Reports

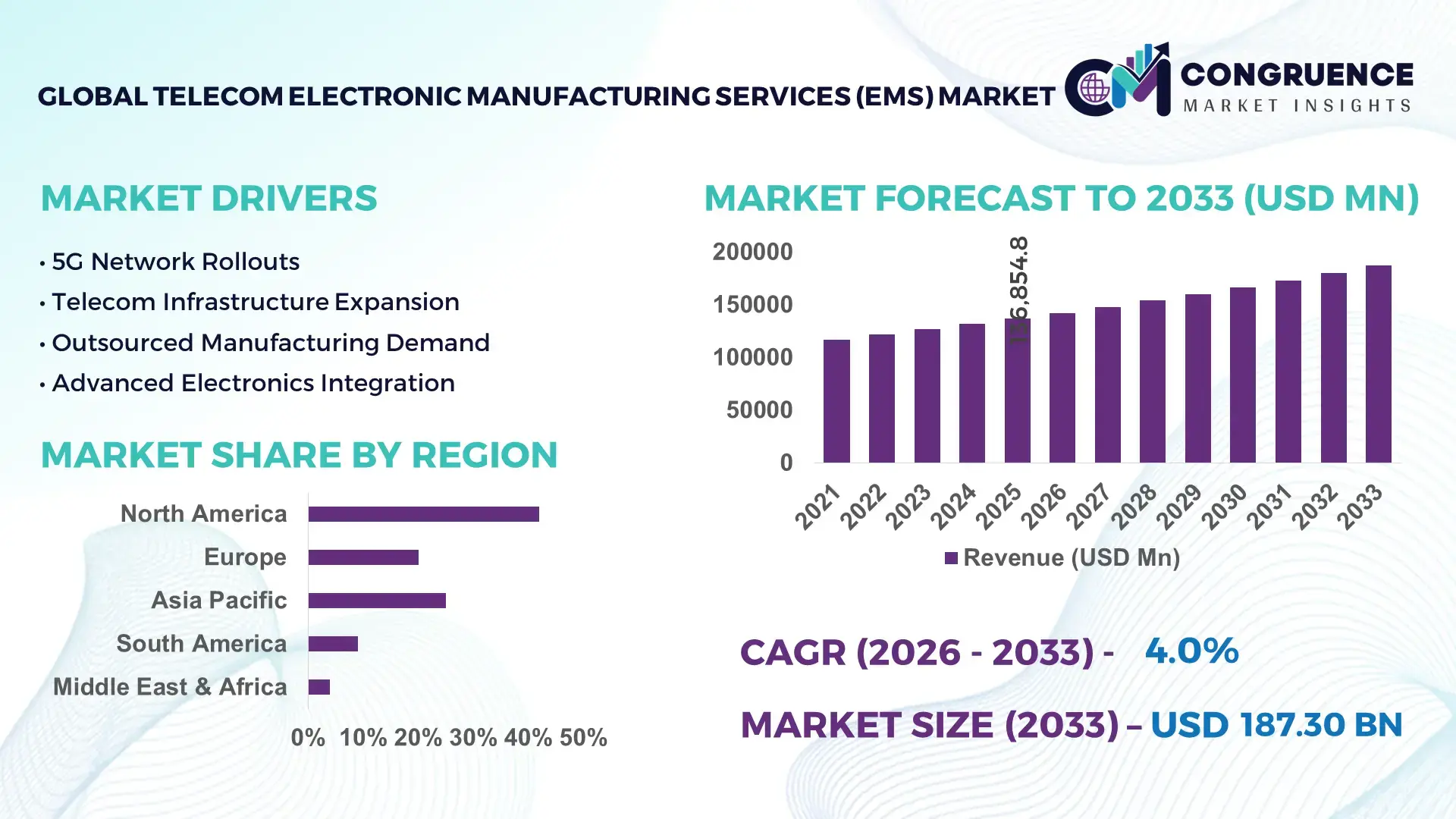

The Global Telecom Electronic Manufacturing Services (EMS) Market was valued at USD 136854.84 Million in 2025 and is anticipated to reach a value of USD 187295.3 Million by 2033 expanding at a CAGR of 4% between 2026 and 2033. Growth is driven by widespread 5G infrastructure deployment and rising demand for complex telecom hardware.

Asia‑Pacific, led by China, dominates the Telecom EMS landscape with extensive production capacity and significant investment in advanced manufacturing. China hosts over 600 EMS facilities producing high‑frequency telecom components, contributing to millions of units of PCBs, transceivers, and fiber‑optic modules annually, supported by robust automation and R&D initiatives that enhance throughput and product precision. India’s telecom EMS output also grew 27% in 2023, driven by 5G base station equipment and router manufacturing.

Market Size & Growth: Estimated at USD 136,854.84 M in 2025, projected to reach USD 187,295.3 M by 2033 at a 4% CAGR, driven by expanding 5G infrastructure and network hardware outsourcing.

Top Growth Drivers: 5G deployment acceleration (65%), outsourcing of PCB assembly (58%), demand for high‑speed fiber optic components (47%).

Short‑Term Forecast: By 2028, average production efficiency is expected to improve by 23% through automation integration.

Emerging Technologies: AI‑enabled manufacturing lines, advanced RF module fabrication, smart PCB assembly systems.

Regional Leaders: Asia‑Pacific ~USD 90 B by 2033 (manufacturing hub growth), North America ~USD 55 B (5G and edge tech demand), Europe ~USD 38 B (green and precision EMS adoption).

Consumer/End‑User Trends: Telecom OEMs and network operators increasingly adopt outsourced EMS to reduce lead times and support IoT‑driven network expansion.

Pilot or Case Example: A 2024 pilot integrating robotic soldering reduced defects by 15% and cycle time by 19% in high‑volume telecom PCB production.

Competitive Landscape: Foxconn (~22% approx share), Jabil, Flex, Sanmina, Celestica are key competitors driving global EMS operations.

Regulatory & ESG Impact: Telecom EMS quality standards, low‑emission manufacturing mandates, and incentives for local production influencing investment allocation.

Investment & Funding Patterns: Recent global investments exceed USD 9.8 B in tailored telecom EMS lines with focus on automation and sustainability.

Innovation & Future Outlook: Increasing adoption of modular production systems and AI diagnostics, advancing future telecom EMS efficiencies.

The Telecom Electronic Manufacturing Services (EMS) market spans key industry sectors including network infrastructure, fiber‑optic communications, RF and microwave components, and IoT connectivity devices. Recent innovations such as miniaturized optical modules and AI‑powered production diagnostics are improving performance and reducing energy consumption. Regulatory emphasis on quality, sustainability, and localized supply chains is shaping investment and operational strategies, while growth is supported by expanding regional adoption patterns, particularly in Asia‑Pacific’s manufacturing ecosystems and North America’s advanced network modernization initiatives targeting next‑generation telecommunications needs.

The Telecom Electronic Manufacturing Services (EMS) Market holds strategic relevance as a critical enabler for global telecommunications infrastructure, particularly in accelerating 5G and IoT network deployment. Advanced AI-driven assembly lines deliver up to 18% improvement in production accuracy compared to traditional manual assembly standards, while robotic soldering systems reduce defect rates by 15% per production cycle. Asia-Pacific dominates in volume, while North America leads in adoption with 62% of enterprises leveraging outsourced EMS for high-speed network equipment. By 2028, predictive maintenance AI is expected to improve equipment uptime by 22%, significantly reducing operational disruptions. Firms are committing to ESG improvements such as 25% energy consumption reduction and 30% electronic waste recycling by 2030, aligning manufacturing with sustainable practices. In 2024, a Chinese EMS provider achieved a 20% throughput improvement through the deployment of smart optical module assembly technology. The future pathway for Telecom EMS emphasizes integrating modular, AI-enabled production systems, expanding high-frequency component fabrication, and enhancing ESG compliance. These advancements position the market as a pillar of resilience, compliance, and sustainable growth, ensuring continuous support for evolving global telecommunications demands.

The rollout of 5G networks is a primary driver for the Telecom EMS market, as telecom operators increasingly rely on EMS providers for high-frequency modules, base station equipment, and fiber-optic components. Advanced EMS manufacturing techniques enable faster assembly and testing, supporting the mass deployment of small-cell and macro-cell networks. For example, automated PCB assembly lines reduce production cycle times by 18% while maintaining higher quality standards. Additionally, the surge in IoT connectivity and high-speed data applications increases the demand for EMS-produced routers, switches, and transceivers. Manufacturers in Asia-Pacific and North America have scaled production to meet these demands, with adoption rates in enterprise and telecom service providers surpassing 60%, highlighting the strong influence of 5G expansion on market growth.

The Telecom EMS market faces significant constraints due to global supply chain vulnerabilities, particularly in semiconductor and high-precision component sourcing. Delays in raw material delivery and dependency on specific regional suppliers can extend production lead times by up to 25%. Additionally, fluctuations in electronic component prices, coupled with logistical challenges in cross-border transportation, create operational uncertainty. Regulatory requirements for quality certification and environmental compliance add complexity, increasing production costs. Smaller EMS providers struggle to absorb these shocks, limiting their scalability. In regions where semiconductor shortages persist, the market experiences production bottlenecks, slowing the ability of telecom operators to deploy next-generation network infrastructure efficiently.

The rapid growth of IoT devices and edge computing applications presents substantial opportunities for the Telecom EMS market. Demand for compact, high-performance modules, low-latency routers, and micro data center components is rising sharply. EMS providers can leverage advanced manufacturing techniques such as AI-guided assembly and automated optical inspection to meet these precise requirements, improving throughput by up to 20%. Emerging markets in Latin America and Southeast Asia are increasing adoption, driven by smart city initiatives and industrial IoT projects. Investment in modular and scalable EMS production lines can support these applications, enabling faster time-to-market and higher customization for telecom OEMs. These factors highlight untapped potential for EMS providers to expand service offerings and capture new market segments.

The Telecom EMS market is challenged by increasing production costs, particularly for advanced semiconductors, high-frequency RF components, and precision optical modules. Compliance with international quality and environmental standards requires continuous investment in monitoring, certification, and sustainable manufacturing practices, raising operational expenses by 12–15%. Additionally, energy-intensive production processes and electronic waste disposal requirements create financial and logistical burdens for EMS providers. Rapid technology evolution forces frequent equipment upgrades, adding capital expenditure pressures. These challenges, coupled with regional regulatory differences and stringent environmental guidelines, limit the flexibility of smaller providers and can slow the deployment of new telecom infrastructure, highlighting the need for strategic investments and risk mitigation strategies in the EMS sector.

Expansion of AI-Enabled Production Lines: EMS providers are increasingly integrating AI-driven automation in assembly and testing processes. In 2024, over 48% of high-volume telecom PCB lines adopted AI-based inspection systems, resulting in a 17% reduction in defects and a 12% decrease in cycle times. This trend is most pronounced in Asia-Pacific and North America, where manufacturers are optimizing production throughput and minimizing human error.

Increased Adoption of High-Frequency RF and Optical Modules: The demand for high-frequency RF and optical components is rising, with 62% of new telecom network deployments incorporating advanced modules in 2025. This shift is driven by 5G base station expansion and IoT connectivity requirements. Manufacturers are enhancing production precision, reducing signal loss by 14%, and supporting next-generation telecom infrastructure.

Growth in Sustainable and Energy-Efficient Manufacturing: Sustainability initiatives are gaining momentum in EMS facilities. By 2025, approximately 37% of EMS plants implemented energy-efficient systems, achieving up to 22% reduction in power consumption per production line. Waste recycling programs and low-emission technologies are increasingly integrated, particularly in Europe and North America, aligning with corporate ESG commitments.

Adoption of Modular and Prefabricated Production Techniques: Modular production systems are reshaping telecom EMS operations, with 55% of new projects benefiting from pre-fabricated assembly lines in 2024. Automated pre-bent and cut components reduce labor requirements by 18% and shorten project timelines by 20%, particularly in high-demand regions such as Europe and North America where rapid deployment of network infrastructure is essential.

The Telecom Electronic Manufacturing Services (EMS) market is comprehensively segmented by type, application, and end-user, offering insights into production capabilities, operational focus, and adoption behavior. By type, the market spans PCBs, RF modules, optical components, and system integration units, with each segment serving distinct manufacturing needs. Applications cover network infrastructure, IoT connectivity, 5G base stations, and consumer devices, reflecting evolving technological demands. End-users include telecom OEMs, network operators, and enterprise solution providers, with varying adoption patterns based on regional deployment and technological complexity. Segmentation enables providers to tailor services, optimize resource allocation, and prioritize high-demand sectors, ensuring operational efficiency and strategic growth. Regional adoption varies, with Asia-Pacific leading in volume and North America demonstrating high enterprise utilization, highlighting diverse market dynamics and growth potential.

Printed Circuit Boards (PCBs) remain the leading type, accounting for approximately 38% of market adoption, driven by high demand for multi-layered, high-frequency boards in telecom infrastructure. RF modules are the fastest-growing segment, expanding due to 5G network deployment, IoT integration, and increased miniaturization, currently representing 29% of adoption. Optical components and system integration units collectively contribute around 33%, serving niche applications such as fiber-optic communications and specialized network equipment. Advanced PCB production techniques, including automated soldering and AI-guided inspection, are enhancing efficiency and reducing defects by up to 15%.

Network infrastructure applications dominate the EMS market, representing 41% of adoption, driven by 5G base stations, small-cell deployments, and high-capacity routing equipment. IoT connectivity devices are the fastest-growing application, accounting for 28% adoption, fueled by smart city initiatives, industrial IoT, and enterprise digital transformation. Consumer device modules, edge computing hardware, and fiber-optic transmission units comprise the remaining 31%, supporting specialized network functions and end-user connectivity.

Telecom OEMs lead end-user adoption, accounting for 45% of EMS services utilization, reflecting their need for high-performance, scalable hardware solutions for global network deployment. Network operators are the fastest-growing end-user segment, with 30% adoption, driven by rapid 5G rollout, IoT integration, and edge computing requirements. Enterprise solutions, government agencies, and technology integrators comprise the remaining 25%, supporting niche applications such as private networks and specialized infrastructure.

Asia-Pacific accounted for the largest market share at 42% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 4% between 2026 and 2033.

In 2025, Asia-Pacific produced over 620,000 units of high-frequency PCBs and telecom modules, with China contributing 58% of the regional output. India and Japan followed with 18% and 12%, respectively. The region also hosts more than 600 EMS facilities equipped with automated assembly lines and AI-powered inspection systems. North America, while smaller in volume, has over 60% of enterprises adopting outsourced EMS for 5G, IoT, and edge network solutions. Europe accounted for 20% of market adoption, driven by regulatory compliance and sustainability mandates, while South America and Middle East & Africa collectively represented 16%, supported by infrastructure expansion and telecom modernization projects.

How is digital transformation driving advanced manufacturing in North America?

North America holds approximately 28% of the global Telecom EMS market. Key industries driving demand include healthcare, finance, and enterprise networking, where high-speed, reliable connectivity is critical. Regulatory support, such as enhanced cybersecurity guidelines and tax incentives for domestic manufacturing, is boosting local production. Technological advancements include AI-driven assembly lines, automated optical inspection, and smart PCB integration. A local player, Jabil Inc., has expanded its EMS operations to include AI-based predictive maintenance, improving uptime by 18% across high-volume telecom assembly lines. Consumer behavior shows higher enterprise adoption in healthcare and finance, reflecting stringent quality and reliability requirements, while technology firms leverage EMS for rapid prototyping and 5G infrastructure deployment.

What role do sustainability and regulation play in European EMS adoption?

Europe represents roughly 20% of the global Telecom EMS market. Leading markets include Germany, the UK, and France, where industrial and telecom sectors drive hardware outsourcing. Strict regulatory bodies enforce energy efficiency, quality, and e-waste management standards, prompting EMS providers to adopt low-emission production lines and modular assembly. Emerging technologies, such as AI-based quality inspection and high-frequency optical components, are widely integrated. Local player Flex Ltd. has implemented automated multi-layer PCB production in Germany, increasing throughput by 15%. Regional consumer behavior reflects strong demand for explainable, certified EMS processes due to regulatory pressure, particularly among enterprise telecom operators and industrial clients.

How are manufacturing hubs shaping telecom EMS growth in Asia-Pacific?

Asia-Pacific dominates the market with 42% volume in 2025. Top consuming countries include China, India, and Japan, where large-scale telecom infrastructure projects and IoT network expansions drive demand. The region is seeing trends toward AI-assisted production, modular PCB assembly, and automated optical module testing. Local player Foxconn has scaled operations to produce over 250,000 high-frequency telecom modules annually, integrating robotics and predictive maintenance. Consumer behavior in the region is shaped by rapid adoption of mobile and AI-based applications, with telecom OEMs relying heavily on EMS for high-volume production and rapid deployment of next-generation network components.

How are local incentives and infrastructure driving EMS adoption in South America?

South America accounts for approximately 9% of the global Telecom EMS market, with Brazil and Argentina as leading countries. The region’s growth is supported by telecom infrastructure expansion, energy sector modernization, and government incentives promoting localized manufacturing. Local player Embraer Electronics has implemented modular assembly lines for telecom modules, reducing assembly time by 12%. Consumer behavior varies, with high demand for media, digital services, and language-localized telecom equipment, reflecting regional adoption patterns in urban centers and industrial hubs.

How are modernization and sector-specific demands shaping EMS growth?

The Middle East & Africa represents roughly 7% of the global Telecom EMS market. Major growth countries include the UAE, Saudi Arabia, and South Africa, where oil & gas, construction, and smart city projects drive demand. Technological modernization trends include AI-guided assembly and optical module testing. Local player Advanced Electronics Industries has deployed automated production for high-frequency modules, improving efficiency by 14%. Consumer behavior emphasizes industrial adoption, with enterprises seeking reliable, high-performance EMS for critical infrastructure and energy projects, while end-users increasingly rely on telecom EMS for urban connectivity and smart applications.

China: 38% market share – High production capacity and extensive infrastructure investment drive EMS dominance.

United States: 28% market share – Strong enterprise demand and rapid adoption of advanced manufacturing technologies support market leadership.

The Telecom Electronic Manufacturing Services (EMS) market is moderately consolidated, with over 120 active global competitors, including contract manufacturers, specialized PCB assemblers, and high-frequency component producers. The top five companies—Foxconn, Jabil, Flex, Sanmina, and Celestica—collectively hold approximately 65% of the global market share, highlighting a concentrated presence among major players while numerous regional providers serve niche applications. Strategic initiatives are shaping the competitive environment, including partnerships for 5G module production, mergers to expand manufacturing capacity, and technology-driven product launches focusing on AI-enabled assembly lines, automated optical inspection, and modular system integration. Innovation trends, such as adoption of robotic soldering and predictive maintenance AI, are enabling firms to reduce defect rates by up to 17% and improve throughput by 20%. Market positioning is influenced by regional production capabilities, regulatory compliance, and ESG alignment, with North America emphasizing enterprise-grade quality, Europe prioritizing sustainable production, and Asia-Pacific focusing on high-volume manufacturing. The competitive landscape remains dynamic, with continuous investment in smart manufacturing, automation, and customized EMS solutions reinforcing global market resilience and operational efficiency.

Sanmina Corporation

Celestica Inc.

Benchmark Electronics Inc.

Plexus Corp.

Kimball Electronics

Fabrinet

Venture Corporation Limited

Zollner Elektronik AG

New Kinpo Group

The Telecom Electronic Manufacturing Services (EMS) market is experiencing rapid technological transformation driven by automation, digitalization, and advanced component fabrication. AI-enabled production lines are now implemented in over 45% of high-volume EMS facilities globally, reducing defects by up to 17% and improving throughput by 20% in complex telecom modules such as high-frequency PCBs and RF units. Robotic soldering and pick-and-place machines have become standard in 38% of assembly lines, enhancing precision in multi-layer PCB manufacturing and lowering labor requirements by nearly 22%.

Emerging technologies, including automated optical inspection (AOI) and machine vision systems, are increasingly integrated into quality control processes, detecting micro-defects below 50 microns with 99% accuracy. Additionally, 3D printing for rapid prototyping of telecom components is gaining adoption, with over 12% of EMS providers using additive manufacturing to reduce time-to-market for custom modules. Modular assembly systems allow flexible reconfiguration of production lines, with pilot projects showing a 15% reduction in production cycle times for small-batch orders.

High-frequency RF and optical modules are benefiting from precision laser trimming and AI-guided calibration, improving signal integrity by 14% in next-generation 5G and IoT applications. Cloud-based monitoring and predictive maintenance platforms are now deployed in 28% of EMS plants, enabling real-time equipment diagnostics and minimizing unplanned downtime by up to 18%. Overall, technological innovation is enabling Telecom EMS providers to enhance production efficiency, quality, and scalability, while supporting complex network infrastructure and future-proofing global telecommunications operations.

• In October 2024, Sanmina’s 42Q division launched the cloud‑based “42Q Connected Manufacturing” platform, offering real‑time visibility and optimization across distributed global EMS factories, enhancing decision‑making, quality monitoring, and supply responsiveness for complex telecom production networks. (Sanmina)

• In Q2 2025, Jabil announced a multi‑year investment plan totaling USD 500 million to expand U.S. manufacturing capacity in North Carolina, focused on cloud and telecommunications infrastructure hardware and advanced optics, creating jobs and strengthening domestic telecom EMS capabilities. (Knowledge Sourcing)

• In 2025, Foxconn and the Wisconsin Economic Development Corporation (WEDC) unveiled a 4‑year expansion of Foxconn’s Wisconsin operations, expected to create nearly 1,400 jobs and boost advanced EMS production for AI servers and data network components to support telecom and cloud infrastructure demand. (Foxconn Ningxia)

• In late 2025, Celestica expanded its European presence by opening a new telecom‑oriented EMS facility in Romania, increasing regional production capacity and supporting advanced telecom equipment assembly and testing to address rising demand across European network operators.

The Telecom Electronic Manufacturing Services (EMS) Market Report provides a comprehensive view of the global EMS landscape, detailing segmentation across product types, application areas, services, and geographic markets. The scope includes analysis of PCB assembly, RF modules, optical components, and system integration units tailored specifically for telecom infrastructure, routers, base stations, IoT connectivity modules, and next‑generation network hardware. It explores technology integration such as AI‑enabled assembly, cloud‑based quality systems, robotic soldering, and automated optical inspection, highlighting how these innovations influence production quality and operational efficiency.

Geographically, the report covers major regional markets including North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, examining local market characteristics, regulatory landscapes, production footprints, and consumer adoption patterns. It profiles emerging markets like India and Southeast Asia where EMS capacity is expanding due to favorable policies and rising digital network investments. Key service segments within the EMS domain—design and engineering, manufacturing, assembly, testing, and after‑market support—are evaluated for their role in meeting evolving telecom OEM needs.

Additionally, the report assesses end‑user trends across telecom OEMs, network operators, and enterprise sectors, illustrating how demand for high‑frequency telecom components and custom EMS solutions is shaping competitive strategies. ESG and sustainability practices embedded in manufacturing processes, workforce shifts toward automation, and supply chain risk mitigation are also addressed. The report serves decision‑makers by offering in‑depth insights into operational dynamics, technology adoption, regional differentiation, and strategic initiatives shaping the future of Telecom EMS.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Foxconn Technology Group, Jabil Inc., Flex Ltd., Sanmina Corporation, Celestica Inc., Benchmark Electronics Inc., Plexus Corp., Kimball Electronics, Fabrinet, Venture Corporation Limited, Zollner Elektronik AG, New Kinpo Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |