Reports

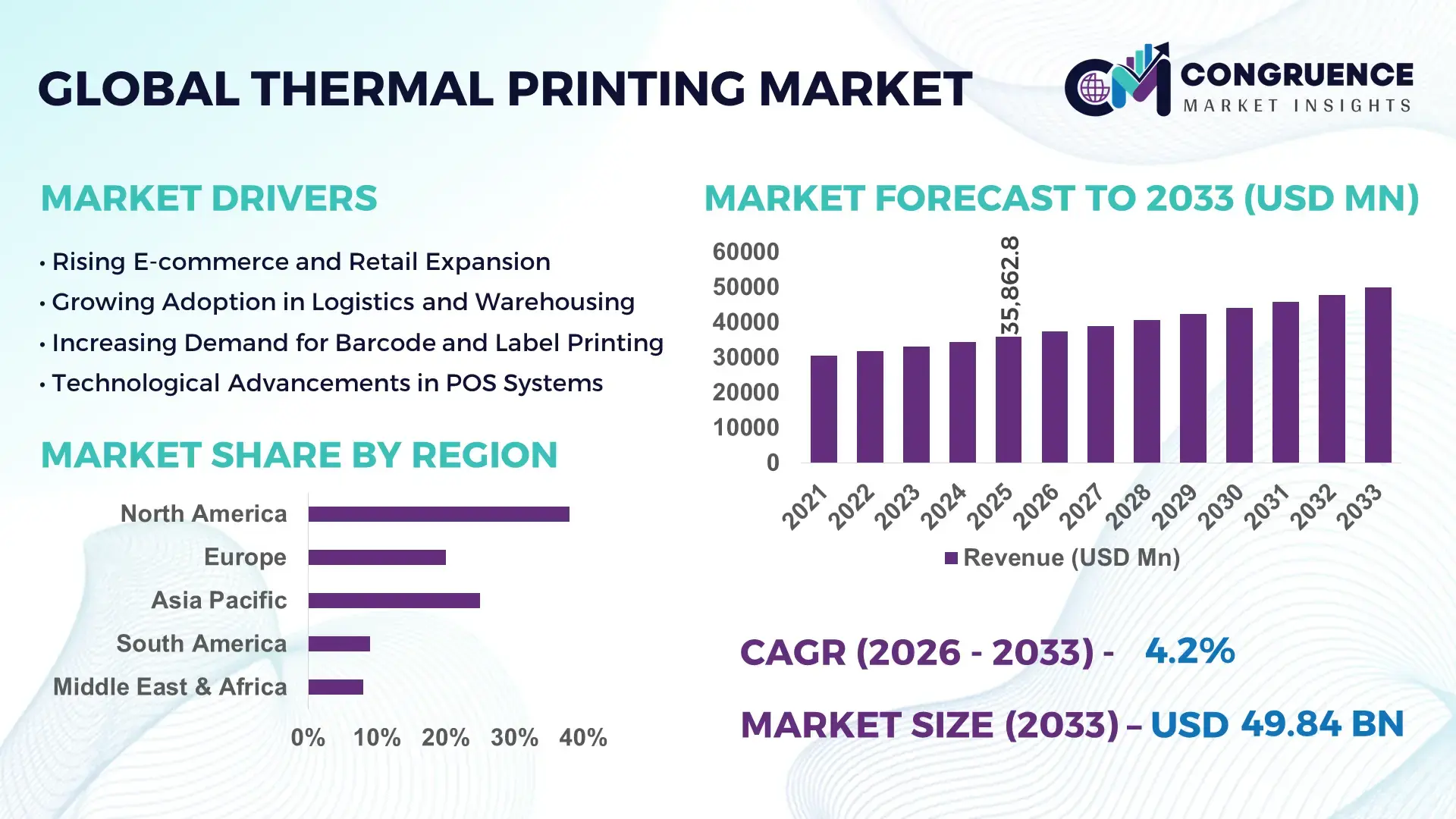

The Global Thermal Printing Market was valued at USD 35862.78 Million in 2025 and is anticipated to reach a value of USD 49840.88 Million by 2033 expanding at a CAGR of 4.2% between 2026 and 2033. This growth is primarily driven by accelerating demand for high-speed barcode labeling, logistics automation, and durable on-demand printing across retail and healthcare environments.

The United States maintains a strong position in the global thermal printing ecosystem with over 30% of installed industrial thermal printer capacity concentrated in North America. The country hosts advanced production facilities integrating high-resolution printheads exceeding 600 dpi and IoT-enabled fleet management systems. More than 75% of large retail chains in the U.S. utilize thermal receipt and label printers for POS and supply chain tracking applications. Annual investments in smart warehouse automation surpassed USD 4 billion in 2024, directly supporting demand for mobile thermal printers and ruggedized industrial labeling solutions. Healthcare adoption is equally significant, with over 80% of hospitals using direct thermal wristband printers for patient identification and specimen labeling, reinforcing high-volume domestic consumption and innovation intensity.

Market Size & Growth: Valued at USD 35,862.78 Million in 2025, projected to reach USD 49,840.88 Million by 2033 at 4.2% CAGR, driven by rapid warehouse digitization and barcode-based inventory optimization.

Top Growth Drivers: 68% retail POS penetration, 54% logistics automation adoption, 47% healthcare labeling compliance implementation.

Short-Term Forecast: By 2028, smart thermal printer integration is expected to reduce labeling errors by 22% and improve print efficiency by 18%.

Emerging Technologies: Cloud-connected thermal printing systems, RFID-integrated label printing, and AI-based predictive maintenance tools.

Regional Leaders: North America projected at USD 16 Billion by 2033 with high retail automation; Asia-Pacific nearing USD 18 Billion driven by e-commerce logistics expansion; Europe approaching USD 11 Billion supported by regulatory labeling standards.

Consumer/End-User Trends: High adoption among 3PL providers, hospital networks, and omnichannel retailers requiring real-time tracking.

Pilot Case Example: In 2024, a multinational logistics operator achieved 25% downtime reduction through AI-enabled thermal printer fleet analytics.

Competitive Landscape: Market leader holds approximately 28% share, followed by four major global manufacturers specializing in industrial and mobile printing systems.

Regulatory & ESG Impact: Sustainable linerless labels and BPA-free thermal paper regulations accelerating eco-compliant product transitions.

Investment & Funding Patterns: Over USD 1.2 Billion invested in smart labeling automation and RFID-print integration projects in the past two years.

Innovation & Future Outlook: Expansion of battery-efficient mobile printers and cloud-managed enterprise printing platforms shaping scalable digital labeling infrastructure.

The Thermal Printing Market serves critical sectors including retail, logistics, healthcare, manufacturing, and transportation. Retail and e-commerce logistics collectively contribute over 45% of total equipment deployment due to barcode labeling and receipt printing needs. Direct thermal printers account for substantial adoption in shipping labels, while thermal transfer printers dominate industrial durability applications. Recent innovations such as antimicrobial thermal coatings, high-speed 14-inch-per-second industrial printers, and integrated RFID encoding modules are transforming performance benchmarks. Regulatory mandates for traceability in pharmaceuticals and food supply chains further reinforce consistent demand. Asia-Pacific consumption continues to accelerate due to cross-border e-commerce expansion, while European markets emphasize eco-friendly linerless label adoption. Forward-looking investments in smart warehouse infrastructure and Industry 4.0 automation are expected to sustain long-term enterprise-grade thermal printing deployments.

The Thermal Printing Market holds strategic relevance as enterprises modernize supply chains, automate retail checkout systems, and implement regulatory-compliant labeling frameworks. Advanced thermal transfer printing delivers 35% longer label durability compared to legacy inkjet-based labeling systems in high-temperature industrial environments. Meanwhile, RFID-integrated thermal printing reduces manual scanning time by nearly 30% compared to traditional barcode-only systems, enhancing operational throughput.

Asia-Pacific dominates in volume manufacturing of thermal printing hardware, while North America leads in enterprise adoption, with over 72% of large-scale distribution centers deploying networked thermal printer fleets. By 2028, AI-driven predictive maintenance tools integrated into smart thermal printers are expected to cut unplanned downtime by 20% and improve consumable utilization efficiency by 15%.

From an ESG perspective, firms are committing to sustainability metrics such as 40% recyclable packaging materials and 25% reduction in chemical-coated thermal paper usage by 2030. In 2024, a leading Japanese electronics manufacturer achieved 18% energy consumption reduction in industrial thermal printers through low-power printhead engineering and optimized firmware algorithms. Strategically, organizations are aligning thermal printing investments with warehouse robotics, cloud-based ERP integration, and real-time inventory analytics. These developments position the Thermal Printing Market as a critical infrastructure pillar supporting compliance-driven labeling, operational resilience, and sustainable digital transformation across global industries.

Global e-commerce shipments have grown by more than 20% over the past three years, significantly increasing demand for high-speed label printing solutions. Large fulfillment centers process over 500,000 packages daily, requiring durable barcode labels printed at speeds exceeding 12 inches per second. Thermal printers eliminate ink and toner costs, reducing consumable maintenance by approximately 30% compared to conventional printing technologies. The integration of warehouse management systems with networked thermal printers ensures real-time order processing and minimizes labeling errors by nearly 25%. As same-day and next-day delivery models expand across urban regions, scalable and mobile thermal printing solutions are becoming indispensable for operational continuity and supply chain efficiency.

Certain thermal papers historically contained chemical coatings such as BPA, raising regulatory scrutiny in Europe and North America. Compliance with evolving environmental directives has increased material reformulation costs for manufacturers. BPA-free and phenol-free thermal papers can cost 10–15% more than conventional alternatives, impacting procurement budgets for high-volume retailers. Additionally, concerns over recyclability of coated paper materials limit adoption in sustainability-focused enterprises. Some organizations are shifting toward digital receipts and paperless billing systems, reducing demand for POS thermal receipt printing. These environmental and regulatory pressures create transitional challenges for suppliers adapting product lines to meet stricter compliance standards.

Smart warehouses integrating robotics and IoT sensors create significant opportunities for advanced thermal printing systems. Over 60% of newly built distribution centers incorporate automated sorting and real-time inventory tracking, requiring synchronized label generation. RFID-enabled thermal printers allow simultaneous encoding and printing, reducing manual scanning steps by nearly 35%. Cloud-managed printer fleets enable centralized diagnostics, lowering maintenance response time by 20%. Emerging markets investing in cross-border trade infrastructure are rapidly deploying mobile thermal printers for customs labeling and freight documentation. These automation-driven requirements open new revenue streams in industrial-grade, wireless, and ruggedized thermal printing segments.

Thermal printer manufacturing depends on precision printheads, semiconductor controllers, and specialized heating elements. Fluctuations in semiconductor supply have previously extended lead times by up to 12 weeks. Rising raw material costs for aluminum frames and high-grade plastics have increased production expenses by nearly 8–12% in certain periods. Logistics bottlenecks also affect global distribution of finished hardware. Small and medium enterprises may delay capital equipment upgrades during cost volatility phases. Furthermore, integration complexity with legacy enterprise software systems can extend deployment timelines, increasing total implementation costs and posing operational challenges for end-users adopting next-generation thermal printing infrastructure.

• Expansion of Mobile and Handheld Printers: Mobile thermal printers are increasingly deployed in logistics, retail, and field service operations, with over 68% of distribution centers integrating portable devices by 2025. Handheld models now support wireless connectivity and 10-hour battery life, reducing label downtime by 27% compared to stationary printers. North America and Asia-Pacific are leading adoption, driven by last-mile delivery optimization and mobile point-of-sale solutions.

• Integration of RFID and Smart Labeling: Thermal printers with RFID encoding capabilities are gaining traction, with adoption rates rising to 42% in industrial and warehouse environments. This integration allows for real-time inventory tracking, cutting manual scanning efforts by 33% in large-scale fulfillment centers. Europe has seen a 50% increase in RFID-enabled thermal printer deployments over the last two years, emphasizing compliance with traceability regulations in pharmaceuticals and food logistics.

• Eco-Friendly and Sustainable Printing Materials: Over 60% of new thermal paper purchases in 2024 were BPA-free or recyclable, responding to growing regulatory and ESG pressures. Companies in Europe and North America report a 15–20% reduction in paper waste through linerless label solutions. Adoption of environmentally safe materials is now a key procurement criterion for retailers and healthcare providers seeking sustainable supply chain practices.

• Cloud-Connected and AI-Enabled Printers: Networked thermal printers with cloud management platforms are implemented in 35% of smart warehouses globally. These systems reduce maintenance response times by 22% and improve consumable utilization efficiency by 18%. Predictive analytics embedded in AI-enabled printers forecast printhead wear and optimize label quality, accelerating operational reliability for enterprises with high-volume printing demands.

The Thermal Printing Market is segmented by product type, application, and end-user, reflecting the diverse operational needs across industries. By type, direct thermal printers dominate due to their low maintenance and high-speed output, while thermal transfer printers are preferred in industrial labeling requiring durability. Applications range from retail POS and shipping labels to healthcare specimen tracking and manufacturing inventory, with retail and logistics comprising the largest adoption share. End-users include large-scale e-commerce fulfillment centers, hospitals, and manufacturing units, with early adoption of mobile and IoT-connected printers driving operational efficiency. Emerging sectors, such as pharmaceuticals and smart warehouses, are leveraging advanced thermal printing solutions for compliance, traceability, and automation. Geographic adoption varies, with North America emphasizing enterprise integration, Europe prioritizing sustainability, and Asia-Pacific focusing on high-volume logistics and mobile printing deployments. Overall, segmentation highlights the interplay between technology, industry requirements, and regional consumption patterns shaping market growth.

Direct thermal printers are currently the leading type, accounting for approximately 48% of adoption due to their low maintenance requirements, fast printing speeds, and suitability for retail and logistics labeling. Thermal transfer printers hold around 30% share and are preferred for industrial applications requiring durable labels that resist heat, chemicals, and abrasion. The fastest-growing type is mobile and handheld thermal printers, which have seen adoption increase by 26% over the past three years due to rising demand in last-mile delivery and field service operations. Other types, including kiosk and specialized industrial printers, contribute a combined 22% share, serving niche requirements in sectors like healthcare, food traceability, and high-resolution barcode printing.

Retail point-of-sale applications dominate the market, currently accounting for 45% of global deployment, driven by widespread adoption of receipts, price tags, and loyalty card printing. Shipping and logistics applications hold 28% share, benefiting from automated warehouse labeling and parcel tracking systems. The fastest-growing application is healthcare labeling, projected to expand rapidly due to increasing adoption of patient wristband and specimen tracking systems, improving compliance and safety protocols. Other applications, such as manufacturing inventory labeling and ticketing services, collectively contribute 27% of the market, serving specialized operational requirements.

Large-scale e-commerce and logistics companies are the leading end-users, accounting for approximately 52% of total thermal printer adoption. Their reliance on automated labeling and real-time shipment tracking drives continuous demand for high-speed, durable printers. The fastest-growing end-user segment is healthcare institutions, with adoption rates increasing by 29% due to regulatory mandates for patient identification and specimen labeling. Other end-users, including manufacturing plants, retail chains, and field service providers, collectively account for 19% of market usage. Industrial and logistics sectors maintain high deployment efficiency, with over 70% of top-tier warehouses incorporating mobile or IoT-enabled thermal printers into daily operations.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

North America continues to lead in enterprise adoption, with over 75% of healthcare facilities and 68% of retail chains utilizing thermal printing solutions. The region saw over 2.5 million thermal printers deployed across logistics, retail, and industrial operations in 2025. Meanwhile, Asia-Pacific investment in smart warehouse and e-commerce labeling technologies reached USD 3.2 billion, driving rapid deployment of mobile and IoT-connected printers. Europe accounted for 23% of the market in 2025, with regulatory-compliant and eco-friendly adoption surging. South America and Middle East & Africa collectively held 16% of the global market, with rising demand in media, shipping, and oil & gas sectors. Global parcel handling volumes exceeding 160 billion units annually have further amplified thermal printer deployment, especially in logistics-intensive regions.

How are technological advancements and regulatory trends reshaping adoption?

North America holds a market share of approximately 38%, driven primarily by high adoption in healthcare, retail, and logistics. Hospitals are increasingly using direct thermal printers for patient wristbands and specimen labeling, while retail chains deploy mobile and POS thermal printers to optimize checkout efficiency. Government initiatives supporting automation and digital compliance have accelerated adoption of smart, cloud-connected printing systems. Technological advancements include IoT-enabled fleet management, predictive maintenance, and energy-efficient printheads. Local players such as Zebra Technologies have introduced AI-integrated mobile printers, reducing labeling errors by 22% across distribution centers. North American enterprises prioritize high-speed printing and reliability, with over 70% of warehouses integrating wireless or mobile solutions to meet evolving operational needs.

What is driving regulatory and sustainable innovation in printing solutions?

Europe commands a 23% market share, with key markets including Germany, the UK, and France leading adoption. Regulatory compliance for traceability, food safety, and chemical-free labeling has driven demand for BPA-free and recyclable thermal papers. Companies are embracing emerging technologies, including RFID-enabled thermal printers and cloud-managed enterprise solutions. Local players like TSC Auto ID are expanding production of eco-friendly thermal printing solutions to meet stringent European standards. Regional consumer behavior emphasizes explainable and sustainable printing solutions, with over 60% of large-scale retailers and manufacturers incorporating energy-efficient devices and linerless label systems into their operations.

How is e-commerce and mobile adoption driving rapid expansion?

Asia-Pacific accounts for 27% of the global market by volume, with top-consuming countries including China, India, and Japan. Rapid expansion of e-commerce, smart warehouse infrastructure, and industrial labeling is fueling high-volume deployment. Technological innovation hubs in China and Japan are integrating mobile AI applications, IoT-connected printers, and RFID labeling systems to enhance operational efficiency. Local players such as Sato Holdings have launched AI-powered thermal printers for logistics and retail applications, improving label accuracy by 18% in urban centers. Regional consumer behavior is highly driven by mobile printing, on-demand labeling, and fast-growing e-commerce logistics networks.

What factors are driving localized printing adoption in media and commerce?

South America holds roughly 9% of the thermal printing market, with Brazil and Argentina as leading contributors. Growth is supported by logistics, media distribution, and retail sectors requiring localized labeling and language-specific printing solutions. Government incentives for digital transformation in logistics and retail have accelerated adoption, with over 400,000 units deployed in key urban centers by 2025. Local players are developing mobile and high-durability printers for transportation hubs. Regional consumer behavior favors multilingual label printing, durable POS receipts, and small-scale industrial applications, reflecting diverse operational and linguistic needs across countries.

How is industrial modernization influencing regional printing trends?

Middle East & Africa contribute approximately 7% of the market, with the UAE and South Africa as major growth countries. Demand is driven by oil & gas, construction, and logistics sectors requiring durable industrial labeling and on-site printing solutions. Technological modernization includes AI-enabled printers, IoT connectivity, and cloud-based management systems. Trade partnerships and regulatory incentives are supporting deployment of sustainable thermal printing solutions. Local players are adopting mobile and ruggedized printers for high-temperature and outdoor environments, while consumer behavior emphasizes durability and field-ready devices for industrial operations.

United States – 38% market share; dominance due to high production capacity, enterprise adoption, and advanced logistics infrastructure.

China – 27% market share; leading due to rapid e-commerce growth, manufacturing output, and mobile printing deployment.

The Thermal Printing Market is moderately consolidated, with approximately 60 active competitors globally, and the top five companies collectively holding around 65% of total market presence. Leading players focus on product innovation, strategic partnerships, and expanding IoT and AI capabilities. Companies such as Zebra Technologies, Sato Holdings, Toshiba TEC, Epson, and Honeywell have introduced cloud-connected and mobile thermal printers, integrated RFID capabilities, and predictive maintenance solutions to strengthen their market positioning. Product launches in 2024-2025 focused on eco-friendly materials, energy efficiency, and high-resolution industrial printing. Mergers and regional alliances have enabled local distribution expansion, particularly in Asia-Pacific and Europe. Market fragmentation remains significant in emerging regions, allowing new entrants to capture niche applications such as healthcare specimen labeling, mobile POS, and smart warehouse automation. Global parcel and retail transaction volumes exceeding 160 billion annually continue to create opportunities for differentiation through speed, reliability, and advanced monitoring technologies. Overall, innovation-driven competition is shaping enterprise deployment and long-term adoption strategies across all regions.

Zebra Technologies

Sato Holdings

Toshiba TEC

Epson Corporation

Honeywell International

TSC Auto ID Technology

Bixolon Co., Ltd.

Brother Industries, Ltd.

Printronix Auto ID

Godex International Co., Ltd.

The Thermal Printing Market is being reshaped by a wave of current and emerging technologies that enhance performance, connectivity, sustainability, and integration with enterprise systems. A significant technological shift is the integration of smart connectivity features such as cloud management, IoT, and real-time analytics. Modern thermal printers equipped with secure wireless interfaces, predictive diagnostics, and remote fleet management platforms enable enterprises to monitor device health and consumable usage across hundreds or thousands of units, reducing unplanned service calls and improving uptime. Networked printers now support Bluetooth 5.0, Wi-Fi 6, and NFC pairing for seamless integration with mobile devices and point-of-sale systems, enhancing operational flexibility across retail, logistics, and hospitality environments.

In addition to connectivity advancements, high-resolution thermal printheads exceeding 600 dots per inch (dpi) are being adopted to provide crisp barcode, QR code, and text output necessary for compliance tracking and traceability in healthcare and pharmaceuticals. This precision supports complex label formats and scannability requirements, especially in regulated supply chains and serialized labeling workflows. Automated media detection and adaptive print optimization technologies are also reducing material waste by adjusting thermal energy based on label size and thickness.

Sustainability-oriented innovations are reducing the environmental footprint of thermal printing. Energy-efficient drive systems and low-power thermal engines enable printers to operate on single-cell Li-ion batteries, lowering energy costs for mobile deployments. Eco-friendly materials, such as recyclable thermal papers and linerless label options, are gaining traction as organizations prioritize waste reduction. Emerging technologies like integrated RFID encoding and enhanced cloud print services are enabling hybrid workflows that combine visual and electronic identification, improving inventory accuracy and automation. RFID-capable thermal printers can encode smart tags on labels during the print process, cutting manual encoding steps and increasing throughput in warehouse operations.

• In August 2025, Kyocera launched its TPA Series thermal printhead for high-speed, eco-friendly portable POS systems with print speeds up to 350 mm/sec, enhancing durability and recyclable paper support for retail applications.

• In January 2025, Epson introduced the TM-T20IV Thermal Receipt Printer designed for seamless integration with both PC-POS and mPOS systems, featuring flexible connectivity, 250 mm/sec print speed, and paper-saving capabilities reducing usage by up to 30%.

• In December 2024, BIXOLON America Inc. unveiled the SRP-Q300II Next Generation Cube Printer tailored for retail and hospitality sectors, offering enhanced performance and compact design to meet evolving enterprise printing requirements.

• In October 2024, HPRT announced plans to showcase a lineup of new thermal receipt printers at the China Business Informatization Industry Conference, highlighting advancements in retail and food service printing technologies.

The scope of the Thermal Printing Market Report encompasses a comprehensive analysis of product segments, application areas, geographic regions, and emerging technological and industry trends shaping the market landscape. By product type, the report examines direct thermal, thermal transfer, and hybrid variants including mobile, desktop, industrial, and RFID-enabled printers, highlighting unit volumes, adoption patterns, and performance benchmarks aligned with evolving enterprise needs. It further delineates applications across retail POS, barcode and shipping label printing, healthcare specimen and wristband labeling, ticketing, and specialized industrial use cases requiring high-resolution output and rugged performance.

Geographically, the report covers major regional markets including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering unit shipment data, adoption trends, and consumption drivers specific to local infrastructure, regulatory frameworks, and end-user preferences. Technology-focused segments examine connectivity protocols such as Bluetooth, Wi-Fi, and NFC; cloud-based print management systems; IoT-enabled diagnostic tools; and RFID integration for smart labeling workflows. Environmental sustainability dimensions analyze the adoption of recyclable thermal media, linerless labels, energy-efficient printers, and waste reduction mechanisms promoted by corporate ESG strategies. Emerging niche focus areas include hybrid printers capable of simultaneous RFID encoding and thermal output, AI-enhanced predictive maintenance platforms, and compact mobile printers designed for last-mile logistics and field operations. The report provides decision-makers with an in-depth view of competitive offerings, deployment scenarios, and innovation trajectories, supporting strategic planning across enterprise, retail, healthcare, and industrial sectors.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Zebra Technologies, Sato Holdings, Toshiba TEC, Epson Corporation, Honeywell International, TSC Auto ID Technology, Bixolon Co., Ltd., Brother Industries, Ltd., Printronix Auto ID, Godex International Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |