Reports

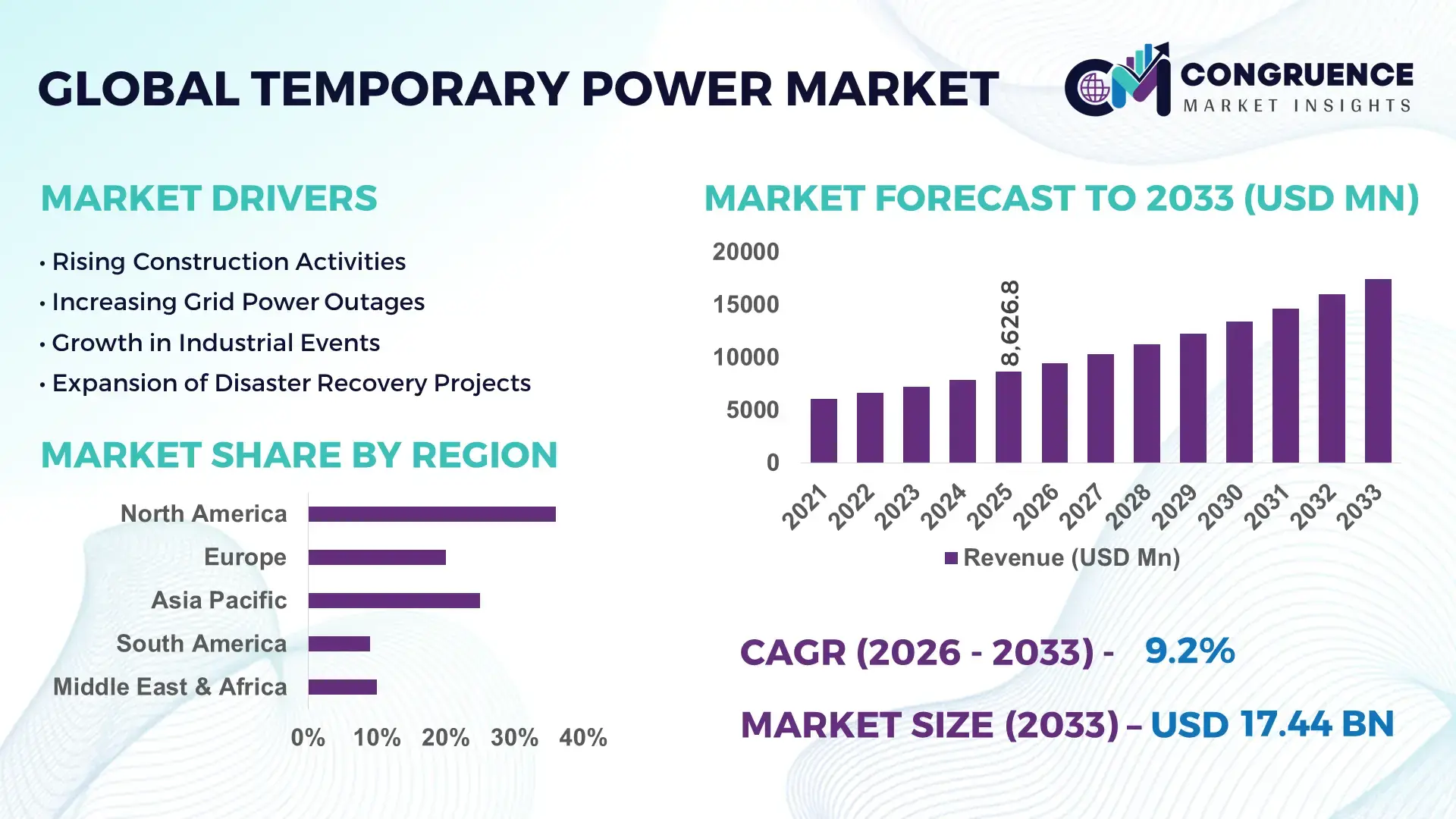

The Global Temporary Power Market was valued at USD 8626.8 Million in 2025 and is anticipated to reach a value of USD 17443.38 Million by 2033 expanding at a CAGR of 9.2% between 2026 and 2033. Rapid expansion of hyperscale data centers, grid instability during extreme weather events, and large-scale infrastructure modernization projects are accelerating deployment of mobile generators, battery-integrated temporary power systems, and hybrid rental fleets across industrial and commercial sectors.

The United States dominates the global temporary power market with an estimated 31% share, supported by more than 5.5 GW of active temporary rental power capacity linked to oil & gas operations, data center construction, utilities, and disaster recovery projects. Following multiple grid disruption events and hurricane-related outages across North America in 2025–2026, utility contractors increased temporary power deployment cycles by nearly 18%, while hybrid diesel-battery systems improved fuel efficiency by over 22% compared to conventional standalone generator fleets. Compared with Europe’s slower utility replacement cycle, North America continues to lead in fast-response power deployment due to stronger investment in resilient energy infrastructure and digital monitoring systems.

Companies prioritizing low-emission hybrid rental fleets, remote monitoring platforms, and high-capacity modular power units are positioned to secure stronger margins in high-demand industrial and emergency-response applications.

Market Size & Growth: USD 8626.8 million in 2025 projected to reach USD 17443.38 million by 2033, supported by rising grid instability and infrastructure expansion.

Top Growth Drivers: Industrial construction demand increased 34%, utility backup deployment rose 21%, and oil & gas temporary power utilization expanded 17%.

Short-Term Forecast: By 2028, hybrid temporary power systems are expected to reduce onsite fuel consumption by 28% while improving operational efficiency.

Emerging Technologies: AI-enabled fleet monitoring, lithium battery integration, and automated load-balancing systems are transforming advanced temporary power operations.

Regional Leaders: North America surpassed USD 3.1 billion, Asia-Pacific exceeded USD 2.7 billion, and Europe crossed USD 2.2 billion with stronger grid resilience adoption.

Consumer/End-User Trends: More than 46% of large commercial facilities adopted temporary backup power contracts following weather-driven and supply chain-related outages.

Pilot/Case Example: A 2026 mining project in Australia improved operational power reliability by 31% through hybrid mobile generator deployment.

Competitive Landscape: Leading companies controlled nearly 14% combined market share, with Aggreko, Caterpillar, Cummins, Atlas Copco, and APR Energy dominating fleet expansion.

Regulatory & ESG Impact: Emission-control regulations reduced diesel-only fleet expansion by 19%, accelerating low-emission temporary power adoption.

Investment & Funding: Global investments exceeded USD 4.3 billion between 2024 and 2026, focused on modular fleet expansion and smart energy systems.

Innovation & Future Outlook: Advanced modular microgrids and digitally managed temporary energy ecosystems are strengthening critical infrastructure resilience globally.

Construction and infrastructure projects account for nearly 38% of temporary power utilization, followed by utilities and oil & gas operations with a combined contribution exceeding 33%. Advanced hybrid generators, battery storage integration, and AI-driven remote monitoring systems are improving fuel efficiency and operational uptime across high-demand applications. Asia-Pacific continues to witness strong deployment growth due to industrial expansion and grid modernization programs, while Europe is accelerating adoption of low-emission temporary energy solutions under stricter sustainability regulations. Increasing integration of modular microgrid-based temporary power systems is emerging as a major industry transition, particularly as supply chain diversification and energy security initiatives reshape procurement strategies worldwide. The market is steadily evolving toward digitally managed, lower-emission, high-efficiency temporary power ecosystems designed for critical infrastructure resilience.

The temporary power market has become strategically critical as utilities, industrial operators, and infrastructure developers prioritize energy resilience amid rising grid instability and accelerated construction cycles. Infrastructure modernization programs across the United States, India, and the Gulf countries are increasing demand for rapid-deployment power systems capable of supporting data centers, mining operations, transport networks, and emergency backup applications. In parallel, stricter emission-control frameworks are reshaping rental fleet strategies, driving replacement of aging diesel-only units with hybrid and gas-powered systems. Companies integrating digital fleet management and predictive maintenance platforms are improving equipment utilization rates by nearly 20%, strengthening operational competitiveness.

Hybrid temporary power systems now deliver up to 25% lower fuel consumption compared to legacy diesel generators while reducing maintenance intervals through battery-assisted load balancing. China continues scaling large industrial temporary power deployments linked to manufacturing expansion, while Germany is prioritizing lower-emission mobile power systems aligned with energy transition policies. During a 2026 utility maintenance project in Texas, modular hybrid generator fleets reduced downtime response time by 30%, demonstrating the operational advantage of intelligent mobile power infrastructure.

Over the next two to three years, adoption of remotely monitored and modular temporary power systems is expected to accelerate across logistics hubs, hyperscale data centers, and renewable energy integration projects. Major suppliers are expanding regional service networks, securing long-term industrial contracts, and forming technology partnerships focused on battery integration and smart-grid compatibility. Companies capable of combining rapid deployment capability, lower operating costs, and emission-compliant fleet solutions will strengthen long-term competitive positioning in mission-critical energy applications.

Large-scale infrastructure modernization and rising grid reliability concerns are accelerating temporary power deployment across industrial and commercial sectors. Utility outage incidents increased by nearly 16% across major industrial economies during 2025, while data center construction activity expanded more than 22%, intensifying demand for high-capacity mobile power systems. In the United States, emergency backup deployment contracts increased significantly following extreme weather-related grid disruptions, pushing rental fleet utilization above 80% during peak periods. This operational pressure is driving companies toward hybrid generators, remote monitoring systems, and modular power units capable of faster deployment and lower fuel consumption. Major suppliers are expanding localized service hubs, strengthening fuel logistics partnerships, and investing in AI-enabled fleet diagnostics to improve uptime reliability and response efficiency across critical infrastructure operations.

Rising diesel price volatility and tightening emission regulations continue to pressure profitability across temporary power operations. Fuel expenses account for nearly 35% of operating costs for conventional rental fleets, while compliance-related equipment upgrades increased fleet conversion expenditure by approximately 18% during 2025. In Germany and the United Kingdom, stricter low-emission standards are limiting deployment of aging diesel generators, creating replacement pressure for smaller rental providers with limited capital flexibility. Supply-chain disruptions affecting engine components and battery modules have also extended equipment delivery timelines by over 20% in certain industrial markets. To reduce operational risk, companies are diversifying sourcing networks, accelerating gas-powered fleet adoption, and securing long-term maintenance contracts that stabilize service costs while improving deployment continuity in emission-regulated environments.

Advanced hybrid temporary power systems integrated with battery storage and AI-driven monitoring platforms are creating strong operational efficiency opportunities. Hybrid deployments can reduce onsite fuel usage by up to 28% while lowering maintenance downtime through intelligent load optimization and predictive diagnostics. India’s industrial corridor expansion and Southeast Asia’s manufacturing diversification are generating untapped demand for scalable temporary energy infrastructure capable of supporting rapid facility commissioning. Companies are increasingly investing in modular microgrid solutions that integrate temporary power with renewable energy assets, particularly for mining and remote industrial operations. In 2026, multiple suppliers expanded partnerships with battery technology firms to strengthen low-emission fleet capabilities and digital energy management services. The emerging shift toward subscription-based energy-as-a-service models is also creating recurring revenue opportunities beyond conventional equipment rentals.

Expanding temporary power networks across complex industrial environments remains operationally challenging due to integration complexity, workforce shortages, and evolving technical requirements. More than 27% of industrial operators reported delays linked to limited availability of skilled power technicians and remote monitoring specialists during 2025. In Australia and Canada, remote mining and energy projects continue facing logistical deployment bottlenecks caused by transportation limitations and maintenance accessibility issues. Simultaneously, cybersecurity exposure is increasing as connected fleet management platforms and IoT-enabled generators become standard across critical operations. These pressures directly affect deployment consistency, service reliability, and long-term scalability. Companies are responding through technician training programs, localized maintenance infrastructure, and investment in secure digital fleet ecosystems designed to support large-scale, multi-site temporary power operations with higher operational resilience.

Diesel Generators remain the leading segment, accounting for nearly 47% of temporary power deployments due to high scalability, immediate load response capability, and suitability for heavy industrial applications. Construction sites, mining operations, and utility maintenance projects continue prioritizing diesel-based systems for continuous high-capacity output and established fuel infrastructure. However, Gas Generators are emerging as the fastest-growing segment as operators pursue lower-emission alternatives capable of reducing fuel-related operating costs by approximately 15%. Battery Storage Systems are also witnessing accelerated adoption, particularly for short-duration backup applications and hybrid fleet integration where fuel efficiency gains exceed 25%. Mobile Power Units are expanding across emergency response and remote infrastructure projects due to rapid deployment flexibility, while Load Banks remain strategically relevant for power testing and commissioning operations. Manufacturers are increasing investments in modular hybrid configurations, digital monitoring compatibility, and emission-compliant generator platforms to align with evolving industrial procurement priorities.

Industrial Operations represent the dominant application segment, contributing nearly 36% of total temporary power utilization due to continuous energy requirements across manufacturing plants, mining facilities, and oilfield operations. High-capacity deployment needs and operational continuity pressures continue concentrating demand within energy-intensive industrial sites. Disaster Recovery is emerging as the fastest-growing application as climate-driven grid disruptions and infrastructure failures increase emergency deployment requirements by over 22%. Construction Sites remain a stable high-volume segment supported by transport, commercial, and urban infrastructure projects, while Utility Support applications are expanding through grid modernization and substation maintenance activities. Emergency Backup systems are increasingly integrated into hospitals, logistics hubs, and hyperscale facilities where downtime reduction has become operationally critical. Suppliers are scaling mobile fleet availability, expanding regional service contracts, and integrating automated load-balancing technologies to improve deployment speed and system reliability across high-demand operational environments.

Construction remains the leading end-user segment, accounting for approximately 33% of temporary power demand due to continuous deployment across transport infrastructure, commercial real estate, and industrial expansion projects. Large-scale infrastructure modernization programs in the United States, India, and the Gulf countries continue driving high equipment utilization rates and long-duration rental contracts. Utilities represent the fastest-growing end-user group as grid modernization projects and emergency restoration activities increase temporary power deployment by nearly 24%. Oil and Gas operators continue prioritizing high-capacity mobile generators for remote drilling and pipeline operations, while Mining companies are accelerating adoption of hybrid systems to reduce fuel logistics complexity. Manufacturing facilities increasingly deploy modular backup systems to minimize production interruptions during maintenance cycles. Providers are responding through sector-specific fleet customization, long-term maintenance agreements, and localized service expansion strategies designed to improve uptime performance and contract retention across industrial customers.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2026 and 2033.

Grid Resilience and Data Infrastructure Expansion

North America maintains strong market leadership through high deployment concentration across utilities, data centers, oil & gas operations, and infrastructure modernization projects. The region contributes nearly 36% of global temporary power demand, supported by extensive rental fleet networks and advanced hybrid generator adoption. Utility restoration contracts and hyperscale data center construction activity increased mobile power deployment by over 21% during 2025. The United States and Canada continue investing in modular temporary energy systems capable of supporting grid maintenance, renewable integration, and emergency response operations. Major suppliers are expanding localized service hubs and AI-enabled fleet monitoring capabilities to improve response speed and reduce operational downtime across industrial corridors and disaster-prone infrastructure zones.

The United States remains the region’s operational center due to large-scale utility infrastructure upgrades, strong industrial construction activity, and expanding data center capacity. More than 5 GW of temporary rental power capacity was actively deployed across industrial and emergency-response applications during 2025. Federal infrastructure modernization programs and rising weather-related outage events are accelerating demand for rapid-deployment hybrid power systems. Companies are increasing investments in remote diagnostics, battery-integrated fleets, and regional maintenance partnerships to strengthen equipment availability and improve service continuity across high-demand operational environments.

Low-Emission Fleet Transformation Accelerates

Europe is undergoing rapid operational restructuring as stricter emission standards and energy transition policies reshape temporary power procurement strategies. The region accounts for approximately 24% of global deployment activity, with growing preference for gas-powered and hybrid temporary power systems across utilities, manufacturing, and infrastructure projects. Diesel-only fleet replacement activity increased by nearly 18% during 2025 following tighter environmental compliance requirements in Germany, France, and the United Kingdom. Companies are prioritizing modular low-emission power solutions with intelligent energy management capabilities to reduce fuel consumption and operational costs. Strategic partnerships between equipment suppliers and battery technology providers are strengthening hybrid fleet availability across industrial and municipal deployment networks.

Germany remains a key operational hub due to advanced industrial infrastructure, strong manufacturing activity, and aggressive decarbonization policies influencing temporary power adoption. Industrial operators increased deployment of gas-powered and battery-assisted mobile generators by approximately 23% during 2025 to comply with stricter low-emission operational standards. Utility maintenance projects and renewable integration programs are also driving demand for modular temporary power systems with digital monitoring capability. Suppliers are strengthening localized service operations and investing in hybrid fleet modernization to support high-efficiency industrial energy requirements.

Industrial Expansion Drives Deployment Scale

Asia-Pacific is emerging as the fastest-expanding regional market due to rapid industrialization, infrastructure development, and manufacturing diversification across China, India, Southeast Asia, and Australia. The region contributes nearly 29% of global temporary power deployment volume, supported by transport infrastructure projects, mining operations, and industrial corridor expansion. Construction-linked power demand increased by over 25% during 2025, while manufacturing facility backup deployments accelerated significantly amid grid reliability concerns. Temporary power suppliers are expanding regional inventory hubs, strengthening localized maintenance partnerships, and increasing modular fleet availability to support high-volume deployment requirements. The growing adoption of battery-integrated generator systems is also improving fuel efficiency across remote industrial operations.

China dominates regional deployment activity through large-scale industrial operations, infrastructure modernization programs, and extensive manufacturing capacity expansion. More than 40% of industrial temporary power utilization in Asia-Pacific is concentrated within Chinese construction, manufacturing, and mining sectors. Rapid deployment requirements linked to factory expansion and transport infrastructure projects are accelerating adoption of modular mobile power systems with remote monitoring capabilities. Domestic manufacturers are scaling production of hybrid generators and smart power distribution units to strengthen operational flexibility and reduce energy-related downtime across industrial facilities.

Mining and Infrastructure Demand Strengthens

South America is witnessing stable temporary power demand growth through mining expansion, transport infrastructure projects, and utility reliability challenges. The region represents nearly 7% of global deployment activity, with Chile, Brazil, and Peru driving most industrial power rental demand. Mining operations increased temporary power utilization by approximately 19% during 2025 due to remote extraction activity and grid accessibility limitations. Infrastructure bottlenecks and fuel logistics constraints continue affecting deployment consistency in certain remote operational zones. To improve equipment availability and response efficiency, companies are expanding regional maintenance facilities and strengthening fuel supply partnerships. Hybrid mobile power systems are also gaining traction across mining applications where operational efficiency and lower fuel transport dependency are becoming critical priorities.

Brazil leads regional temporary power utilization due to extensive infrastructure projects, industrial activity, and recurring grid reliability challenges across remote operational areas. Industrial backup deployment activity increased by nearly 17% during 2025, particularly within mining, manufacturing, and utility maintenance sectors. Logistics limitations in remote regions continue increasing demand for modular mobile generator fleets capable of rapid installation and flexible transport. Equipment providers are expanding localized service networks and hybrid fleet offerings to improve operational uptime and reduce fuel consumption across long-duration industrial deployment environments.

Energy Infrastructure Investment Expands Rapidly

Middle East & Africa continues strengthening its position through large-scale energy infrastructure investments, industrial diversification programs, and rising construction activity. The region contributes approximately 11% of global temporary power deployment demand, supported by oil & gas operations, utility expansion projects, and mega infrastructure developments. Temporary power utilization linked to industrial construction and event-driven deployment activity increased by over 20% during 2025. Gulf countries are accelerating adoption of hybrid temporary power systems to improve fuel efficiency and align with national sustainability initiatives. Companies are forming long-term partnerships with energy contractors and expanding regional fleet capacity to support continuous deployment requirements across industrial and infrastructure-intensive operational environments.

Saudi Arabia remains a strategic deployment hub due to large-scale infrastructure projects, industrial diversification programs, and extensive oil & gas operations requiring uninterrupted mobile energy support. Utility-linked temporary power deployments increased by approximately 22% during 2025 as industrial zones and transport projects expanded rapidly. Government-backed infrastructure modernization initiatives are accelerating demand for modular generator fleets with digital monitoring and lower-emission capabilities. Suppliers are strengthening regional partnerships, localized maintenance operations, and hybrid fleet investments to support long-duration deployment contracts across critical industrial and construction applications.

Aggreko, Caterpillar, Cummins, Atlas Copco, APR Energy, and United Rentals compete aggressively against regional rental operators and low-cost fleet providers. The top five players collectively control nearly 42% of global deployment capacity, competing through fleet availability, fuel efficiency, rapid mobilization, and hybrid-system integration. Advanced fleet monitoring reduced maintenance downtime by 18%, while hybrid generator adoption improved fuel efficiency by over 22%, intensifying technology-based competition. Global leaders are expanding service hubs, securing utility partnerships, and vertically integrating digital energy management capabilities. Regional players compete on pricing flexibility and localized response speed. High capital intensity, compliance costs, and fleet modernization requirements remain critical entry barriers requiring continuous operational innovation.

Aggreko

Caterpillar

Cummins

Atlas Copco

APR Energy

United Rentals

Generac Power Systems

Kohler Energy

Wärtsilä

HIMOINSA

Speedy Hire

Ashtead Group

Herc Rentals

Byrne Equipment Rental

Hybrid temporary power systems combining diesel or gas generators with battery storage have become the most influential technology shift across industrial and utility operations. These systems reduce fuel consumption by 20–30% compared to conventional diesel-only fleets while lowering maintenance intervals through intelligent load balancing. More than 38% of newly deployed temporary power fleets in 2026 included battery-assisted configurations, particularly across mining, construction, and remote infrastructure projects. Operators benefit from lower operating costs, faster response capability, and improved compliance with tightening emission standards. Large fleet providers and industrial contractors are accelerating partnerships with battery integrators and energy management software developers to strengthen deployment flexibility and reduce fuel logistics dependency.

AI-enabled remote monitoring and predictive maintenance platforms are transforming temporary power fleet management. Connected fleet systems reduced unplanned downtime by nearly 18% and improved equipment utilization rates by over 15% across large industrial deployments. Compared with legacy manual monitoring processes, automated diagnostics significantly improve response speed and maintenance scheduling accuracy. Companies with integrated digital fleet ecosystems are securing stronger long-term contracts due to higher operational reliability and lower service interruption risk.

Between 2026 and 2028, modular microgrids integrating generators, battery storage, and smart distribution software are expected to accelerate adoption across hyperscale data centers, mining corridors, and utility modernization projects. Rapid-deployment containerized power systems improve installation efficiency by nearly 25% compared to traditional fixed temporary infrastructure. Global rental leaders, utility contractors, and industrial operators adopting scalable hybrid energy ecosystems will strengthen competitive positioning as infrastructure resilience and low-emission deployment capability become critical procurement priorities.

June 2024 – Cummins expanded its Centum™ Force containerized generator portfolio for global 50Hz markets, delivering up to 34% space-utilization savings for temporary and backup power deployments, strengthening rapid-installation capability across critical infrastructure sectors. Source: Cummins

December 2024 – Cummins India launched CPCBIV+ compliant gensets with telematics-enabled monitoring, reducing particulate matter and NOx emissions by up to 90% while improving uptime efficiency across infrastructure, mining, and industrial temporary power operations. Source: Cummins India

June 2025 – Aggreko introduced advanced natural gas generators including 1500 kW rapid-deploy models, expanding its lower-emission modular fleet portfolio and improving operational flexibility for industrial sites and remote temporary energy deployments.

April 2026 – Aggreko signed a 15-year agreement for Australia’s largest off-grid renewable hybrid power facility featuring 118 MWp solar capacity and 250 MWh battery storage, strengthening large-scale mining power resilience and hybrid deployment leadership. Source: International Mining

The report provides comprehensive analysis of temporary power deployment trends across diesel generators, gas generators, battery storage systems, load banks, and mobile power units, covering operational demand across construction sites, industrial operations, emergency backup, disaster recovery, utility support, and events applications. The study evaluates market positioning across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, while assessing deployment concentration, technology integration, infrastructure modernization, and enterprise procurement patterns. More than 40% of current deployment activity is concentrated within industrial and utility-linked applications requiring rapid-response mobile power capability.

The report also examines adoption of hybrid power systems, AI-enabled fleet monitoring, modular microgrids, and low-emission temporary energy solutions shaping competitive differentiation between 2026 and 2033. It delivers strategic insight into operational expansion priorities, fleet modernization, industrial partnerships, supply-chain optimization, and sector-specific demand evolution. Coverage includes both established industrial markets and emerging deployment environments linked to mining expansion, hyperscale digital infrastructure, renewable integration, and energy resilience modernization initiatives.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 8626.8 Million |

|

Market Revenue in 2033 |

USD 17443.38 Million |

|

CAGR (2026 - 2033) |

9.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Aggreko, Caterpillar, Cummins, Atlas Copco, APR Energy, United Rentals, Generac Power Systems, Kohler Energy, Wärtsilä, HIMOINSA, Speedy Hire, Ashtead Group, Herc Rentals, Byrne Equipment Rental |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |