Reports

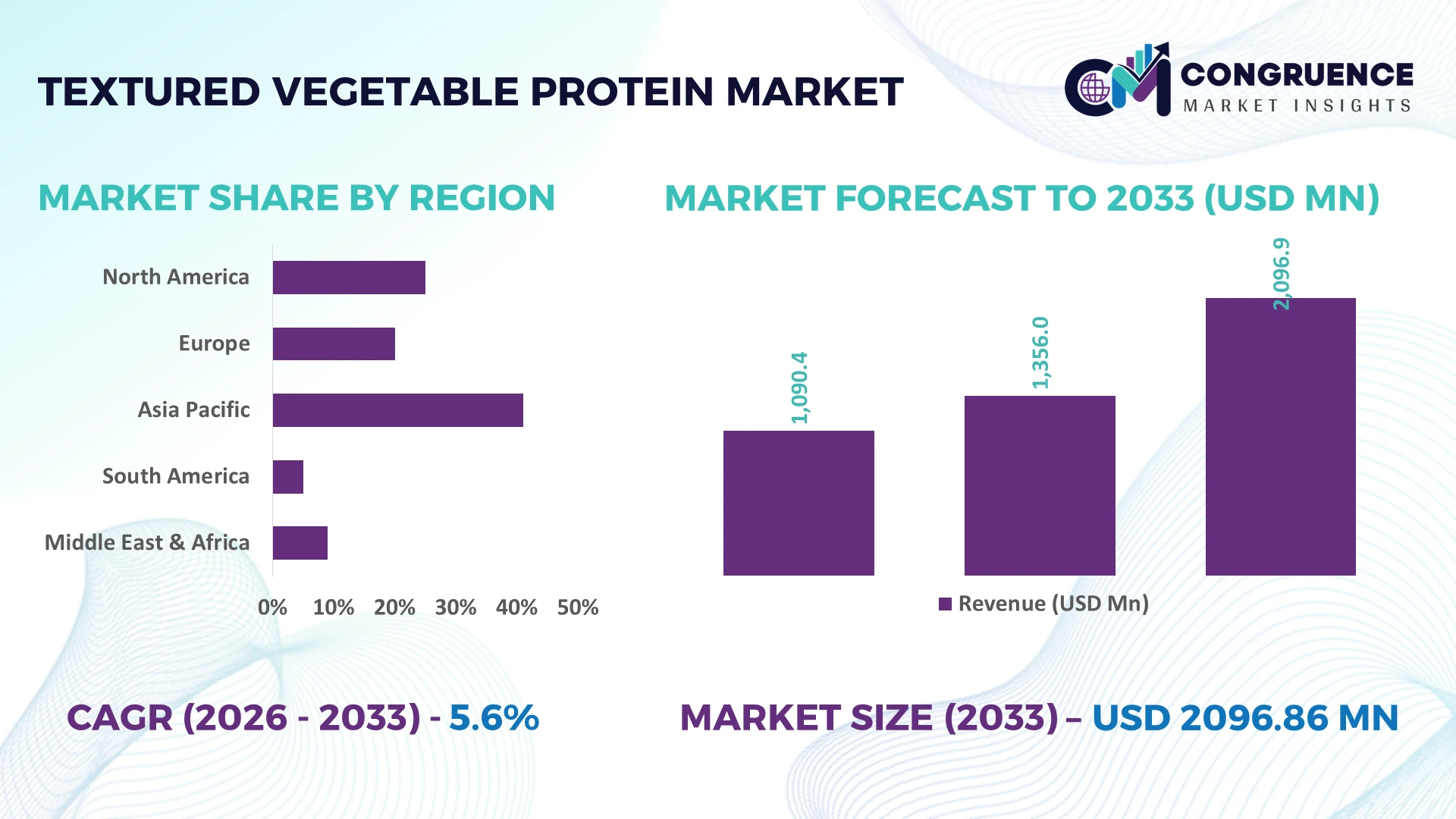

The Global Textured Vegetable Protein Market was valued at USD 1356 Million in 2025 and is anticipated to reach a value of USD 2096.86 Million by 2033 expanding at a CAGR of 5.6% between 2026 and 2033. Growth is supported by continuous expansion in plant-based protein processing, improved extrusion technologies, and increasing use of textured proteins across meat alternatives, processed foods, and foodservice manufacturing.

The United States remains the dominant country, accounting for approximately 31% of global textured vegetable protein production, supported by large-scale soybean processing, advanced food manufacturing, and investments exceeding USD 1 billion in plant-based protein capacity upgrades. Compared with Germany, where high-value product innovation drives premium applications, the U.S. benefits from stronger industrial-scale processing and wider foodservice adoption. Ongoing trade diversification following global supply-chain realignments has strengthened raw material availability and manufacturing resilience.

Strategic investment in advanced protein processing, diversified feedstock sourcing, and regional manufacturing capacity will remain essential for sustaining competitive advantage in the global textured vegetable protein market.

Market Size & Growth: Valued at USD 1356 million in 2025 and projected to reach USD 2096.86 million by 2033 at a CAGR of 5.6%; growth is supported by advanced extrusion technology and expanding plant-based food manufacturing.

Top Growth Drivers: Meat-alternative consumption (+18%), high-protein convenience foods (+15%), and food processing automation (+12%) continue strengthening global market expansion.

Short-Term Forecast: By 2027, production efficiency is expected to improve by approximately 14% through automated extrusion systems and optimized ingredient utilization.

Emerging Technologies: AI-enabled quality monitoring, high-moisture extrusion, and precision process automation reduce production variability by approximately 16% while improving product consistency.

Regional Leaders: North America approaches USD 760 million, Europe USD 560 million, and Asia-Pacific USD 490 million, supported by manufacturing expansion and localized product innovation.

Consumer/End-User Trends: More than 42% of urban consumers actively purchase protein-enriched plant-based products, encouraging diversified textured protein formulations across retail and foodservice.

Pilot/Case Example: In 2026, an automated production modernization project improved extrusion throughput by approximately 20% while reducing processing waste by nearly 11%.

Competitive Landscape: Leading manufacturers collectively account for around 38% of global supply, with competition focused on innovation, capacity expansion, and premium protein portfolios.

Regulatory & ESG Impact: Sustainable production initiatives reduce processing emissions by nearly 18%, while cleaner-label compliance accelerates product reformulation across international markets.

Investment & Funding: More than USD 900 million has been invested in facility expansion, strategic partnerships, and supply-chain modernization amid ongoing regional manufacturing diversification.

Innovation & Future Outlook: Next-generation protein blends, precision extrusion, and sustainable ingredient sourcing strengthen high-growth product portfolios and accelerate commercial adoption.

The Textured Vegetable Protein Market is increasingly shaped by demand from meat alternatives, ready-to-eat meals, and protein-fortified foods. High-moisture extrusion and cleaner-label formulations are improving texture and functionality, while nearly 24% of new product launches emphasize blended plant-protein innovation. Ongoing supply-chain localization and evolving food ingredient standards are encouraging regional manufacturing investments, setting the foundation for the strategic market assessment that follows.

The Textured Vegetable Protein Market has become strategically important as food manufacturers seek resilient protein supply chains, diversified ingredient portfolios, and scalable alternatives to animal-based proteins. Supply-chain restructuring following global commodity disruptions has accelerated investment in localized protein processing and contract manufacturing. Companies are strengthening upstream sourcing while expanding product portfolios for retail, foodservice, and industrial food processing to improve operational resilience and competitive differentiation.

Modern high-moisture extrusion systems deliver up to 18% higher production efficiency and reduce energy consumption by approximately 12% compared with conventional dry extrusion technologies, improving consistency and lowering manufacturing costs. The United States leads large-scale commercial production through integrated soybean processing, while Germany emphasizes premium formulations and process innovation for clean-label applications. Over the next two to three years, automated quality monitoring is expected to exceed 45% adoption among large processing facilities, improving production reliability and reducing material losses.

A leading deployment trend involves integrating AI-assisted process controls with advanced extrusion lines to optimize texture, moisture balance, and raw material utilization. Manufacturers are increasing investments in localized production facilities, strategic ingredient partnerships, and sustainable processing technologies to strengthen supply security. Businesses that combine manufacturing flexibility with advanced processing capabilities will secure stronger competitive positioning and long-term operational advantage.

Rapid expansion of plant-based food manufacturing continues to reshape textured vegetable protein demand across industrial food processing. More than 35% of newly launched meat-alternative products now incorporate textured vegetable protein, while automated extrusion improves production throughput by nearly 20% and reduces material waste by around 10%. The United States continues expanding domestic soybean processing capacity to strengthen ingredient security following global supply-chain realignments. In response, manufacturers are investing in vertically integrated production, expanding processing facilities, and developing customized protein formulations for foodservice and packaged foods. This strategy strengthens supply resilience, improves product consistency, and enables faster commercialization of value-added protein ingredients.

Volatility in soybean and pea protein prices remains a structural challenge for manufacturers, with raw materials representing nearly 55% of production costs. Ingredient procurement costs have fluctuated by approximately 15% due to weather variability, logistics disruptions, and export policy changes across major producing countries. Smaller processors face reduced pricing flexibility and compressed operating margins, limiting production scalability. Companies are responding by diversifying protein sources, expanding local sourcing agreements, and securing long-term supply contracts to stabilize procurement costs. Strategic ingredient diversification is becoming essential for maintaining consistent production economics and reducing exposure to commodity market fluctuations.

Next-generation protein technologies are opening opportunities beyond traditional meat substitutes through hybrid protein formulations, precision fermentation integration, and functional nutrition products. More than 30% of new product development projects now focus on blended plant proteins, while AI-assisted formulation platforms reduce development cycles by nearly 25%. India is expanding domestic plant-protein processing to support both food manufacturing and export demand through government-backed food processing initiatives. Companies are increasing R&D investments, collaborating with ingredient technology firms, and expanding application portfolios into bakery, snacks, and clinical nutrition. These initiatives create differentiated products with higher functionality and stronger commercial value.

Maintaining consistent texture, flavor, and functionality across high-volume production remains a major execution challenge as product portfolios expand. Production variability can increase rejection rates by nearly 8%, while advanced extrusion systems require approximately 20% higher technical workforce capability than conventional processing lines. Manufacturers in Japan and other technology-intensive markets continue facing skilled workforce shortages for sophisticated processing operations. Companies must strengthen automation, digital process monitoring, workforce training, and predictive maintenance to achieve consistent quality across facilities. Solving manufacturing complexity will be critical for sustaining competitiveness, supporting premium product positioning, and meeting evolving customer performance expectations.

High-Moisture Processing Expansion Modern high-moisture extrusion is replacing conventional processing across premium product lines, improving texture consistency by nearly 18% while reducing production waste by approximately 11%. Large manufacturers in the United States are upgrading integrated processing facilities following labor shortages and higher efficiency requirements. Companies are expanding automated extrusion capacity and standardizing production workflows to improve output quality and manufacturing flexibility.

Localized Protein Supply Networks Supply-chain diversification has accelerated localized sourcing, with domestic protein procurement increasing by roughly 22% and average ingredient lead times declining by nearly 15%. Food processors are reducing dependence on imported raw materials after recent logistics disruptions. Manufacturers are strengthening long-term supplier agreements, investing in regional processing facilities, and restructuring procurement strategies to improve supply security and production continuity.

AI-Driven Manufacturing Optimization Digital production platforms are becoming standard across large processing plants, reducing quality inspection time by around 30% while improving batch consistency by nearly 17%. Enterprise manufacturers are integrating AI-enabled monitoring with automated production control systems to reduce manual intervention. Companies continue expanding digital manufacturing partnerships to improve operational efficiency and minimize product variability throughout commercial production.

Clean-Label Product Reformulation Ingredient transparency has become a key operational priority, with more than 40% of newly introduced formulations emphasizing simplified ingredient declarations and reduced additives. Regulatory expectations and evolving consumer purchasing patterns are accelerating formulation changes across Europe and North America. Producers are increasing investments in natural processing technologies, ingredient traceability, and product reformulation to strengthen retail acceptance and premium market positioning.

Soy Protein remains the leading segment due to its established supply chain, superior functionality, and cost-efficient large-scale processing. It represents nearly 60% of commercial textured vegetable protein utilization because of its excellent water absorption, protein concentration, and compatibility with industrial extrusion systems. Manufacturers continue expanding soy processing capacity while optimizing formulation performance for meat alternatives and processed food applications. Wheat Protein maintains strategic importance in improving product elasticity and texture, whereas Rice Protein supports allergen-friendly formulations for specialized nutrition products.

Pea Protein is the fastest-growing segment as manufacturers diversify beyond soy-based ingredients to address allergen concerns and product differentiation. Adoption has increased by approximately 21% across premium plant-based products, supported by advances in extraction efficiency and formulation technologies. Fava Bean Protein is steadily gaining commercial interest for sustainable protein blends and regional ingredient sourcing. Companies are expanding partnerships with ingredient innovators while investing in multi-protein formulations that improve nutritional profiles and supply-chain resilience, shifting investment priorities toward diversified protein portfolios.

Meat Alternatives remain the dominant application because they require consistent texture, moisture retention, and protein functionality across high-volume manufacturing. Nearly 48% of commercial textured vegetable protein consumption is directed toward meat analogue production, where automated extrusion and formulation optimization improve product consistency and manufacturing efficiency. Processed Foods continue generating stable demand as manufacturers incorporate textured proteins into value-added formulations that enhance nutritional content without significantly increasing production complexity.

Ready Meals represent the fastest-growing application as demand for convenient, protein-rich meal solutions expands across urban markets. Product adoption has risen by approximately 19%, supported by improved freezing stability and standardized manufacturing processes. Snacks and Bakery Products are also strengthening their strategic relevance through protein fortification and clean-label innovation. Manufacturers are scaling dedicated production lines, optimizing ingredient integration, and introducing customized formulations to improve operational flexibility while meeting evolving consumer preferences across multiple food categories.

Food Manufacturers represent the largest end-user segment because of their extensive processing infrastructure, long-term procurement contracts, and large-scale product development capabilities. They account for approximately 52% of commercial textured vegetable protein demand, supported by integrated manufacturing operations and continuous product innovation. Ingredient Suppliers remain essential by ensuring standardized raw material quality and stable commercial availability, while Retail Brands increasingly collaborate with manufacturers to develop differentiated private-label protein products.

Plant-Based Food Companies are the fastest-growing end-user group, with procurement volumes expanding by nearly 24% as product portfolios diversify across retail and foodservice channels. Foodservice operators are also increasing adoption through menu expansion and standardized protein formulations. Companies are responding with customized ingredient solutions, collaborative product development, flexible pricing models, and strategic partnerships that strengthen long-term commercial relationships. Competitive positioning is increasingly driven by formulation expertise, manufacturing responsiveness, and supply-chain integration.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

Integrated Protein Processing Strengthens Market Leadership

North America maintains the largest share of the Textured Vegetable Protein Market through its highly integrated soybean processing infrastructure, advanced extrusion technologies, and established food manufacturing ecosystem. The region contributes approximately 37% of global production capacity, supported by large commercial processing facilities and strong enterprise adoption of plant-based ingredients. More than 45% of newly commissioned protein-processing upgrades are focused on automation and digital quality monitoring to improve production consistency and operational efficiency. Manufacturers continue expanding processing capacity, strengthening supplier partnerships, and optimizing vertically integrated operations to improve raw material security and support diversified food applications.

United States Market Outlook: The United States remains the regional growth engine because of its large soybean processing industry, extensive food manufacturing base, and continuous investment in advanced protein processing technologies. More than 31% of global textured vegetable protein production originates from U.S.-based facilities, supported by integrated supply chains and commercial-scale extrusion capacity. Companies continue expanding automated production lines, improving ingredient traceability, and investing in premium plant-protein formulations to strengthen export competitiveness and manufacturing resilience.

Clean-Label Innovation Reshapes Industrial Production

Europe continues strengthening its position through sustainable food manufacturing, clean-label product development, and advanced ingredient innovation. The region accounts for approximately 29% of global market activity, supported by strong regulatory alignment and modern food processing infrastructure. Nearly 40% of new commercial product launches emphasize simplified ingredient formulations and improved nutritional profiles. Manufacturers are expanding collaborations with ingredient specialists while modernizing production facilities to enhance efficiency, reduce processing waste, and accelerate premium product commercialization across established food brands.

Germany Market Outlook: Germany leads the European market through advanced food engineering capabilities, high-value manufacturing, and continuous innovation in plant-based protein applications. Commercial processors increasingly deploy precision extrusion technologies, with automated production now representing nearly 46% of large-scale processing operations. Strategic partnerships between food manufacturers and ingredient developers continue improving formulation performance while supporting industrial competitiveness across domestic and export markets.

Manufacturing Scale Accelerates Commercial Expansion

Asia-Pacific is emerging as the fastest-expanding market due to expanding food processing capacity, rising protein consumption, and continuous manufacturing investments. The region contributes nearly 27% of global production, while new processing facilities have increased by approximately 18% over recent years. Domestic manufacturers are strengthening localized protein supply chains, expanding extrusion capacity, and integrating automated processing technologies to improve production efficiency. Export-oriented manufacturing and growing investment in functional food ingredients continue strengthening the region's competitive position within global protein supply networks.

China Market Outlook: China remains the region's largest production hub because of its extensive soybean processing capacity, integrated food manufacturing infrastructure, and expanding plant-based food industry. Large enterprises continue investing in intelligent manufacturing systems and modern extrusion equipment, improving production efficiency by approximately 16%. Domestic manufacturers are also strengthening export capabilities through quality standardization, automated processing, and long-term supply partnerships across international food markets.

Agricultural Resources Support Processing Expansion

South America benefits from abundant agricultural resources and expanding oilseed processing capacity, creating favorable conditions for textured vegetable protein production. The region represents approximately 6% of global market activity and continues increasing value-added processing rather than exporting raw commodities. Processing capacity utilization has improved by nearly 14% through facility modernization and operational optimization. Manufacturers are expanding industrial partnerships, improving regional logistics, and strengthening downstream food processing capabilities despite infrastructure constraints affecting transportation efficiency.

Brazil Market Outlook: Brazil serves as the region's primary manufacturing center due to its leadership in soybean cultivation and large-scale agricultural processing infrastructure. Integrated crushing and protein processing operations enable consistent raw material availability while supporting commercial food manufacturing. Processing efficiency has improved by approximately 15% following equipment modernization, encouraging companies to expand domestic production and strengthen export-oriented ingredient supply strategies.

Food Security Investments Drive Adoption

The Middle East & Africa market is advancing through food security initiatives, expanding food manufacturing capacity, and greater investment in localized ingredient production. The region contributes approximately 4% of global market activity, with industrial food processing facilities increasing by nearly 12% across key investment hubs. Governments and private enterprises continue supporting manufacturing modernization, strategic import diversification, and regional processing infrastructure to improve long-term food supply resilience while reducing dependence on imported finished products.

Saudi Arabia Market Outlook: Saudi Arabia leads regional investment through large-scale food manufacturing expansion, industrial diversification programs, and advanced food processing initiatives. Modern production facilities increasingly incorporate automated processing technologies to improve operational efficiency and reduce production variability. Domestic enterprises continue establishing strategic partnerships with international ingredient manufacturers while strengthening local production capabilities to support national food security objectives and long-term industrial development.

The Textured Vegetable Protein Market is led by ADM, Cargill, Roquette, Ingredion, and International Flavors & Fragrances, with global ingredient leaders competing against regional protein processors and specialized plant-based ingredient innovators. The top five players collectively account for approximately 44% of the market, while regional manufacturers compete through localized sourcing and lower production costs. Competition centers on formulation performance, raw material integration, manufacturing efficiency, and supply reliability. Companies using automated extrusion reduce production waste by nearly 12% and improve batch consistency by around 17%, while vertically integrated processors lower procurement exposure by approximately 15%. Strategic competition increasingly involves production expansion, long-term supply partnerships, customized protein solutions, and investments in clean-label formulations. Control of soybean and pea protein supply chains has become a decisive competitive advantage as procurement volatility influences pricing and delivery performance. High capital requirements for advanced extrusion systems and stringent food quality standards remain major entry barriers. Winning requires integrated sourcing, continuous formulation innovation, automated production, and reliable commercial-scale manufacturing execution.

ADM

Cargill

Roquette

Ingredion Incorporated

International Flavors & Fragrances Inc.

Bunge Global SA

Kerry Group plc

BENEO GmbH

Axiom Foods, Inc.

Puris

Emsland Group

Cosucra Groupe Warcoing SA

Burcon NutraScience Corporation

Sotexpro

High-moisture extrusion has become the benchmark technology for premium textured vegetable protein production, replacing conventional dry extrusion in high-value applications. Modern extrusion systems improve texture uniformity by approximately 18% while reducing energy consumption by nearly 12%. Around 46% of newly commissioned commercial production lines now integrate automated process controls for continuous monitoring of moisture, temperature, and pressure. These technologies enable manufacturers to deliver consistent functionality while lowering operating costs and improving production scalability.

Artificial intelligence, machine vision, and digital twin platforms are transforming manufacturing workflows through predictive quality management and process optimization. AI-assisted monitoring reduces quality deviations by nearly 20%, while predictive maintenance decreases unplanned downtime by approximately 15%. Compared with traditional manual inspection systems, intelligent production platforms improve production consistency by almost 22%. Large integrated ingredient manufacturers gain the strongest competitive advantage because they can deploy digital technologies across multiple production facilities and rapidly standardize manufacturing performance.

Between 2026 and 2028, precision extrusion, advanced protein blending, and intelligent formulation software will reshape commercial production. Automated ingredient optimization is expected to exceed 50% deployment among large-scale manufacturers, accelerating new product development and reducing formulation cycles. Companies investing early in integrated digital processing, smart automation, and next-generation protein engineering will strengthen manufacturing flexibility, improve supply-chain resilience, and secure long-term competitive differentiation in premium plant-based ingredient markets.

May 2026 ADM expanded its plant protein portfolio with eight new soy and pea protein solutions, including textured protein innovations for meat alternatives. The launch added 8 new products, strengthening regional sourcing flexibility and accelerating product development for food manufacturers.

April 2026 dsm-firmenich introduced next-generation Vertis™ Textured Vegetable Proteins integrated with ModulaSENSE® technology, offering 55% and 65% protein variants with improved flavor performance. The innovation simplifies formulations and reduces reliance on additional masking systems, improving manufacturing efficiency.

June 2025 Roquette expanded its NUTRALYS® portfolio by launching its first textured wheat protein alongside a new textured pea protein containing over 60% protein. The expansion broadened functional ingredient options and strengthened the company's position in advanced plant-based protein applications.

May 2024 Roquette launched its first fava bean protein isolate, extending its alternative protein portfolio with a solution supporting diversified plant-protein formulations. The ingredient delivers over 80% protein content, enabling manufacturers to reduce soy dependency while expanding clean-label product innovation.

The report provides comprehensive analysis of the Textured Vegetable Protein Market across Soy Protein, Pea Protein, Wheat Protein, Fava Bean Protein, and Rice Protein while evaluating demand across Meat Alternatives, Processed Foods, Ready Meals, Snacks, and Bakery Products. It further assesses procurement trends among Food Manufacturers, Foodservice operators, Retail Brands, Plant-Based Food Companies, and Ingredient Suppliers. Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by operational benchmarks, production trends, technology adoption, and competitive positioning.

The study evaluates advanced extrusion technologies, AI-enabled manufacturing, digital quality monitoring, and sustainable processing innovations shaping industrial competitiveness. More than 40% of strategic analysis focuses on operational efficiency, supply-chain optimization, manufacturing modernization, and product innovation across leading enterprises. The report delivers practical intelligence for investment planning, capacity expansion, partnership evaluation, portfolio diversification, competitive benchmarking, and long-term strategic decision-making between 2026 and 2033 while identifying emerging application areas and evolving commercial opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1356 Million |

Market Revenue in 2033 | USD 2096.86 Million |

CAGR (2026 - 2033) | 5.6% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | ADM, Cargill, Roquette, Ingredion Incorporated, International Flavors & Fragrances Inc., Bunge Global SA, Kerry Group plc, BENEO GmbH, Axiom Foods, Inc., Puris, Emsland Group, Cosucra Groupe Warcoing SA, Burcon NutraScience Corporation, Sotexpro |

Customization & Pricing | Available on Request (10% Customization is Free) |