Reports

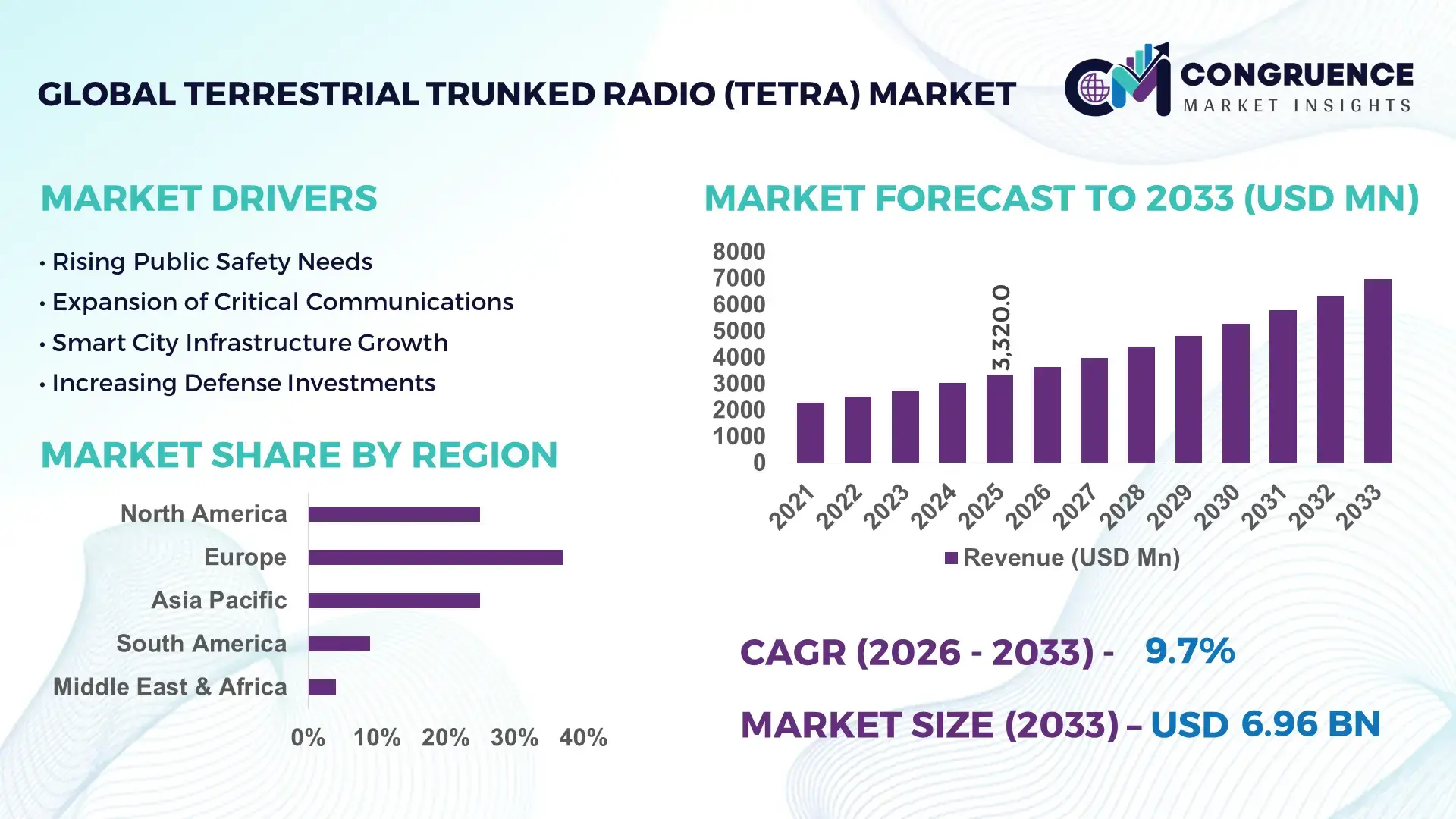

The Global Terrestrial Trunked Radio (TETRA) Market was valued at USD 3320.01 Million in 2025 and is anticipated to reach a value of USD 6962.95 Million by 2033 expanding at a CAGR of 9.7% between 2026 and 2033. Rapid migration toward mission-critical broadband communication networks across public safety, transportation, utilities, and defense sectors is accelerating advanced TETRA deployment, with hybrid LTE-TETRA integration reducing emergency response latency by nearly 35% compared to legacy analog systems.

