Reports

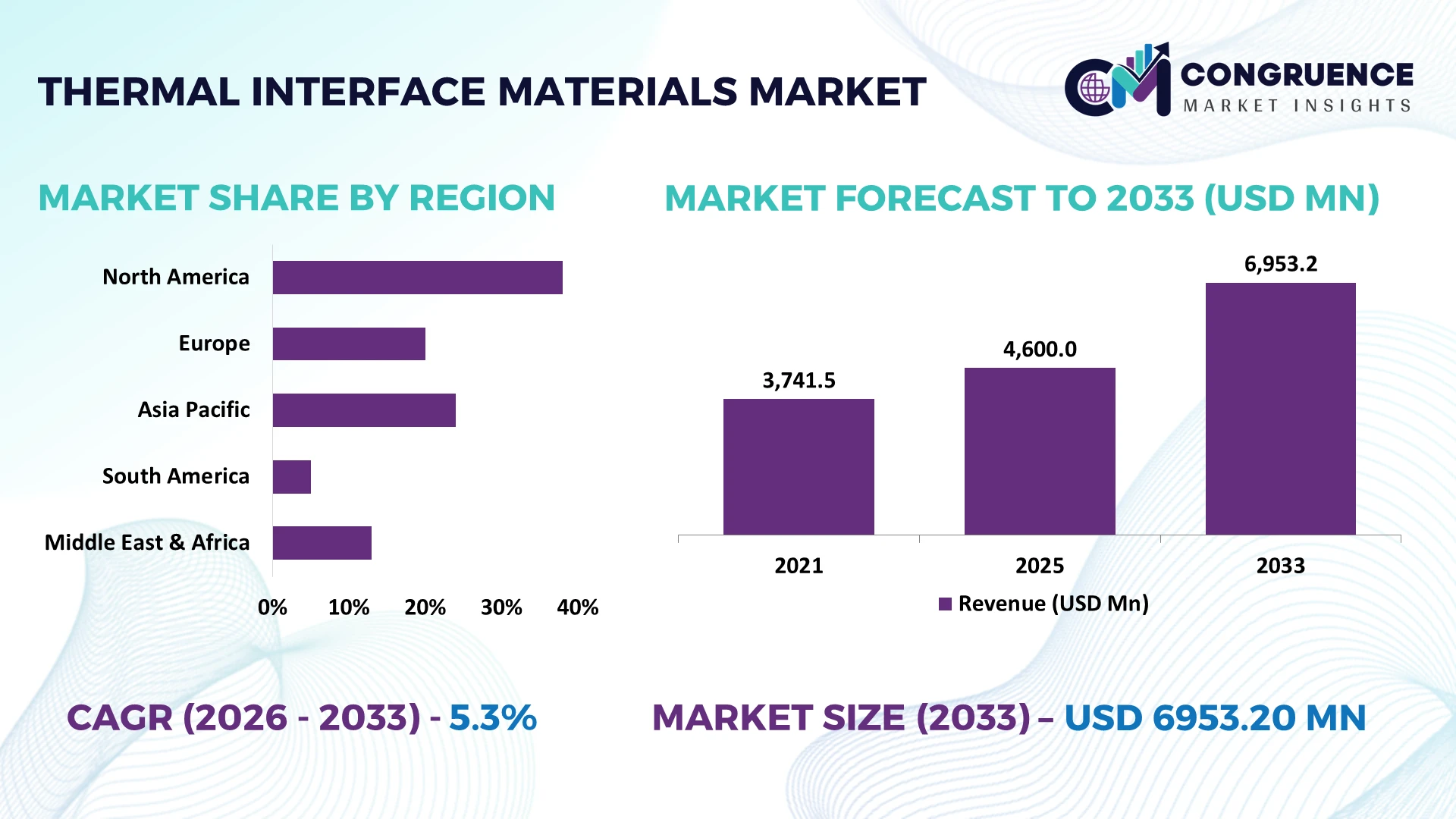

The Global Thermal Interface Materials Market was valued at USD 4600 Million in 2025 and is anticipated to reach a value of USD 6953.2 Million by 2033 expanding at a CAGR of 5.3% between 2026 and 2033. Growth is being accelerated by rising thermal management requirements in AI servers, electric vehicles, advanced semiconductor packaging, and high-density power electronics requiring superior heat dissipation performance.

China remains the dominant manufacturing and consumption hub, accounting for approximately 38% of global electronics production while supporting over 45% of battery manufacturing capacity, strengthening demand for advanced thermal interface materials across EVs, consumer electronics, and industrial equipment. Compared with the United States, which leads in high-performance semiconductor innovation and data center deployment, China maintains stronger volume-driven adoption. Ongoing technology export controls continue reshaping global electronics supply chains, prompting regional manufacturing diversification and accelerated material qualification programs.

Manufacturers should prioritize regional production resilience, high-performance material portfolios, and partnerships across semiconductor and electrification value chains to strengthen long-term competitive positioning.

Market Size & Growth: USD 4600 Million in 2025, reaching USD 6953.2 Million by 2033 at 5.3% CAGR, supported by AI infrastructure expansion and advanced semiconductor packaging.

Top Growth Drivers: EV thermal management demand exceeds 30%, AI server deployment grows above 25%, and advanced electronics production expands nearly 18% globally.

Short-Term Forecast: By 2028, thermal conductivity efficiency improves 20% while manufacturing cycle times decline approximately 15% through process automation.

Emerging Technologies: AI-driven material design, automated dispensing systems, and graphene-enhanced thermal compounds improve heat transfer by over 25%.

Regional Leaders: Asia-Pacific exceeds USD 3400 Million, North America approaches USD 1600 Million, and Europe surpasses USD 1100 Million, driven by semiconductor, EV, and industrial automation investments.

Consumer/End-User Trends: More than 60% of premium EV battery systems now integrate advanced thermal interface materials for enhanced thermal stability.

Pilot/Case Example: In 2026, advanced AI server cooling deployments improved thermal efficiency by approximately 18%, reducing system overheating during high-density computing operations.

Competitive Landscape: The leading supplier holds roughly 14% market share alongside major participants including Henkel, Dow, Shin-Etsu Chemical, Parker Hannifin, and 3M.

Regulatory & ESG Impact: Low-VOC formulations and recyclable material initiatives reduce manufacturing emissions by nearly 12% while supporting evolving environmental compliance requirements.

Investment & Funding: More than USD 1.4 Billion supports capacity expansion, strategic partnerships, and regional manufacturing diversification amid shifting global supply chains.

Innovation & Future Outlook: High-conductivity phase-change materials, silicone-free formulations, and AI-optimized thermal solutions strengthen next-generation electronics and electrification strategies.

Thermal Interface Materials Market demand is increasingly concentrated in AI computing hardware, electric vehicle battery systems, telecommunications equipment, and advanced industrial electronics requiring higher thermal reliability. New graphene-enhanced fillers and phase-change formulations improve heat transfer performance by over 20%, while regional manufacturing expansion addresses supply-chain diversification and stricter material qualification requirements, setting the foundation for the strategic market assessment.

Thermal interface materials have become strategically important as semiconductor complexity, AI computing infrastructure, and vehicle electrification raise thermal performance requirements across critical industries. Competition has shifted from standard heat-transfer compounds toward engineered materials that improve reliability under high power density. At the same time, supply-chain restructuring following geopolitical trade restrictions is encouraging manufacturers to localize production, qualify multiple raw material suppliers, and establish regional manufacturing networks for greater operational resilience.

Advanced phase-change materials and graphene-enhanced formulations deliver approximately 20% higher thermal conductivity and reduce assembly complexity by nearly 15% compared with conventional silicone-based pads in demanding applications. China continues to lead high-volume electronics manufacturing, while the United States focuses on high-performance chip design and advanced data center deployment requiring premium thermal management solutions. Over the next two to three years, AI server installations are expected to increase by more than 30%, accelerating qualification of higher-performance interface materials across computing and industrial electronics.

A practical example is the deployment of advanced thermal gap fillers in next-generation EV battery packs, where improved heat distribution extends battery reliability while simplifying automated assembly. Manufacturers are expanding localized production, strengthening material partnerships, and increasing investment in application-specific formulations. Companies that combine advanced material innovation with resilient supply networks and customer-focused engineering support will secure stronger competitive positioning across high-value thermal management applications.

Rapid deployment of AI servers, electric vehicles, and high-density semiconductor packages is transforming thermal management into a core engineering priority. AI computing systems generate over 30% higher thermal loads than previous server architectures, while EV battery platforms increasingly require materials capable of maintaining consistent heat dissipation under demanding operating conditions. More than 60% of premium battery systems now integrate advanced thermal interface solutions to improve safety and operational stability. In response to semiconductor manufacturing expansion in Taiwan and the United States, companies are increasing production capacity, investing in high-conductivity formulations, and forming strategic partnerships with OEMs to deliver customized thermal solutions, strengthening long-term customer integration and product differentiation.

Performance-grade fillers, specialty silicones, and advanced ceramic materials remain exposed to supply concentration and price volatility, creating procurement challenges for manufacturers. Prices of selected thermal filler materials have fluctuated by nearly 18% during recent supply disruptions, while qualification cycles for replacement materials frequently extend beyond 12 months. Japan and South Korea continue to dominate several high-performance material segments, increasing dependency for downstream producers. Companies are mitigating these constraints through localized sourcing, long-term procurement agreements, and multi-supplier qualification strategies. The ability to stabilize raw material availability has become a decisive operational advantage, particularly for suppliers serving automotive and semiconductor production programs with strict quality requirements.

Emerging opportunities are expanding beyond conventional electronics into AI accelerators, power semiconductor modules, energy storage systems, and aerospace electronics. Graphene-enhanced composites improve thermal conductivity by over 25%, while automated dispensing technologies reduce manufacturing waste by approximately 15%. India is strengthening electronics manufacturing through semiconductor ecosystem investments, creating additional demand for localized thermal management materials and engineering support. Companies are accelerating R&D, expanding application laboratories, and partnering with device manufacturers to develop customized formulations. An important strategic opportunity lies in co-designing thermal materials alongside chip packaging and battery architectures, enabling higher system efficiency rather than competing solely on material performance.

Commercializing next-generation thermal interface materials requires consistent integration across diverse manufacturing environments, qualification standards, and automated assembly processes. More than 40% of electronics manufacturers continue operating mixed production lines, increasing validation complexity for new materials. Advanced semiconductor packaging also requires thermal interface thickness tolerances below 100 microns, demanding greater process precision and workforce expertise. Manufacturers are investing in digital quality monitoring, automated dispensing equipment, and collaborative engineering partnerships to improve deployment consistency. Companies that standardize manufacturing processes while maintaining compatibility with evolving semiconductor, automotive, and industrial platforms will achieve stronger operational resilience and sustainable competitive differentiation.

AI Server Cooling Evolution: AI accelerator deployment is pushing thermal loads above previous enterprise computing standards, increasing demand for high-conductivity interface materials by over 30%. Automated dispensing has reduced assembly variation by nearly 18%, while advanced gap fillers improve thermal contact consistency. Semiconductor expansion in the United States is accelerating qualification cycles, prompting suppliers to scale localized production, strengthen OEM collaborations, and optimize manufacturing workflows for faster commercial deployment.

Localized Supply Network Expansion: Manufacturers are restructuring sourcing strategies as over 40% of electronics companies expand multi-country procurement to improve resilience against geopolitical disruptions. China remains the largest production hub, while India and Vietnam continue attracting electronics manufacturing investment. Companies are increasing regional inventories, establishing local converting facilities, and forming long-term supplier partnerships to reduce logistics risks, improve delivery reliability, and shorten customer lead times by approximately 15%.

Automation Improves Material Precision: Robotics-assisted dispensing and AI-enabled process monitoring are transforming thermal interface material application across semiconductor and automotive production. Automated systems reduce material waste by around 20% while improving placement accuracy by nearly 25%. Labor availability constraints and stricter quality requirements are encouraging manufacturers to integrate digital inspection platforms, increasing production consistency and reducing downstream rework across high-volume assembly operations.

Sustainable Material Engineering: Low-siloxane formulations, recyclable packaging, and solvent-reduction initiatives are becoming standard product development priorities as environmental compliance expectations increase. Manufacturing facilities adopting closed-loop material handling report waste reductions approaching 15%, while energy-efficient curing technologies shorten production cycles by roughly 10%. Companies are expanding sustainable product portfolios and collaborating with electronics manufacturers to qualify environmentally optimized thermal management solutions without compromising thermal performance.

Thermal Greases remain the leading product category, accounting for approximately 34% of market demand due to their cost efficiency, excellent thermal conductivity, and compatibility with high-volume electronics manufacturing. Their established use across processors, power modules, and industrial electronics supports broad commercial adoption. Gap Fillers continue strengthening their position in EV battery packs and power electronics where vibration resistance and uneven surface accommodation are operational priorities. Thermal Pads retain stable demand for simplified assembly and maintenance, while Thermal Adhesives support applications requiring permanent bonding and structural reliability.

Phase Change Materials represent the fastest-growing segment as AI computing platforms and advanced semiconductor packages require improved heat transfer with cleaner automated assembly. Adoption has increased by nearly 24% across high-performance computing applications, while manufacturers report process efficiency improvements approaching 15% compared with conventional interfaces. Companies are expanding specialized material portfolios, investing in advanced formulations, and collaborating with semiconductor manufacturers to optimize application-specific thermal performance. Investment priorities are steadily shifting toward premium engineered materials supporting miniaturization, higher power density, and automated production environments.

Consumer Electronics remain the largest application segment, representing approximately 39% of overall demand because of sustained production volumes for smartphones, laptops, gaming devices, and wearable technologies. Continuous device miniaturization and higher processing power require more efficient thermal management without increasing component size. Automotive Electronics continue expanding through battery systems, power control units, and onboard computing, while Telecommunications benefits from 5G infrastructure upgrades requiring reliable thermal performance in networking equipment.

Data Centers represent the fastest-growing application as AI computing clusters significantly increase processor heat density. Deployment of liquid-assisted cooling architectures has increased by nearly 22%, while demand for premium thermal interface materials has expanded by approximately 28% within high-performance computing facilities. Industrial Equipment continues adopting advanced thermal management for robotics and factory automation. Manufacturers are increasing production capacity, integrating automated dispensing technologies, and developing customized materials optimized for enterprise computing, telecom infrastructure, and electrified mobility systems where operational reliability is mission critical.

Electronics Manufacturers account for approximately 47% of total demand because of large-scale production of semiconductors, computing hardware, consumer electronics, and networking equipment requiring precise thermal management. High-volume manufacturing, automated assembly lines, and rapid product refresh cycles reinforce purchasing consistency. Telecom Industry buyers continue investing in advanced network equipment supporting higher operating temperatures, while Industrial Manufacturers integrate thermal interface materials into automation systems, power electronics, and precision machinery requiring long operating lifecycles.

The Automotive Industry represents the fastest-growing end-user segment as electrification, battery innovation, and advanced driver assistance systems increase thermal management requirements. Material adoption within EV platforms has expanded by nearly 26%, while automated battery assembly efficiency has improved by approximately 16% through optimized dispensing technologies. Suppliers are strengthening OEM partnerships, offering application-specific formulations, and expanding engineering support to secure long-term supply agreements. Competitive positioning increasingly depends on customized solutions rather than standardized products, reflecting changing procurement priorities among high-value industrial customers.

Asia-Pacific accounted for the largest market share at 47% in 2025 however, North America is expected to register the fastest growth, expanding at a 6.2% CAGR between 2026 and 2033.

Advanced Semiconductor Expansion Drives Premium Thermal Solutions

North America represents a high-value market supported by advanced semiconductor manufacturing, AI computing infrastructure, electric vehicle production, and aerospace electronics. The region contributes approximately 24% of global demand, with enterprise adoption concentrated around high-performance computing and data center investments. Growing deployment of advanced chip packaging has increased demand for premium thermal interface materials capable of handling higher power densities. During 2026, multiple semiconductor fabrication and packaging expansion projects accelerated domestic material qualification, while automated dispensing technologies improved production consistency by nearly 18%. Manufacturers continue strengthening regional partnerships with semiconductor and automotive OEMs while expanding localized engineering capabilities to shorten product validation cycles and enhance supply resilience for mission-critical applications.

United States Market Outlook: The United States leads regional demand through its concentration of semiconductor fabrication, AI infrastructure, hyperscale data centers, and electric vehicle innovation. More than 55% of North America's advanced semiconductor manufacturing capacity is linked to U.S.-based facilities, encouraging suppliers to establish localized technical support and application laboratories. Federal manufacturing initiatives and private-sector investments continue accelerating qualification of advanced thermal interface materials designed for high-density computing, power electronics, and next-generation mobility platforms.

Electrification and Sustainability Shape Industrial Modernization

Europe accounts for approximately 21% of global market activity, supported by strong automotive engineering, industrial automation, renewable energy equipment, and advanced manufacturing capabilities. Demand increasingly centers on premium thermal management solutions for electric mobility and power electronics operating under stringent efficiency requirements. Sustainability regulations are encouraging wider adoption of low-emission production methods and environmentally optimized formulations. Automated battery production capacity expanded by approximately 16% during recent industrial modernization initiatives, strengthening requirements for reliable thermal interface technologies. Companies continue investing in localized production, collaborative product development, and qualification partnerships to improve operational efficiency while supporting increasingly sophisticated manufacturing ecosystems.

Germany Market Outlook: Germany remains the strategic center of Europe's thermal interface materials market through its leadership in automotive manufacturing, industrial engineering, and advanced production technologies. More than 35% of the region's electric vehicle manufacturing activity is associated with German production networks, creating sustained demand for high-performance thermal solutions. Companies are integrating thermal materials into battery modules, industrial drives, and semiconductor equipment while strengthening partnerships between material developers and automotive manufacturers.

Manufacturing Scale Reinforces Global Leadership

Asia-Pacific dominates the global market with approximately 47% share, driven by extensive electronics manufacturing, semiconductor fabrication, EV battery production, and export-oriented industrial ecosystems. China, Japan, South Korea, and Taiwan collectively represent the world's largest concentration of thermal interface material consumption across consumer electronics and power electronics manufacturing. Regional battery manufacturing capacity exceeds 45% of global output, reinforcing continuous material demand. Increasing automation, advanced packaging investments, and localized semiconductor expansion continue improving manufacturing efficiency while shortening product development timelines. Suppliers are expanding production facilities, strengthening raw material integration, and establishing application engineering centers to serve growing enterprise demand across multiple technology sectors.

China Market Outlook: China remains the largest national market due to its extensive electronics manufacturing base, EV production leadership, and integrated semiconductor supply chain. The country contributes roughly 38% of global electronics manufacturing output, creating unmatched demand for thermal greases, gap fillers, and advanced interface materials. Domestic manufacturers continue expanding production capacity while collaborating with battery producers and electronics OEMs to improve product localization and supply-chain stability.

Industrial Electronics Support Emerging Demand

South America represents a developing market where industrial automation, automotive assembly, consumer electronics manufacturing, and telecommunications infrastructure are gradually strengthening thermal management requirements. The region contributes approximately 5% of global demand, with Brazil accounting for the largest share of manufacturing activity. Expansion of industrial modernization projects has improved adoption of advanced thermal materials, while localized electronics assembly continues supporting steady procurement. Infrastructure limitations and imported specialty material dependence remain operational constraints. Companies are responding through regional distribution partnerships, inventory optimization, and localized technical services that improve product availability and reduce procurement delays for industrial customers.

Brazil Market Outlook: Brazil leads regional demand through its automotive production, industrial equipment manufacturing, and growing electronics assembly operations. Approximately half of South America's vehicle production is concentrated within Brazil, increasing requirements for battery and power electronics thermal management. Material suppliers are strengthening local distribution networks, technical support capabilities, and industrial partnerships to improve responsiveness while reducing reliance on lengthy import supply chains.

Infrastructure Investment Expands Industrial Adoption

The Middle East & Africa market continues advancing through digital infrastructure projects, industrial diversification, telecommunications expansion, and investments in advanced manufacturing capabilities. The region accounts for approximately 3% of global demand, with increasing adoption across power electronics, industrial automation, and data center infrastructure. Government-supported technology initiatives are encouraging deployment of higher-performance electronic systems requiring reliable thermal management. Recent enterprise infrastructure programs have increased regional data center capacity by approximately 14%, creating additional demand for advanced interface materials. Suppliers are expanding channel partnerships, establishing regional technical support, and improving inventory availability to strengthen market access while supporting industrial modernization strategies.

Saudi Arabia Market Outlook: Saudi Arabia represents the region's strongest growth platform through large-scale digital infrastructure investments, industrial diversification initiatives, and advanced manufacturing development. Expansion of technology parks, smart industrial facilities, and enterprise computing infrastructure is increasing demand for thermal management materials across multiple sectors. Companies are strengthening regional partnerships and localized engineering support while aligning product portfolios with national industrial modernization and electronics manufacturing objectives.

The competitive landscape is led by Henkel, Dow, Shin-Etsu Chemical, Parker Hannifin, and 3M, competing against specialized thermal material innovators and regional manufacturers across semiconductor, automotive, and electronics supply chains. The top five players collectively control approximately 52% of global market activity, while regional suppliers compete aggressively on localized production and faster customer support. Global leaders differentiate through high-performance formulations, application engineering, and integrated supply agreements, whereas cost-focused manufacturers emphasize pricing advantages of 10–15% for standard products. Premium suppliers deliver thermal conductivity improvements exceeding 20% through advanced fillers and customized formulations, reducing customer qualification time by nearly 18%. Competition increasingly centers on localized manufacturing expansion, semiconductor partnerships, and vertical integration of specialty materials to secure raw material availability. Technology-intensive applications are shifting purchasing decisions from price toward reliability and co-development capabilities. High qualification requirements, intellectual property, and customer validation cycles remain major entry barriers. Winning requires application-specific innovation, resilient supply chains, rapid engineering support, and scalable manufacturing aligned with next-generation electronics and electrification programs.

Henkel AG & Co. KGaA

Dow Inc.

Shin-Etsu Chemical Co., Ltd.

Parker Hannifin Corporation

3M

Momentive Performance Materials

Indium Corporation

Fujipoly Corporation

Laird Thermal Systems

Kitagawa Industries Co., Ltd.

Zalman Tech Co., Ltd.

Wakefield Thermal

AI Technology, Inc.

Noctua

Advanced thermal interface materials are rapidly evolving from conventional silicone greases toward graphene-enhanced composites, phase-change materials, and hybrid ceramic fillers designed for AI processors, electric vehicle batteries, and advanced semiconductor packages. Compared with traditional thermal greases, graphene-enhanced formulations improve thermal conductivity by more than 25% while reducing interface resistance by approximately 18%. Automated dispensing systems are now deployed across nearly 60% of high-volume electronics manufacturing lines, improving placement accuracy and minimizing material waste. These technologies provide measurable operational advantages by increasing product reliability, reducing maintenance requirements, and supporting compact, high-power electronic designs.

Artificial intelligence is increasingly integrated into material development, enabling predictive formulation optimization and accelerated qualification cycles. Digital simulation platforms reduce prototype iterations by approximately 20%, while machine vision inspection improves dispensing precision by nearly 15% compared with conventional manual quality control. Semiconductor manufacturers, hyperscale data center operators, and premium automotive OEMs benefit most because optimized thermal performance directly improves computing efficiency, battery durability, and system stability under continuous high-load operation.

Between 2026 and 2028, next-generation phase-change materials, nano-engineered fillers, and AI-assisted manufacturing are expected to become standard across premium electronics production. Companies investing early in automated processing, customized material engineering, and advanced packaging compatibility will strengthen competitive differentiation, shorten commercialization timelines, and secure long-term supply positions within increasingly technology-driven thermal management value chains.

October 2024 Dow partnered with Carbice to develop multi-generational thermal interface materials combining silicone and carbon nanotube technologies for electronics and mobility applications. The collaboration targets improved thermal reliability using patented CNT interfaces, strengthening next-generation semiconductor and EV thermal management.

March 2025 Henkel introduced Bergquist Liqui Form TLF 6500 CGel-SF, a silicone-free thermal curable gel delivering thermal conductivity of 6.5 W/m·K for ADAS domain controllers. The launch enhances heat dissipation for autonomous driving electronics while expanding Henkel's advanced automotive thermal management portfolio. Source: (Henkel)

May 2026 Dow launched DOWSIL TC-3120 Thermal Gel featuring approximately 12 W/m·K thermal conductivity for 800G and 1.6T optical modules and dense electronics. The innovation improves heat transfer and optical cleanliness, supporting high-speed AI networking and advanced data center infrastructure. Source: (Dow Corporate)

2026 SEMI highlighted continued expansion of advanced semiconductor packaging capacity worldwide, increasing deployment of high-performance thermal interface materials for chiplet architectures and high-density processors. The industry shift supports stronger supplier investment in specialized thermal formulations and automated manufacturing capabilities.

The report delivers comprehensive analysis across Thermal Greases, Thermal Pads, Phase Change Materials, Thermal Adhesives, and Gap Fillers, covering strategic applications in Consumer Electronics, Automotive Electronics, Telecommunications, Industrial Equipment, and Data Centers. It evaluates demand patterns across Electronics Manufacturers, Automotive Industry, Telecom Industry, and Industrial Manufacturers while assessing competitive positioning across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 50% of market activity is concentrated within advanced electronics and semiconductor manufacturing ecosystems, highlighting strong deployment intensity.

The assessment examines manufacturing trends, material innovation, automation, advanced semiconductor packaging, AI computing infrastructure, and battery thermal management technologies. It provides strategic insights into company positioning, product differentiation, regional expansion strategies, supply-chain resilience, and evolving procurement priorities between 2026 and 2033. The report also supports investment evaluation, partnership planning, technology benchmarking, competitive assessment, and identification of emerging high-value opportunities across established and niche thermal management applications.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 4600 Million |

Market Revenue in 2033 | USD 6953.2 Million |

CAGR (2026 - 2033) | 5.3% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Henkel AG & Co. KGaA, Dow Inc., Shin-Etsu Chemical Co., Ltd., Parker Hannifin Corporation, 3M, Momentive Performance Materials, Indium Corporation, Fujipoly Corporation, Laird Thermal Systems, Kitagawa Industries Co., Ltd., Zalman Tech Co., Ltd., Wakefield Thermal, AI Technology, Inc., Noctua |

Customization & Pricing | Available on Request (10% Customization is Free) |