Reports

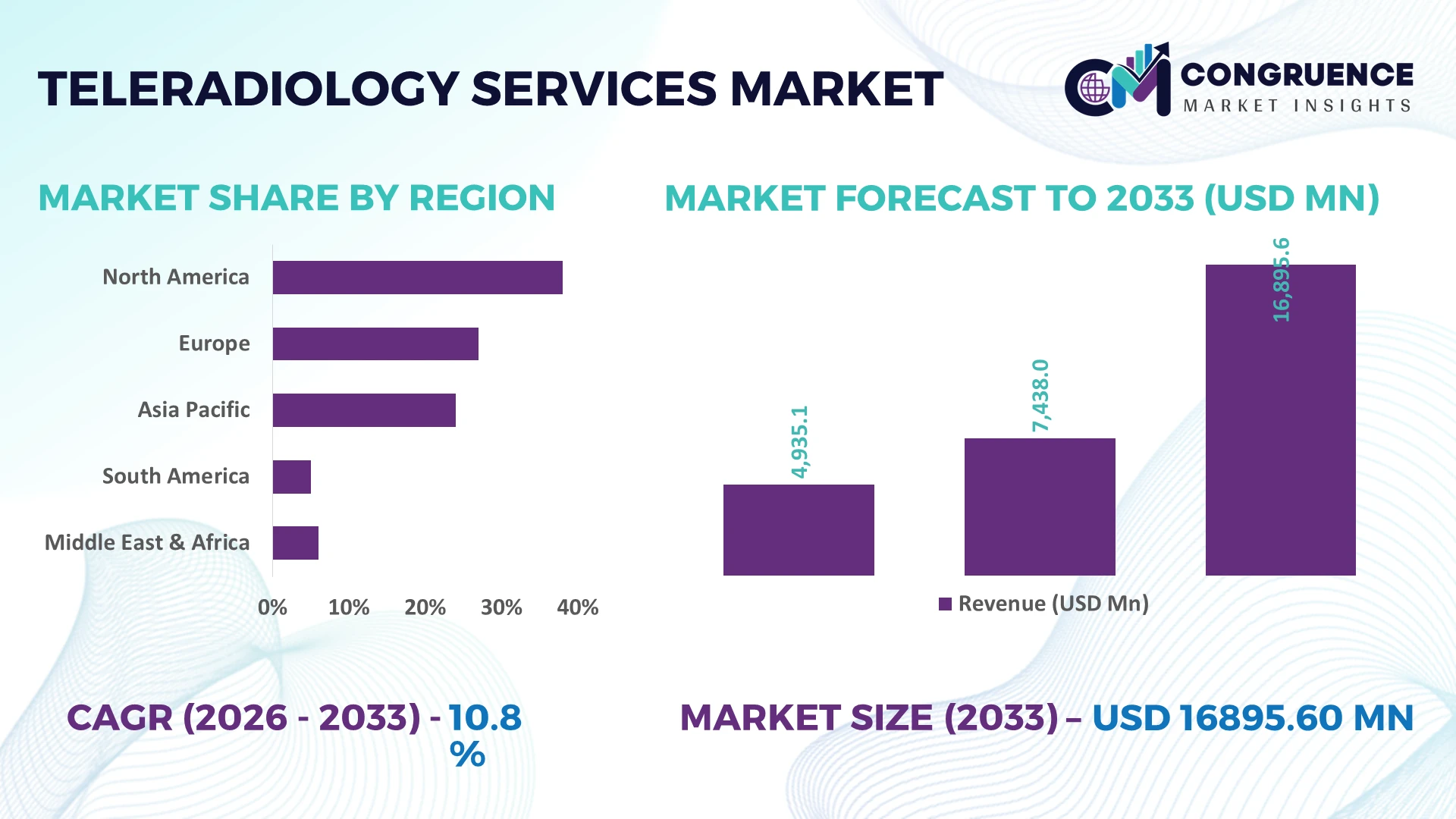

The Global Teleradiology Services Market was valued at USD 7437.99 Million in 2025 and is anticipated to reach a value of USD 16895.6 Million by 2033 expanding at a CAGR of 10.8% between 2026 and 2033. The market is expanding through rapid integration of AI-assisted image interpretation, cloud-based diagnostic platforms, and growing cross-border reporting networks that address radiologist shortages while improving emergency imaging turnaround times.

The United States dominates the global teleradiology services market with approximately 41% of advanced service deployment, supported by extensive hospital digitization, strong healthcare IT investments, and nationwide imaging networks. More than 84% of large hospital systems have adopted cloud-enabled PACS and remote reporting solutions, compared with nearly 66% in Japan. Continued healthcare cybersecurity investments and digital infrastructure modernization across allied economies in 2026 further strengthen the country's leadership in high-volume diagnostic imaging.

Healthcare providers and imaging service companies should prioritize AI-enabled reporting platforms, interoperable imaging ecosystems, and scalable international diagnostic networks to improve operational resilience and secure long-term enterprise contracts.

Market Size & Growth: USD 7437.99 Million (2025) to USD 16895.6 Million (2033) at 10.8% CAGR, driven by AI-powered diagnostic workflow automation.

Top Growth Drivers: AI-assisted reporting (+34%), cloud imaging adoption (72%+), and radiologist workforce shortages exceeding 24% globally.

Short-Term Forecast: By 2028, reporting turnaround time decreases by 36% while imaging workflow efficiency improves by approximately 31%.

Emerging Technologies: Generative AI, cloud-native PACS, intelligent workflow orchestration, and automated triage improve reporting accuracy by over 40%.

Regional Leaders: North America exceeds USD 6.9 Billion, Europe reaches USD 4.8 Billion, and Asia-Pacific approaches USD 3.8 Billion through expanding digital healthcare infrastructure.

Consumer & End-User Trends: Around 69% of multispecialty hospitals rely on 24/7 remote radiology services to enhance emergency diagnostic coverage.

Pilot/Case Example: A 2026 AI-enabled hospital imaging network reduced critical-case reporting time by 42%, significantly improving emergency care prioritization.

Competitive Landscape: The leading provider holds approximately 12% global share, while major competition comes from GE HealthCare, Everlight Radiology, Radiology Partners, Siemens Healthineers, and Philips.

Regulatory & ESG Impact: Digital health compliance programs and secure cloud adoption reduce imaging data management risks by nearly 28% while strengthening cross-border reporting standards.

Investment & Funding: More than USD 2.4 Billion in healthcare imaging and digital diagnostics investments support AI partnerships, cloud expansion, and enterprise imaging platforms.

Innovation & Future Outlook: Federated AI, predictive workflow analytics, and enterprise imaging interoperability are accelerating next-generation diagnostic service delivery across global healthcare networks.

The Teleradiology Services Market continues to gain momentum as healthcare providers expand remote diagnostic capabilities across emergency medicine, oncology, neurology, and musculoskeletal imaging. AI-assisted image prioritization and cloud-native reporting platforms now improve diagnostic workflow efficiency by approximately 30%, while stricter digital health regulations and secure cross-border data exchange frameworks established during 2026 are accelerating enterprise adoption. These developments set the foundation for the market's evolving strategic landscape.

Teleradiology services have become strategically important as healthcare providers seek continuous diagnostic coverage while addressing persistent radiologist shortages and rising imaging volumes. The market is shifting from outsourced reporting toward integrated enterprise imaging ecosystems that combine AI, cloud infrastructure, and secure data exchange. In 2026, stricter digital health compliance requirements and healthcare infrastructure modernization are accelerating investment in interoperable imaging platforms, strengthening competition among diagnostic service providers and technology vendors.

Compared with conventional on-site reporting, AI-assisted teleradiology workflows reduce image prioritization time by nearly 35% and improve reporting productivity by approximately 30%, enabling faster clinical decision-making without proportional workforce expansion. The United States leads large-scale deployment through mature enterprise hospital networks, while India has emerged as a global reporting hub due to its highly specialized radiology workforce and expanding digital healthcare infrastructure. Over the next two to three years, cloud-enabled reporting adoption is expected to exceed 75% among large healthcare organizations, supported by wider enterprise integration.

Healthcare companies are increasingly deploying unified imaging platforms that connect hospitals, diagnostic centers, and remote specialists within a single reporting environment. Strategic investments increasingly focus on AI partnerships, cybersecurity, and interoperable cloud architecture to improve operational resilience, strengthen diagnostic quality, and establish sustainable competitive differentiation across global healthcare networks.

The primary market driver is the rapid transition toward AI-supported enterprise imaging platforms that improve diagnostic speed, workforce utilization, and clinical consistency. More than 72% of large healthcare systems now prioritize cloud-based imaging infrastructure, while AI-assisted workflow automation improves radiologist productivity by approximately 34% and reduces reporting turnaround time by nearly 30%. The United States continues expanding digital hospital infrastructure through healthcare modernization initiatives, encouraging greater interoperability between imaging networks. In response, leading service providers are investing in AI integration, cloud-native PACS, and cross-border diagnostic partnerships to deliver continuous reporting capacity, improve service scalability, and secure long-term contracts with hospital networks seeking operational efficiency.

Fragmented healthcare IT environments and differing data governance requirements remain significant barriers to market expansion. Nearly 43% of healthcare organizations continue operating mixed legacy and modern imaging systems, while integration costs increase digital transformation budgets by approximately 18%. Cross-border diagnostic services also face varying patient privacy regulations that delay implementation timelines and complicate workflow standardization. Healthcare providers in Germany and other highly regulated markets often require extensive compliance validation before deployment. Companies are mitigating these constraints through standardized interoperability frameworks, localized data hosting, long-term technology partnerships, and cybersecurity investments that reduce implementation complexity while improving operational reliability across distributed imaging networks.

Significant opportunities are emerging through AI-driven clinical decision support, predictive workflow optimization, and integrated enterprise imaging ecosystems. More than 65% of healthcare executives are prioritizing AI-enabled diagnostic automation, while cloud imaging adoption is expected to surpass 78% among tertiary hospitals within the next few years. India is strengthening its position through expanding digital health infrastructure and specialized radiology expertise, creating opportunities for international reporting partnerships. Companies are accelerating R&D investments, forming strategic collaborations with healthcare technology providers, and developing scalable imaging platforms that reduce operational costs while supporting higher reporting volumes and improved clinical workflow efficiency.

Sustaining secure and standardized diagnostic operations across expanding global networks remains the industry's most complex execution challenge. Approximately 29% of healthcare organizations identify cybersecurity readiness as a major deployment obstacle, while imaging data volumes continue increasing by more than 20% annually, placing pressure on infrastructure scalability and storage management. Integrating AI applications with legacy hospital information systems also requires specialized technical expertise and continuous validation. Companies must strengthen cybersecurity architecture, expand cloud infrastructure, invest in workforce development, and establish standardized governance frameworks to ensure consistent diagnostic quality, regulatory compliance, and long-term competitiveness across increasingly interconnected healthcare ecosystems.

AI-Driven Workflow Optimization: AI-enabled triage and intelligent worklist prioritization are reshaping diagnostic operations, with reporting productivity improving by nearly 34% and critical-case turnaround time declining by approximately 38%. Following tighter digital health governance in 2026, healthcare providers are integrating AI directly into enterprise imaging workflows. Service providers are expanding automation partnerships and standardizing cloud-native reporting environments to improve consistency while reducing radiologist workload across multi-site hospital networks.

Cloud-Native Imaging Expansion: Cloud-based PACS deployment has exceeded 72% among large healthcare organizations, while enterprise image-sharing volumes have increased by over 28% during the past two years. Hospitals are replacing fragmented local infrastructure with centralized imaging platforms to improve scalability and disaster recovery capabilities. Technology vendors are accelerating hybrid-cloud deployment strategies and strengthening cybersecurity architecture to support uninterrupted diagnostic operations across distributed healthcare systems.

Cross-Border Reporting Networks: India continues expanding its role as a global reporting hub, supported by highly specialized radiology expertise and continuous 24/7 reporting models. International reporting capacity has increased by approximately 26%, while after-hours diagnostic coverage has improved by nearly 31% for participating healthcare organizations. Companies are strengthening international partnerships, regional reporting centers, and multilingual clinical support teams to improve operational flexibility while balancing workforce availability across different time zones.

Cybersecurity-Centric Platform Modernization: Secure imaging infrastructure has become a competitive differentiator as healthcare organizations respond to increasing cyber threats targeting medical data. More than 67% of enterprise imaging investments now prioritize zero-trust security architecture, while encrypted image-sharing adoption has increased by approximately 35%. Vendors are embedding identity management, continuous monitoring, and compliance automation into diagnostic platforms, reducing operational disruptions and strengthening customer confidence in large-scale teleradiology deployments.

CT Reporting remains the leading segment because of its extensive use in emergency medicine, trauma diagnosis, stroke assessment, oncology, and cardiovascular imaging. Approximately 37% of remote diagnostic reporting volumes are associated with CT examinations, supported by rapid image acquisition and standardized reporting workflows. Healthcare providers prioritize CT reporting because it integrates efficiently with AI-assisted triage systems, enabling faster emergency decision-making and improving resource utilization. X-ray Reporting continues serving high-volume routine diagnostics, while MRI Reporting maintains strong demand for neurological and musculoskeletal assessments where specialist interpretation remains essential.

PET-CT Reporting is the fastest-growing segment as precision oncology and advanced molecular imaging become increasingly integrated into cancer management pathways. PET-CT reporting volumes have increased by nearly 24% across specialized healthcare institutions, while MRI reporting adoption continues expanding by approximately 16% through advanced neuroimaging applications. Ultrasound Reporting remains strategically important for obstetrics, abdominal imaging, and point-of-care diagnostics. Companies are strengthening AI-assisted reporting capabilities, expanding subspecialty radiologist networks, and developing enterprise imaging partnerships to capture higher-value diagnostic workloads and improve reporting efficiency.

CT Reporting represents the largest application segment due to its critical role in emergency departments, trauma centers, oncology services, and acute neurological diagnosis. Nearly 39% of remote diagnostic workloads are generated through CT applications because clinicians require rapid interpretation for time-sensitive treatment decisions. AI-enabled prioritization further improves emergency reporting speed while supporting continuous diagnostic coverage. X-ray Reporting remains widely deployed for routine clinical examinations, whereas MRI Reporting continues expanding within advanced neurological and orthopedic imaging services.

PET-CT Reporting is emerging as the fastest-growing application owing to increasing utilization in precision oncology, treatment monitoring, and personalized medicine. Adoption of PET-CT reporting has expanded by approximately 22%, while Ultrasound Reporting utilization has increased by nearly 15% through telemedicine-supported maternal and rural healthcare programs. Healthcare providers are integrating automated workflow management, cloud imaging infrastructure, and enterprise reporting platforms to manage rising imaging volumes while maintaining consistent diagnostic quality across geographically distributed healthcare facilities.

Hospitals remain the dominant end-user segment because they operate the highest imaging volumes, require continuous specialist availability, and maintain complex multi-modality diagnostic infrastructure. Nearly 58% of enterprise teleradiology deployments are concentrated within hospital networks, where centralized imaging platforms improve workflow coordination and emergency reporting capacity. Diagnostic Centers continue expanding remote reporting utilization to manage increasing outpatient imaging demand, while Imaging Centers are adopting cloud-based reporting systems to improve operational flexibility and reduce turnaround times.

Telehealth Providers represent the fastest-growing end-user segment as virtual care integration expands beyond primary consultations into diagnostic services. Telehealth-enabled imaging referrals have increased by approximately 27%, while Specialty Clinics have expanded remote radiology utilization by nearly 18% for oncology, cardiology, and neurology services. Companies are developing customized enterprise platforms, subscription-based reporting models, and strategic healthcare partnerships to strengthen customer retention while supporting integrated digital care ecosystems across both urban and underserved healthcare markets.

North America accounted for the largest market share at 42.1% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.6% between 2026 and 2033.

Strategic Leadership Through Enterprise Imaging Integration

North America maintains the leading position through mature digital healthcare infrastructure, advanced enterprise imaging platforms, and extensive adoption of AI-assisted diagnostic workflows. The region contributes more than 42% of global deployment activity, supported by widespread cloud-based PACS implementation and large multi-hospital healthcare networks. More than 83% of tertiary hospitals utilize integrated remote radiology platforms for continuous emergency coverage and subspecialty reporting. Healthcare providers continue modernizing enterprise imaging environments through cybersecurity investments, interoperable health information exchanges, and long-term technology partnerships that improve reporting efficiency while supporting higher diagnostic volumes across geographically distributed healthcare facilities.

United States Market Outlook: The United States remains the regional leader because of its extensive hospital network, advanced imaging infrastructure, and high enterprise digitalization. More than 85% of large integrated healthcare systems have implemented cloud-enabled diagnostic imaging workflows, while AI-assisted prioritization continues improving emergency reporting performance. Healthcare organizations are strengthening strategic partnerships with enterprise software providers, expanding subspecialty reporting networks, and investing in secure cloud architecture to enhance nationwide diagnostic accessibility and operational resilience.

Regulatory Standardization Accelerates Digital Diagnostics

Europe continues strengthening its position through standardized digital healthcare policies, advanced interoperability frameworks, and increasing investment in secure diagnostic data exchange. The region accounts for nearly 29% of global deployment activity, supported by expanding enterprise imaging modernization across public healthcare systems. More than 69% of major hospital groups have integrated centralized image-sharing infrastructure to improve specialist collaboration and reporting consistency. Healthcare organizations are prioritizing secure cross-border reporting capabilities, AI validation programs, and interoperable diagnostic platforms that improve operational efficiency while maintaining compliance with stringent healthcare data governance requirements.

Germany Market Outlook: Germany leads the European market through advanced hospital infrastructure, strong healthcare digitization programs, and early deployment of enterprise imaging technologies. Approximately 71% of university hospitals utilize integrated digital radiology platforms supporting remote specialist collaboration. Technology providers continue expanding AI validation partnerships and cybersecurity investments, enabling healthcare institutions to improve workflow standardization while strengthening secure diagnostic reporting across nationwide healthcare networks.

Large-Scale Digital Healthcare Expansion

Asia-Pacific is experiencing the fastest operational expansion, driven by increasing healthcare digitalization, specialist workforce availability, and rapid deployment of enterprise imaging infrastructure. The region represents approximately 22% of global market activity while recording the highest rate of new platform implementation. Cloud-enabled diagnostic imaging adoption has surpassed 61% among leading metropolitan hospital networks, supported by national digital health initiatives and expanding telemedicine ecosystems. Service providers are increasing regional reporting capacity, establishing specialized diagnostic hubs, and investing in AI-enabled workflow automation to address rising imaging demand and improve healthcare accessibility across densely populated markets.

India Market Outlook: India has become a strategic global teleradiology hub because of its highly specialized radiology workforce, strong IT ecosystem, and cost-efficient reporting capabilities. More than 1,500 diagnostic facilities actively support remote imaging services for domestic and international healthcare providers. Companies continue expanding enterprise reporting centers, AI-assisted workflow deployment, and international hospital partnerships to strengthen service quality while supporting round-the-clock diagnostic operations across multiple time zones.

Healthcare Connectivity Expands Remote Diagnostics

South America is steadily increasing adoption of remote diagnostic services through healthcare infrastructure upgrades, expanding broadband connectivity, and growing investment in digital imaging platforms. The region contributes approximately 5% of global deployment, with remote reporting utilization increasing by nearly 19% across large healthcare organizations. Public and private healthcare providers are implementing centralized imaging networks to improve specialist access in underserved locations. Technology vendors are responding through regional partnerships, localized cloud deployment, and integrated reporting solutions that improve operational efficiency despite continuing infrastructure disparities between urban and rural healthcare systems.

Brazil Market Outlook: Brazil leads regional deployment through its large hospital network, expanding digital healthcare initiatives, and increasing enterprise imaging investment. Nearly 63% of major private hospital groups have adopted centralized remote radiology workflows supporting emergency and specialty imaging services. Companies continue strengthening regional reporting hubs, cloud infrastructure, and healthcare technology collaborations to improve diagnostic consistency while expanding access across geographically dispersed patient populations.

Digital Health Investment Reshapes Diagnostic Infrastructure

The Middle East & Africa market is advancing through sustained healthcare modernization, smart hospital development, and government-backed digital transformation initiatives. The region contributes approximately 4% of global deployment while recording consistent expansion in enterprise imaging implementation. More than 54% of newly commissioned tertiary hospitals are integrating cloud-based imaging systems into their digital health infrastructure. Healthcare organizations are increasing investment in secure diagnostic platforms, AI-enabled reporting workflows, and regional specialist collaboration to improve service accessibility while addressing shortages of experienced radiologists across rapidly developing healthcare systems.

Saudi Arabia Market Outlook: Saudi Arabia remains the region's most strategically significant market, supported by large-scale healthcare modernization programs, advanced hospital construction, and strong digital transformation initiatives. Over 60% of major government healthcare facilities are implementing enterprise imaging modernization projects integrated with national digital health strategies. Companies are expanding partnerships with healthcare technology providers, deploying secure cloud-based diagnostic platforms, and strengthening AI-assisted reporting capabilities to improve nationwide diagnostic efficiency and specialist accessibility.

The competitive landscape is defined by global imaging technology leaders including GE HealthCare, Siemens Healthineers, Philips, and specialized teleradiology providers such as Radiology Partners and Everlight Radiology competing against regional diagnostic service networks and AI imaging platform developers. The top five participants collectively account for approximately 46% of the global market, creating moderate consolidation while leaving opportunities for specialized providers. Competition centers on AI-enabled reporting accuracy, turnaround speed, enterprise interoperability, and cybersecurity rather than pricing alone. AI-assisted workflow automation improves reporting productivity by nearly 34%, cloud-native deployment reduces infrastructure costs by approximately 25%, and automated case prioritization shortens critical reporting time by around 38%. Companies are expanding through hospital partnerships, enterprise imaging integration, international reporting centers, and proprietary AI development. Competition is shifting toward platform ecosystems combining cloud infrastructure, workflow orchestration, and diagnostic intelligence. Regulatory compliance, cybersecurity investment, and enterprise-scale interoperability remain significant entry barriers. Sustained leadership depends on delivering scalable, secure, AI-integrated diagnostic networks with consistently superior clinical performance.

Everlight Radiology

Radiology Partners

Virtual Radiologic (vRad)

TeleDiagnosys

ONRAD Inc.

Medica Group

USARAD Holdings Inc.

Teleradiology Solutions

Agfa HealthCare

GE HealthCare

Siemens Healthineers

Philips

Fujifilm Healthcare

Artificial intelligence has become the core technology transforming modern teleradiology services by automating image prioritization, anomaly detection, and workflow orchestration. AI-assisted reporting improves radiologist productivity by approximately 34% while reducing emergency case turnaround time by nearly 38%. More than 70% of enterprise healthcare organizations are deploying AI-enabled imaging workflows alongside cloud-native PACS platforms. Compared with conventional manual reporting processes, integrated AI workflows improve diagnostic efficiency by around 30%, allowing providers to manage increasing imaging volumes without proportionally expanding specialist workforces.

Cloud-native enterprise imaging, zero-trust cybersecurity architecture, and interoperable health information exchanges are accelerating operational transformation. Secure cloud deployment lowers infrastructure management costs by nearly 25% while improving system availability across distributed hospital networks. Edge computing and intelligent workload balancing further optimize image routing between reporting centers. Large hospital systems and multinational diagnostic providers benefit most because these technologies strengthen scalability, improve disaster recovery, and support continuous cross-border diagnostic operations without disrupting clinical workflows.

Between 2026 and 2028, generative AI, multimodal clinical decision support, and predictive workflow analytics will redefine enterprise imaging ecosystems. Adoption of intelligent workflow orchestration is expected to exceed 75% among leading healthcare organizations, enabling proactive resource allocation and standardized reporting quality. Companies investing early in interoperable AI platforms, automated quality assurance, and cybersecurity-integrated imaging infrastructure will strengthen competitive differentiation, improve operational resilience, and secure long-term enterprise healthcare partnerships.

November 2024 – Everlight Radiology partnered with DataFirst to integrate the Silverback® imaging orchestration platform into its global reporting network, supporting more than 200 GMC specialist consultant radiologists and improving enterprise workflow coordination across multiple continents. This strengthened large-scale operational efficiency and service scalability.

November 2025 – GE HealthCare announced the acquisition of Intelerad for USD 2.3 billion, expanding its cloud-first enterprise imaging portfolio across hospital, outpatient, and teleradiology environments. The transaction significantly enhanced AI-enabled imaging capabilities and strengthened end-to-end diagnostic workflow integration.

May 2026 – Everlight Radiology entered a five-year strategic partnership with Sirona Medical to deploy the RadOS cloud-native workflow platform across 350 hospitals supporting 19 million patients annually through 800 radiologists. The deployment accelerates AI-enabled reporting and enterprise imaging modernization worldwide.

June 2026 – GE HealthCare introduced expanded enterprise imaging solutions including Genesis Radiology Workspace and InteleShare, targeting cloud-enabled diagnostic workflows. The initiative addresses the radiologist workforce shortage identified by the American College of Radiology while improving productivity and remote imaging collaboration across healthcare systems.

The report provides comprehensive coverage of the global Teleradiology Services Market across X-ray Reporting, CT Reporting, MRI Reporting, Ultrasound Reporting, and PET-CT Reporting, together with detailed analysis by application and end-user categories including hospitals, diagnostic centers, imaging centers, specialty clinics, and telehealth providers. It evaluates market performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while assessing adoption trends, deployment models, enterprise strategies, and competitive positioning. More than 70% of enterprise healthcare organizations are accelerating cloud-enabled imaging deployment, making technology integration a central focus of market evaluation.

The study further examines AI-assisted diagnostics, cloud-native PACS, enterprise imaging platforms, interoperability, cybersecurity, workflow automation, and emerging digital imaging ecosystems. It delivers strategic intelligence on company positioning, technology adoption, partnership activity, investment priorities, and operational benchmarking, enabling stakeholders to support expansion planning, portfolio optimization, competitive differentiation, and long-term business strategy between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 7437.99 Million |

Market Revenue in 2033 | USD 16895.6 Million |

CAGR (2026 - 2033) | 10.8% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Everlight Radiology, Radiology Partners, Virtual Radiologic (vRad), TeleDiagnosys, ONRAD Inc., Medica Group, USARAD Holdings Inc., Teleradiology Solutions, Agfa HealthCare, GE HealthCare, Siemens Healthineers, Philips, Fujifilm Healthcare |

Customization & Pricing | Available on Request (10% Customization is Free) |