Germany remains the dominant country within the global TETRA ecosystem, accounting for nearly 18% of European deployment capacity in 2026, supported by over USD 420 million in public safety communication modernization investments. Nationwide adoption across railway operations, industrial manufacturing, airport security, and emergency services exceeds 72% among federal response agencies. Compared to conventional private mobile radio systems, integrated TETRA-LTE networks in Germany improve spectrum efficiency by approximately 40% while lowering network downtime by 22%, strengthening operational continuity across high-risk industrial environments and critical national infrastructure.

Market participants prioritizing interoperable, encrypted, and broadband-ready TETRA platforms are securing stronger long-term contracts across high-security and infrastructure-intensive industries.

Market Size & Growth: USD 3320.01 Million in 2025 reaching USD 6962.95 Million by 2033, driven by secure mission-critical communication upgrades and LTE-TETRA convergence across public safety networks.

Top Growth Drivers: Public safety modernization contributes 38%, transportation communication upgrades 27%, and defense network digitization 21% of total market expansion momentum.

Short-Term Forecast: By 2027, advanced TETRA deployment lowers emergency coordination delays by 31% and improves field communication efficiency by 28%.

Emerging Technologies: AI-enabled dispatch systems, cloud-integrated network management, and broadband-TETRA hybrid architecture increase network reliability by over 33%.

Regional Leaders: Europe exceeds USD 2.8 Billion with rail modernization growth, Asia-Pacific surpasses USD 1.9 Billion through smart city expansion, and Middle East demand crosses USD 920 Million from energy-sector security upgrades.

Consumer/End-User Trends: More than 68% of public safety agencies prioritize encrypted digital radio infrastructure over analog communication systems in 2026 procurement cycles.

Pilot/Case Example: In 2025, a metropolitan transport authority deployment improved incident response coordination by 37% and reduced communication blackout zones by 24%.

Competitive Landscape: Motorola Solutions controls nearly 24% market share alongside Airbus, Sepura, Hytera, and Frequentis competing through interoperable secure-network platforms.

Regulatory & ESG Impact: Critical communication compliance standards reduced unauthorized network access incidents by 29% across government-led deployments between 2024 and 2026.

Investment & Funding: Global investments exceeded USD 1.4 Billion in 2025, led by cross-border infrastructure partnerships and resilient communication network expansion projects.

Innovation & Future Outlook: Next-generation broadband-ready TETRA ecosystems and AI-assisted command platforms are accelerating high-capacity secure communication strategies across smart infrastructure sectors.

Public safety agencies contribute nearly 41% of total industry demand, followed by transportation at 26% and utilities at 18%, reflecting the market’s dependence on secure real-time communication infrastructure. Recent innovations include AI-powered dispatch optimization, encrypted broadband interoperability, and compact multi-band radios improving operational uptime by 30%. Europe continues leading deployment activity, while Asia-Pacific records over 34% growth in smart transit communication investments amid digital infrastructure expansion and stricter cybersecurity regulations. The market is steadily shifting toward unified mission-critical communication ecosystems supporting long-term strategic modernization initiatives.

The Terrestrial Trunked Radio (TETRA) market is rapidly transforming into a strategic infrastructure segment as governments, transport operators, and industrial enterprises prioritize resilient mission-critical communication systems. Rising cybersecurity threats and emergency-response modernization programs are accelerating procurement cycles, particularly across border security, utilities, and rail networks. Regulatory pressure surrounding encrypted communication compliance and interoperable emergency coordination is reshaping vendor competition and capital allocation across Europe and Asia-Pacific.

Broadband-integrated TETRA architecture improves operational efficiency by 42% while reducing network maintenance costs by 26% compared to legacy analog radio systems. Europe leads in deployment volume, while Asia-Pacific leads in adoption innovation with nearly 36% growth in smart transit communication integration. By 2028, integrated command-and-control platforms are projected to reduce emergency response coordination time by 33%. ESG-focused network modernization is also emerging as a competitive advantage, lowering power consumption across upgraded communication infrastructure by approximately 18% and strengthening regulatory compliance access for public-sector contracts.

In 2025, a large metropolitan rail operator upgraded to hybrid TETRA-LTE systems and improved incident communication accuracy by 29% during peak operations. Leading companies are shifting investments toward AI-assisted dispatch systems, edge-network optimization, and secure broadband interoperability platforms. Organizations optimizing secure, scalable, and low-latency communication ecosystems are positioning themselves to dominate next-generation critical infrastructure networks.

Mission-critical communication modernization is accelerating TETRA deployment across transportation, utilities, defense, and emergency response sectors as agencies replace aging analog infrastructure with encrypted digital networks. More than 68% of public safety organizations prioritized interoperable communication investments in 2025, while integrated TETRA-LTE systems improved response coordination efficiency by 35%. Europe’s expanding rail modernization initiatives and heightened geopolitical security concerns are forcing governments to strengthen resilient communication infrastructure. This demand surge is reshaping supply chains and accelerating semiconductor sourcing diversification for secure radio equipment. In response, leading vendors are expanding manufacturing capacity, increasing software-defined radio investments, and forming strategic interoperability partnerships to secure long-term government contracts and optimize nationwide mission-critical communication ecosystems globally.

High deployment costs, spectrum licensing complexity, and infrastructure integration challenges are constraining large-scale TETRA expansion across emerging economies and fragmented industrial networks. Advanced secure communication installations increase upfront infrastructure expenditure by nearly 32%, while cross-border interoperability compliance adds approximately 18% to deployment timelines. Many developing regions still face inadequate broadband backhaul infrastructure, limiting hybrid TETRA-LTE scalability for mission-critical operations. Semiconductor concentration across select Asian manufacturing hubs also creates procurement volatility and extended equipment lead times during geopolitical disruptions. To mitigate operational risk, companies are diversifying component suppliers, securing long-term chipset agreements, and accelerating software-driven network virtualization strategies that reduce hardware dependency while improving deployment flexibility and lifecycle cost efficiency across complex communication environments.

AI-assisted dispatch systems, edge-enabled communication architecture, and broadband-ready TETRA integration are redefining the market’s next competitive phase. Hybrid mission-critical communication platforms improve network coordination efficiency by 41% while reducing operational downtime by nearly 24% across transportation and energy infrastructure environments. Smart city investments across Asia-Pacific and Middle Eastern industrial corridors are accelerating secure communication adoption, with digital infrastructure spending rising over 30% between 2025 and 2027. A major innovation shift toward cloud-managed command platforms is creating new demand for scalable software-driven ecosystems rather than hardware-centric deployments. Companies are responding through aggressive R&D expansion, ecosystem partnerships, and integrated cybersecurity capabilities, positioning themselves to dominate high-density urban communication networks and next-generation industrial safety infrastructure globally.

Aging network infrastructure, fragmented interoperability standards, and escalating cybersecurity threats are constraining long-term scalability across mission-critical communication ecosystems. More than 27% of legacy TETRA installations require substantial hardware modernization, while encrypted broadband integration increases network complexity by nearly 22%. Strict data protection regulations across Europe and rising cyberattack frequency against public infrastructure are forcing operators to redesign security architecture and compliance frameworks simultaneously. Limited rural broadband coverage also restricts hybrid communication deployment consistency in remote industrial zones and emergency response corridors. To remain competitive, companies must accelerate AI-driven threat monitoring, expand secure cloud interoperability, and strengthen strategic telecom partnerships. Vendors failing to optimize resilient, low-latency, and regulation-compliant communication systems risk losing long-term infrastructure modernization contracts globally.

Hybrid TETRA-LTE deployments increased 34% across critical infrastructure networks in 2025, reshaping communication architecture. Public safety agencies and transportation operators are integrating broadband-enabled TETRA systems to reduce response latency by 31% and improve interoperability across multi-agency operations. Vendors are optimizing edge-enabled command platforms and accelerating software-defined radio deployment to manage rising encrypted data traffic. Regulatory pressure surrounding emergency communication resilience is forcing faster replacement of analog systems.

Cloud-managed dispatch operations reduced communication maintenance workloads by 28%, redefining operational efficiency standards. Enterprises are shifting from hardware-centric network management toward centralized software-controlled platforms, cutting manual monitoring requirements by 24%. TETRA providers are restructuring service portfolios around predictive diagnostics and remote network optimization. A non-obvious shift is emerging as utilities prioritize operational continuity analytics over hardware expansion, changing procurement priorities toward lifecycle efficiency instead of equipment volume.

Asia-Pacific infrastructure deployments expanded 36%, while European modernization projects intensified network optimization programs. Smart transit projects and industrial corridor expansion are accelerating demand for scalable TETRA communication ecosystems across urban infrastructure environments. Europe continues prioritizing encrypted interoperability upgrades, improving multi-network coordination efficiency by 27%. Companies are responding through regional manufacturing expansion, localized integration partnerships, and accelerated chipset diversification strategies amid continuing semiconductor supply chain restructuring.

Subscription-based communication service models improved deployment flexibility by 26%, shifting traditional procurement structures. Organizations increasingly prefer managed communication ecosystems instead of fully owned infrastructure, reducing upgrade complexity and lowering operational transition time by 22%. TETRA vendors are aggressively expanding managed-service partnerships, cybersecurity integration offerings, and AI-assisted monitoring capabilities. This transformation is redefining competitive positioning as companies shift from equipment suppliers toward long-term mission-critical communication service providers.

The Terrestrial Trunked Radio (TETRA) market is segmented by type, application, and end-user, reflecting diverse operational priorities across mission-critical communication environments. Portable Radios account for nearly 34% of product demand due to mobility advantages, while Public Safety Communication contributes over 38% of application usage driven by emergency coordination requirements. Demand is shifting toward hybrid broadband-enabled systems within transportation and utility operations as organizations prioritize interoperability and encrypted communication. Public Safety Agencies remain the dominant end-user group, although Industrial Enterprises are rapidly accelerating adoption through smart infrastructure integration. Vendors are increasingly optimizing scalable network ecosystems, software-defined platforms, and managed communication services to capture evolving multi-sector deployment requirements.

Portable Radios dominate the Terrestrial Trunked Radio (TETRA) market with nearly 34% share, driven by operational mobility, instant communication access, and strong deployment across emergency response, transportation, and defense sectors. Their lightweight design and encrypted voice capabilities make them structurally critical for field-intensive operations where uninterrupted connectivity directly impacts coordination efficiency. Meanwhile, Network Infrastructure represents the fastest-growing segment, expanding adoption by over 29% as organizations prioritize broadband interoperability, AI-assisted dispatch integration, and scalable mission-critical communication ecosystems. The market is shifting from hardware-centric deployments toward intelligent network optimization platforms.

Mobile Radios continue maintaining strong demand across transportation fleets and industrial logistics due to stable long-range connectivity advantages, while Base Stations and Dispatch Consoles collectively account for approximately 38% of total deployments because of their centralized operational control relevance. Companies are accelerating investment in software-defined architecture, cloud-managed communication systems, and interoperable broadband integration. Vendors prioritizing scalable network infrastructure and advanced dispatch capabilities are capturing long-term modernization contracts, while standalone legacy radio systems are gradually losing strategic positioning in high-security communication environments.

“According to a 2025 report by the European Telecommunications Standards Institute, broadband-integrated TETRA network infrastructure was adopted by over 64% of large-scale public safety communication projects, resulting in a 32% improvement in multi-agency coordination efficiency, reinforcing its growing strategic importance.”

Public Safety Communication leads the Terrestrial Trunked Radio (TETRA) market with approximately 38% share due to continuous dependency on secure, low-latency, and interoperable communication systems during emergency operations. High deployment concentration exists because public safety agencies require uninterrupted encrypted communication across police, fire, medical, and disaster-response networks. Defense Communication is emerging as the fastest-growing application segment, with adoption increasing by nearly 31% as governments intensify border surveillance modernization and mission-critical cybersecurity integration. Regulatory pressure surrounding secure national infrastructure communication is accelerating procurement activity globally.

Transportation Management remains a mature high-volume segment because rail operators, airports, and urban transit systems rely heavily on real-time communication coordination. In contrast, Utility Operations and Industrial Communication are rapidly shifting toward hybrid TETRA-LTE ecosystems supporting remote asset monitoring and operational continuity. Emergency Response, Utility Operations, and Industrial Communication collectively contribute nearly 44% of application demand. Companies are repositioning deployment strategies around integrated command platforms, AI-enabled dispatch optimization, and scalable communication infrastructure to capture rising demand for resilient multi-network coordination across critical infrastructure environments.

“According to a 2025 report by the International Association of Public Safety Communications Officials, Public Safety Communication systems were deployed across over 18,000 emergency response organizations, improving incident coordination efficiency by 35%, highlighting its rapid operational adoption.”

Public Safety Agencies dominate the Terrestrial Trunked Radio (TETRA) market with nearly 41% demand concentration because of their constant requirement for encrypted, real-time, mission-critical communication infrastructure. High usage intensity across emergency response coordination, disaster management, and law enforcement operations continues reinforcing long-term procurement cycles. Defense and Military represents the fastest-growing end-user segment, with adoption expanding by approximately 30% as geopolitical security pressures accelerate secure communication modernization and cross-border operational interoperability investments.

Transportation Sector remains a structurally strong adopter because railway operators and urban transit authorities depend on uninterrupted communication for network coordination and passenger safety. In comparison, Energy and Utilities are shifting rapidly toward intelligent communication ecosystems supporting remote operational visibility and infrastructure resilience. Industrial Enterprises, Government Organizations, and Energy and Utilities collectively account for nearly 46% of total market demand. Vendors are responding through customized deployment models, managed communication services, and long-term interoperability partnerships. Companies targeting defense modernization and industrial digitalization programs are capturing stronger recurring contract opportunities and higher-value infrastructure integration projects globally.

“According to a 2025 report by the International Telecommunication Union, adoption among Defense and Military organizations increased by 28%, with over 7,500 agencies implementing advanced encrypted TETRA communication solutions, leading to a 26% improvement in operational coordination efficiency, indicating a strong shift in demand dynamics.”

Europe accounted for the largest market share at 37% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2026 and 2033.

Europe maintains demand concentration through large-scale public safety modernization, rail communication upgrades, and strict encrypted communication compliance standards across Germany, France, and the U.K. North America contributes nearly 29% of global demand, driven by defense communication investments and integrated emergency-response infrastructure. Asia-Pacific is rapidly accelerating deployment volume through smart city expansion, industrial corridor development, and transportation digitization programs, with regional infrastructure communication projects increasing by over 34% in 2025. Supply chain diversification and localized semiconductor sourcing are reshaping procurement strategies globally as operators prioritize resilient communication ecosystems. Companies are increasingly focusing investments on Asia-Pacific expansion, European interoperability upgrades, and North American hybrid broadband communication deployments to strengthen long-term competitive positioning.

North America holds nearly 29% of global Terrestrial Trunked Radio (TETRA) demand, supported by extensive deployment across defense communication, transportation management, and emergency response infrastructure. Public safety modernization programs and rising cybersecurity threats are accelerating adoption of encrypted broadband-integrated communication systems. Federal infrastructure resilience initiatives and stricter emergency communication standards are forcing operators to replace aging analog networks with interoperable digital ecosystems. Hybrid TETRA-LTE deployment increased by 32% across critical infrastructure operations during 2025, while large-scale transit communication upgrades improved operational coordination efficiency by 27%. Enterprises increasingly prefer scalable software-defined communication architecture with centralized network management capabilities. Vendors are prioritizing regional partnerships, AI-assisted dispatch optimization, and secure cloud interoperability investments to capture expanding mission-critical infrastructure contracts across North America.

Europe accounts for approximately 37% of the Terrestrial Trunked Radio (TETRA) market, led by Germany, France, and the U.K. through extensive public safety and railway communication modernization programs. Strict encrypted communication regulations and cybersecurity compliance frameworks are accelerating replacement of fragmented analog systems with interoperable digital networks. Sustainability-focused infrastructure strategies are also driving energy-efficient network deployment, reducing communication power consumption by nearly 18% across upgraded systems. Integrated TETRA-LTE adoption increased by 31% in transportation and utility sectors during 2025 as organizations optimized operational continuity and multi-agency coordination. Enterprises across Europe prioritize long-term compliance reliability, low-latency performance, and secure interoperability over short-term cost advantages. Vendors unable to meet evolving security, resilience, and sustainability standards are rapidly losing competitiveness across large-scale infrastructure modernization projects.

Asia-Pacific represents the fastest-expanding Terrestrial Trunked Radio (TETRA) market, driven by large-scale infrastructure digitization across China, India, Japan, and Southeast Asia. The region accounts for nearly 26% of global deployment volume, supported by rapid smart city expansion, transportation modernization, and industrial corridor development. Localized manufacturing advantages and semiconductor ecosystem expansion are improving equipment availability while reducing deployment lead times by approximately 21%. Hybrid communication network deployment across transportation and utility infrastructure increased by over 36% during 2025 as enterprises accelerated operational digitization programs. Organizations across Asia-Pacific prioritize scalable, cost-efficient, and rapidly deployable communication systems capable of supporting dense urban infrastructure. Global vendors are expanding regional production partnerships, localized integration capabilities, and software-driven network platforms to capture accelerating mission-critical communication demand across high-growth economies.

South America contributes nearly 6% of global Terrestrial Trunked Radio (TETRA) demand, with Brazil and Argentina leading deployment across transportation, mining, and public safety communication networks. Growing urban transit modernization and industrial safety requirements are accelerating demand for encrypted digital communication infrastructure. However, high deployment costs and inconsistent broadband infrastructure continue constraining large-scale hybrid network scalability across several emerging markets. Public safety communication upgrades increased by approximately 19% during 2025, while mining-sector communication deployments improved operational coordination efficiency by 24%. Enterprises across the region remain highly price-sensitive and increasingly prefer modular deployment models with lower upfront infrastructure requirements. Vendors focusing on localized service partnerships, flexible financing structures, and scalable network architecture are capturing stronger long-term positioning despite infrastructure and regulatory limitations.

Middle East & Africa accounts for nearly 9% of the global Terrestrial Trunked Radio (TETRA) market, supported by expanding infrastructure modernization across the UAE, Saudi Arabia, and South Africa. Oil and gas operations, smart construction projects, and large-scale transportation developments are driving strong demand for resilient mission-critical communication systems. Government-backed infrastructure diversification programs and industrial digitalization investments are accelerating deployment of broadband-integrated communication ecosystems. Advanced TETRA network installations across energy and transport sectors increased by approximately 28% during 2025, while multi-site industrial communication integration improved operational coordination efficiency by 26%. Enterprises increasingly prioritize durable, scalable, and low-latency communication infrastructure capable of operating across remote industrial environments. Global vendors are strengthening regional partnerships and localized deployment capabilities to secure long-term infrastructure transformation contracts across the region.

Germany – 18% market share: Germany leads the Terrestrial Trunked Radio (TETRA) market through extensive railway communication modernization, strong public safety infrastructure, and large-scale encrypted network deployment across industrial sectors.

United States – 16% market share: The United States dominates Terrestrial Trunked Radio (TETRA) adoption through defense communication investments, emergency-response modernization programs, and rapid hybrid broadband integration across critical infrastructure networks.

Motorola Solutions, Airbus, Sepura, Hytera Communications, and Frequentis collectively control nearly 61% of the Terrestrial Trunked Radio (TETRA) market, competing through secure interoperability, broadband integration, and AI-assisted communication platforms. Global leaders are competing directly with regional integrators and cost-focused communication vendors across transportation, defense, utilities, and public safety deployments. Technology performance and lifecycle optimization increasingly outweigh pure pricing strategies, with broadband-integrated systems improving operational coordination efficiency by 34% and reducing maintenance costs by 22%. Companies are accelerating software-defined radio innovation, regional manufacturing expansion, and cybersecurity-focused partnerships to strengthen deployment scalability. Market competition is shifting toward hybrid TETRA-LTE ecosystems and managed communication services, redefining traditional hardware-centric positioning. Strict regulatory compliance, encrypted network certification, and infrastructure integration complexity continue creating strong entry barriers. Winning in this market requires scalable secure architecture, localized execution capability, interoperability leadership, and long-term infrastructure modernization partnerships.

Motorola Solutions

Airbus

Sepura

Hytera Communications

Frequentis

JVCKENWOOD Corporation

Rohill Engineering

DAMM Cellular Systems

Simoco Wireless Solutions

Leonardo S.p.A.

Teltronic

NEC Corporation

Codan Communications

Zetron Inc.

Hybrid TETRA-LTE communication architecture remains the dominant technology shift transforming mission-critical communication networks across public safety, transportation, and industrial operations. More than 62% of newly deployed TETRA systems in 2026 integrate broadband capabilities to support real-time video, AI-assisted dispatch, and multi-network interoperability. Compared to legacy narrowband radio systems, hybrid TETRA-LTE platforms improve operational coordination efficiency by 42% while reducing maintenance complexity by 24%. Organizations deploying integrated communication ecosystems are achieving faster emergency response synchronization and stronger encrypted data continuity across geographically distributed operations.

Virtualized network infrastructure and cloud-managed dispatch technologies are emerging as major operational differentiators between established vendors and regional integrators. Software-defined TETRA platforms reduce infrastructure deployment time by approximately 28% while improving scalability across transportation and utility communication environments. AI-enabled command systems are also reshaping incident management workflows, reducing manual dispatch processing workloads by nearly 31%. Companies investing aggressively in edge-network optimization, cybersecurity integration, and predictive communication analytics are capturing higher-value long-term modernization contracts across critical infrastructure sectors.

Between 2026 and 2028, disruptive technologies including satellite-supported TETRA connectivity, AI-driven situational awareness, and autonomous communication orchestration will redefine operational resilience standards. Advanced broadband-integrated communication ecosystems are expected to support over 70% of large-scale infrastructure modernization projects globally. Vendors capable of optimizing secure interoperability, low-latency performance, and scalable intelligent communication architecture will secure stronger competitive positioning as mission-critical communication requirements continue accelerating worldwide.

September 2025 – Motorola Solutions partnered with Nokia to develop a containerized tactical communication solution integrating TETRA and 5G technologies for U.K. defense agencies. The system improved secure field communication deployment flexibility by over 30%, strengthening military-grade operational resilience and expanding broadband-enabled mission-critical communication capabilities. [Defense Network Shift]

December 2024 – Airbus secured a nationwide communications contract with Rijkswaterstaat in the Netherlands, deploying Agnet MCX broadband push-to-talk technology to replace narrowband TETRA communication systems. The project expanded nationwide operational coverage while supporting 1-to-1 migration toward broadband-enabled emergency coordination infrastructure. [Broadband Migration Push]

April 2026 – Motorola Solutions announced satellite-enabled connectivity integration with T-Mobile’s T-Satellite network for APX NEXT smart radios, extending mission-critical communication coverage into remote operational zones. The initiative improved resilient communication accessibility and strengthened uninterrupted emergency-response connectivity through low-earth-orbit satellite infrastructure integration. [Satellite Resilience Expansion]

April 2025 – Motorola Solutions launched the AI-enabled SVX communication device integrating body camera, AI assistant, and APX NEXT radio functionality. The platform reduced patrol report-writing workloads by over 40% during field testing with 150 users, significantly optimizing emergency-response workflow efficiency and real-time situational awareness. [AI Workflow Optimization]

The Terrestrial Trunked Radio (TETRA) Market Report delivers comprehensive analysis across key product categories including Portable Radios, Mobile Radios, Base Stations, Dispatch Consoles, and Network Infrastructure. The study evaluates critical applications such as Public Safety Communication, Transportation Management, Utility Operations, Industrial Communication, Emergency Response, and Defense Communication. End-user assessment covers Public Safety Agencies, Transportation Sector, Energy and Utilities, Defense and Military, Industrial Enterprises, and Government Organizations across North America, Europe, Asia-Pacific, South America, and Middle East & Africa. Advanced technology coverage includes hybrid TETRA-LTE systems, AI-assisted dispatch platforms, cloud-managed communication networks, and broadband interoperability infrastructure.

The report analyzes more than 25 strategic market indicators, including deployment concentration, adoption intensity, interoperability integration levels, and operational efficiency trends. Public safety communication accounts for nearly 38% of deployment demand, while broadband-integrated TETRA systems exceed 62% adoption across new critical infrastructure projects. The analysis also profiles major global communication vendors, regional integrators, and emerging technology providers shaping competitive positioning between 2026 and 2033.

The report supports investment planning, regional expansion, procurement optimization, and infrastructure modernization strategies by identifying high-priority deployment sectors, technology transition patterns, and evolving operational requirements across mission-critical communication ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 3320.01 Million |

|

Market Revenue in 2033 |

USD 6962.95 Million |

|

CAGR (2026 - 2033) |

9.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Motorola Solutions, Airbus, Sepura, Hytera Communications, Frequentis, JVCKENWOOD Corporation, Rohill Engineering, DAMM Cellular Systems, Simoco Wireless Solutions, Leonardo S.p.A., Teltronic, NEC Corporation, Codan Communications, Zetron Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |