Reports

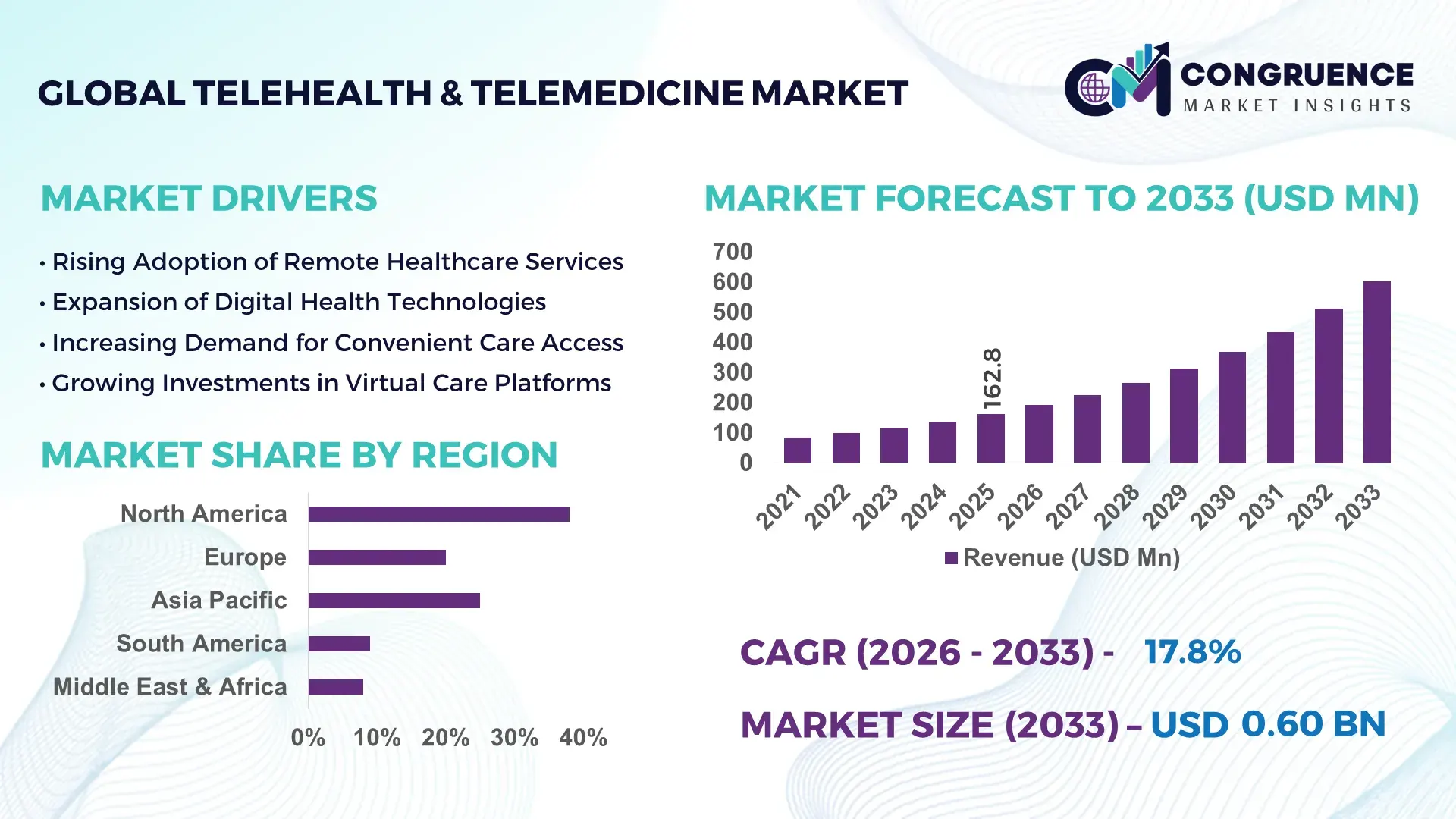

The Global Telehealth & Telemedicine Market was valued at USD 162.77 Million in 2025 and is anticipated to reach a value of USD 603.6 Million by 2033 expanding at a CAGR of 17.8% between 2026 and 2033. This accelerated expansion is primarily driven by rapid digital healthcare adoption, rising chronic disease prevalence, and scalable remote patient monitoring infrastructure across developed and emerging economies.

In the United States, telehealth infrastructure investment has surpassed USD 15 billion annually across hospital systems, payer networks, and digital health platforms. More than 80% of large healthcare providers have integrated virtual care platforms with electronic health records, while remote patient monitoring programs cover over 30 million patients nationwide. Medicare-supported teleconsultations exceeded 50 million visits annually in recent years, reflecting large-scale consumer adoption. Advanced AI-enabled triage systems, cloud-based telemedicine platforms, and secure interoperable health data exchanges are widely deployed across primary care, behavioral health, cardiology, and post-acute care services, supported by over 6,000 telehealth-enabled hospital facilities nationwide.

Market Size & Growth: USD 162.77 Million (2025) projected to reach USD 603.6 Million by 2033 at a CAGR of 17.8%, driven by digital transformation in healthcare delivery and scalable virtual care models.

Top Growth Drivers: 65% digital consultation adoption rate, 40% reduction in outpatient operational costs, 55% improvement in chronic disease monitoring compliance.

Short-Term Forecast: By 2028, virtual care platforms are expected to reduce hospital readmissions by 25% and improve appointment efficiency by 30%.

Emerging Technologies: AI-driven diagnostic support tools, IoT-enabled remote patient monitoring devices, and blockchain-based secure health data exchange platforms.

Regional Leaders: North America projected at USD 240 Million by 2033 with high insurance-backed virtual visits; Europe at USD 170 Million supported by public eHealth integration; Asia-Pacific at USD 140 Million driven by mobile-first teleconsultation growth.

Consumer/End-User Trends: Increasing adoption among elderly patients, behavioral health users, and rural populations, with over 60% preferring hybrid care models combining virtual and in-person services.

Pilot or Case Example: In 2024, a multi-hospital tele-ICU program demonstrated a 22% reduction in patient mortality and 18% decrease in ICU length of stay through centralized remote monitoring.

Competitive Landscape: Teladoc Health holds approximately 18% share, followed by Amwell, MDLIVE, Doctor on Demand, and Siemens Healthineers in integrated digital health solutions.

Regulatory & ESG Impact: Expansion of reimbursement parity laws, cross-state licensure compacts, and data privacy frameworks accelerating compliant telemedicine adoption.

Investment & Funding Patterns: Over USD 12 billion invested globally in digital health and telemedicine platforms in recent funding cycles, with strong venture capital and strategic hospital partnerships.

Innovation & Future Outlook: Integration of predictive analytics, AI-assisted triage automation, and wearable biosensor ecosystems shaping next-generation connected healthcare delivery.

The telehealth & telemedicine market spans primary care consultations, mental health services, chronic disease management, tele-ICU monitoring, and post-operative follow-ups, with primary care contributing approximately 35% of total service utilization and behavioral health accounting for nearly 25%. Rapid innovation in AI-enabled diagnostics, high-resolution remote imaging, and 5G-supported virtual consultations is enhancing clinical outcomes and reducing treatment delays. Regulatory support through reimbursement expansion, digital health compliance frameworks, and cross-border telemedicine agreements continues to strengthen market confidence. Regional consumption patterns indicate higher per-capita usage in North America and accelerating mobile-based adoption across Asia-Pacific. Future growth is expected to be fueled by value-based care integration, advanced analytics-driven patient engagement platforms, and expanded remote therapeutic monitoring programs targeting chronic cardiovascular and metabolic conditions.

The Telehealth & Telemedicine Market has evolved into a strategically critical pillar within modern healthcare ecosystems, enabling cost-efficient, scalable, and patient-centric service delivery. Healthcare providers are embedding virtual care models into enterprise-level digital transformation strategies, targeting measurable improvements in care accessibility and operational efficiency. AI-powered teleconsultation platforms deliver 35% faster triage response compared to traditional in-person scheduling systems, while remote patient monitoring reduces emergency admissions by nearly 25% compared to conventional episodic care models.

North America dominates in service volume due to extensive hospital network integration, while Asia-Pacific leads in adoption with over 60% of urban healthcare users accessing mobile-based teleconsultation services. Strategic investments are focused on interoperable health data systems, cloud-based electronic health records integration, and predictive analytics that enhance diagnostic precision. By 2028, AI-enabled remote monitoring is expected to reduce hospital readmission rates by 28% and improve chronic care compliance by 32%.

Compliance and ESG considerations are increasingly embedded into telemedicine strategies. Firms are committing to digital carbon footprint reductions such as 40% lower patient travel emissions by 2030 through expanded virtual visit adoption. In 2024, a nationwide telehealth initiative in the United Kingdom achieved a 20% reduction in outpatient backlog through centralized virtual triage systems. As digital therapeutics, wearable biosensors, and secure data-sharing frameworks mature, the Telehealth & Telemedicine Market is positioned as a resilient, compliance-driven, and sustainable healthcare delivery infrastructure supporting long-term system stability and equitable access.

The increasing burden of chronic diseases is significantly strengthening demand for advanced telehealth and telemedicine solutions. Globally, chronic conditions account for nearly 70% of total deaths, requiring long-term monitoring and continuous patient engagement. Remote patient monitoring devices improve medication adherence by approximately 30% and reduce avoidable hospital visits by nearly 20%. Digital care coordination platforms enable physicians to track real-time patient vitals, improving intervention speed by 25% compared to traditional periodic consultations. Additionally, aging populations are driving virtual care demand, with individuals aged 60 and above representing more than 35% of teleconsultation users in developed healthcare systems. Employers and insurers are increasingly integrating telemedicine into preventive health programs, resulting in measurable productivity gains and reduced absenteeism. These factors collectively reinforce telehealth as a scalable, cost-efficient solution for chronic disease management and long-term patient outcomes optimization.

Cybersecurity vulnerabilities and stringent data protection regulations present notable limitations for telehealth and telemedicine platform expansion. Healthcare data breaches have increased by over 40% in recent years, exposing millions of patient records and raising compliance risks for providers. Advanced encryption, secure cloud hosting, and multi-factor authentication increase implementation costs by up to 18% compared to conventional IT systems. Regulatory frameworks such as cross-border data localization laws create operational complexity for multinational telemedicine providers. Smaller healthcare facilities often lack robust cybersecurity infrastructure, slowing adoption of fully integrated virtual care ecosystems. Additionally, patient concerns regarding digital privacy reduce trust in remote consultation platforms, particularly in emerging markets where regulatory clarity is evolving. These constraints require sustained investment in secure architecture, compliance auditing, and digital risk mitigation frameworks to maintain scalable growth.

AI-driven remote patient monitoring presents transformative growth opportunities within the telehealth and telemedicine ecosystem. Predictive analytics platforms improve early disease detection accuracy by nearly 27% compared to traditional symptom-based assessments. Wearable biosensors capable of continuous cardiovascular and glucose monitoring expand remote care coverage for millions of high-risk patients. Digital therapeutics integrated into telemedicine platforms enhance treatment adherence by 35% through automated alerts and personalized feedback. Emerging 5G connectivity infrastructure supports high-definition virtual diagnostics, reducing latency by over 50% compared to legacy networks. Rural healthcare access programs leveraging mobile-first teleconsultation models are expanding patient outreach by approximately 30% in underserved regions. Strategic partnerships between hospitals, technology firms, and insurers are accelerating AI-based innovation, positioning telehealth platforms as proactive, data-driven care management systems capable of delivering measurable clinical and operational improvements.

Regulatory fragmentation across jurisdictions remains a critical obstacle for telehealth and telemedicine providers. Licensing requirements vary by region, limiting cross-border physician consultations and creating administrative inefficiencies. Reimbursement policies differ significantly among public and private payers, with some regions reimbursing virtual visits at rates 15–25% lower than in-person consultations. These inconsistencies reduce provider incentives to fully transition to digital care models. Additionally, telemedicine hardware procurement, including remote diagnostic equipment and secure communication systems, can increase capital expenditure by nearly 20% compared to conventional clinic setups. Infrastructure disparities, particularly in low-bandwidth rural areas, restrict high-quality video consultation reliability. Overcoming these structural and policy-related challenges requires harmonized regulatory frameworks, reimbursement standardization, and targeted digital infrastructure investments to ensure equitable and scalable telehealth deployment across global healthcare systems.

• AI-Integrated Virtual Care Platforms Achieving 30% Faster Clinical Decision-Making: Healthcare systems are rapidly deploying AI-enabled telehealth platforms that reduce patient triage time by nearly 30% compared to traditional appointment workflows. Automated symptom checkers now manage over 40% of initial patient queries in digital-first hospitals. Clinical documentation powered by generative AI tools has lowered physician administrative workload by approximately 25%, improving patient throughput efficiency. More than 65% of large healthcare networks have integrated predictive analytics into remote monitoring programs, enhancing early risk detection for chronic disease patients and reducing avoidable escalations by 20%.

• Remote Patient Monitoring Devices Expanding Chronic Care Coverage by 35%: Wearable biosensors and connected health devices are significantly strengthening telemedicine ecosystems. Over 50 million patients globally are enrolled in remote patient monitoring programs, with cardiac and diabetes management representing nearly 45% of total device deployments. Continuous glucose monitoring systems have improved treatment adherence by 33%, while connected blood pressure monitoring has reduced uncontrolled hypertension cases by 18% in managed populations. Hospitals implementing tele-ICU systems report a 22% reduction in critical event response times, highlighting measurable improvements in high-acuity virtual care models.

• Hybrid Care Models Increasing Patient Retention by 28%: Healthcare providers are adopting integrated hybrid models combining in-person visits with digital follow-ups, resulting in 28% higher patient retention rates compared to standalone physical care models. Approximately 60% of urban healthcare consumers now prefer virtual consultations for non-emergency services. Behavioral health teleconsultations account for nearly 25% of all virtual visits, reflecting growing acceptance of remote therapy services. Digital appointment scheduling platforms have reduced no-show rates by 19%, improving operational resource allocation and clinical efficiency across outpatient networks.

• Expansion of Cross-Border Telemedicine and Digital Health Compliance Frameworks: Regulatory modernization is enabling scalable telehealth expansion across multiple jurisdictions. Over 70% of developed healthcare systems have introduced reimbursement parity measures for virtual consultations. Cross-state or cross-region licensure compacts now cover more than 35% of practicing physicians in certain developed markets, enabling broader service delivery. Secure cloud-based telemedicine platforms with end-to-end encryption have achieved 99.9% uptime reliability, supporting high-volume consultation demand. ESG-aligned digital health programs are contributing to an estimated 40% reduction in patient travel-related carbon emissions through expanded virtual care adoption.

The Telehealth & Telemedicine Market is segmented by type, application, and end-user, reflecting the diversified structure of digital healthcare delivery. By type, the market includes services, software platforms, and hardware devices such as remote patient monitoring tools and connected diagnostic equipment. Services dominate utilization due to increasing virtual consultations across primary and specialty care. By application, teleconsultation, remote patient monitoring, tele-ICU, mental health, and chronic disease management represent the core segments, with teleconsultation accounting for the largest proportion of virtual interactions globally. From an end-user perspective, hospitals, ambulatory care centers, homecare settings, and corporate healthcare programs drive demand. Hospitals maintain the largest deployment scale due to integrated IT systems, while homecare settings are expanding rapidly as wearable and AI-enabled monitoring devices gain patient acceptance. Segmentation trends indicate a strategic shift toward platform-based ecosystems combining clinical software, connected devices, and value-based care services.

The Telehealth & Telemedicine Market by type is categorized into services, software, and hardware solutions. Services currently account for approximately 48% of total adoption, driven by high-volume teleconsultations, tele-ICU management, and virtual behavioral health sessions. Software platforms hold nearly 32%, supported by AI-enabled diagnostics, secure video interfaces, and cloud-based electronic health record integration. Hardware, including remote patient monitoring devices, connected stethoscopes, and wearable biosensors, contributes about 20% of the overall market. While services lead in adoption, hardware solutions represent the fastest-growing segment, expanding at an estimated CAGR of 19% due to rising chronic disease prevalence and demand for continuous home-based monitoring. Wearable cardiac monitoring devices have improved early arrhythmia detection rates by 27%, reinforcing hardware investment. Software platforms are also expanding through predictive analytics and automation capabilities that reduce clinical documentation time by 25%.

By application, teleconsultation remains the leading segment, accounting for nearly 40% of overall telehealth utilization due to its scalability and integration with outpatient services. Remote patient monitoring represents around 28%, while mental health services contribute approximately 18%. Tele-ICU and post-acute care applications collectively hold close to 14% of total usage. Teleconsultation leads primarily because over 60% of non-emergency primary care visits in digitally advanced healthcare systems now incorporate virtual components. Remote patient monitoring is the fastest-growing application, expanding at an estimated CAGR of 20%, supported by the increasing prevalence of cardiovascular diseases and diabetes affecting more than 30% of adult populations globally. Continuous monitoring solutions reduce hospital readmissions by nearly 25%, strengthening provider adoption. Mental health teletherapy is also expanding, with virtual behavioral sessions improving appointment adherence by 35%.

Hospitals represent the leading end-user segment in the Telehealth & Telemedicine Market, accounting for approximately 45% of total deployments due to advanced IT infrastructure and integrated electronic health record systems. Ambulatory care centers contribute nearly 25%, while homecare settings represent around 20%. Corporate healthcare programs and employer-sponsored digital clinics collectively account for approximately 10% of the remaining usage. Although hospitals dominate deployment scale, homecare settings are the fastest-growing end-user segment, expanding at an estimated CAGR of 21%, fueled by increasing demand for remote chronic disease management and elderly care solutions. More than 55% of patients enrolled in remote monitoring programs now receive care primarily within home environments. Ambulatory centers report a 22% improvement in scheduling efficiency through teleconsultation integration, while employer-sponsored telehealth programs have reduced workplace absenteeism by 18%.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 20% between 2026 and 2033.

North America processed more than 120 million virtual consultations annually, supported by over 6,000 telehealth-enabled hospital facilities and 75% electronic health record interoperability across major health systems. Europe represented approximately 27% of total market activity, with over 50% of outpatient follow-ups in digitally advanced countries incorporating virtual elements. Asia-Pacific held nearly 23% share, driven by mobile-first healthcare platforms serving more than 200 million users across China and India combined. South America accounted for about 7%, with Brazil contributing nearly 45% of regional teleconsultations. The Middle East & Africa represented close to 5%, with the UAE and South Africa leading digital hospital integration initiatives exceeding 60% platform adoption in private healthcare networks.

How Are Advanced Reimbursement Models Accelerating Virtual Care Integration?

The North America Telehealth & Telemedicine Market holds approximately 38% of global share, supported by large-scale hospital digitization and insurance-backed virtual care models. The healthcare and employer-sponsored wellness sectors are primary demand drivers, with over 70% of large enterprises offering telehealth benefits. Regulatory enhancements, including reimbursement parity policies and cross-state licensure compacts covering nearly 35 states, have improved physician participation rates by 22%. Technological advancements such as AI-powered triage tools and remote patient monitoring devices have reduced hospital readmissions by nearly 25% in chronic care programs. Teladoc Health has expanded integrated mental health and chronic care solutions, managing millions of annual digital consultations. Consumer behavior reflects strong hybrid-care preference, with over 60% of patients opting for virtual visits for non-emergency services and higher enterprise-level adoption across healthcare and insurance industries.

How Is Digital Health Regulation Driving Secure and Scalable Virtual Care Systems?

The Europe Telehealth & Telemedicine Market accounts for nearly 27% of global adoption, with Germany, the United Kingdom, and France representing over 65% of regional activity. Regulatory oversight from health data compliance frameworks and digital health certification systems has increased platform standardization by approximately 30%. More than 50% of general practitioners in digitally advanced European countries now offer video consultations. Sustainability initiatives aligned with carbon neutrality goals have encouraged a 35% reduction in patient travel through teleconsultation substitution. Babylon Health expanded AI-driven primary care services within the United Kingdom, enhancing appointment efficiency by nearly 20%. Regional consumer behavior emphasizes privacy and explainable AI systems, with over 58% of users prioritizing data security assurances before engaging in telemedicine services.

What Is Fueling the Surge in Mobile-First Digital Healthcare Ecosystems?

The Asia-Pacific Telehealth & Telemedicine Market ranks second globally in volume, accounting for approximately 23% of total utilization, with China, India, and Japan as top consuming countries. China alone facilitates over 100 million annual online medical consultations through integrated digital hospital platforms. India’s telemedicine guidelines have enabled more than 150,000 registered practitioners to offer remote services nationwide. Infrastructure investments in 5G networks have reduced video latency by 50%, improving high-definition teleconsultation reliability. Ping An Good Doctor continues expanding AI-powered medical consultation services to millions of active users. Consumer behavior is mobile-centric, with over 65% of telehealth interactions conducted via smartphone applications, reflecting strong digital engagement across urban and semi-urban populations.

How Are Public Health Reforms Expanding Remote Care Accessibility?

The South America Telehealth & Telemedicine Market represents approximately 7% of global share, with Brazil and Argentina leading regional adoption. Brazil contributes nearly 45% of total regional teleconsultations, supported by digital public health reforms and expanded broadband coverage reaching over 80% of urban households. Government-backed telehealth frameworks have improved rural consultation access by 30%. Private healthcare providers are integrating cloud-based consultation platforms, enhancing appointment scheduling efficiency by 18%. Conexa Saúde has expanded remote specialty care services across multiple states, increasing physician network coverage by more than 25%. Consumer demand is influenced by language localization and affordability, with over 55% of virtual consultations conducted via mobile platforms in metropolitan areas.

How Is Healthcare Modernization Strengthening Digital Care Infrastructure?

The Middle East & Africa Telehealth & Telemedicine Market accounts for close to 5% of global activity, with the UAE and South Africa emerging as primary growth hubs. The UAE reports more than 60% telemedicine integration across private hospital networks, supported by national digital health transformation programs. South Africa has expanded rural teleconsultation programs by nearly 28%, improving specialist access in underserved regions. Investments in smart hospital infrastructure and secure cloud platforms have increased system uptime reliability to above 99%. Okadoc in the UAE has enhanced online appointment bookings, serving hundreds of thousands of users annually. Consumer behavior indicates rising demand for specialist virtual consultations, particularly in cardiology and dermatology, reflecting growing digital trust and healthcare accessibility needs.

United States – 34% market share: The Telehealth & Telemedicine Market in the United States leads due to advanced hospital digitization, reimbursement parity laws, and over 80% electronic health record interoperability across major healthcare systems.

China – 18% market share: The Telehealth & Telemedicine Market in China is driven by large-scale mobile health platforms facilitating over 100 million annual online consultations and strong government-backed digital healthcare infrastructure expansion.

The Telehealth & Telemedicine Market demonstrates a moderately fragmented competitive structure, with more than 250 active digital health and virtual care providers operating globally. The top five companies collectively account for approximately 45% of total market presence, indicating strong competition alongside emerging regional and niche innovators. Leading firms focus on integrated care ecosystems combining virtual consultations, remote patient monitoring, AI-driven diagnostics, and electronic health record interoperability.

Strategic initiatives are intensifying, with over 60% of top-tier players engaging in partnerships with hospital networks and insurance providers to strengthen reimbursement-backed service models. In recent years, more than 40 strategic mergers and acquisitions have been executed to expand service portfolios, enhance geographic coverage, and integrate AI-based analytics capabilities. Product innovation remains central, with nearly 70% of leading vendors launching upgraded teleconsultation platforms featuring predictive triage automation and real-time clinical documentation tools.

Competitive differentiation increasingly revolves around platform scalability, cybersecurity compliance, and patient engagement metrics. Approximately 55% of enterprise contracts now require end-to-end encryption and multi-factor authentication standards. Vendors investing in wearable integration and IoT-enabled monitoring report 20–30% higher client retention rates. The competitive landscape is also shaped by hybrid-care positioning strategies, as over 65% of leading companies offer bundled digital and in-person coordination services to healthcare providers and corporate clients.

Teladoc Health

Amwell

MDLIVE

Doctor On Demand

Siemens Healthineers

Philips Healthcare

Cerner Corporation

Ping An Good Doctor

Babylon Health

Conexa Saúde

Okadoc

American Well

The Telehealth & Telemedicine Market is undergoing rapid technological transformation driven by artificial intelligence, cloud computing, advanced connectivity, and secure health data interoperability frameworks. AI-powered clinical decision support systems are now embedded in over 60% of enterprise-grade telehealth platforms, reducing diagnostic turnaround time by approximately 30% and improving early disease detection accuracy by nearly 25%. Automated medical transcription and natural language processing tools have lowered physician documentation workloads by 20–35%, directly enhancing consultation capacity and operational efficiency.

Remote patient monitoring technology remains a core innovation pillar, with more than 50 million connected devices actively transmitting real-time health data, including cardiac rhythms, blood glucose levels, oxygen saturation, and blood pressure metrics. Wearable ECG patches have improved arrhythmia detection rates by 27%, while continuous glucose monitoring systems have increased therapy adherence by 33% among diabetic patients. Integration of IoT-enabled biosensors with centralized dashboards allows healthcare providers to track high-risk patient cohorts, reducing hospital readmission rates by nearly 25%.

Cloud-based telemedicine architectures now support 99.9% system uptime, enabling scalable deployment across multi-hospital networks. Over 70% of large healthcare providers utilize interoperable electronic health record integration, facilitating seamless exchange of patient data between virtual and in-person care environments. The expansion of 5G networks has reduced video latency by more than 50%, improving high-definition teleconsultation quality and enabling real-time remote diagnostics, including dermatology and radiology assessments.

Cybersecurity technologies, including end-to-end encryption, blockchain-secured data exchange, and multi-factor authentication, are increasingly standard, with 55% of enterprise buyers mandating advanced compliance certifications. Additionally, predictive analytics platforms leverage machine learning algorithms to identify at-risk patients up to 20% earlier than conventional screening protocols. As digital therapeutics, virtual reality rehabilitation modules, and AI-enabled triage chatbots continue evolving, technology remains central to building scalable, secure, and patient-centric telehealth ecosystems capable of meeting rising global healthcare demands.

• In January 2024, Teladoc Health expanded its chronic care management program by integrating AI-enabled predictive analytics into its Primary360 platform, enhancing early intervention capabilities and improving care coordination across cardiovascular and diabetes populations. The upgrade strengthened virtual-first primary care delivery across large employer groups. Source: www.teladochealth.com

• In March 2024, Amwell announced the integration of generative AI capabilities within its Converge platform to automate clinical documentation and improve provider workflow efficiency, reducing administrative burden and enabling faster virtual consultations across health system partners. Source: www.amwell.com

• In February 2025, Siemens Healthineers enhanced its digital health portfolio by advancing remote imaging collaboration tools, enabling radiologists to conduct secure, real-time virtual consultations and image reviews across distributed hospital networks, supporting improved diagnostic turnaround times. Source: www.siemens-healthineers.com

• In April 2025, Philips expanded its remote patient monitoring solutions by integrating advanced wearable biosensor analytics into its connected care ecosystem, strengthening home-based cardiac monitoring programs and improving continuous data transmission accuracy for high-risk patient groups. Source: www.philips.com

The Telehealth & Telemedicine Market Report provides a comprehensive evaluation of digital healthcare delivery models across services, software platforms, and connected medical devices. The scope covers key segments including teleconsultation, remote patient monitoring, tele-ICU, behavioral health, chronic disease management, and post-acute follow-up care. Service-based solutions represent nearly half of total deployment activity, while remote monitoring devices account for over 20% of structured virtual care programs globally. Geographically, the report analyzes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing regional variations in digital infrastructure, regulatory compliance, and consumer adoption patterns. North America leads in enterprise-level hospital integration exceeding 70% digital interoperability, while Asia-Pacific demonstrates strong mobile-first engagement with over 60% of consultations conducted via smartphone platforms.

Technological coverage includes AI-driven clinical decision support systems, IoT-enabled wearable biosensors, cloud-based electronic health record integration, cybersecurity frameworks, blockchain-secured data exchange, and 5G-enabled teleconsultation networks. More than 50 million connected monitoring devices globally contribute to continuous patient data flows, shaping predictive care strategies. The report further evaluates end-user adoption across hospitals, ambulatory centers, homecare settings, and corporate healthcare programs, where hospitals account for approximately 45% of structured deployments. It also addresses regulatory frameworks, reimbursement models, ESG-driven digital healthcare initiatives, and hybrid care integration strategies. Emerging niche areas such as digital therapeutics, virtual rehabilitation modules, and AI-assisted triage automation are included to provide forward-looking insights for healthcare executives, investors, and policy stakeholders assessing scalable, secure, and technology-enabled care delivery ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

17.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Teladoc Health , Amwell, MDLIVE, Doctor On Demand, Siemens Healthineers, Philips Healthcare, Cerner Corporation, Ping An Good Doctor, Babylon Health , Conexa Saúde, Okadoc, American Well |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |