major European manufacturing facilities now incorporate advanced monitoring and power-control architectures requiring precision resistor integration. Sustainability regulations and energy-efficiency standards are influencing component selection criteria, encouraging adoption of durable and thermally optimized resistor technologies. Manufacturers are responding through localized engineering support, compliance-focused product development, and increased collaboration with industrial equipment providers.

Germany Market Outlook: Germany serves as the region's primary market due to its dominant automotive manufacturing base, advanced industrial automation ecosystem, and strong engineering expertise. The country contributes roughly 30% of European industrial electronics production and continues expanding smart factory deployments. German manufacturers increasingly prioritize automotive-grade passive components capable of supporting electric mobility systems and Industry 4.0 applications. Strategic investments in manufacturing modernization and energy-efficient industrial infrastructure continue strengthening demand for advanced resistor technologies across multiple end-use sectors.

Asia-Pacific leads the global market with approximately 48.7% share, supported by unmatched electronics manufacturing capacity, extensive supply-chain integration, and strong consumer electronics production. China, Japan, South Korea, and Taiwan collectively account for a substantial portion of global passive component output. More than 60% of worldwide electronics assembly activity occurs within Asia-Pacific manufacturing networks, creating sustained demand for high-volume resistor production. Ongoing investments in semiconductor fabrication, automotive electronics, and industrial automation continue strengthening regional competitiveness. Manufacturers are expanding production footprints, enhancing automation capabilities, and developing advanced miniaturized resistor platforms to support next-generation electronic systems.

China Market Outlook: China remains the largest country-level market due to its extensive electronics manufacturing infrastructure and vertically integrated supply chains. The country contributes more than 45% of global passive electronic component production capacity and continues investing heavily in domestic semiconductor and electronic component ecosystems. Strong demand from electric vehicle manufacturers, telecommunications equipment providers, and consumer electronics producers reinforces market leadership. Companies are accelerating automation upgrades and expanding high-precision manufacturing facilities to improve efficiency, output consistency, and technological self-sufficiency.

South America represents approximately 4.6% of global market participation but is emerging as a strategically important growth center. Industrial modernization initiatives, automotive assembly expansion, and increasing electronics localization efforts are driving component demand. Brazil and Argentina continue attracting investment in manufacturing infrastructure aimed at reducing import dependency and improving supply-chain resilience. Industrial automation deployments have increased by nearly 15% across selected manufacturing sectors, strengthening demand for reliable passive electronic components. While infrastructure constraints and import costs remain challenges, enterprises are actively pursuing partnerships and regional sourcing strategies to improve operational efficiency and procurement stability.

Brazil Market Outlook: Brazil dominates regional demand through its large automotive production base, expanding industrial manufacturing sector, and growing electronics assembly activity. The country accounts for more than 50% of South American industrial output and continues implementing modernization initiatives across key manufacturing industries. Increasing deployment of automated production systems and energy management solutions is creating stronger demand for thick film resistor technologies. Companies are prioritizing supplier partnerships, local distribution expansion, and technical support capabilities to capitalize on evolving industrial requirements.

The Middle East & Africa contributes approximately 4.5% of global demand and is gradually strengthening its position through infrastructure modernization, industrial diversification programs, and technology investment initiatives. Demand is concentrated within telecommunications infrastructure, energy systems, industrial equipment, and transportation projects. Several Gulf countries have increased investments in advanced manufacturing and smart infrastructure deployments, creating new opportunities for electronic component suppliers. More than 20% of recent industrial modernization projects across key Gulf economies incorporate enhanced automation and monitoring technologies requiring precision passive components. Companies are expanding regional distribution networks and technical partnerships to support growing deployment requirements.

Saudi Arabia Market Outlook: Saudi Arabia represents the most strategically significant market within the region due to large-scale industrial diversification initiatives, smart infrastructure development, and manufacturing investment programs. The country continues expanding industrial zones and technology-focused projects aligned with long-term economic transformation objectives. Deployment of advanced energy management systems, industrial automation platforms, and telecommunications infrastructure is increasing component consumption. Ongoing investments in local manufacturing capabilities and digital infrastructure projects are strengthening the operational foundation for future thick film resistor demand across multiple industrial sectors.

The Thick Film Resistors Market is led by global component manufacturers such as Yageo, Vishay Intertechnology, Panasonic Industry, KOA Corporation, and Bourns, which collectively control approximately 45–50% of global market activity. Competition is increasingly defined by global technology leaders competing against regional volume manufacturers, while automotive-qualified suppliers compete directly with cost-focused consumer electronics vendors. Price remains critical in high-volume chip resistor segments, yet performance differentiation is becoming decisive. Automotive-grade products command qualification cycles that are 30–40% longer than standard devices, while advanced laser-trimmed solutions improve resistance accuracy by up to 25%. Manufacturers are expanding production capacity, strengthening OEM partnerships, and integrating automated inspection systems that reduce defect rates by over 15%. The competitive shift is moving toward supply-chain control, miniaturization expertise, and automotive certification capabilities. High capital requirements, qualification barriers, and customer validation timelines create significant entry pressure. Winning requires manufacturing scale, precision engineering, supply reliability, and application-specific innovation rather than price alone.

Vishay Intertechnology, Inc.

Panasonic Industry Co., Ltd.

Bourns, Inc.

Rohm Co., Ltd.

TT Electronics plc

Viking Tech Corporation

Ever Ohms Technology Co., Ltd.

Samsung Electro-Mechanics Co., Ltd.

Ohmite Manufacturing Company

Tateyama Kagaku Industry Co., Ltd.

Riedon Inc.

Susumu Co., Ltd.

Thick film resistor technology is undergoing a transition from conventional screen-printing optimization toward precision-engineered, application-specific platforms. Advanced laser trimming systems now improve resistance accuracy by 20–30% compared with traditional calibration processes while reducing manufacturing rework requirements. More than 60% of automotive-grade resistor production lines utilize automated inspection and trimming technologies to achieve tighter tolerance control. The operational benefit is improved reliability, reduced defect rates, and stronger qualification performance for automotive and industrial customers.

Emerging technologies focus on high-power density architectures, advanced conductive pastes, and ultra-miniaturized resistor formats. New material formulations improve thermal stability by approximately 15–20%, while compact package designs reduce board-space requirements by nearly 25%. Compared with legacy resistor technologies, modern laser-trimmed thick film solutions deliver up to 30% better precision and 15% lower assembly complexity. Automotive OEMs, telecommunications equipment providers, and industrial automation manufacturers benefit most from these advancements due to increasing circuit density requirements.

Between 2026 and 2028, AI-assisted quality inspection, predictive manufacturing analytics, and smart factory integration will become stronger competitive differentiators. Adoption rates for automated visual inspection systems are expected to exceed 70% among leading manufacturers. Companies investing early in advanced materials, automation platforms, and digital production environments will secure faster qualification cycles, stronger customer retention, and improved operational scalability.

April 2025 – Vishay Intertechnology launched the MCB ISOA200 thick film power resistor with optional NTC monitoring and power dissipation up to 200 W, enabling reduced board space and improved thermal management for EV, industrial, and aerospace applications. Source: www.ir.vishay.com

May 2025 – Vishay Intertechnology expanded its D2TO35 series with an automotive-grade thick film power resistor delivering 30% higher energy absorption and 35 W power dissipation, strengthening protection against transient pulses in next-generation vehicle electronics.

July 2025 – Bourns, Inc. introduced the Riedon PF2270 Series thick film resistor platform featuring up to 300 W power dissipation with heatsink support, targeting battery energy storage systems, motor drives, and industrial power conversion applications.

November 2025 – Vishay Intertechnology released the AEC-Q200-qualified LTA 30 thick film power resistor supporting 500 V operating voltage and enhanced overload capability, improving durability for battery management systems and electric vehicle power-control architectures.

The report provides comprehensive coverage of the Thick Film Resistors Market across major product categories, applications, end-user industries, and regional ecosystems. Analysis includes Thick Film Chip Resistors, Shunt Thick Film Resistors, Power Thick Film Resistors, and High Voltage Thick Film Resistors, with detailed evaluation of adoption patterns across automotive electronics, electric vehicles, industrial equipment, telecommunications infrastructure, and consumer electronics. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing more than 95% of global deployment activity.

The study examines manufacturing trends, supply-chain developments, technology adoption rates, and competitive positioning among leading component suppliers. More than 60% of industry demand is linked to automotive and electronics manufacturing ecosystems, making operational resilience and product qualification critical investment considerations. The report supports strategic decision-making through segmentation insights, regional opportunity mapping, technology benchmarking, competitive analysis, and forward-looking assessment of emerging application areas expected to influence market direction between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,903.0 Million |

| Market Revenue (2033) | USD 3,102.5 Million |

| CAGR (2026–2033) | 6.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Yageo Corporation; Vishay Intertechnology, Inc.; KOA Corporation; Panasonic Industry Co., Ltd.; Bourns, Inc.; Rohm Co., Ltd.; TT Electronics plc; Viking Tech Corporation; Ever Ohms Technology Co., Ltd.; Samsung Electro-Mechanics Co., Ltd.; Ohmite Manufacturing Company; Tateyama Kagaku Industry Co., Ltd.; Riedon Inc.; Susumu Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |