Reports

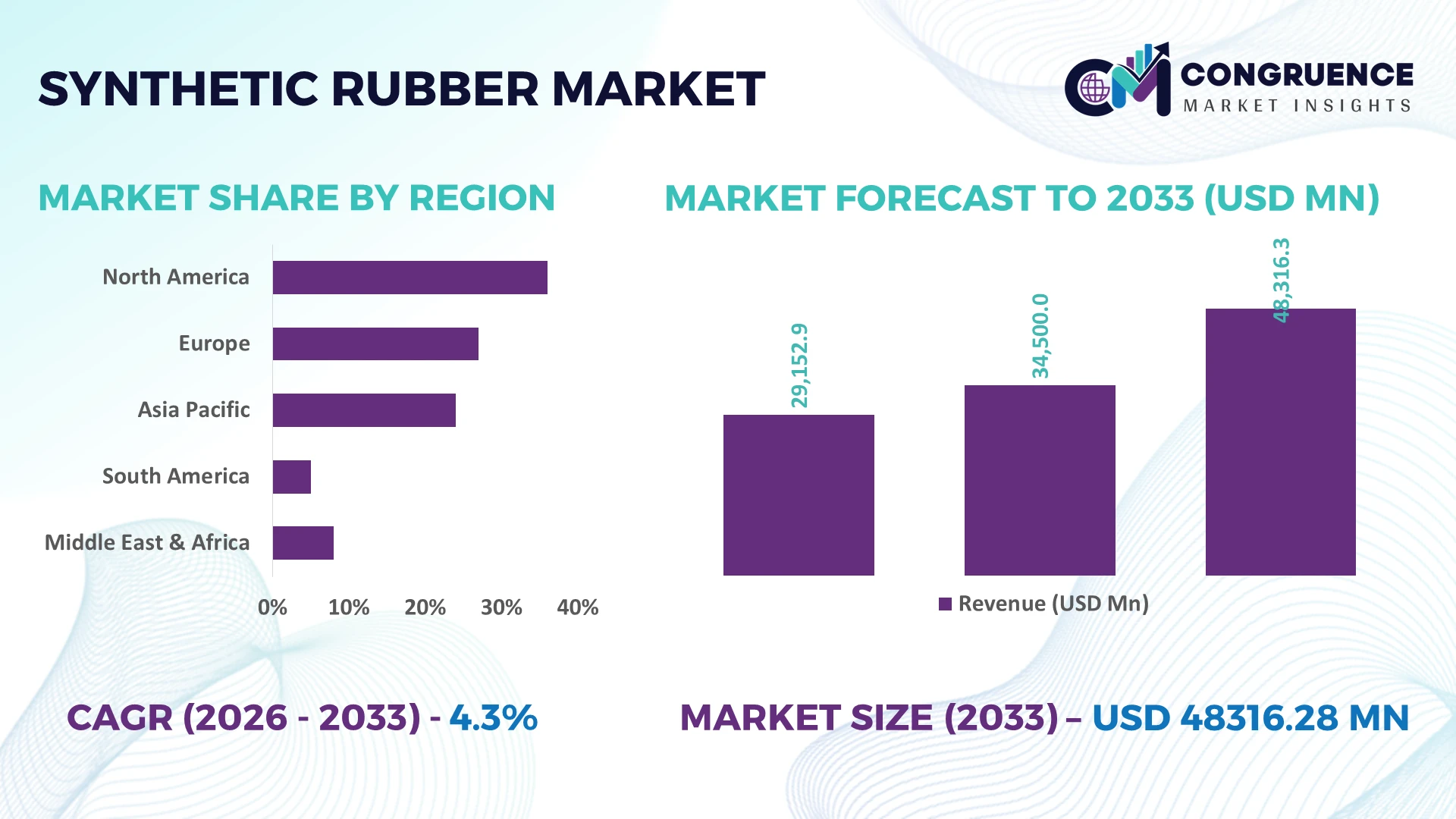

The Global Synthetic Rubber Market was valued at USD 34500 Million in 2025 and is anticipated to reach a value of USD 48316.28 Million by 2033 expanding at a CAGR of 4.3% between 2026 and 2033. Growth is driven by expanding electric vehicle tire production, rising high-performance industrial rubber applications, bio-based polymer innovation, and resilient regional manufacturing investments strengthening supply chain localization.

China remains the dominant country, accounting for approximately 38% of global synthetic rubber production capacity, supported by integrated petrochemical complexes, a tire manufacturing base exceeding 45% of global output, and sustained investments in advanced polymer technologies. Compared with India, where domestic capacity expansion continues at a faster pace, China benefits from larger feedstock integration despite ongoing supply-chain diversification following Red Sea shipping disruptions in 2026. This reinforces Asia-Pacific's leadership in global production and procurement strategies.

Strategic implication: Companies prioritizing localized production, feedstock security, and advanced elastomer development are positioned to strengthen long-term competitiveness across global industrial and automotive value chains.

Market Size & Growth: USD 34500 Million (2025) reaching USD 48316.28 Million by 2033 at 4.3% CAGR, supported by EV tire production and advanced elastomer manufacturing.

Top Growth Drivers: EV demand +18%, industrial automation +12%, sustainable material adoption +15% accelerate global market expansion.

Short-Term Forecast: By 2028, manufacturing efficiency improves 10% through digital process optimization and energy-efficient polymerization technologies.

Emerging Technologies: AI-driven quality control, automated production systems, and bio-based synthetic rubber improve consistency while reducing waste by 14%.

Regional Leaders: Asia-Pacific exceeds USD 24 billion, Europe surpasses USD 10 billion, North America approaches USD 9 billion, driven by localized manufacturing expansion.

Consumer/End-User Trends: More than 62% of premium tire production incorporates advanced synthetic rubber grades for durability and rolling resistance improvements.

Pilot/Case Example: 2025 modernization projects improved plant throughput by 16% while lowering production downtime through automated monitoring systems.

Competitive Landscape: Top manufacturers control nearly 48% market share, led by Arlanxeo, Kumho Petrochemical, Sinopec, Synthos, and TSRC Corporation.

Regulatory & ESG Impact: Lower-emission manufacturing initiatives reduce energy consumption by approximately 12% while supporting stricter industrial sustainability standards.

Investment & Funding: Over USD 4 billion supports capacity expansion, strategic partnerships, specialty elastomer development, and regional supply-chain resilience.

Innovation & Future Outlook: Next-generation bio-feedstocks, circular rubber recycling, and high-performance specialty elastomers strengthen long-term global competitiveness.

Demand continues to strengthen across automotive tires, industrial components, construction materials, and medical products as manufacturers prioritize durability and sustainable performance. Advanced catalyst technologies, bio-based formulations, and digital process controls are improving production consistency, with recycled material integration exceeding 12% in selected applications. Regional supply-chain diversification and evolving environmental compliance continue shaping strategic investments, setting the foundation for the market dynamics discussed below.

Synthetic rubber has become a strategic industrial material as automotive electrification, advanced manufacturing, and resilient supply-chain planning reshape global production priorities. Manufacturers are reducing dependence on single-source feedstocks through localized polymer production, while stricter environmental standards accelerate investment in cleaner processing technologies. This transition is strengthening competitive positioning for companies capable of balancing cost efficiency, material performance, and supply security across multiple end-use industries.

Digital manufacturing technologies are improving operational performance throughout synthetic rubber production. AI-enabled process control and predictive maintenance reduce unplanned downtime by approximately 18% while lowering energy consumption by nearly 10% compared with conventional plant operations. China continues to lead in production scale and integrated petrochemical infrastructure, whereas Japan emphasizes specialty elastomer innovation and premium-grade materials for high-performance automotive and electronics applications. Over the next two to three years, digital quality inspection is expected to exceed 55% adoption among newly upgraded production facilities, improving consistency and reducing manufacturing waste.

A practical example is the expansion of integrated synthetic rubber production alongside tire manufacturing clusters, allowing companies to shorten procurement cycles and improve feedstock availability. Leading producers are increasing investments in advanced elastomer technologies, regional manufacturing capacity, and strategic petrochemical partnerships to strengthen operational resilience. Companies that combine localized production with process innovation and sustainable material development will secure stronger competitive differentiation and long-term industrial relevance.

Electric vehicle production is reshaping synthetic rubber consumption by increasing demand for low rolling resistance tires, high-temperature sealing systems, and lightweight elastomer components. Premium tire manufacturers report performance improvements exceeding 15% through advanced solution styrene-butadiene rubber formulations, while automated production systems improve manufacturing efficiency by approximately 12%. China's continued investment in integrated petrochemical and tire manufacturing clusters strengthens feedstock availability despite global logistics realignment following recent maritime shipping disruptions. In response, manufacturers are expanding specialty elastomer capacity, investing in digital process optimization, and forming technology partnerships to supply higher-value automotive applications. The strategic advantage increasingly lies in vertically integrated operations that combine feedstock security with advanced material engineering.

Synthetic rubber producers continue to face structural pressure from fluctuating butadiene and styrene prices, with feedstock costs representing nearly 60% of total production expenses. Price swings exceeding 20% during procurement cycles create margin uncertainty and complicate long-term supply contracts. Japan and South Korea remain highly dependent on imported energy and petrochemical inputs, exposing manufacturers to logistics disruptions and geopolitical trade uncertainty. Companies are responding by diversifying sourcing networks, increasing regional storage capacity, and negotiating long-term procurement agreements while expanding recycled and alternative feedstock development. Operational resilience increasingly depends on procurement flexibility rather than production scale alone.

Commercial adoption of bio-based synthetic rubber and intelligent manufacturing platforms is creating new value across industrial supply chains. Advanced process automation improves production efficiency by approximately 14%, while digital quality analytics reduce material defects by nearly 16%. India is expanding specialty chemical manufacturing through production-linked industrial initiatives, encouraging investment in sustainable elastomer technologies and downstream processing. Companies are strengthening R&D partnerships, deploying AI-enabled production monitoring, and developing circular material ecosystems to serve premium automotive and industrial applications. A notable strategic opportunity lies in combining renewable feedstocks with digitally optimized manufacturing to improve sustainability without compromising product performance.

Expanding high-performance synthetic rubber production requires complex process integration, specialized technical expertise, and consistent quality control across multiple manufacturing sites. Premium elastomer production typically demands quality variation below 2%, while advanced automation projects often require workforce upskilling exceeding 30% of technical personnel. Germany's specialty manufacturing sector illustrates the challenge of balancing automation with strict product certification requirements. Companies must strengthen digital process control, expand technical training programs, and modernize manufacturing infrastructure while integrating real-time quality monitoring. Long-term competitiveness depends on scaling advanced production without sacrificing consistency, operational flexibility, or compliance with evolving industrial standards.

Digital Polymer Production Expands: Manufacturers are accelerating AI-enabled process optimization, with automated quality inspection improving production accuracy by 17% and predictive maintenance reducing equipment downtime by 15%. Rising labor costs and tighter environmental compliance requirements are driving plant modernization, particularly in China and Germany. Companies are integrating real-time process analytics with manufacturing execution systems, shortening production cycles while improving batch consistency and reducing operational waste across high-volume elastomer facilities.

Localized Supply Networks Strengthen: Feedstock procurement strategies are shifting toward regional integration, with localized sourcing improving delivery reliability by 20% and reducing logistics lead times by nearly 18%. Continued shipping disruptions and geopolitical trade adjustments are encouraging manufacturers to establish production closer to downstream tire and automotive facilities. Leading producers are restructuring supplier ecosystems, expanding storage infrastructure, and increasing long-term procurement agreements to improve operational continuity and reduce inventory risk.

Specialty Rubber Portfolio Diversifies: Demand for premium elastomers is increasing as high-performance automotive, electronics, and industrial applications require greater heat resistance and durability. Specialty product shipments have expanded by approximately 14%, while customized compound development has increased by nearly 16%. Japanese and South Korean manufacturers are scaling advanced formulation capabilities through collaborative development programs, enabling faster commercialization and stronger differentiation in technically demanding applications where performance outweighs commodity pricing.

Circular Material Integration Advances: Rubber recycling and circular manufacturing are becoming operational priorities, with recycled material utilization exceeding 12% in selected industrial applications and production waste declining by nearly 10% through closed-loop processing. Regulatory pressure and sustainability commitments are accelerating investment in devulcanization technologies and alternative feedstocks. A notable shift is the integration of recycled content into premium formulations rather than only commodity products, allowing companies to improve environmental performance without compromising material quality.

Styrene Butadiene Rubber (SBR) remains the leading segment because of its broad integration across tire manufacturing, balanced performance characteristics, and cost-efficient large-scale production. It accounts for approximately 42% of overall synthetic rubber demand, supported by consistent adoption in passenger and commercial vehicle tires. Polybutadiene Rubber (PBR) continues to hold a strong position for premium tire applications where abrasion resistance and durability are critical. Butyl Rubber retains strategic importance for inner liners and air-retention systems, while Nitrile Butadiene Rubber (NBR) supports industrial sealing applications requiring oil resistance.

EPDM Rubber is the fastest-growing segment as automotive electrification, construction modernization, and renewable energy infrastructure increase demand for weather-resistant sealing materials. Adoption of EPDM compounds has increased by nearly 15% in advanced automotive systems, while manufacturers continue expanding specialty elastomer production and investing in customized formulations. Companies are prioritizing high-value product portfolios, digital compound development, and collaborative innovation to improve margins while reducing exposure to commodity-grade competition.

Tires remain the dominant application, representing nearly 68% of synthetic rubber consumption due to continuous production across passenger vehicles, commercial fleets, and electric mobility platforms. Demand is reinforced by stricter efficiency standards requiring advanced elastomer compounds that improve rolling resistance and durability. Industrial Goods continue providing stable demand through conveyor systems, vibration control products, and engineered rubber components, while Footwear maintains consistent consumption through lightweight performance materials.

Automotive Components represent the fastest-growing application as vehicle electrification increases requirements for seals, bushings, hoses, and vibration-control systems. Adoption of advanced synthetic rubber compounds in automotive components has expanded by approximately 16%, while automated component manufacturing improves production efficiency by nearly 12%. Adhesives & Sealants are also gaining strategic relevance through construction modernization and industrial assembly applications. Manufacturers are expanding production capacity, optimizing compound formulations, and strengthening partnerships with automotive suppliers to support evolving product specifications.

Automotive remains the dominant end-user, accounting for approximately 58% of synthetic rubber demand through tire production, sealing systems, vibration-control components, and fluid-handling applications. Large-scale vehicle manufacturing and replacement tire demand sustain high procurement volumes, while Industrial buyers maintain consistent purchasing for machinery, mining equipment, and manufacturing infrastructure. Consumer Goods and Footwear continue benefiting from product durability requirements and expanding specialty material applications.

Construction is emerging as the fastest-growing end-user segment, supported by infrastructure modernization, commercial development, and energy-efficient building projects requiring advanced sealing and insulation materials. Demand from construction applications has increased by approximately 14%, while industrial-grade EPDM adoption has expanded by nearly 13% in building systems. Companies are responding through application-specific product customization, localized manufacturing, and strategic partnerships with construction material suppliers. Pricing strategies increasingly emphasize performance-based value rather than commodity competition, strengthening long-term customer relationships across industrial sectors.

Asia-Pacific accounted for the largest market share at 51.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 5.6% CAGR between 2026 and 2033.

Advanced Manufacturing and Supply Chain Localization

North America maintains a strong position through integrated petrochemical infrastructure, advanced tire manufacturing, and high adoption of specialty elastomers across automotive and industrial applications. The region contributes approximately 22% of global synthetic rubber production, supported by increasing investments in digital manufacturing and feedstock optimization. Manufacturers are expanding regional sourcing strategies to improve procurement resilience, while predictive process control is reducing production downtime by nearly 15%. Strategic partnerships between chemical producers and automotive suppliers are strengthening localized value chains and accelerating deployment of premium elastomer compounds for electric vehicle platforms.

United States Market Outlook: The United States leads the regional market through its extensive petrochemical industry, established tire manufacturing network, and continuous investment in advanced polymer technologies. More than 70% of North America's synthetic rubber production capacity is concentrated within the country, supported by Gulf Coast chemical infrastructure and integrated feedstock availability. Companies continue modernizing production facilities with automation, specialty compound development, and long-term supply agreements to improve manufacturing flexibility while supporting expanding automotive and industrial demand.

Sustainability Standards Accelerate Premium Elastomer Production

Europe continues strengthening its competitive position through sustainable manufacturing practices, specialty material innovation, and strict environmental compliance. The region represents approximately 19% of global market demand, with advanced automotive manufacturing driving consistent consumption of premium synthetic rubber grades. Digital production technologies and energy-efficient polymerization systems have lowered operational energy use by approximately 11%, while manufacturers increasingly prioritize circular material integration. Industrial collaboration between chemical producers and automotive suppliers continues supporting advanced product development for high-performance mobility and engineering applications.

Germany Market Outlook: Germany remains the region's strategic manufacturing hub because of its advanced automotive sector, specialty chemical expertise, and engineering capabilities. The country accounts for nearly one-third of Europe's premium elastomer production, supported by strong research collaboration and automated manufacturing infrastructure. Companies continue investing in specialty EPDM and high-performance rubber compounds while integrating digital quality monitoring systems that improve production consistency and strengthen export competitiveness across industrial and automotive applications.

Integrated Manufacturing Scale Strengthens Market Leadership

Asia-Pacific dominates global synthetic rubber production through extensive petrochemical integration, large-scale tire manufacturing, and competitive production economics. The region contributes more than 55% of worldwide manufacturing capacity while benefiting from expanding downstream automotive and industrial sectors. Capacity utilization across major production hubs consistently exceeds 85%, supported by continuous investment in advanced polymer processing and logistics infrastructure. Producers are expanding specialty elastomer portfolios and integrating automated manufacturing technologies to improve operational efficiency while strengthening export competitiveness across global supply chains.

China Market Outlook: China represents the largest national market, supported by integrated refining capacity, extensive petrochemical complexes, and the world's largest tire manufacturing industry. Approximately 38% of global synthetic rubber production capacity is located within China, enabling strong feedstock integration and cost efficiency. Domestic manufacturers continue expanding specialty rubber production, digital manufacturing capabilities, and environmentally efficient processing technologies while strengthening partnerships with automotive and industrial equipment manufacturers to support higher-value applications.

Industrial Expansion Supports Downstream Demand

South America continues developing its synthetic rubber industry through automotive manufacturing, mining operations, and industrial infrastructure investment. The region accounts for approximately 5% of global consumption, with demand increasingly supported by localized manufacturing and replacement tire production. Industrial modernization programs have improved manufacturing productivity by nearly 9%, although logistics infrastructure and feedstock dependence continue affecting operational efficiency. Companies are responding by expanding regional distribution networks, strengthening supplier relationships, and investing in localized compounding operations to improve responsiveness to industrial customers.

Brazil Market Outlook: Brazil dominates the regional market through its established automotive manufacturing sector, petrochemical production capabilities, and expanding industrial base. The country contributes more than 45% of South America's synthetic rubber demand, supported by domestic tire manufacturing and infrastructure development. Manufacturers continue increasing investments in localized production, operational automation, and downstream processing while strengthening supply-chain resilience through regional procurement partnerships and long-term industrial customer agreements.

Petrochemical Investments Drive Industrial Transformation

The Middle East & Africa market is strengthening through petrochemical expansion, industrial diversification, and downstream manufacturing development. The region contributes approximately 4% of global market demand while benefiting from competitively priced hydrocarbon feedstocks and increasing investment in value-added chemical production. New industrial projects have expanded polymer processing capability by nearly 12%, encouraging greater domestic utilization of petrochemical resources. Companies are prioritizing integrated manufacturing investments, export-oriented production strategies, and partnerships that strengthen regional processing capabilities while reducing dependence on imported finished materials.

Saudi Arabia Market Outlook: Saudi Arabia leads regional development through world-scale petrochemical infrastructure, integrated refining capacity, and national industrial diversification initiatives. The country continues expanding downstream chemical manufacturing while leveraging competitively available feedstocks to improve production efficiency. Recent investments in specialty polymer processing and industrial clusters have strengthened manufacturing capabilities, enabling domestic producers to increase value-added elastomer production and improve competitiveness across automotive, construction, and industrial supply chains.

Global leaders including Arlanxeo, Kumho Petrochemical, Synthos, TSRC Corporation, and Sinopec compete directly with regional manufacturers on production scale, specialty formulations, and feedstock integration, while independent compounders challenge through customized elastomer solutions. The top five players collectively control approximately 48% of global capacity, creating strong influence over pricing, technology investment, and long-term supply agreements. Competition increasingly depends on specialty product performance rather than commodity pricing, with advanced production automation improving manufacturing efficiency by nearly 15% and integrated supply chains reducing procurement costs by approximately 12%. Companies are expanding specialty elastomer facilities, forming automotive partnerships, investing in digital process control, and strengthening vertical integration to secure raw material availability. The competitive landscape is shifting toward technology-enabled manufacturing and feedstock security as consolidation increases among large chemical producers. High capital requirements, petrochemical integration, and product qualification cycles remain major entry barriers. Winning requires differentiated materials, resilient supply networks, rapid product commercialization, and consistent manufacturing quality.

Arlanxeo

Kumho Petrochemical

Sinopec

Synthos S.A.

TSRC Corporation

JSR Corporation

LG Chem

Zeon Corporation

Versalis S.p.A.

Sibur

Reliance Industries Limited

Lion Elastomers

Asahi Kasei Corporation

Digital manufacturing platforms, AI-enabled process optimization, and advanced catalyst systems are transforming synthetic rubber production by improving operational precision and reducing manufacturing variability. AI-assisted quality control lowers defect rates by approximately 18%, while predictive maintenance decreases unplanned equipment downtime by nearly 15%. More than 50% of newly modernized production facilities are deploying integrated manufacturing execution systems, allowing producers to optimize energy use, improve throughput, and strengthen production consistency across high-volume elastomer operations.

Emerging technologies are shifting development toward bio-based feedstocks, advanced polymer engineering, and circular recycling processes. Compared with conventional polymerization methods, next-generation catalyst technologies improve reaction efficiency by nearly 12% while reducing energy consumption by approximately 10%. Companies specializing in premium automotive, industrial sealing, and specialty elastomers benefit most because these technologies improve material durability, shorten development cycles, and support increasingly stringent environmental performance requirements without compromising product quality.

Between 2026 and 2028, intelligent digital twins, continuous process monitoring, and automated compound formulation will reshape production economics. Adoption of digital simulation platforms is expected to exceed 60% among leading manufacturers, enabling faster product qualification and more efficient plant utilization. Companies investing early in integrated digital manufacturing, specialty material innovation, and circular production technologies will strengthen supply resilience, accelerate commercialization, and establish sustainable competitive advantages in increasingly performance-driven synthetic rubber markets.

March 2024 – Kumho Petrochemical signed a strategic partnership with SK geo centric and Tongsuh Petrochemical to establish a bio-monomer supply chain for sustainable synthetic rubber production while expanding ISCC+ certified product coverage. The initiative supports lower-carbon raw materials and broadens environmentally certified elastomer portfolios. Source: European Rubber Journal

April 2024 – Arlanxeo broke ground on a new hydrogenated nitrile butadiene rubber (HNBR) plant in Changzhou, China, with a planned 5 kilotonnes per year nameplate capacity. The expansion strengthens regional supply for advanced mobility, industrial, and energy applications while reinforcing localized manufacturing capabilities. Source: European Rubber Journal

February 2026 – Arlanxeo officially inaugurated the first phase of its Changzhou HNBR facility, commissioned at 2,500 tonnes per year, with future plans to double capacity. The investment enhances supply reliability for new energy and mobility markets while expanding the company's China manufacturing footprint. Source: ICIS

February 2026 – Lotte Versalis Elastomers reported its first operating profit as demand strengthened for EV tire-grade solution styrene-butadiene rubber (SSBR), prompting additional capital support from Lotte Chemical. The turnaround reflects stronger specialty product competitiveness and improved operational performance in premium synthetic rubber markets. Source: ChosunBiz

The report provides comprehensive analysis of the global synthetic rubber industry across five major product types, five core application areas, and five primary end-user segments, delivering strategic evaluation of manufacturing trends, technology adoption, competitive positioning, and operational developments. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting production concentration, deployment patterns, supply-chain evolution, and industrial investment priorities. More than 50% of demand analysis focuses on automotive and tire-related value chains while also examining specialty elastomer applications.

The study evaluates manufacturing modernization, digital production technologies, advanced elastomer development, circular material initiatives, and feedstock optimization shaping industry competitiveness between 2026 and 2033. It delivers actionable intelligence on segment performance, country-level opportunities, enterprise expansion strategies, partnership activity, and innovation priorities, enabling stakeholders to strengthen investment planning, optimize market entry decisions, improve competitive positioning, and identify emerging high-value opportunities across established and niche synthetic rubber applications.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 34500 Million |

Market Revenue in 2033 | USD 48316.28 Million |

CAGR (2026 - 2033) | 4.3% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Arlanxeo, Kumho Petrochemical, Sinopec, Synthos S.A., TSRC Corporation, JSR Corporation, LG Chem, Zeon Corporation, Versalis S.p.A., Sibur, Reliance Industries Limited, Lion Elastomers, Asahi Kasei Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |