Reports

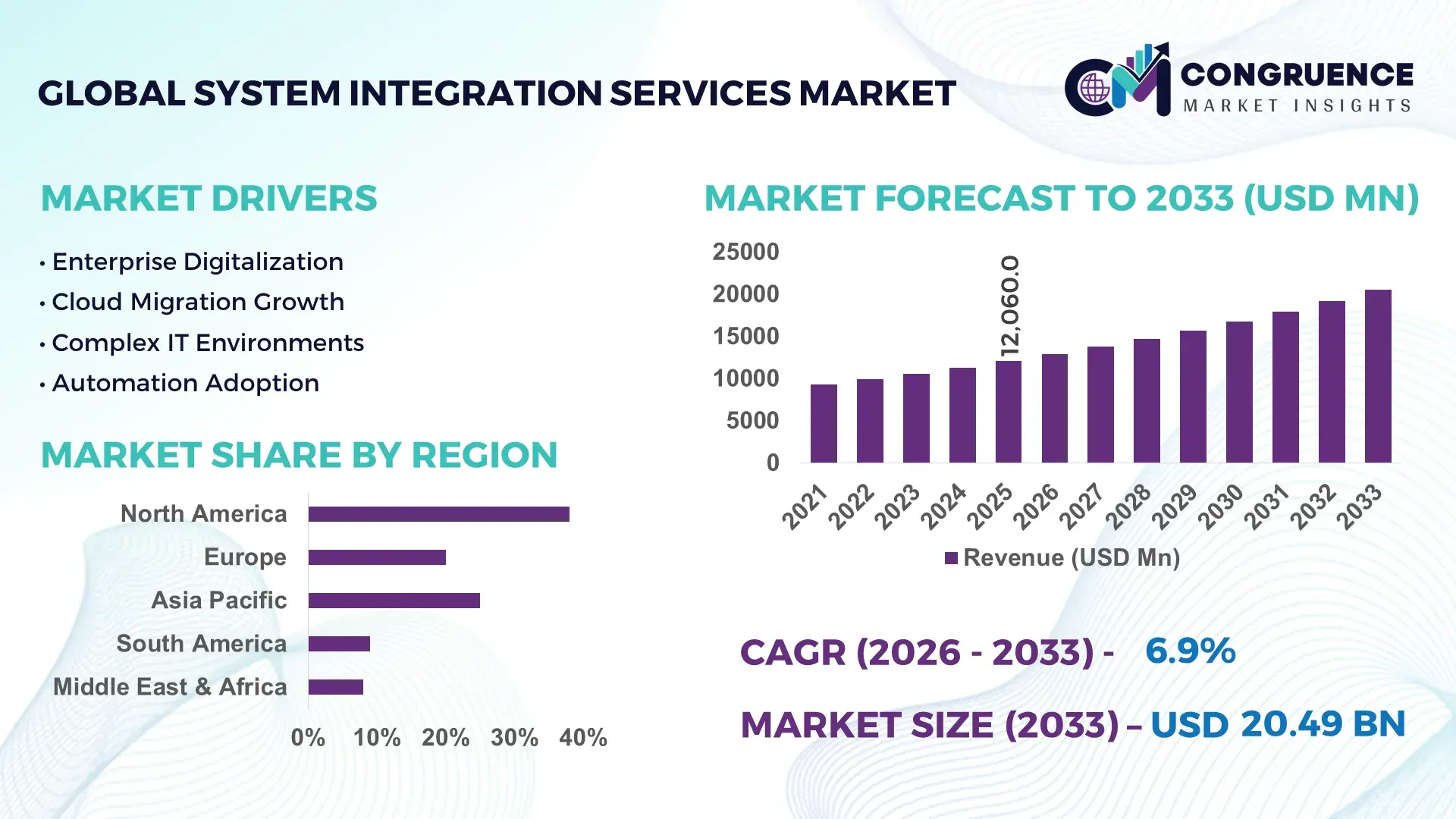

The Global System Integration Services Market was valued at USD 12060 Million in 2025 and is anticipated to reach a value of USD 20490.07 Million by 2033 expanding at a CAGR of 6.85% between 2026 and 2033. Growth is accelerating through enterprise-wide AI integration, industrial cloud migration, cybersecurity modernization, and multi-vendor IT consolidation projects across manufacturing, BFSI, telecom, healthcare, and government infrastructure networks.

The United States dominates the global system integration services market with over 34% deployment share, supported by hyperscale cloud investments exceeding USD 90 billion and rapid adoption of AI-enabled enterprise platforms across defense, banking, and industrial automation sectors. More than 68% of large U.S. enterprises now operate hybrid IT environments requiring advanced integration frameworks, compared to nearly 49% across Germany and Japan combined. China continues expanding aggressively through smart manufacturing and digital infrastructure programs, with industrial IoT deployment in factories surpassing 35% during 2026 amid regional supply-chain restructuring and semiconductor localization efforts influenced by ongoing geopolitical technology restrictions between the U.S. and China. India is emerging as a high-growth integration hub, supported by expanding GCC operations, enterprise SaaS deployment, and public digital infrastructure modernization.

Organizations prioritizing scalable integration ecosystems, automation-driven interoperability, and cyber-resilient infrastructure partnerships are securing stronger operational continuity, lower deployment complexity, and faster enterprise transformation execution.

Market Size & Growth: USD 12060 Million in 2025 reaching USD 20490.07 Million by 2033 at 6.85% CAGR, driven by AI-led enterprise modernization and industrial cloud integration.

Top Growth Drivers: Cloud migration contributes 41% demand growth, cybersecurity integration 32%, and industrial automation projects 27% across global enterprises.

Short-Term Forecast: By 2028, integration automation reduces enterprise deployment time by 38% while improving operational efficiency by 29% across hybrid IT environments.

Emerging Technologies: AI orchestration, edge computing, and low-code integration platforms improve workflow accuracy by 34% and reduce manual configuration dependency by 31%.

Regional Leaders: North America exceeds USD 7 billion through hyperscale cloud adoption, Asia-Pacific crosses USD 5 billion via smart manufacturing, while Europe advances digital compliance integration investments.

Consumer/End-User Trends: Over 64% of enterprises prioritize unified multi-cloud integration strategies to improve data visibility, cybersecurity resilience, and cross-platform operational continuity.

Pilot/Case Example: In 2025, a global telecom integration initiative reduced network downtime by 26% using AI-assisted orchestration and automated infrastructure monitoring systems.

Competitive Landscape: Top providers control nearly 44% market share, with leading participation from IBM, Accenture, Capgemini, TCS, and Infosys in high-value transformation contracts.

Regulatory & ESG Impact: Digital sovereignty policies and ESG compliance frameworks improved secure data integration adoption by 33% across European and Asia-Pacific enterprises.

Investment & Funding: Enterprise digital transformation investments surpassed USD 70 billion globally, driven by cloud partnerships, industrial automation expansion, and supply-chain resilience initiatives.

Innovation & Future Outlook: Advanced autonomous integration platforms and AI-driven observability tools are accelerating predictive infrastructure management and enterprise-wide operational interoperability.

System integration services demand remains strongest across BFSI, telecom, healthcare, manufacturing, and smart infrastructure projects requiring real-time interoperability and cyber-resilient operations. AI-enabled orchestration platforms improved integration efficiency by nearly 30% during 2026, while edge-cloud convergence accelerated deployment speed across distributed enterprises. Regulatory data localization requirements and supply-chain digitalization initiatives are further reshaping enterprise integration strategies, setting the foundation for deeper competitive and operational analysis.

Enterprise infrastructure modernization is positioning the system integration services market as a core strategic layer for industrial competitiveness, cybersecurity resilience, and AI-driven operational scalability. Organizations are consolidating fragmented cloud, edge, ERP, and cybersecurity architectures to reduce latency, improve data interoperability, and strengthen decision-making accuracy. The market is also benefiting from supply-chain restructuring across the United States, Germany, and Southeast Asia, where manufacturers are accelerating smart factory integration and digital logistics visibility following semiconductor and industrial component disruptions experienced after global trade realignments.

AI-enabled integration platforms are delivering nearly 35% faster deployment cycles compared with legacy middleware-based systems while reducing infrastructure maintenance costs by approximately 22%. The United States leads large-scale enterprise orchestration projects, whereas Japan and South Korea prioritize precision manufacturing integration and robotics interoperability. Over 61% of global enterprises are expected to expand hybrid integration frameworks within the next three years, driven by increasing adoption of industrial IoT, multi-cloud infrastructure, and real-time analytics environments.

A leading automotive manufacturer recently integrated predictive maintenance, warehouse automation, and supplier tracking into a unified platform, reducing operational downtime by 27% across production facilities. Companies are increasing investments in AI observability tools, cybersecurity alliances, and industry-specific integration ecosystems to secure stronger operational continuity, accelerate automation maturity, and strengthen long-term competitive positioning.

Large enterprises are accelerating integration investments to unify fragmented cloud, cybersecurity, ERP, and operational technology environments. More than 64% of global enterprises now operate multi-cloud infrastructures, while nearly 47% of manufacturers are deploying integrated industrial IoT frameworks to improve operational visibility and predictive maintenance efficiency. In Germany and the United States, infrastructure modernization initiatives tied to semiconductor production and smart manufacturing expansion are increasing demand for advanced orchestration and interoperability services. This shift is directly reducing process latency and improving cross-platform workflow automation. Service providers are responding through AI-enabled integration platforms, industry-specific consulting partnerships, and cybersecurity-focused acquisitions. A critical strategic advantage is emerging for vendors capable of integrating legacy industrial systems without disrupting ongoing production operations.

Complex legacy infrastructure remains a major operational restraint across banking, healthcare, and manufacturing sectors where over 43% of enterprise systems still operate on outdated architecture frameworks. Integration costs for hybrid environments have increased by nearly 18% due to compatibility gaps between cloud-native applications and older enterprise software stacks. In Japan and parts of Eastern Europe, industrial operators continue facing deployment delays because proprietary operational technology systems limit interoperability flexibility. These constraints directly affect implementation speed, operational scalability, and cybersecurity consistency. Companies are mitigating risks through phased migration strategies, localized data infrastructure deployment, and standardized API-based integration frameworks. Vendors capable of simplifying cross-platform compatibility are gaining stronger contract retention and long-term enterprise service expansion opportunities.

AI-driven orchestration and autonomous workflow integration are creating high-value opportunities across logistics, manufacturing, healthcare, and telecom infrastructure modernization projects. Nearly 58% of enterprises are prioritizing intelligent automation investments, while edge-enabled industrial monitoring systems have improved operational response efficiency by over 30% in large production facilities. India is emerging as a strategic deployment center due to expanding GCC operations, public digital infrastructure growth, and enterprise SaaS adoption. Government-backed digitalization initiatives and sovereign cloud frameworks are also increasing demand for secure integration ecosystems. Companies are expanding R&D investment into low-code integration platforms, AI observability tools, and industry-specific automation partnerships. A notable opportunity exists in integrating sustainability monitoring systems with operational analytics to optimize industrial energy utilization and compliance tracking.

Expanding hybrid infrastructure and interconnected enterprise ecosystems are intensifying cybersecurity and execution complexity across integration deployments. Nearly 52% of enterprises report increased security exposure from multi-cloud environments, while ransomware attacks targeting operational technology networks have risen by over 28% across industrial sectors. In the United States and South Korea, real-time manufacturing systems require continuous interoperability without compromising cybersecurity resilience, creating major deployment consistency challenges. The shortage of advanced cloud-security and integration engineering talent is also extending implementation timelines for large-scale projects. Companies must strengthen zero-trust architectures, AI-assisted threat monitoring, and cross-platform security governance frameworks to maintain operational continuity. Long-term competitiveness increasingly depends on scalable cyber-resilient integration infrastructure capable of supporting autonomous enterprise operations.

AI-Led Workflow Consolidation Enterprises are replacing fragmented middleware stacks with AI-enabled orchestration platforms to unify ERP, cybersecurity, analytics, and cloud operations. More than 57% of large enterprises expanded intelligent workflow integration during 2026, while automated incident resolution improved operational response speed by nearly 33%. Labor shortages in enterprise IT operations are accelerating low-code deployment adoption, particularly across the United States and India. Companies are responding through AI integration partnerships, automation-focused acquisitions, and centralized observability infrastructure to reduce operational complexity and improve infrastructure scalability.

Industry-Specific Integration Expansion Manufacturing, healthcare, and BFSI enterprises are demanding sector-specific integration architectures rather than generalized deployment frameworks. Nearly 48% of industrial firms now require real-time operational technology interoperability, while healthcare organizations reduced data synchronization delays by approximately 26% through API-driven clinical platform integration. Germany and Japan are prioritizing precision manufacturing integration to support smart factory modernization. Vendors are restructuring service portfolios around vertical expertise, cybersecurity customization, and operational compliance management to improve deployment consistency and enterprise retention rates.

Edge and Hybrid Infrastructure Scaling Distributed enterprise operations are accelerating edge-cloud integration deployment across logistics, telecom, and industrial automation environments. More than 44% of telecom operators implemented hybrid integration frameworks in 2026 to support low-latency applications and 5G infrastructure coordination. Real-time warehouse visibility deployments improved supply-chain response efficiency by nearly 29% following global logistics disruptions. Companies are increasing investment in edge orchestration tools, localized cloud partnerships, and decentralized monitoring systems to strengthen infrastructure resilience and reduce operational downtime.

Cyber-Resilient Integration Priorities Cybersecurity is becoming a primary purchasing factor in integration contracts as enterprises manage rising ransomware exposure and regulatory scrutiny. Over 52% of enterprises expanded zero-trust integration architecture deployment, while automated compliance monitoring reduced audit preparation workloads by nearly 24%. South Korean semiconductor manufacturers and U.S. defense contractors are accelerating secure interoperability projects following stricter data governance standards. Service providers are integrating AI-assisted threat detection, encrypted workflow management, and sovereign cloud compatibility into enterprise integration strategies to strengthen long-term operational continuity.

Cloud Integration leads the market due to rising enterprise migration toward hybrid infrastructure, scalable orchestration frameworks, and real-time interoperability across distributed operations. Nearly 62% of enterprises now prioritize cloud-native integration platforms to improve deployment flexibility and reduce infrastructure maintenance complexity. Infrastructure Integration maintains strong demand across telecom, manufacturing, and government modernization projects where operational continuity and cybersecurity resilience remain critical. Data Integration is emerging rapidly as enterprises expand AI analytics, with integrated data visibility improving decision-making efficiency by approximately 31%. Application Integration continues supporting ERP and workflow modernization, particularly across banking and retail ecosystems, while Consulting Services are expanding through enterprise transformation planning and cybersecurity advisory requirements. Companies are strengthening platform interoperability, expanding managed integration services, and forming cloud ecosystem alliances to improve deployment speed and customer retention. Investment priorities are shifting toward automation-ready architectures capable of supporting multi-cloud and edge-enabled enterprise environments.

ERP Integration remains the dominant application segment as enterprises modernize finance, procurement, inventory, and supply-chain operations through unified digital infrastructure. More than 59% of multinational enterprises expanded ERP interoperability projects during 2026 to improve workflow standardization and operational visibility. Cloud Migration is the fastest-growing application as organizations transition from legacy infrastructure toward scalable hybrid environments, reducing infrastructure provisioning time by nearly 34%. Process Automation adoption is also accelerating across manufacturing and telecom operations to improve response speed and reduce manual dependency. CRM Integration continues evolving through AI-enabled customer analytics and omnichannel engagement frameworks, while Data Management integration is becoming strategically important for governance, cybersecurity, and predictive analytics initiatives. Companies are increasing investments in API orchestration, workflow automation, and industry-specific deployment ecosystems to strengthen operational continuity and digital transformation execution.

BFSI represents the leading end-user segment due to high transaction volumes, regulatory compliance requirements, and increasing dependence on secure real-time interoperability across digital banking ecosystems. Nearly 61% of financial institutions expanded integration modernization initiatives in 2026 to strengthen fraud detection, customer analytics, and cross-platform payment infrastructure. Healthcare is emerging as the fastest-growing end-user segment as hospitals and healthcare networks accelerate interoperability deployment for clinical systems, digital records, and AI-assisted diagnostics. Manufacturing maintains strong integration demand through industrial automation and predictive maintenance expansion, while IT and Telecom operators are prioritizing network orchestration and hybrid infrastructure management. Government agencies are increasing secure cloud integration spending tied to digital public infrastructure modernization, and retail enterprises are scaling omnichannel operational integration to improve inventory visibility and customer engagement efficiency. Service providers are responding with industry-specific platforms, cybersecurity-focused deployment models, and flexible managed-service pricing strategies to strengthen competitive positioning.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2026 and 2033.

AI-Driven Enterprise Infrastructure Modernization

North America maintains leadership through advanced enterprise digitalization, hyperscale cloud deployment, and strong cybersecurity integration demand across BFSI, telecom, defense, and healthcare industries. The region contributes nearly 36% of global deployment activity, supported by rapid AI-enabled workflow modernization and industrial automation investments. More than 63% of large enterprises in the United States and Canada now operate hybrid cloud ecosystems requiring multi-platform interoperability services. Telecom providers accelerated 5G infrastructure integration projects during 2026, while manufacturing firms expanded predictive maintenance deployment across connected production facilities. Strategic partnerships between cloud providers, cybersecurity vendors, and integration service firms are strengthening operational scalability and reducing enterprise deployment complexity across high-value digital transformation projects.

United States Market Outlook: The United States remains the region’s primary integration hub due to strong hyperscale cloud infrastructure, enterprise AI adoption, and defense-sector modernization programs. More than 68% of Fortune 1000 companies expanded AI-assisted integration frameworks in 2026 to improve interoperability, cybersecurity visibility, and workflow automation efficiency. Federal cybersecurity mandates and semiconductor manufacturing expansion are also accelerating demand for secure operational technology integration and industrial infrastructure orchestration across large enterprise networks.

Industrial Automation and Compliance-Led Integration Expansion

Europe is strengthening its position through industrial automation modernization, sovereign cloud deployment, and stricter digital compliance frameworks across manufacturing, automotive, and public infrastructure sectors. Nearly 31% of enterprises across Germany, France, and the Nordic countries increased operational technology integration spending during 2026 to improve cybersecurity resilience and supply-chain visibility. Smart manufacturing investments and ESG-focused infrastructure modernization are accelerating deployment of AI-enabled interoperability platforms. Cross-border data governance requirements are also increasing demand for localized cloud integration and compliance-driven orchestration services. Integration vendors are expanding partnerships with industrial software providers and cybersecurity specialists to support enterprise modernization programs while reducing operational risk and regulatory complexity.

Germany Market Outlook: Germany leads the European market through advanced manufacturing infrastructure, industrial automation density, and strong Industry 4.0 deployment activity. More than 52% of large manufacturing enterprises expanded connected factory integration systems in 2026 to improve predictive maintenance and production coordination efficiency. Automotive and industrial engineering firms are prioritizing edge-cloud interoperability and real-time analytics integration to strengthen operational precision, energy optimization, and supply-chain resilience across high-value export-oriented manufacturing ecosystems.

Large-Scale Digital Infrastructure Deployment

Asia-Pacific is emerging as the fastest-expanding regional market due to rapid industrial digitalization, expanding enterprise cloud adoption, and large-scale smart infrastructure deployment across China, India, Japan, and Southeast Asia. The region accounts for nearly 29% of global integration deployment activity, supported by aggressive investment in telecom modernization, industrial IoT ecosystems, and public digital infrastructure. More than 58% of enterprises across major Asian industrial hubs increased automation-focused integration spending during 2026. Manufacturing localization strategies and semiconductor supply-chain restructuring are accelerating demand for real-time operational interoperability. Companies are expanding regional delivery centers, AI orchestration capabilities, and localized cloud partnerships to support large-scale enterprise transformation and infrastructure modernization requirements.

China Market Outlook: China remains strategically dominant due to extensive smart manufacturing deployment, industrial AI adoption, and large-scale digital infrastructure expansion. More than 46% of industrial enterprises accelerated integrated factory modernization projects during 2026 to improve production coordination and logistics visibility. Government-backed digital infrastructure initiatives and semiconductor localization efforts are strengthening demand for secure industrial integration platforms, predictive maintenance systems, and AI-enabled operational orchestration across manufacturing and telecom ecosystems.

Cloud Modernization Driving Enterprise Demand

South America is experiencing increasing integration demand through enterprise cloud migration, telecom modernization, and digital banking expansion across Brazil, Chile, and Colombia. The region represents nearly 8% of global deployment activity, with financial services and retail enterprises accelerating interoperability investments to improve operational agility and customer analytics capabilities. More than 41% of enterprises in key urban markets expanded hybrid infrastructure deployment during 2026 to support digital transaction growth and remote operational management. Infrastructure limitations and cybersecurity maturity gaps continue affecting deployment consistency in some sectors. Integration providers are responding through localized cloud partnerships, managed-service expansion, and industry-specific automation frameworks to improve scalability and reduce implementation complexity.

Brazil Market Outlook: Brazil leads the regional market through expanding fintech infrastructure, enterprise cloud adoption, and telecom digitalization initiatives. Nearly 49% of large enterprises increased operational integration spending during 2026 to improve payment interoperability, logistics visibility, and customer engagement workflows. Retail and banking institutions are accelerating AI-enabled CRM and data integration deployment to strengthen digital service delivery while improving operational resilience across increasingly distributed enterprise environments.

Smart Infrastructure and Sovereign Cloud Expansion

Middle East & Africa is advancing through smart city programs, public-sector digitalization, and sovereign cloud infrastructure investments across the Gulf region and selected African technology hubs. The region contributes approximately 7% of global integration deployment activity, supported by large-scale government modernization initiatives and expanding telecom infrastructure projects. More than 38% of enterprises across Gulf Cooperation Council countries accelerated cybersecurity-focused integration deployment during 2026 to support digital governance and critical infrastructure resilience. Energy-sector modernization and logistics automation projects are also increasing demand for industrial interoperability solutions. Service providers are strengthening regional partnerships, localized delivery capabilities, and managed cybersecurity integration services to support infrastructure scalability and operational continuity.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region’s leading market through aggressive smart city investment, public digital transformation programs, and expanding cloud infrastructure deployment. More than 44% of large enterprises increased integration spending during 2026 to support AI-enabled public services, industrial automation, and energy-sector modernization initiatives. National digital infrastructure programs and data localization priorities are accelerating deployment of secure interoperability frameworks, sovereign cloud ecosystems, and real-time operational analytics platforms across government and enterprise sectors.

Accenture, IBM, Capgemini, Tata Consultancy Services, Infosys, and Wipro compete aggressively across enterprise cloud integration, AI orchestration, cybersecurity modernization, and industrial automation projects. Global leaders are competing against regional specialists on deployment speed, industry customization, and managed-service scalability, while cloud-native integrators challenge legacy consulting firms through automation-first delivery models. The top five players collectively control nearly 44% of market activity through long-term enterprise contracts and multi-cloud ecosystem partnerships. AI-enabled workflow integration improves deployment efficiency by almost 35%, while automated observability platforms reduce operational downtime by nearly 28%, intensifying technology-led competition. Companies are expanding through cybersecurity acquisitions, sovereign cloud alliances, and industry-focused integration frameworks targeting manufacturing, BFSI, and telecom sectors. Market consolidation is accelerating as enterprises prioritize fewer strategic vendors with end-to-end interoperability capabilities. High entry barriers stem from cybersecurity certification requirements, enterprise trust, and complex infrastructure expertise. Winning requires scalable AI-driven integration ecosystems, deep vertical specialization, and resilient multi-cloud delivery execution.

Accenture

IBM

Capgemini

Tata Consultancy Services

Infosys

Wipro

Cognizant

HCLTech

Fujitsu

DXC Technology

NTT DATA

Atos

Tech Mahindra

Deloitte

AI-enabled orchestration platforms, hybrid cloud integration, and API-led interoperability frameworks are reshaping enterprise integration architecture across telecom, BFSI, manufacturing, and healthcare sectors. More than 62% of large enterprises deployed AI-assisted integration monitoring in 2026, improving incident response efficiency by nearly 34%. Cloud-native integration platforms reduced deployment complexity by approximately 28% compared with legacy middleware environments. Enterprises are increasingly consolidating fragmented ERP, cybersecurity, and analytics systems into unified interoperability ecosystems to improve operational visibility, workflow automation, and cross-platform scalability.

Edge computing integration, low-code automation, and agentic AI systems are emerging as high-impact technologies between 2026 and 2028. Nearly 49% of industrial enterprises expanded edge-cloud orchestration deployments to support low-latency manufacturing analytics and predictive maintenance operations. AI-enabled observability platforms improved infrastructure uptime by almost 31%, while automated API governance reduced integration maintenance workloads by 24%. Companies are responding through sovereign cloud partnerships, industry-specific automation platforms, and cybersecurity-focused orchestration ecosystems designed for real-time operational continuity and compliance-intensive infrastructure environments.

Disruptive integration models centered on autonomous AI agents and self-healing enterprise systems are creating a competitive divide between advanced digital operators and legacy infrastructure providers. Agent-driven integration environments process workflows nearly 40% faster than rule-based legacy architectures while lowering operational support costs by approximately 22%. Global consulting leaders, hyperscale cloud providers, and cybersecurity-focused integration firms benefit most from this shift because enterprises increasingly prioritize scalable AI interoperability, secure data orchestration, and predictive infrastructure management. Organizations delaying modernization risk operational fragmentation, slower deployment execution, and rising cybersecurity exposure as enterprise ecosystems become increasingly distributed and automation dependent.

April 2026 – Accenture and Google Cloud expanded enterprise AI integration collaboration through Gemini Enterprise Acceleration Program, enabling deployment of hundreds of industry-specific AI agents and improving workflow scalability for multinational enterprises.

March 2026 – Accenture and Databricks launched a dedicated AI integration business group supported by over 25,000 Databricks-trained professionals, accelerating enterprise deployment of agent-ready databases and scalable AI applications. Source: newsroom.accenture.com/databricks

October 2024 – Capgemini strengthened focus on AI-driven transformation services despite weak manufacturing demand, with quarterly operational adjustments supporting long-term enterprise integration modernization and digital infrastructure optimization initiatives globally. Source: reuters.com

May 2026 – HUMAIN and Accenture partnered to accelerate sovereign AI and enterprise integration deployment across Saudi Arabia, supporting production-grade AI systems through localized infrastructure, cloud platforms, and modernization frameworks. Source: newsroom.accenture.com/humain

The report delivers comprehensive analysis across Infrastructure Integration, Application Integration, Data Integration, Cloud Integration, and Consulting Services while evaluating operational demand trends across ERP Integration, CRM Integration, Process Automation, Data Management, and Cloud Migration environments. It assesses adoption patterns across BFSI, Healthcare, Manufacturing, Retail, IT and Telecom, and Government sectors, where over 60% of enterprises are expanding hybrid integration and AI-enabled interoperability deployment strategies. The study also examines deployment concentration, cloud modernization intensity, cybersecurity integration trends, and enterprise automation priorities across North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The report provides strategic insights into AI orchestration platforms, edge-cloud interoperability, low-code integration ecosystems, and sovereign cloud infrastructure modernization between 2026 and 2033. It evaluates competitive positioning, enterprise transformation strategies, operational scalability, and integration deployment models used by global service providers and regional specialists. Coverage includes industrial automation integration, cybersecurity-driven interoperability, sector-specific modernization frameworks, and emerging opportunities tied to smart manufacturing, public digital infrastructure, and distributed enterprise ecosystems supporting long-term investment planning and market expansion decisions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 12060 Million |

|

Market Revenue in 2033 |

USD 20490.07 Million |

|

CAGR (2026 - 2033) |

6.85% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Accenture, IBM, Capgemini, Tata Consultancy Services, Infosys, Wipro, Cognizant, HCLTech, Fujitsu, DXC Technology, NTT DATA, Atos, Tech Mahindra, Deloitte |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |