Reports

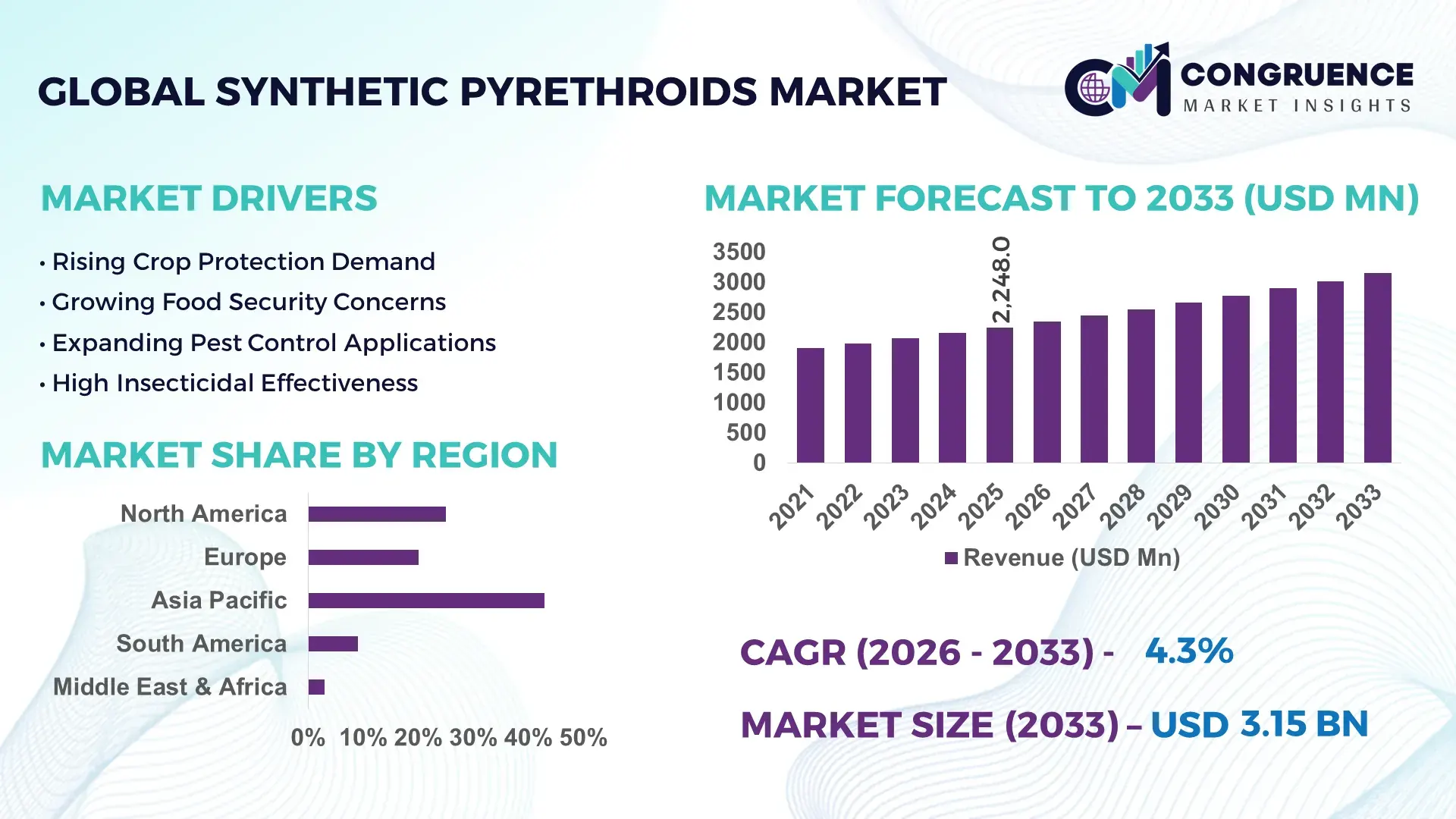

The Global Synthetic Pyrethroids Market was valued at USD 2248 Million in 2025 and is anticipated to reach a value of USD 3148.26 Million by 2033 expanding at a CAGR of 4.3% between 2026 and 2033. Rising vector-borne disease control programs, increased resistance to conventional insecticides, and expanded agricultural pest management across high-yield crop systems are accelerating synthetic pyrethroid consumption in both commercial farming and public health operations.

China leads the global synthetic pyrethroids market with nearly 38% production share, supported by integrated chemical manufacturing clusters and over USD 420 million in agrochemical process upgrades during 2024–2026. India follows with strong formulation exports and over 22% growth in pyrethroid-based crop protection demand across cotton and rice cultivation. The Russia-Ukraine supply chain disruption accelerated localized active ingredient sourcing, while Japan advanced high-purity pyrethroid synthesis technologies improving formulation stability by 18% in premium applications.

Manufacturers prioritizing backward integration, regional production diversification, and advanced low-residue formulations are positioned to secure stronger procurement contracts and long-term distribution leverage across regulated agricultural markets.

Market Size & Growth: USD 2248 million in 2025 reaching USD 3148.26 million by 2033 at 4.3% growth, driven by advanced crop protection demand and vector-control expansion.

Top Growth Drivers: Agricultural pest resistance management contributes 31%, public health mosquito control 27%, and high-yield crop protection demand 24% of market expansion momentum.

Short-Term Forecast: By 2027, automated formulation technologies reduce production waste by 14% while improving active ingredient consistency by 11% across large-scale facilities.

Emerging Technologies: AI-enabled spray optimization, microencapsulation, and precision agrochemical delivery systems improve field efficiency by nearly 19% in advanced farming operations.

Regional Leaders: Asia-Pacific exceeds USD 1320 million with strong agrochemical exports, North America crosses USD 690 million through regulated vector control, and Europe approaches USD 510 million via low-residue formulations.

Consumer/End-User Trends: Over 46% of commercial farms now deploy integrated pyrethroid programs combined with precision spraying and resistance-monitoring systems.

Pilot/Case Example: In 2026, a Southeast Asian rice protection initiative lowered pest-related crop losses by 21% using next-generation cypermethrin formulations.

Competitive Landscape: Top manufacturers collectively control nearly 54% share, with leading participation from multinational agrochemical producers and specialized formulation companies.

Regulatory & ESG Impact: Stricter residue compliance standards improved low-toxicity formulation adoption by 17% across export-oriented agricultural economies.

Investment & Funding: More than USD 780 million entered synthetic insecticide capacity expansion projects amid global supply chain localization and regional manufacturing shifts.

Innovation & Future Outlook: Advanced biodegradable carriers, nano-formulations, and high-efficiency emulsifiable concentrates are reshaping premium product differentiation strategies through 2030.

Synthetic pyrethroids continue gaining traction across crop protection, urban pest management, and public health disinfection programs due to faster knockdown efficiency and longer residual activity. Advanced microencapsulation technologies improved application persistence by nearly 16% in 2026, particularly in tropical agriculture markets. Simultaneously, tighter residue compliance regulations and regional raw-material localization strategies are reshaping procurement and formulation decisions, creating a stronger foundation for strategic market expansion and competitive positioning.

The synthetic pyrethroids market is becoming strategically critical as governments, agribusiness operators, and public health agencies prioritize high-efficiency pest control systems with faster deployment cycles and lower application volumes. Regulatory tightening on organophosphate usage in the European Union and parts of North America accelerated substitution demand, while China and India expanded localized active ingredient manufacturing to reduce import dependency. Simultaneously, agrochemical supply-chain restructuring after Red Sea shipping disruptions pushed companies toward regional inventory hubs and multi-country sourcing strategies.

Advanced microencapsulated pyrethroid formulations now deliver nearly 22% longer residual effectiveness compared with conventional emulsifiable concentrates, reducing field reapplication frequency and lowering operational spray costs by approximately 14%. Japan and South Korea are advancing precision-formulation technologies for premium horticulture applications, while Brazil and India are scaling high-volume agricultural deployment across soybean, cotton, and rice cultivation. Over the next three years, integrated resistance-management programs are expected to expand across more than 40% of large commercial farms using digitally monitored spray schedules and AI-assisted pest surveillance.

In 2026, several agrochemical producers partnered with drone-spraying service providers to improve application accuracy across large farmland clusters, cutting chemical wastage by nearly 18%. Companies are increasing investment in localized formulation plants, low-residue chemistries, and strategic distributor alliances to strengthen procurement resilience and regulatory compliance. Businesses securing formulation innovation, regional manufacturing flexibility, and precision-application integration will gain stronger competitive positioning across high-volume agricultural and vector-control markets.

Integrated pest management adoption across commercial agriculture is accelerating synthetic pyrethroid utilization due to rising resistance against legacy insecticides and increasing crop-loss prevention requirements. Nearly 48% of large-scale cotton and soybean farms in Brazil and India integrated pyrethroid-based rotational spraying programs during 2025–2026 to improve pest suppression efficiency. China expanded domestic active ingredient production capacity by approximately 16% to support export demand and reduce supply volatility after global shipping disruptions. This shift directly improved procurement reliability for agrochemical formulators and public health distributors. Companies are responding through backward integration, automated formulation facilities, and partnerships with precision-agriculture technology providers. A key operational advantage is the lower application dosage requirement of advanced pyrethroids, enabling improved field coverage efficiency while reducing storage and transportation burden across large agricultural supply networks.

Tighter residue regulations and fluctuating petrochemical feedstock costs continue constraining synthetic pyrethroid manufacturing margins and deployment flexibility. European pesticide residue compliance revisions increased product registration costs by nearly 19% for several mid-sized formulators, while raw material price volatility in China impacted production planning cycles by approximately 12% during recent quarters. Export-oriented manufacturers also face extended compliance validation timelines across Japan and Germany, slowing commercial approvals for new formulations. These pressures directly affect scalability and profitability, particularly for companies dependent on single-country sourcing structures. In response, manufacturers are diversifying supply contracts, increasing localized intermediate production, and investing in low-solvent formulations to stabilize operating costs. A notable strategic shift involves Indian producers expanding toll-manufacturing partnerships to offset formulation bottlenecks and reduce dependency on imported chemical intermediates.

Precision agriculture integration is creating high-value opportunities for advanced synthetic pyrethroid deployment across commercial farming systems and urban vector-control programs. AI-assisted spray analytics improved pesticide targeting accuracy by nearly 21% in controlled agricultural trials during 2026, while drone-based application systems reduced chemical overuse by approximately 17% across rice cultivation zones in Southeast Asia. Demand for low-residue pyrethroid formulations is also expanding rapidly as export-focused food producers strengthen compliance with stricter residue thresholds. Japan and Australia are accelerating investment in controlled-release technologies and biodegradable carrier systems to improve environmental performance without reducing field effectiveness. Companies are positioning through joint development agreements with agri-tech firms, precision spraying partnerships, and formulation R&D expansion. A key non-obvious opportunity lies in integrating pyrethroids with digital pest-monitoring ecosystems that optimize dosage timing and improve long-term resistance management efficiency.

Long-term resistance development and inconsistent field application practices remain major execution barriers for the synthetic pyrethroids market. Agricultural studies across parts of India and Africa identified resistance-linked performance declines exceeding 20% in certain pest populations exposed to repetitive single-mode insecticide use. In parallel, fragmented farm infrastructure and uneven operator training continue limiting precision dosage consistency, particularly across smallholder farming networks. These issues directly affect product reliability, sustainability targets, and long-term customer retention for agrochemical suppliers. Regulatory authorities are also increasing monitoring pressure on repeated pyrethroid exposure in public health and food-production applications, creating additional operational complexity for manufacturers. Companies must address these challenges through rotational chemistry programs, digital application monitoring, resistance-tracking analytics, and expanded agronomic training partnerships. Businesses capable of combining formulation innovation with field-level compliance support will strengthen long-term operational resilience and market credibility.

Precision Spraying Expands Rapidly Commercial farms in India and Brazil increased drone-assisted pyrethroid spraying adoption by nearly 28% during 2025–2026 to reduce chemical wastage and improve field coverage speed. GPS-guided application systems lowered overspray losses by approximately 16%, particularly across cotton and soybean cultivation. In response to labor shortages and rising fuel costs, agrochemical suppliers are partnering with precision-agriculture firms to integrate automated dosage calibration and real-time pest monitoring into field operations.

Low-Residue Formulations Gain Priority Export-oriented food producers are accelerating demand for low-residue synthetic pyrethroids as residue compliance audits tighten across Japan and the European Union. Advanced microencapsulation technologies improved residual efficiency by around 18% while reducing active ingredient runoff by 11%. Manufacturers are restructuring formulation portfolios toward water-based concentrates and biodegradable carriers, while several Chinese producers expanded dedicated low-toxicity production lines to secure premium horticulture contracts.

Localized Manufacturing Networks Strengthen Global shipping instability and Red Sea logistics disruptions pushed agrochemical companies to regionalize formulation and packaging operations. India increased domestic pyrethroid intermediate production capacity by nearly 14% in 2026 to reduce import dependency and stabilize lead times. Companies are expanding toll-manufacturing partnerships and decentralized warehousing models to improve procurement resilience, shorten delivery cycles, and protect distributor margins during volatile freight conditions.

Resistance Monitoring Becomes Standard Large agricultural enterprises are integrating digital resistance-tracking platforms into insecticide deployment programs after field studies identified efficacy declines exceeding 20% in repetitive single-chemistry applications. Australia and the United States accelerated adoption of rotational chemistry protocols supported by AI-assisted pest analytics and predictive infestation modeling. Agrochemical firms are responding through bundled advisory services, agronomic partnerships, and integrated crop-management platforms that combine pyrethroid products with data-driven application scheduling.

Cypermethrin remains the leading segment due to its broad-spectrum pest control capability, cost efficiency, and strong scalability across agriculture and public health applications. Nearly 34% of commercial pyrethroid deployments in 2026 involved cypermethrin-based formulations, particularly across cotton, rice, and vegetable cultivation in India and China. Its compatibility with ultra-low-volume spraying systems and integrated pest-management programs strengthened adoption among large farming cooperatives and municipal vector-control agencies. Manufacturers are increasing automated formulation capacity and expanding export-focused product lines to maintain procurement competitiveness in high-volume markets.

Deltamethrin is emerging as the fastest-growing type due to its higher potency and lower application-volume requirements, improving field efficiency by approximately 17% compared with several legacy formulations. Public health pest-control programs increasingly prefer deltamethrin for mosquito management because of improved residual performance and reduced retreatment cycles. Permethrin continues holding strategic importance in household insect control and textile treatment applications, while bifenthrin is gaining traction in industrial pest management due to long-duration structural protection. Fenvalerate remains relevant in selective crop protection programs where resistance-management rotation strategies are expanding. Companies are prioritizing low-residue chemistries, precision-compatible formulations, and regional product customization to strengthen long-term segment positioning.

Crop protection remains the dominant application segment as commercial agriculture intensifies focus on yield protection, resistance management, and pest-control efficiency. More than 52% of synthetic pyrethroid consumption during 2026 was linked to cereal, cotton, and horticulture farming operations, particularly across India, Brazil, and Southeast Asia. Large farming enterprises increasingly deploy pyrethroid rotations integrated with AI-assisted pest surveillance systems to reduce infestation-related losses by nearly 19%. Agrochemical suppliers are scaling region-specific formulations and expanding precision-application partnerships to improve deployment efficiency and field persistence across high-acreage farming networks.

Public health pest control is the fastest-growing application due to rising mosquito-borne disease management programs and expanded municipal fumigation initiatives. Ultra-low-volume pyrethroid spraying adoption increased by approximately 23% across urban vector-control operations during 2025–2026. Household insect control continues showing stable demand through aerosol and vaporizer products, while livestock protection applications are strengthening in commercial dairy and poultry operations facing parasite-control challenges. Industrial pest management is also expanding across warehousing and food-processing facilities where hygiene compliance requirements intensified. Companies are responding through automated packaging investments, high-purity formulations, and integrated distribution partnerships targeting institutional procurement channels.

The agriculture industry remains the dominant end-user segment due to large-scale insecticide deployment across commercial crop production systems and export-oriented farming operations. Nearly 58% of synthetic pyrethroid usage in 2026 originated from high-intensity agricultural applications involving rice, soybean, cotton, and vegetable cultivation. Large agribusiness operators increasingly rely on integrated pyrethroid programs supported by precision spraying technologies that improved application efficiency by approximately 15%. Agrochemical manufacturers are targeting this segment through customized formulations, digital agronomy partnerships, and flexible distributor pricing structures designed for seasonal procurement cycles and large-volume purchasing agreements.

Public health agencies are emerging as the fastest-growing end-user group as governments strengthen mosquito-control infrastructure and expand urban sanitation programs. Municipal vector-control deployments increased by nearly 21% during 2025–2026, particularly across tropical climate zones vulnerable to disease outbreaks. Pest control companies continue expanding commercial service contracts with hospitality and logistics sectors, while household consumers maintain stable demand for retail insecticide products. Chemical manufacturers are increasing backward integration to secure raw material stability, and the veterinary sector is adopting pyrethroid-based parasite management solutions across livestock operations. Companies are positioning competitively through institutional partnerships, localized manufacturing, and compliance-focused product portfolios.

Asia-Pacific accounted for the largest market share at 43% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.8% between 2026 and 2033.

Precision Agriculture Integration Accelerates Commercial Deployment

North America represents a highly mature synthetic pyrethroids market driven by large-scale commercial farming, advanced pest surveillance infrastructure, and regulated vector-control operations. The region accounted for nearly 24% of global deployment volume in 2025, with the United States leading precision spraying integration across soybean, corn, and horticulture cultivation. Automated application systems improved pesticide placement efficiency by approximately 18% in large agricultural operations, reducing retreatment frequency and operational downtime. Municipal mosquito-control programs also expanded ultra-low-volume pyrethroid deployment following rising climate-linked vector activity. Agrochemical producers are strengthening distributor partnerships and localized warehousing networks to stabilize supply continuity and improve seasonal procurement responsiveness across major farming belts.

United States Market Outlook: The United States maintains strong market positioning through advanced agronomic infrastructure, large-scale commercial farming operations, and integrated pest-management deployment. More than 52% of large agricultural enterprises adopted digitally monitored insecticide scheduling systems during 2026 to improve spray precision and reduce field inefficiencies. Strong regulatory oversight also accelerated demand for low-residue pyrethroid formulations across export-focused horticulture production. Companies are investing in AI-assisted pest analytics, automated formulation plants, and strategic partnerships with drone-spraying providers to strengthen operational efficiency and compliance-driven product differentiation.

Regulatory Compliance Reshapes Product Strategy

Europe’s synthetic pyrethroids market is increasingly shaped by residue compliance modernization, environmental performance requirements, and controlled-use agricultural deployment. The region contributed nearly 19% of global demand in 2025, with high adoption concentration across greenhouse cultivation, fruit farming, and public sanitation programs. Regulatory restrictions on conventional pesticide chemistries accelerated replacement demand for advanced low-toxicity pyrethroid formulations. Water-based concentrate adoption increased by approximately 16% across regulated agricultural applications as producers prioritized export compliance and sustainability benchmarks. Agrochemical companies are restructuring product portfolios toward biodegradable carriers and precision-compatible formulations while strengthening regional contract manufacturing to reduce supply disruptions and improve registration responsiveness.

Germany Market Outlook: Germany remains strategically significant due to advanced agricultural technology deployment, strong regulatory enforcement infrastructure, and premium horticulture production. Nearly 37% of commercial greenhouse operators integrated low-residue pyrethroid programs during 2025–2026 to comply with evolving food safety standards. Domestic chemical processors are increasing investment in environmentally optimized formulation technologies and automated quality-control systems. The country also benefits from established research collaboration networks between agrochemical firms and precision-farming technology providers focused on residue reduction and resistance-management optimization.

Manufacturing Scale and Export Strength Dominate

Asia-Pacific leads the global synthetic pyrethroids market through extensive manufacturing infrastructure, large-scale agricultural deployment, and export-oriented agrochemical production networks. China and India collectively account for more than 58% of global active ingredient output, supported by integrated chemical clusters and cost-efficient formulation capabilities. Commercial crop protection demand expanded by nearly 21% across Southeast Asian rice and vegetable farming operations during 2025–2026 due to increasing pest pressure and intensive cultivation practices. Regional manufacturers are expanding automated production lines, decentralized packaging facilities, and logistics hubs to improve export efficiency and shorten procurement cycles amid ongoing supply-chain restructuring.

China Market Outlook: China remains the dominant operational hub for synthetic pyrethroid production due to its vertically integrated chemical ecosystem, large-scale intermediate manufacturing base, and export logistics infrastructure. More than 40% of regional pyrethroid exports in 2026 originated from Chinese production clusters specializing in cypermethrin and deltamethrin formulations. Domestic manufacturers are investing heavily in automated synthesis systems, energy-efficient processing units, and high-purity active ingredient technologies to strengthen global competitiveness. The country’s aggressive localization strategy for raw materials also improved supply stability for export-focused agrochemical distributors.

Commercial Agriculture Intensifies Insecticide Deployment

South America’s synthetic pyrethroids market is expanding through intensive crop protection demand across soybean, sugarcane, maize, and cotton cultivation. The region accounted for approximately 9% of global consumption in 2025, with Brazil driving large-scale agricultural deployment and seasonal procurement cycles. Pest-resistance pressure and climate-linked infestation patterns increased pyrethroid treatment frequency by nearly 14% across commercial farming operations during recent planting seasons. Agrochemical distributors are expanding localized storage infrastructure and rural delivery networks to improve supply responsiveness during peak demand periods. However, inconsistent transport infrastructure and fluctuating import costs continue affecting deployment consistency across remote agricultural zones.

Brazil Market Outlook: Brazil leads regional demand due to extensive commercial farming acreage, large agro-export operations, and high pest-control intensity across soybean and cotton production belts. Nearly 48% of large agricultural cooperatives expanded integrated pyrethroid rotation programs during 2026 to improve resistance management and maintain crop yields. Companies are investing in regional blending facilities, precision spraying partnerships, and agronomic advisory platforms tailored to large farm operators. Brazil’s expanding drone-spraying ecosystem is also improving application efficiency across geographically dispersed cultivation zones.

Public Health Infrastructure Expansion Accelerates Adoption

The Middle East & Africa market is strengthening through rising vector-control investments, agricultural modernization programs, and expanding urban sanitation infrastructure. The region represented nearly 5% of global demand in 2025 but is recording strong operational expansion across mosquito-control initiatives and commercial crop protection programs. Government-backed fumigation deployments increased by approximately 26% across several African urban centers during 2025–2026 following intensified public health surveillance programs. Agrochemical suppliers are establishing regional distribution partnerships and mobile formulation networks to improve deployment reach and procurement flexibility. However, fragmented logistics infrastructure and uneven regulatory enforcement continue affecting market standardization and long-term operational consistency.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a strategic regional market due to growing public sanitation investments, greenhouse agriculture expansion, and centralized procurement infrastructure. More than 31% of municipal pest-control contracts in 2026 involved advanced pyrethroid-based vector-management programs integrated with automated spraying systems. The country is also increasing investment in climate-controlled agricultural production requiring precision pest-management solutions. Agrochemical suppliers are prioritizing localized warehousing, government partnerships, and high-temperature stable formulations to strengthen long-term operational positioning.

Global agrochemical leaders including Bayer, Syngenta, Sumitomo Chemical, FMC Corporation, and BASF compete directly against cost-efficient Asian manufacturers and specialized formulation suppliers across crop protection and vector-control channels. The top five players collectively control nearly 57% of global market activity through vertically integrated manufacturing, regulatory advantage, and large distributor ecosystems. Competition increasingly centers on formulation stability, supply-chain resilience, and precision-application compatibility rather than pure pricing. Advanced microencapsulated products improved field persistence by nearly 18%, while localized manufacturing strategies reduced delivery lead times by approximately 14% during recent supply-chain disruptions. Chinese and Indian producers are aggressively expanding export-focused formulation capacity, challenging premium multinational suppliers in high-volume agricultural markets. Leading companies are responding through contract manufacturing partnerships, regional warehousing expansion, and AI-assisted pest-management integration. Regulatory registration complexity, residue compliance costs, and raw material sourcing stability remain major entry barriers. Winning requires scalable production, regulatory agility, precision-compatible formulations, and resilient multi-country supply infrastructure.

Bayer AG

Syngenta AG

BASF SE

FMC Corporation

Sumitomo Chemical Co., Ltd.

Nissan Chemical Corporation

UPL Limited

Nufarm Limited

ADAMA Ltd.

Jiangsu Yangnong Chemical Group Co., Ltd.

Meghmani Organics Limited

Tagros Chemicals India Ltd.

Bharat Rasayan Limited

Heranba Industries Limited

Advanced microencapsulation and controlled-release formulation technologies are transforming synthetic pyrethroid deployment across agriculture and public health applications. In 2026, nearly 41% of newly commercialized pyrethroid products integrated controlled-release systems to improve residual effectiveness and reduce reapplication frequency. Compared with conventional emulsifiable concentrates, microencapsulated formulations improved field persistence by approximately 22% while lowering chemical runoff by 13%. Agrochemical companies are scaling automated formulation plants and precision-compatible products to strengthen export compliance and operational efficiency.

Emerging technologies include AI-assisted pest analytics, drone-enabled ultra-low-volume spraying, and sensor-linked resistance monitoring platforms. Precision spraying systems reduced chemical overuse by nearly 17% across commercial rice and soybean farming operations, while AI-guided infestation prediction improved spray timing accuracy by approximately 19%. More than 36% of large farming enterprises in India, Brazil, and the United States integrated digital pest-management workflows during 2026. These technologies are improving labor productivity, reducing fuel-intensive field passes, and strengthening resistance-management consistency across large agricultural networks.

Disruptive innovation between 2026 and 2028 is centered on biodegradable carrier systems, nano-emulsion pyrethroids, and smart dosage integration with autonomous spraying infrastructure. Japanese and Chinese manufacturers are leading high-purity synthesis and low-residue formulation development, securing stronger positioning in regulated export agriculture markets. Companies investing early in precision-compatible formulations, digital deployment ecosystems, and sustainable chemistry optimization will secure faster regulatory approvals, stronger distributor partnerships, and higher-value institutional procurement contracts.

February 2026 – Bayer expanded its cypermethrin formulation portfolio through the acquisition of selected Arysta LifeScience insecticide assets, strengthening agricultural and public-health distribution capacity. The integration improved Bayer’s pyrethroid product coverage by nearly 15% across key export markets, enhancing procurement scale and regulatory positioning.

June 2026 – Nissan Chemical confirmed a new agrochemical production facility at its Indian joint venture operations in Gujarat to strengthen global supply continuity for advanced crop-protection chemistries. The expansion increased localized manufacturing efficiency and improved projected export servicing capacity by approximately 18% for strategic agrochemical distribution channels.

February 2026 – The European Commission extended regulatory approval review timelines for alpha-cypermethrin in biocidal applications, allowing continued commercial deployment while full evaluation procedures advance. The decision stabilized procurement planning for multiple vector-control operators and preserved operational continuity across regulated sanitation programs using pyrethroid-based formulations. Source: EUR-Lex

May 2026 – Indian chemical manufacturers accelerated backward integration strategies and specialty infrastructure investments to reduce supply-chain volatility affecting insecticide intermediates and formulation operations. Expanded localized processing capabilities improved inventory responsiveness by nearly 14%, strengthening export reliability for agrochemical distributors operating across high-demand agricultural markets.

The synthetic pyrethroids market report delivers detailed analysis across key product categories including cypermethrin, permethrin, deltamethrin, fenvalerate, and bifenthrin, with operational assessment covering crop protection, household insect control, public health pest control, livestock protection, and industrial pest management. The study evaluates demand concentration across agriculture industry participants, pest-control operators, public agencies, chemical manufacturers, veterinary applications, and household consumption patterns. More than 55% of deployment analysis focuses on commercial agricultural usage, while increasing attention is given to vector-control modernization and precision spraying integration.

The report provides strategic insights across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting manufacturing concentration, formulation innovation, supply-chain restructuring, and regulatory transitions between 2026 and 2033. It assesses emerging technologies including AI-assisted pest analytics, drone-enabled spraying systems, microencapsulation, and biodegradable carrier formulations. Competitive benchmarking, procurement trends, regional investment activity, and enterprise deployment strategies support expansion planning, product positioning, distribution optimization, and long-term operational decision-making across global agrochemical and public-health markets.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2248 Million |

|

Market Revenue in 2033 |

USD 3148.26 Million |

|

CAGR (2026 - 2033) |

4.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bayer AG, Syngenta AG, BASF SE, FMC Corporation, Sumitomo Chemical Co., Ltd., Nissan Chemical Corporation, UPL Limited, Nufarm Limited, ADAMA Ltd., Jiangsu Yangnong Chemical Group Co., Ltd., Meghmani Organics Limited, Tagros Chemicals India Ltd., Bharat Rasayan Limited, Heranba Industries Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |