Reports

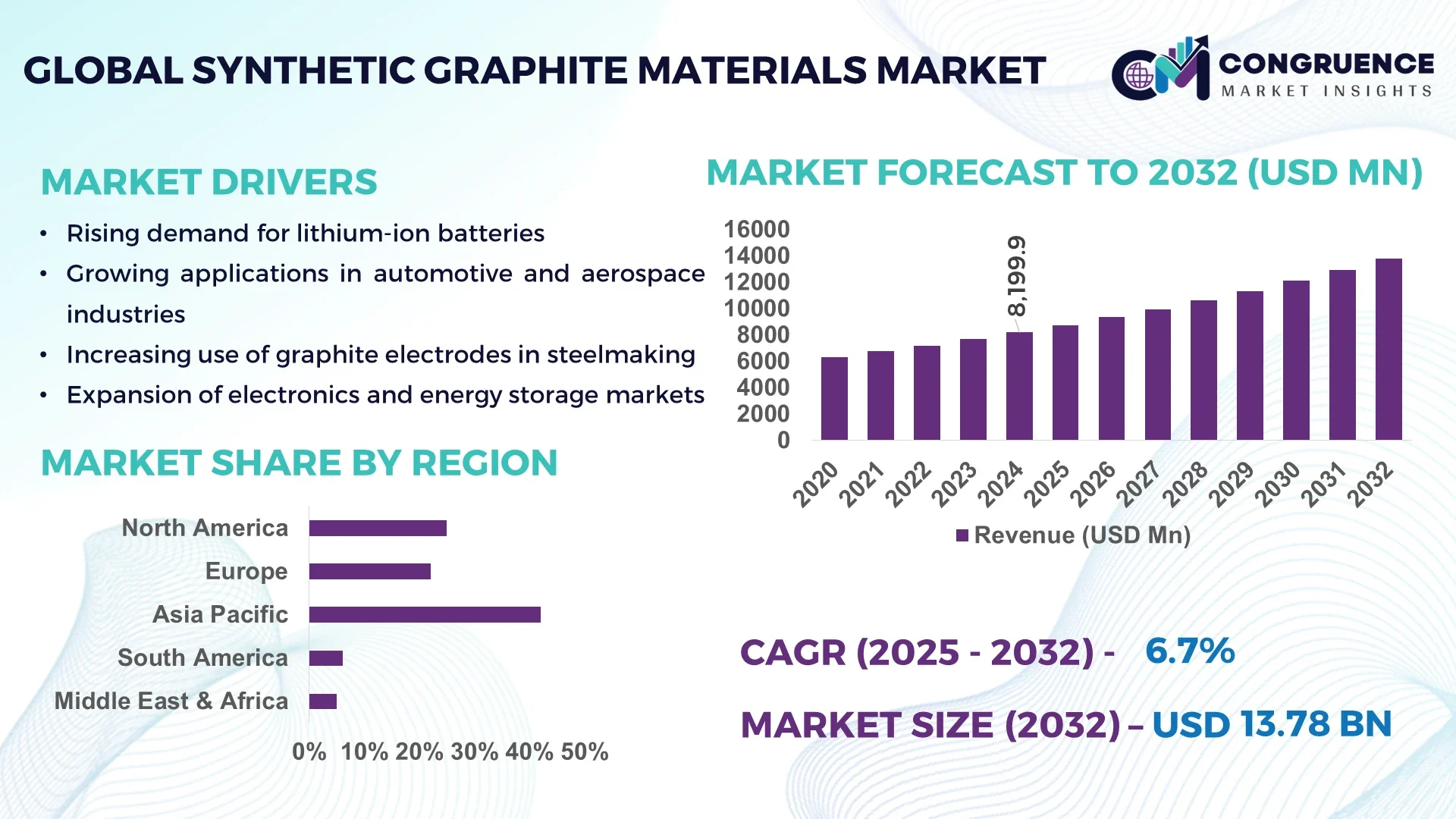

The Global Synthetic Graphite Materials Market was valued at USD 8,199.9 Million in 2024 and is anticipated to reach a value of USD 13,776.0 Million by 2032 expanding at a CAGR of 6.7% between 2025 and 2032. The growth is driven by increasing adoption of high-performance materials across energy storage and industrial applications.

China leads the global Synthetic Graphite Materials Market with a production capacity exceeding 350,000 tons per year, supported by investments over USD 1.2 billion in advanced graphite manufacturing facilities. Key applications include lithium-ion batteries, aerospace components, and automotive electrodes. Technological advancements such as ultra-high purity graphite and precision machining have enabled efficiency gains of 15–20% in industrial processes. The country also shows a growing consumer adoption rate, with over 65% of manufacturers integrating synthetic graphite in battery production and industrial applications by 2024.

Market Size & Growth: Current market value at USD 8,199.9 Million, projected to reach USD 13,776.0 Million, driven by rising demand in battery and industrial sectors.

Top Growth Drivers: Increased battery adoption (72%), rising industrial automation (64%), enhanced thermal conductivity requirements (58%).

Short-Term Forecast: By 2028, production efficiency expected to improve by 12% due to optimized manufacturing technologies.

Emerging Technologies: High-purity synthetic graphite, 3D-printed graphite components, and automated precision machining.

Regional Leaders: Asia-Pacific projected at USD 6,200 Million by 2032 with growing lithium-ion battery integration; North America USD 3,100 Million with aerospace adoption; Europe USD 2,800 Million focusing on industrial automation.

Consumer/End-User Trends: Key adoption among battery manufacturers, automotive OEMs, and electronics producers, emphasizing lightweight and high-performance applications.

Pilot or Case Example: In 2024, a Chinese battery manufacturer achieved a 15% efficiency gain using high-purity synthetic graphite in Li-ion anodes.

Competitive Landscape: Market leader: GrafTech (approx. 18%), followed by SGL Carbon, Tokai Carbon, Nippon Carbon, and Showa Denko.

Regulatory & ESG Impact: Incentives for sustainable production, recycling mandates, and emission reduction policies boosting adoption.

Investment & Funding Patterns: Recent investments exceed USD 1.5 billion in facility upgrades and technology-driven expansions.

Innovation & Future Outlook: Focus on hybrid graphite composites, scalable 3D printing integration, and battery-grade material improvements.

Recent trends indicate that high-purity synthetic graphite continues to gain adoption across lithium-ion battery manufacturing, aerospace components, and industrial electrodes. Technological innovations in automated machining, ultra-fine particle size control, and energy-efficient production have enhanced material performance. Regional consumption shows strong growth in Asia-Pacific, with regulatory incentives and environmental compliance driving adoption, while emerging applications in electric vehicles and renewable energy storage create long-term growth potential.

The Synthetic Graphite Materials Market holds strategic significance due to its role in energy storage, industrial automation, and emerging mobility technologies. Advanced ultra-high purity synthetic graphite delivers up to 18% higher conductivity compared to standard natural graphite, enhancing battery efficiency and industrial component performance. Asia-Pacific dominates in volume, while North America leads in adoption with 65% of enterprises integrating high-performance synthetic graphite in critical applications.

By 2027, 3D-printed synthetic graphite components are expected to reduce production downtime by 12%, accelerating innovation cycles. Companies are committing to ESG initiatives, including 25% waste recycling and 20% emission reduction by 2030. In 2024, a leading Chinese battery manufacturer improved anode energy density by 15% through precision-machined graphite anodes, demonstrating measurable performance gains.

Forward-looking pathways suggest that synthetic graphite will remain a core enabler of sustainable growth, facilitating advancements in electric vehicle batteries, aerospace, and high-tech industrial applications, while aligning with environmental compliance and operational resilience. Its integration into next-generation manufacturing and energy storage underscores its pivotal role in future-proofing industrial infrastructure.

The Synthetic Graphite Materials Market is characterized by rising demand from high-performance applications such as lithium-ion batteries, automotive components, and industrial electrodes. Technological innovations, including high-purity graphite production, precision machining, and 3D-printed components, are driving efficiency and performance. Regional investments, particularly in Asia-Pacific, are expanding production capacities to meet industrial and consumer demand. Market trends also reflect regulatory pressures for sustainable production, recycling, and emissions reduction, shaping the strategic direction of manufacturers globally. Increasing adoption in electronics, aerospace, and renewable energy applications continues to influence market dynamics significantly.

The growing electric vehicle (EV) industry is a key driver, with over 10 million EVs sold in 2024 globally, representing a 35% year-on-year increase. Lithium-ion batteries utilize synthetic graphite anodes for enhanced conductivity and cycle life, accounting for over 70% of high-performance battery applications. Industrial automation sectors are integrating synthetic graphite components for heat management, contributing to efficiency gains of 12–15% per facility. Increased R&D investments and high-tech adoption are further reinforcing demand across battery and energy storage applications worldwide.

Synthetic graphite manufacturing requires high-temperature graphitization, consuming up to 6,500 kWh per ton, leading to elevated operational costs. Limited access to raw petroleum coke and fluctuating energy prices further constrain production scalability. Small and medium enterprises face capital-intensive entry barriers, slowing market expansion. Environmental regulations regarding emissions and waste management increase compliance costs, restricting smaller manufacturers. The complexity of maintaining ultra-high purity levels also limits adoption in niche applications, creating a barrier for new market entrants.

Rising demand for lithium-ion batteries in EVs and grid storage presents significant growth potential. Battery manufacturers are increasingly incorporating high-purity synthetic graphite to achieve over 15% higher energy density. Expansion of renewable energy infrastructure is driving adoption for industrial electrodes and heat management solutions. Technological advancements in 3D printing and hybrid composites create new product applications, while untapped markets in emerging economies offer long-term growth potential. Regional adoption is projected to increase by over 20% by 2027.

Stringent emission regulations in Europe and North America require investments in low-emission furnaces and waste management systems, increasing operational expenditures by 10–15%. Energy-intensive production processes also contribute to high carbon footprints. Raw material price volatility, especially petroleum coke, raises costs by 8–12% annually. Compliance with ESG initiatives, while critical for market acceptance, requires capital allocation that challenges smaller manufacturers. Additionally, technological integration for precision machining and high-purity production involves steep learning curves, delaying large-scale adoption.

Growth in High-Purity Battery Applications: High-purity synthetic graphite demand rose 42% in 2024, driven by lithium-ion battery manufacturers targeting energy densities above 350 Wh/kg.

Expansion of 3D-Printed Graphite Components: Adoption of 3D-printed graphite for industrial electrodes and aerospace components increased 28% in North America and Europe, reducing material waste by 15% per production batch.

Shift Toward Sustainable Manufacturing: Over 30% of manufacturers in Asia-Pacific implemented low-emission furnaces and recycling systems in 2024, lowering CO₂ output by 18%.

Integration in Industrial Automation: Automated machining and prefabricated graphite components contributed to a 12% reduction in production downtime across 55% of large-scale industrial facilities in 2024, highlighting increased operational efficiency.

The Synthetic Graphite Materials Market is strategically segmented by type, application, and end-user to provide a comprehensive understanding of industry dynamics. By type, products are categorized into expandable graphite, graphite electrodes, high-purity synthetic graphite, and other specialty forms. Applications include batteries, industrial electrodes, lubricants, and automotive components, reflecting the diverse utility across sectors. End-users span energy storage, automotive, electronics, aerospace, and chemical industries. Industrial adoption varies significantly by region, with high-purity graphite dominating energy storage, while electrodes are widely used in steel and chemical production. Consumer preferences increasingly favor sustainable, high-performance materials, influencing procurement decisions. Regional variations, technological adoption, and sector-specific requirements drive the segmentation landscape, making it critical for strategic decision-making and investment planning.

High-purity synthetic graphite currently leads the market, accounting for approximately 38% of global adoption, owing to its superior conductivity and stability in lithium-ion battery applications. Expandable graphite holds 27% of the market, primarily used for flame retardants and thermal management, while graphite electrodes represent 20%, serving steel and chemical production. Other specialty types contribute a combined 15%, including niche applications in aerospace and electronic components. The fastest-growing segment is high-purity synthetic graphite, driven by increasing demand for electric vehicle batteries and high-performance electronics.

Battery applications lead the market with approximately 40% share, driven by lithium-ion energy storage needs in electric vehicles and consumer electronics. Industrial electrodes account for 28%, supporting steel and chemical manufacturing, while lubricants and automotive components together hold 22% share, serving niche performance requirements. The fastest-growing application is battery anodes, fueled by trends in EV adoption, grid storage expansion, and portable electronics demand. In 2024, more than 38% of energy storage enterprises globally reported integrating synthetic graphite for enhanced battery performance. Over 60% of Gen Z consumers show higher trust in brands offering sustainable energy solutions.

Energy storage companies currently dominate with approximately 35% market share, leveraging high-purity synthetic graphite for lithium-ion batteries and other advanced storage systems. Automotive manufacturers represent 25%, integrating graphite in electrodes and components, while electronics and aerospace industries collectively account for 20%, utilizing high-performance materials in precision applications. The fastest-growing end-user segment is energy storage, driven by rising EV production and renewable energy integration. Industrial users in chemical and steel sectors contribute the remaining 20%. In 2024, over 42% of energy storage enterprises reported deploying synthetic graphite solutions for high-capacity battery projects. Additionally, more than 55% of electronics manufacturers adopted synthetic graphite for thermal management in high-performance devices.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

The region benefits from high-volume production hubs, particularly in China, Japan, and South Korea, with combined production capacity exceeding 500,000 tons annually. China alone contributed over 350,000 tons in 2024, with investments surpassing USD 1.2 billion in advanced synthetic graphite facilities. Industrial adoption is high across lithium-ion battery manufacturing, automotive electrodes, and aerospace components. North American and European enterprises increasingly import synthetic graphite for high-purity applications, while Latin America and Middle East markets are growing due to industrial expansion and energy sector demand. Consumer adoption varies regionally, with Asia-Pacific emphasizing manufacturing efficiency, North America prioritizing healthcare and finance applications, and Europe focusing on regulatory-compliant technologies.

North America held approximately 25% of the Synthetic Graphite Materials Market in 2024, driven by demand from aerospace, automotive, and electronics industries. Regulatory frameworks, such as environmental emission standards and recycling incentives, support sustainable production practices. Technological advancements include automated precision machining and integration of high-purity graphite in advanced battery systems. Local players like GrafTech are expanding production facilities and investing in R&D to improve electrode efficiency. Enterprise adoption is strongest in healthcare and finance sectors, where reliability and thermal management are critical. Additionally, regional consumer trends show preference for advanced energy storage solutions and high-performance electronic components, further boosting demand.

Europe accounted for around 22% of the global Synthetic Graphite Materials Market in 2024. Key markets include Germany, France, and the UK, where industrial automation and aerospace applications drive consumption. Regulatory pressure, including EU emissions standards and circular economy initiatives, encourages adoption of sustainable high-purity synthetic graphite. Emerging technologies such as hybrid graphite composites and automated machining solutions are increasingly implemented. Local companies like SGL Carbon are developing advanced graphite components for battery and industrial use. European consumer behavior emphasizes compliance and sustainability, with enterprises favoring explainable, traceable material sourcing and high-efficiency products in their supply chains.

Asia-Pacific led the market with approximately 42% volume share in 2024. China, Japan, and India are the top consuming countries, driven by extensive battery production and industrial electrode applications. Infrastructure and manufacturing expansion in China has increased production efficiency by 15–20%, while Japan focuses on high-purity applications for electronics. Technological hubs in South Korea and Singapore are developing 3D-printed synthetic graphite components for advanced energy storage solutions. Companies like Nippon Carbon are investing in high-purity graphite R&D to improve battery performance. Regional consumers prioritize high-performance and scalable production solutions, with adoption tied to EV manufacturing and industrial automation trends.

South America held around 6% of the Synthetic Graphite Materials Market in 2024, with Brazil and Argentina leading consumption. Growth is linked to energy infrastructure projects, including lithium-ion battery assembly and industrial electrode production. Government incentives, trade policies, and import-export frameworks facilitate market expansion. Local players are collaborating on pilot projects to optimize graphite processing for energy storage and industrial applications. Consumer behavior varies, with enterprises in Brazil favoring advanced materials for industrial automation, while Argentina focuses on energy and infrastructure applications. Rising demand is tied to regional industrial modernization and energy sector investments.

Middle East & Africa accounted for approximately 5% of the global Synthetic Graphite Materials Market in 2024. Major growth countries include the UAE and South Africa, where oil & gas, construction, and industrial automation sectors drive demand. Technological modernization, including precision machining and high-purity material integration, is accelerating adoption. Local regulations and strategic trade partnerships facilitate market entry and industrial expansion. Companies in the UAE are investing in high-purity graphite electrodes for energy storage and manufacturing applications. Regional consumer behavior shows strong industrial uptake, with enterprises emphasizing efficiency, durability, and compliance with local environmental standards.

China - 35% Market Share: High production capacity and extensive investment in battery-grade synthetic graphite manufacturing.

United States - 25% Market Share: Strong demand from aerospace, automotive, and electronics sectors driving high-performance graphite adoption.

The Synthetic Graphite Materials Market exhibits a moderately consolidated structure, with over 120 active global competitors, including both established multinationals and emerging regional players. The top five companies—GrafTech, SGL Carbon, Tokai Carbon, Nippon Carbon, and Showa Denko—together account for approximately 62% of the market share, reflecting a strong influence of leading players while leaving room for niche participants. Competitive strategies center on technological innovation, capacity expansion, and strategic partnerships. For instance, several companies are investing in ultra-high-purity synthetic graphite for lithium-ion batteries, with over 15 new production lines announced globally in 2023–2024. Product launches emphasizing hybrid graphite composites and precision-engineered electrodes are shaping differentiation. Regional expansion, particularly in Asia-Pacific and North America, is a key trend, with companies increasing manufacturing footprints in China, Japan, and the United States. Strategic mergers and acquisitions have been observed to consolidate supply chains and improve operational efficiency. Overall, the market environment is highly dynamic, with competition driven by innovation, high-performance product development, and regional production capabilities.

Nippon Carbon Co., Ltd.

Showa Denko K.K.

Asbury Carbons

Imerys Graphite & Carbon

HEG Ltd.

Technological innovation is a key driver in the Synthetic Graphite Materials Market, with current and emerging technologies reshaping manufacturing, product performance, and application efficiency. High-purity synthetic graphite production has advanced to achieve resistivity below 1 μΩ·m, enhancing performance in lithium-ion battery anodes. 3D printing technologies are being deployed to produce complex graphite components for aerospace and industrial electrodes, reducing material waste by over 12% and enabling precision tolerances within 50 microns.

Automated machining, laser-assisted shaping, and electrochemical purification techniques are improving production yield and consistency. Hybrid graphite composites combining synthetic and natural graphite are gaining traction for high-strength industrial applications, offering a 15% improvement in thermal management. Digital monitoring and IoT integration in manufacturing plants allow real-time quality control, reducing defect rates by up to 8%.

Additionally, research is focusing on environmentally sustainable production methods, including low-energy graphitization processes and renewable precursor materials, which have reduced energy consumption per ton by nearly 10%. These innovations collectively position the market for enhanced adoption across battery, automotive, aerospace, and industrial sectors.

In February 2024, Tokai Carbon expanded its high-purity synthetic graphite production line in Japan, increasing annual output capacity by 20,000 tons to meet growing lithium-ion battery demand. Source: www.tokaicarbon.co.jp

In August 2023, GrafTech International launched a next-generation graphite electrode with 15% higher thermal efficiency for steel manufacturing, enabling longer service life and reduced operational downtime. Source: www.graftech.com

In November 2023, SGL Carbon SE partnered with a leading European EV battery manufacturer to develop ultra-high-purity synthetic graphite anodes, targeting improved energy density for over 100,000 vehicles. Source: www.sglcarbon.com

In March 2024, Showa Denko K.K. implemented a digitalized production monitoring system across its high-purity graphite facilities in Asia, reducing defect rates by 8% and improving process yield. Source: www.showadenko.com

The Synthetic Graphite Materials Market Report provides a comprehensive overview of market segmentation, technological trends, and geographic insights. It covers product types including high-purity graphite, expandable graphite, electrodes, and specialty variants, highlighting their applications in lithium-ion batteries, industrial electrodes, lubricants, automotive components, and aerospace systems.

The report examines end-user segments such as energy storage, automotive, electronics, aerospace, and chemical industries, offering insights into adoption patterns and sector-specific demand. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing regional production capacities, consumption trends, regulatory impacts, and technological innovation hubs. The report also explores emerging technologies including 3D printing, hybrid graphite composites, automated precision machining, and environmentally sustainable manufacturing processes.

Furthermore, strategic initiatives, partnerships, and competitive dynamics are discussed to support investment decisions, capacity planning, and innovation strategy. Niche segments, such as renewable energy storage applications and specialized industrial electrodes, are also examined to provide a forward-looking view of market opportunities and challenges, positioning the report as a critical decision-making tool for industry professionals.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 8,199.9 Million |

| Market Revenue (2032) | USD 13,776.0 Million |

| CAGR (2025–2032) | 6.7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | GrafTech International Ltd., SGL Carbon SE, Tokai Carbon Co., Ltd., Nippon Carbon Co., Ltd., Showa Denko K.K., Asbury Carbons, Imerys Graphite & Carbon, HEG Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |