Reports

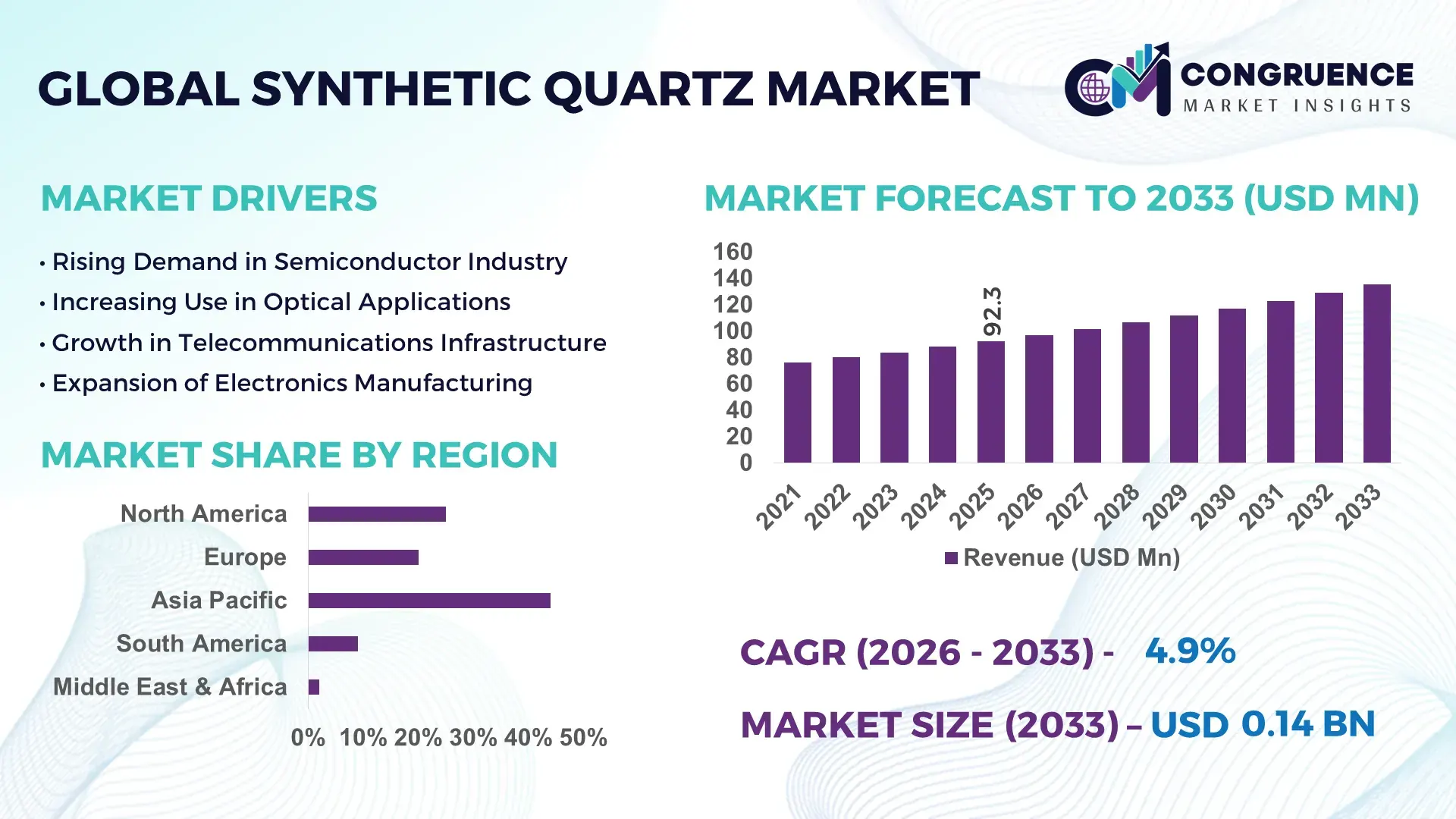

The Global Synthetic Quartz Market was valued at USD 92.3 Million in 2025 and is anticipated to reach a value of USD 135.33 Million by 2033 expanding at a CAGR of 4.9% between 2026 and 2033. Growth is primarily driven by increasing demand for high-purity quartz in semiconductor manufacturing and precision electronics applications.

Japan remains the dominant country in the synthetic quartz market, supported by advanced production capabilities and deep integration within the global semiconductor supply chain. The country produces over 35% of high-purity synthetic quartz components used in photolithography and wafer processing equipment. Japanese manufacturers have invested more than USD 500 million over the past five years in upgrading hydrothermal synthesis facilities and automation technologies. Synthetic quartz is extensively used in optical fibers, semiconductor crucibles, and piezoelectric devices, with over 60% of domestic consumption linked to electronics manufacturing. Technological advancements such as ultra-low defect density quartz and improved crystal growth rates exceeding 2.5 mm/day further strengthen the country’s industrial position.

Market Size & Growth: USD 92.3 Million (2025) to USD 135.33 Million (2033), CAGR 4.9%, driven by rising semiconductor fabrication demand.

Top Growth Drivers: Semiconductor demand growth 35%, optical fiber deployment 28%, high-frequency electronics adoption 22%.

Short-Term Forecast: By 2028, production efficiency is expected to improve by 18% through automation and AI-based process control.

Emerging Technologies: Hydrothermal crystal growth optimization, AI-driven defect detection, advanced quartz purification techniques.

Regional Leaders: Asia-Pacific projected USD 62 Million by 2033 with strong semiconductor demand; North America USD 32 Million driven by aerospace electronics; Europe USD 26 Million with precision optics expansion.

Consumer/End-User Trends: Semiconductor manufacturers account for over 50% of usage, followed by telecommunications and industrial optics sectors.

Pilot or Case Example: In 2024, a Japanese facility improved crystal yield by 20% using AI-based monitoring systems.

Competitive Landscape: Market leader holds approximately 30% share, with key players including Shin-Etsu Chemical, Heraeus Holding, Tosoh Corporation, Momentive Technologies, and Ohara Inc.

Regulatory & ESG Impact: Strict environmental standards are pushing adoption of energy-efficient furnaces reducing emissions by 15%.

Investment & Funding Patterns: Over USD 1.2 Billion invested globally in quartz processing and semiconductor-grade material expansion.

Innovation & Future Outlook: Integration with next-generation chip manufacturing and quantum computing applications is shaping long-term demand.

The synthetic quartz market is influenced by key sectors such as semiconductors contributing nearly 52% of demand, telecommunications around 25%, and optical instrumentation approximately 15%. Recent innovations include ultra-high purity quartz with impurity levels below 1 ppm and improved thermal stability for high-temperature applications. Regulatory frameworks emphasizing sustainability have driven energy-efficient production methods, reducing operational emissions by up to 20%. Regional consumption is heavily concentrated in Asia-Pacific due to electronics manufacturing hubs, while North America shows strong growth in aerospace-grade applications. Emerging trends such as quantum computing components, 5G infrastructure, and advanced lithography systems are expected to further accelerate adoption, positioning synthetic quartz as a critical material in next-generation technology ecosystems.

The synthetic quartz market holds strong strategic relevance due to its indispensable role in semiconductor fabrication, optical communication systems, and precision instrumentation. As global chip production scales to meet rising demand for AI processors and advanced electronics, synthetic quartz components are becoming critical in ensuring high thermal stability and purity. Advanced hydrothermal synthesis technology delivers up to 25% improvement in crystal uniformity compared to conventional quartz melting techniques, significantly enhancing performance in photolithography processes.

Asia-Pacific dominates in production volume, while North America leads in adoption with over 65% of semiconductor enterprises integrating synthetic quartz in advanced chip manufacturing processes. The increasing shift toward smaller node sizes below 5 nm requires ultra-pure quartz materials with minimal defects, driving continuous innovation in purification and crystal growth technologies. By 2028, AI-driven manufacturing optimization is expected to reduce defect rates by nearly 30%, improving yield efficiency across fabrication facilities. From an ESG perspective, firms are committing to sustainability improvements such as 20% reduction in energy consumption by 2030 through adoption of energy-efficient furnaces and recycling of quartz waste materials. In 2025, a leading Japanese manufacturer achieved a 22% reduction in production defects through implementation of real-time AI monitoring and predictive maintenance systems.

The future pathways of the synthetic quartz market are closely tied to advancements in quantum computing, 5G infrastructure, and high-frequency electronics. With increasing regulatory focus on environmental compliance and supply chain resilience, the synthetic quartz market is emerging as a pillar of technological stability, operational efficiency, and sustainable industrial growth.

The rapid expansion of semiconductor manufacturing is a primary driver of the synthetic quartz market. Synthetic quartz is essential for wafer processing equipment, photomasks, and crucibles used in silicon crystal growth. Global semiconductor production volumes have increased by over 15% annually in recent years, directly impacting demand for high-purity quartz components. Advanced chip manufacturing processes require materials with impurity levels below 1 ppm and high thermal resistance exceeding 1,000°C. As fabrication facilities expand capacity, particularly in Asia-Pacific, the need for precision quartz components continues to grow. Furthermore, the transition to smaller process nodes and advanced lithography techniques has intensified reliance on defect-free quartz, pushing manufacturers to enhance production capabilities and invest in next-generation synthesis technologies.

The synthetic quartz market faces significant restraints due to high production costs and technically complex manufacturing processes. Hydrothermal synthesis requires controlled high-pressure and high-temperature environments, often exceeding 350°C and 1,000 bar pressure, leading to substantial energy consumption. Equipment costs for crystal growth chambers and purification systems can exceed millions of dollars per facility. Additionally, maintaining ultra-high purity standards demands advanced filtration and contamination control measures, increasing operational expenses. These factors limit entry for new manufacturers and restrict production scalability. Supply chain dependencies for raw silica and specialized chemicals further add to cost pressures. As a result, smaller firms face challenges in competing with established players that benefit from economies of scale and technological expertise.

Advancements in optical communication and telecommunications technologies present significant opportunities for the synthetic quartz market. The deployment of 5G networks and expansion of fiber-optic infrastructure have increased demand for high-quality quartz materials used in optical fibers and signal transmission systems. Global fiber-optic cable installations are growing at over 20% annually, creating substantial demand for synthetic quartz preforms. Additionally, emerging technologies such as quantum communication and photonic computing require ultra-pure quartz components with exceptional optical clarity and minimal signal distortion. Innovations in manufacturing processes, including AI-driven quality control and automated crystal growth, are improving yield rates and reducing defects, making high-performance quartz more accessible. These developments open new avenues for market expansion across telecommunications, defense, and advanced computing sectors.

The synthetic quartz market faces ongoing challenges related to supply chain disruptions and stringent quality requirements. Production relies heavily on high-purity silica and specialized equipment, both of which are subject to global supply fluctuations. Any disruption in raw material supply can delay production cycles and increase costs. Moreover, maintaining strict quality standards is critical, as even minor impurities or defects can compromise performance in semiconductor and optical applications. Quality assurance processes often involve multiple inspection stages, including X-ray analysis and optical testing, increasing production time and costs. Regulatory compliance related to environmental and safety standards also adds complexity to manufacturing operations. These challenges require continuous investment in supply chain resilience, advanced quality control technologies, and process optimization strategies.

• Increasing Semiconductor Node Miniaturization Driving Material Precision: The shift toward advanced semiconductor nodes below 5 nm has significantly increased demand for ultra-high purity synthetic quartz. Over 70% of next-generation chip fabrication facilities now require quartz components with impurity levels below 1 ppm and thermal resistance exceeding 1,100°C. Precision polishing technologies have improved surface uniformity by nearly 25%, enabling higher wafer yields. This trend is particularly evident in Asia-Pacific, where more than 60% of semiconductor fabs have upgraded quartz components to meet stringent process requirements.

• Expansion of Fiber-Optic Infrastructure Supporting Optical Quartz Demand: The rapid rollout of global fiber-optic networks has driven synthetic quartz usage in telecommunications. Fiber deployments have grown by over 20% annually, with nearly 65% of new installations utilizing high-purity quartz preforms for low signal attenuation. Optical transmission efficiency has improved by approximately 18% due to advancements in quartz clarity and structural integrity. North America and Europe collectively account for over 45% of high-performance optical fiber adoption, reinforcing the role of synthetic quartz in digital infrastructure expansion.

• Integration of AI-Based Quality Control Enhancing Manufacturing Efficiency: The adoption of AI-driven inspection systems has transformed synthetic quartz production processes. Automated defect detection systems have reduced material rejection rates by nearly 30%, while improving crystal growth consistency by over 22%. More than 50% of leading manufacturers have implemented machine learning algorithms to monitor hydrothermal synthesis conditions in real time. This integration has shortened production cycles by approximately 15%, enabling higher throughput and improved cost efficiency in large-scale manufacturing operations.

• Rising Demand for High-Temperature Industrial Applications: Synthetic quartz is increasingly used in high-temperature industrial environments such as aerospace and advanced manufacturing. Demand for quartz components capable of withstanding temperatures above 1,200°C has increased by 28% in the past three years. Industrial furnaces and precision instruments now incorporate quartz materials with improved thermal shock resistance, enhancing operational lifespan by up to 20%. Europe has seen a 35% increase in adoption of quartz-based components in aerospace testing and advanced materials processing facilities.

The synthetic quartz market is segmented across types, applications, and end-user industries, each reflecting distinct demand patterns and technological requirements. Product types are primarily categorized into high-purity synthetic quartz crystals, quartz glass, and specialized engineered quartz components, with varying performance characteristics tailored for industrial applications. In terms of applications, semiconductor manufacturing dominates usage, followed by telecommunications, optical devices, and precision instrumentation. End-user segmentation highlights semiconductor fabrication plants, telecom infrastructure providers, and industrial manufacturing sectors as the primary consumers. Over 50% of demand is concentrated in electronics-related industries, driven by increasing miniaturization and performance requirements. Regional consumption patterns show strong alignment with industrial clusters, particularly in Asia-Pacific and North America, where technological infrastructure and manufacturing capabilities are well established.

The synthetic quartz market includes key product types such as synthetic quartz crystals, fused quartz (quartz glass), and engineered quartz components. Synthetic quartz crystals dominate the segment, accounting for approximately 48% of total adoption due to their extensive use in semiconductor wafers, oscillators, and piezoelectric devices. These crystals offer superior purity and structural consistency, making them indispensable for high-frequency and precision applications. Fused quartz holds around 32% share, widely utilized in optical fibers, laboratory equipment, and high-temperature industrial applications due to its excellent thermal stability and transparency.

Engineered quartz components represent the fastest-growing segment, expanding at an estimated CAGR of 6.2%, driven by increasing demand for customized, high-performance materials in aerospace and advanced manufacturing. These components are designed for specific industrial requirements, including enhanced durability and resistance to extreme conditions. Other niche types, including specialty coatings and composite quartz materials, collectively contribute around 20% of the market, serving specialized applications in research and high-end instrumentation.

Semiconductor manufacturing remains the leading application segment in the synthetic quartz market, accounting for approximately 52% of total usage. The material’s high purity and thermal resistance make it essential for wafer fabrication, photolithography equipment, and silicon crystal growth processes. Telecommunications applications, including fiber-optic cables and signal transmission systems, hold around 25% share, benefiting from the superior optical properties of synthetic quartz.

Optical and precision instrumentation represent the fastest-growing application segment, expanding at a CAGR of 5.8%, driven by advancements in photonics, medical imaging, and aerospace technologies. These applications require high-performance quartz materials with minimal defects and exceptional clarity. Other applications, including laboratory equipment and industrial heating systems, collectively contribute approximately 23% of the market, reflecting steady demand across diverse industrial sectors.

Semiconductor fabrication plants represent the leading end-user segment in the synthetic quartz market, accounting for nearly 50% of total demand. These facilities rely heavily on high-purity quartz components for wafer processing, ensuring consistent performance under extreme thermal and chemical conditions. Telecommunications providers account for approximately 27% of market usage, driven by large-scale fiber-optic network expansions and increasing demand for high-speed connectivity.

The aerospace and defense sector is the fastest-growing end-user segment, with an estimated CAGR of 6.5%, fueled by rising demand for high-temperature-resistant materials in advanced testing and manufacturing environments. Synthetic quartz is widely used in sensors, optical systems, and thermal shielding components within this sector. Other end-users, including research laboratories and industrial manufacturing firms, collectively contribute around 23% of the market, with adoption rates exceeding 40% in high-precision applications.

Region Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.6% between 2026 and 2033.

Asia-Pacific’s dominance is supported by over 65% of global semiconductor fabrication capacity concentrated in countries such as China, Japan, and South Korea. The region processes more than 70% of global silicon wafers, directly driving demand for high-purity synthetic quartz. North America, holding approximately 24% share, is witnessing accelerated investment in advanced chip manufacturing, with over 35 new fabrication facilities planned or under construction. Europe accounts for nearly 20% of the market, driven by precision optics and aerospace demand, while South America and the Middle East & Africa collectively contribute around 10%, with emerging industrial applications and infrastructure expansion supporting gradual adoption. Increasing regional investments in 5G infrastructure, quantum computing, and high-frequency electronics continue to shape demand patterns globally.

How is advanced semiconductor innovation accelerating demand for high-purity materials?

North America holds approximately 24% of the synthetic quartz market, driven primarily by strong demand from semiconductor manufacturing, aerospace, and telecommunications sectors. The United States accounts for over 80% of regional consumption, supported by increased investments in domestic chip production and advanced electronics. Government initiatives promoting semiconductor independence have resulted in more than 30% growth in fabrication infrastructure projects. Regulatory frameworks emphasize environmental compliance, with energy-efficient manufacturing technologies reducing emissions by nearly 18%. Technological advancements such as AI-driven quality control and automation are widely adopted, improving production efficiency by over 20%. A key regional player, Momentive Technologies, has expanded its high-purity quartz production capacity by nearly 25% to meet rising semiconductor demand. Consumer behavior reflects high enterprise adoption, particularly in healthcare, finance, and data center applications, where over 60% of organizations rely on advanced electronics infrastructure.

Why is sustainability-driven innovation shaping high-performance material demand?

Europe accounts for approximately 20% of the synthetic quartz market, with key contributions from Germany, the United Kingdom, and France. Germany leads regional consumption with over 35% share, supported by strong industrial manufacturing and precision engineering sectors. Regulatory bodies enforcing strict environmental standards have driven adoption of energy-efficient quartz production methods, reducing carbon emissions by up to 20%. The European Union’s sustainability initiatives have accelerated the shift toward recyclable materials and low-impact manufacturing processes. Advanced technologies such as photonics and precision optics are expanding rapidly, with adoption rates increasing by 22% across industrial applications. Heraeus Holding, a major regional player, has invested significantly in advanced quartz materials for optical and semiconductor applications, enhancing product performance and durability. Consumer behavior in Europe reflects a strong preference for environmentally compliant and high-precision materials, with over 55% of industrial users prioritizing sustainability certifications in procurement decisions.

What factors are driving large-scale production and consumption of precision materials?

Asia-Pacific dominates the synthetic quartz market in both volume and consumption, accounting for approximately 46% of global demand. China, Japan, and South Korea collectively contribute over 75% of regional consumption, driven by extensive semiconductor manufacturing and electronics production. China alone accounts for nearly 40% of regional demand, supported by large-scale industrial infrastructure and government-backed technology initiatives. The region hosts more than 60% of global semiconductor fabrication facilities, significantly boosting demand for high-purity quartz components. Technological innovation hubs in Japan and South Korea are advancing crystal growth techniques, improving production efficiency by nearly 25%. Shin-Etsu Chemical, a leading regional player, continues to invest in next-generation quartz materials for advanced chip manufacturing. Consumer behavior in this region is characterized by high adoption in electronics and telecommunications, with over 70% of demand linked to mobile devices, data centers, and digital infrastructure expansion.

How are infrastructure and energy developments influencing specialized material adoption?

South America represents approximately 6% of the synthetic quartz market, with Brazil and Argentina as key contributors. Brazil accounts for over 55% of regional demand, driven by expanding industrial manufacturing and energy sector investments. Infrastructure development projects have increased demand for high-temperature-resistant materials by nearly 18%, particularly in power generation and industrial processing facilities. Government policies supporting local manufacturing and import substitution have encouraged adoption of advanced materials, including synthetic quartz. The region is also witnessing growth in telecommunications infrastructure, with fiber-optic network expansion increasing by over 15% annually. Local manufacturers are gradually enhancing production capabilities, focusing on cost-effective quartz solutions for industrial use. Consumer behavior reflects demand linked to media, telecommunications, and industrial applications, with approximately 40% of usage concentrated in infrastructure-related projects.

What role do industrial diversification and modernization play in material demand?

The Middle East & Africa region holds around 4% of the synthetic quartz market, with key growth observed in the UAE and South Africa. Demand is primarily driven by oil and gas, construction, and emerging electronics manufacturing sectors. Industrial diversification initiatives have increased adoption of high-performance materials by approximately 20% in the past five years. Infrastructure modernization projects, including smart city developments, are contributing to rising demand for precision materials. Trade partnerships and government incentives aimed at boosting local manufacturing capabilities are supporting market growth. Technological modernization, including adoption of automated industrial systems, has improved efficiency by nearly 15%. Regional players are investing in advanced material processing to support industrial expansion. Consumer behavior varies, with demand largely tied to construction, energy, and industrial development, accounting for over 60% of regional usage.

Japan – 32% share in the Synthetic Quartz market, driven by advanced production capacity and high adoption in semiconductor manufacturing.

China – 28% share in the Synthetic Quartz market, supported by large-scale electronics production and strong industrial infrastructure.

The synthetic quartz market exhibits a moderately consolidated structure, with the top five companies collectively accounting for approximately 58% of global market share. The competitive environment is characterized by strong technological capabilities, high entry barriers, and significant capital investment requirements. Over 25 active global competitors operate in this market, ranging from established multinational corporations to specialized material manufacturers. Leading companies are focusing on strategic initiatives such as capacity expansion, product innovation, and long-term supply agreements with semiconductor manufacturers.

Innovation plays a central role in competition, with more than 40% of market players investing in advanced crystal growth technologies and AI-driven quality control systems. Partnerships between quartz manufacturers and semiconductor firms have increased by nearly 30% in recent years, enabling co-development of customized high-performance materials. Mergers and acquisitions have also gained traction, with at least five notable consolidation deals completed in the past three years to strengthen market positioning and expand geographic reach.

The market is also witnessing increased competition in sustainability, with over 50% of leading companies implementing energy-efficient production methods to reduce emissions and operational costs. Continuous advancements in ultra-high purity quartz and defect-free crystal production are further intensifying competition, as companies strive to meet the evolving requirements of next-generation electronics and optical applications.

Shin-Etsu Chemical Co., Ltd.

Heraeus Holding GmbH

Tosoh Corporation

Momentive Technologies

Ohara Inc.

Saint-Gobain Quartz

Kyocera Corporation

Corning Incorporated

Murata Manufacturing Co., Ltd.

Nikon Corporation

Technological advancements in the synthetic quartz market are primarily centered around improving purity levels, crystal growth efficiency, and defect minimization to meet the stringent requirements of semiconductor and optical industries. Hydrothermal synthesis remains the dominant production method, with recent innovations enabling crystal growth rates exceeding 3 mm/day while maintaining impurity levels below 0.5 ppm. These improvements have enhanced material consistency by nearly 20%, making synthetic quartz more reliable for advanced photolithography and wafer processing applications.

Automation and digitalization are transforming manufacturing processes, with over 55% of leading producers integrating AI-driven monitoring systems into crystal growth chambers. These systems enable real-time adjustments in pressure and temperature, reducing defect rates by approximately 30% and improving overall yield efficiency by more than 22%. Advanced spectroscopy and X-ray diffraction technologies are also being used to detect micro-level imperfections, ensuring compliance with ultra-high purity standards required for sub-5 nm semiconductor nodes.

Emerging technologies such as plasma-based purification and laser-assisted crystal shaping are gaining traction, improving surface precision by up to 25% and enhancing thermal resistance beyond 1,200°C. Additive manufacturing techniques are being explored for producing complex quartz components, with early-stage trials indicating a 15% reduction in material waste. Additionally, the integration of IoT-enabled sensors in production facilities has improved predictive maintenance capabilities, reducing equipment downtime by nearly 18%.

Innovation is also focused on sustainability, with energy-efficient furnaces reducing power consumption by approximately 20% and recycling technologies recovering up to 35% of quartz waste materials. These technological developments are positioning synthetic quartz as a critical material in next-generation electronics, telecommunications infrastructure, and high-performance industrial applications.

• In March 2025, Shin-Etsu Chemical announced the expansion of its quartz products manufacturing capacity in Japan to support rising semiconductor demand. The company increased production capabilities for high-purity quartz components used in lithography and wafer processing equipment, strengthening supply reliability for advanced chip fabrication facilities. Source: www.shinetsu.co.jp

• In September 2024, Heraeus Holding expanded its portfolio of high-purity fused quartz materials designed for semiconductor and optical applications. The development focused on improving thermal stability and reducing impurity levels, enabling enhanced performance in extreme-temperature environments and advanced photonics systems. Source: www.heraeus.com

• In July 2024, Momentive Technologies introduced a new range of ultra-high purity quartz materials engineered for next-generation semiconductor manufacturing. These materials demonstrated improved resistance to thermal shock and extended operational lifespan in high-temperature processing environments. Source: www.momentivetech.com

• In January 2025, Tosoh Corporation upgraded its production facilities to incorporate advanced automation and quality control technologies for synthetic quartz manufacturing. The initiative improved production efficiency by over 15% and reduced defect rates, supporting the growing demand for precision materials in semiconductor and electronics industries. Source: www.tosoh.com

The Synthetic Quartz Market Report provides a comprehensive analysis of the global industry, covering a wide range of segments, technologies, and geographic regions to support strategic decision-making. The report evaluates key product categories, including synthetic quartz crystals, fused quartz, and engineered quartz components, collectively accounting for over 90% of industrial usage. It further analyzes application areas such as semiconductor manufacturing, telecommunications, optical systems, and industrial processing, with electronics-related applications contributing more than 50% of total demand. Geographically, the report spans major regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, with detailed insights into country-level consumption patterns across over 15 key markets. Asia-Pacific alone represents nearly half of global demand, driven by extensive semiconductor fabrication capacity and electronics production hubs. The report also highlights emerging markets where infrastructure development and digital transformation are accelerating adoption of high-performance materials.

From a technological perspective, the report examines advancements in hydrothermal synthesis, AI-driven manufacturing, plasma purification, and laser-assisted processing, which collectively improve material efficiency and production scalability by up to 25%. It also explores sustainability trends, including energy-efficient production methods and recycling initiatives that reduce waste by approximately 30%. Additionally, the report includes analysis of end-user industries such as semiconductor fabs, telecom providers, aerospace manufacturers, and research institutions, offering insights into adoption rates exceeding 40% in high-precision applications. The scope further extends to niche segments such as quantum computing materials and advanced photonics, ensuring a forward-looking perspective on industry evolution.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Shin-Etsu Chemical Co., Ltd., Heraeus Holding GmbH, Tosoh Corporation, Momentive Technologies, Ohara Inc., Saint-Gobain Quartz, Kyocera Corporation, Corning Incorporated, Murata Manufacturing Co., Ltd., Nikon Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |