Reports

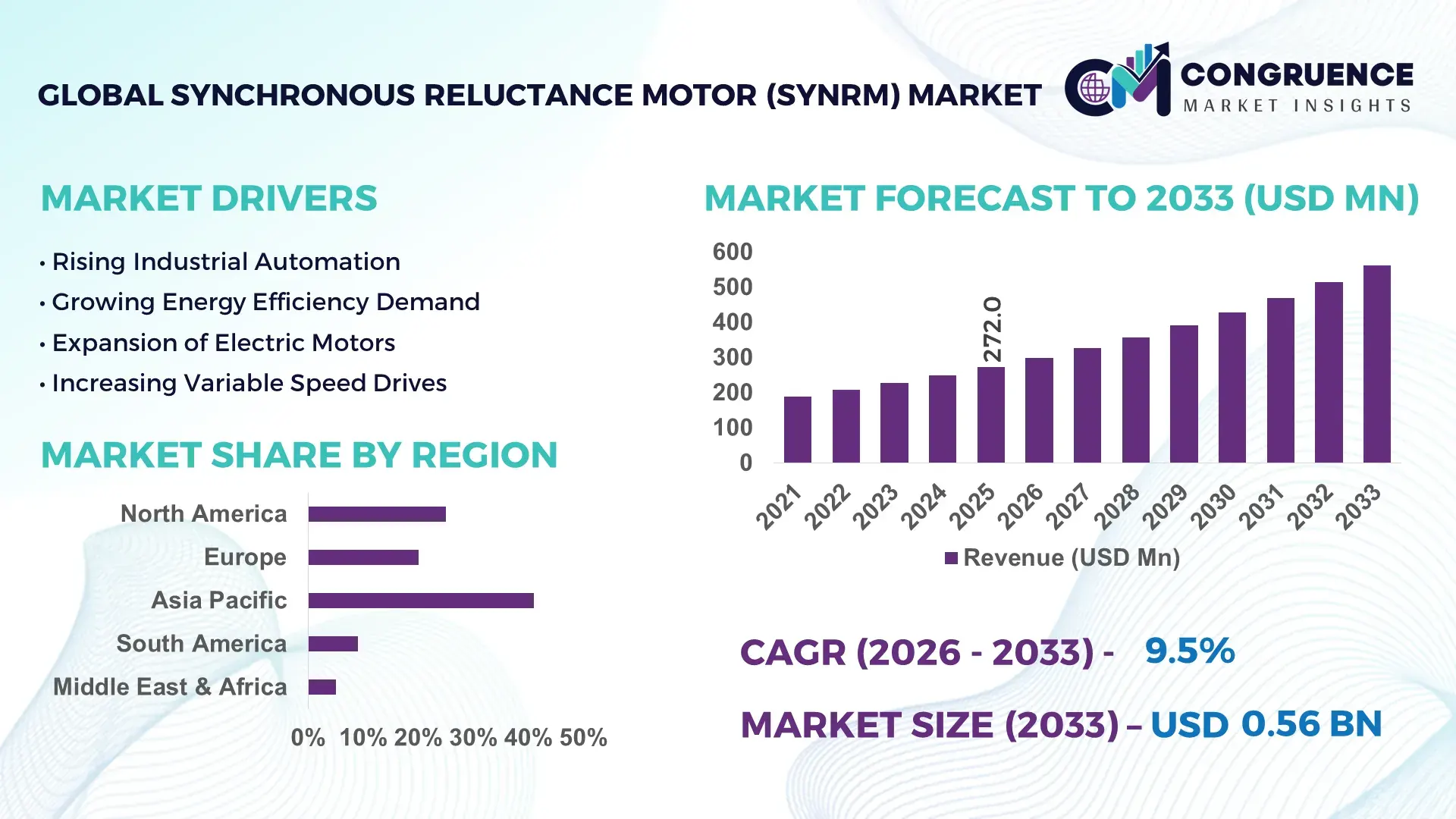

The Global Synchronous Reluctance Motor (SynRM) Market was valued at USD 272 Million in 2025 and is anticipated to reach a value of USD 562.18 Million by 2033 expanding at a CAGR of 9.5% between 2026 and 2033. Rising industrial electrification, tightening IE5 efficiency mandates, and accelerated replacement of rare-earth magnet motors across HVAC, water treatment, and process manufacturing facilities are driving large-scale SynRM deployment in 2026.

China accounts for nearly 34% of global industrial motor production capacity, supported by over USD 8 billion in high-efficiency motor modernization investments targeting steel, chemicals, and automation-intensive manufacturing zones, while Germany leads advanced SynRM integration in precision machinery with factory energy savings exceeding 18% in selected industrial retrofits. Ongoing Red Sea shipping disruptions further accelerated localized motor sourcing strategies across Asia and Europe, strengthening regional production resilience and reducing procurement lead times by approximately 12%.

Strategic expansion into localized high-efficiency motor manufacturing and industrial retrofit partnerships remains critical for suppliers targeting long-term procurement contracts and energy-transition-driven market positioning.

Market Size & Growth: USD 272 Million in 2025 rising to USD 562.18 Million by 2033 at 9.5% growth, supported by IE5 motor upgrades and industrial energy-efficiency mandates.

Top Growth Drivers: Industrial automation adoption increased 21%, HVAC electrification expanded 17%, and rare-earth-free motor demand rose 24% globally during 2025–2026.

Short-Term Forecast: By 2028, advanced SynRM systems are projected to reduce industrial motor energy losses by 14% and maintenance downtime by 11%.

Emerging Technologies: AI-driven motor monitoring, sensorless control systems, and advanced rotor lamination designs improved operational efficiency by nearly 16% in automated facilities.

Regional Leaders: Asia-Pacific exceeds USD 240 Million driven by factory automation, Europe approaches USD 150 Million through IE5 compliance, and North America crosses USD 110 Million via water infrastructure modernization.

Consumer/End-User Trends: More than 38% of industrial operators prioritized rare-earth-free motor procurement in 2026 amid supply-chain volatility and cost-control initiatives.

Pilot/Case Example: In 2026, a Nordic manufacturing retrofit project lowered electricity consumption by 19% after replacing conventional induction motors with high-efficiency SynRM units.

Competitive Landscape: ABB holds approximately 18% market share alongside Siemens, WEG, Nidec, and Danfoss competing through advanced industrial drive integration.

Regulatory & ESG Impact: European industrial efficiency policies reduced motor-related emissions by nearly 13% across regulated facilities implementing premium-efficiency systems.

Investment & Funding: Global investments surpassed USD 1.1 billion in motor modernization, led by automation partnerships, localized production expansion, and smart manufacturing upgrades.

Innovation & Future Outlook: Integrated digital drives, compact rotor architectures, and low-noise high-speed SynRM platforms are reshaping next-generation industrial motion strategies.

Synchronous Reluctance Motor (SynRM) systems are gaining strong traction across industrial pumps, compressors, conveyors, and HVAC infrastructure due to lower rare-earth dependency and higher operational efficiency. Advanced rotor optimization and sensorless drive technologies improved energy performance by nearly 15% in recent industrial deployments. Expanding factory electrification programs across Southeast Asia and Europe, alongside tightening industrial efficiency regulations, are accelerating strategic procurement and long-term automation investments across the global SynRM ecosystem.

The Synchronous Reluctance Motor (SynRM) market is becoming strategically important as industrial operators prioritize energy-efficient electrification, rare-earth-free motor architectures, and lower lifecycle operating costs. Tightened IE4 and IE5 efficiency regulations across Europe and industrial modernization programs in China and India are accelerating replacement cycles for conventional induction motors. At the same time, supply-chain restructuring following Red Sea logistics disruptions and volatile magnet material pricing pushed manufacturers toward localized motor production and integrated drive partnerships to secure procurement stability.

Advanced SynRM systems paired with variable frequency drives deliver up to 20% lower energy consumption compared to standard induction motors in continuous-load applications such as compressors, pumps, and HVAC systems. Germany leads high-precision industrial deployment through automated manufacturing facilities, while China scales volume adoption across steel, chemicals, and wastewater infrastructure projects. In 2026, several Nordic processing plants reported nearly 15% maintenance cost reductions after retrofitting older motor fleets with digitally monitored SynRM platforms.

Over the next two to three years, industrial automation upgrades and smart-factory investments are expected to expand sensor-integrated motor adoption by more than 25% across process manufacturing environments. Companies are increasing investments in compact rotor design, localized assembly, and OEM partnerships to strengthen aftermarket positioning and industrial service networks. Suppliers capable of combining efficiency performance, digital integration, and supply resilience will secure stronger long-term competitiveness in the evolving industrial motion ecosystem.

Industrial operators are accelerating SynRM deployment to reduce electricity consumption and minimize dependence on rare-earth magnet supply chains. High-efficiency SynRM systems lower energy losses by nearly 18% in continuous-duty industrial applications, while maintenance requirements decline approximately 12% due to simplified rotor structures. China’s industrial efficiency modernization targets and Europe’s IE5 motor regulations are forcing rapid replacement of legacy induction motors across HVAC, water treatment, and chemical processing facilities. In response, manufacturers are expanding integrated motor-drive portfolios and increasing localized production capacity to reduce procurement delays. A notable operational shift involves OEMs prioritizing rare-earth-free designs to stabilize long-term production economics amid ongoing geopolitical material supply uncertainty and rising industrial electrification demand.

Despite efficiency gains, SynRM adoption remains constrained by dependence on advanced variable frequency drives and higher integration complexity within older industrial infrastructure. Retrofitting costs for medium-scale facilities can rise 15%–22% due to inverter upgrades, control-system modifications, and engineering recalibration requirements. In India and Southeast Asia, nearly 40% of installed industrial motor bases still operate on aging fixed-speed systems with limited compatibility for advanced synchronous motor controls. Supply bottlenecks affecting semiconductor components and industrial-grade laminations during 2025–2026 also increased delivery lead times by approximately 10%. To reduce operational risk, manufacturers are expanding local sourcing agreements, standardizing modular drive platforms, and offering bundled retrofit services that improve deployment economics for energy-intensive industries.

The expanding adoption of Industry 4.0 infrastructure is creating strong opportunities for digitally integrated SynRM systems across manufacturing, logistics, and process automation environments. Sensor-enabled motor platforms improved predictive maintenance accuracy by nearly 28% in automated facilities, while energy-monitoring integration reduced unplanned downtime by approximately 14%. Japan and Germany are increasing investments in smart industrial retrofits where compact high-efficiency motors support robotics, precision machining, and intelligent conveyor systems. Emerging policy incentives tied to industrial decarbonization and grid-efficiency optimization are further accelerating deployment of premium-efficiency motor technologies. Companies are responding through AI-enabled motor diagnostics, strategic automation partnerships, and development of low-noise compact rotor platforms targeting untapped mid-sized industrial facilities with rising electrification requirements.

Long-term SynRM scalability depends heavily on skilled workforce availability, digital integration capabilities, and consistent industrial infrastructure readiness. Nearly 32% of industrial facilities upgrading to advanced motor systems reported commissioning delays linked to shortages in drive-control engineering expertise and automation integration specialists. Complex synchronization between motor controllers, predictive monitoring software, and legacy factory equipment continues to challenge deployment consistency, particularly across medium-sized industrial clusters in Latin America and South Asia. Increasing cybersecurity exposure from connected industrial motor networks also intensified operational risk as factories adopt cloud-based monitoring platforms. To sustain competitiveness, companies must strengthen technical training programs, expand industrial software partnerships, and invest in standardized interoperable motor-control ecosystems that improve deployment speed and long-term operational reliability.

• Integrated Drive Adoption Accelerates Industrial facilities are increasingly deploying integrated drive SynRM systems to simplify commissioning and improve process automation efficiency. In 2026, integrated motor-drive installations expanded nearly 26% across packaging, water treatment, and conveyor-intensive manufacturing sites. German automation suppliers reduced wiring complexity by approximately 18% through compact drive integration, while Chinese OEMs accelerated bundled motor-control deployments to shorten installation cycles. Companies are restructuring product portfolios around pre-configured smart motor platforms to reduce engineering costs and improve aftermarket service responsiveness.

• Rare-Earth-Free Procurement Expands Volatile magnet material pricing and geopolitical supply uncertainty pushed nearly 38% of industrial buyers toward rare-earth-free SynRM procurement strategies during 2025–2026. Scandinavian process industries increased adoption of magnet-free motor architectures to stabilize long-term maintenance and sourcing costs. Japanese manufacturers are strengthening localized rotor lamination partnerships and dual-sourcing strategies after logistics disruptions affected industrial motor imports. This transition is also reducing exposure to commodity price fluctuations while improving procurement predictability for energy-intensive operations.

• Digital Monitoring Becomes Standard Sensor-enabled SynRM platforms with predictive diagnostics gained strong traction as factories prioritized uptime optimization and remote maintenance visibility. Smart monitoring deployments increased over 30% in continuous-process industries, while predictive maintenance systems reduced unplanned shutdowns by nearly 16%. Food processing facilities in Italy and pharmaceutical plants in Singapore integrated cloud-based motor analytics into centralized production workflows. Suppliers are responding through industrial software alliances, embedded condition-monitoring capabilities, and subscription-based service models tied to operational performance guarantees.

• High-Efficiency Retrofits Intensify Aging industrial motor fleets are being rapidly replaced as energy regulations tighten across Europe and India. IE5-focused retrofit projects lowered electricity consumption by approximately 14% in selected HVAC and pump-intensive facilities during 2026. A non-obvious shift emerged in medium-sized factories, where operators prioritized retrofit-ready compact SynRM units over full equipment replacement to minimize downtime and preserve existing infrastructure. Manufacturers are scaling modular retrofit kits, expanding regional engineering support, and increasing partnerships with industrial contractors to accelerate deployment speed.

High-Efficiency SynRM currently leads the market due to strong deployment across industrial pumps, compressors, and HVAC systems requiring continuous-duty energy optimization. These systems account for nearly 34% of industrial SynRM installations because they deliver approximately 15% lower operational energy losses compared to standard induction motors. IE4 SynRM variants remain widely adopted across mid-scale manufacturing facilities where cost-performance balance and compatibility with existing drive infrastructure remain critical. Standard SynRM systems continue serving price-sensitive industrial operations, particularly in Southeast Asian manufacturing clusters focused on incremental efficiency upgrades rather than complete automation transitions.

IE5 SynRM is emerging as the fastest-growing segment as industrial operators respond to tightening efficiency regulations and rising electricity costs. Adoption of IE5-rated systems increased nearly 28% during 2025–2026 across Germany, China, and Nordic processing industries. Integrated Drive SynRM platforms are also gaining momentum due to simplified installation workflows and improved predictive maintenance integration. Companies are prioritizing compact rotor innovation, embedded diagnostics, and bundled drive-control solutions to strengthen differentiation in retrofit-heavy industrial markets while reducing commissioning complexity and lifecycle servicing costs.

Pumps remain the dominant application segment due to extensive usage across water treatment, chemical processing, and industrial fluid management operations. Nearly 36% of installed SynRM systems are currently deployed in pump-driven environments where energy optimization and continuous-load performance are operationally critical. SynRM integration in pump systems reduced electricity usage by approximately 14% in high-duty industrial facilities during 2026. Compressors maintain strong adoption in manufacturing and process industries where lower rotor heating and reduced maintenance intervals improve uptime stability. Conveyor applications are expanding steadily within automated logistics and packaging facilities focused on high-throughput material handling efficiency.

HVAC Systems represent the fastest-growing application segment as commercial infrastructure modernization and industrial climate-control upgrades accelerate globally. Deployment of high-efficiency SynRM HVAC systems increased approximately 24% across data centers, pharmaceutical plants, and smart commercial buildings. Fans and blowers are also transitioning toward digitally monitored SynRM platforms to improve airflow precision and lower acoustic output in regulated industrial environments. Companies are expanding application-specific motor portfolios, strengthening automation partnerships, and integrating variable-speed control technologies to improve performance consistency and operational flexibility across energy-intensive sectors.

The Manufacturing Industry remains the dominant end-user segment due to large-scale deployment across conveyors, pumps, compressors, and automated production systems. More than 40% of industrial SynRM demand originates from manufacturing facilities focused on reducing electricity intensity and improving equipment uptime. Automotive and precision engineering plants in Germany and China accelerated replacement of aging induction motors during 2025–2026 to align with industrial efficiency mandates. The Chemical Industry and Oil and Gas Industry continue adopting SynRM systems for high-load process environments where reduced maintenance intervals and thermal stability directly improve operational continuity and equipment reliability.

Water and Wastewater Industry applications are emerging as the fastest-growing end-user segment driven by infrastructure modernization and rising municipal energy-efficiency targets. SynRM adoption in wastewater pumping and aeration systems increased nearly 27% during 2026, particularly across India and the Middle East. Food and Beverage Industry operators are also expanding deployment of low-noise, hygienic motor systems integrated with automated production lines. Power Generation facilities remain strategically important for auxiliary motor operations requiring stable continuous-duty performance. Companies are targeting these sectors through customized drive integration, long-term service contracts, and localized engineering support tailored to industry-specific operational requirements.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2026 and 2033.

Industrial Automation and Retrofit Modernization Accelerate Deployment

North America maintains strong SynRM adoption through industrial automation upgrades, data center cooling expansion, and energy-efficiency retrofits across manufacturing and utility infrastructure. The region contributed nearly 24% of global deployment activity in 2025, with high concentration across HVAC, water treatment, and food processing operations. U.S. industrial facilities increasingly replaced aging induction motors with integrated drive SynRM platforms to reduce electricity intensity and improve predictive maintenance capabilities. In 2026, multiple utility modernization projects across Texas and Ontario accelerated deployment of premium-efficiency motor systems within municipal pumping infrastructure, reducing operational energy usage by approximately 15%. Companies are strengthening regional engineering partnerships and localized assembly capabilities to shorten industrial delivery cycles and improve aftermarket servicing responsiveness.

United States Market Outlook: The United States leads North American SynRM demand due to large-scale industrial electrification, advanced automation penetration, and strict enterprise-level energy optimization targets. Manufacturing facilities across Michigan, Texas, and Ohio expanded deployment of sensor-integrated SynRM systems within conveyor, compressor, and HVAC operations during 2025–2026. More than 35% of newly installed premium-efficiency industrial motor systems in selected process industries incorporated digital monitoring capabilities, reflecting growing demand for predictive maintenance integration and operational uptime optimization.

Efficiency Regulation and Smart Manufacturing Drive Market Transition

Europe is emerging as the fastest-transforming SynRM market due to aggressive industrial efficiency mandates, smart manufacturing investments, and accelerated decarbonization programs. The region accounted for approximately 28% of global high-efficiency motor deployments in 2025, with Germany, Italy, and Nordic countries leading industrial retrofitting activity. Industrial operators are replacing legacy induction motors with IE5-rated SynRM systems to comply with tightening energy regulations and reduce electricity consumption across automated production facilities. In 2026, several large-scale industrial modernization projects in Germany reduced motor-related power losses by nearly 17% through digitally integrated SynRM deployment. Manufacturers are strengthening partnerships with automation integrators and expanding localized engineering support to improve retrofit scalability and lifecycle servicing efficiency.

Germany Market Outlook: Germany remains the strategic center of Europe’s SynRM ecosystem due to its advanced manufacturing base, automation leadership, and strong industrial energy-efficiency compliance framework. Automotive and precision engineering facilities across Bavaria and Baden-Württemberg accelerated adoption of integrated drive SynRM platforms for robotics, machining, and material handling applications. Nearly 32% of upgraded industrial motor systems installed in German smart factories during 2026 incorporated predictive diagnostics and variable-speed optimization technologies to improve operational consistency and reduce maintenance intervention frequency.

Large-Scale Manufacturing and Infrastructure Deployment Sustain Dominance

Asia-Pacific leads the global SynRM market through large-scale industrial manufacturing, infrastructure expansion, and strong deployment across energy-intensive sectors. The region represented nearly 41% of total market activity in 2025, supported by extensive motor production capacity in China, Japan, and India. Industrial automation upgrades, wastewater infrastructure modernization, and rapid HVAC expansion are accelerating demand for high-efficiency motor systems across manufacturing clusters. In 2026, several Chinese industrial parks implemented premium-efficiency motor replacement programs that reduced facility-wide electricity consumption by approximately 14%. Companies are expanding regional assembly operations, strengthening supply-chain localization, and increasing partnerships with industrial automation providers to improve delivery stability and cost competitiveness.

China Market Outlook: China dominates Asia-Pacific SynRM deployment due to its massive industrial production base, aggressive factory modernization strategy, and strong domestic motor manufacturing ecosystem. Steel, chemicals, and electronics manufacturing facilities across Guangdong, Jiangsu, and Zhejiang accelerated adoption of rare-earth-free SynRM systems during 2025–2026 to improve energy efficiency and reduce long-term procurement risk. More than 38% of newly commissioned industrial automation projects in selected manufacturing zones integrated advanced variable-speed motor platforms to support continuous-load operational optimization and smart-factory deployment goals.

Industrial Efficiency Upgrades Strengthen Demand Momentum

South America is witnessing gradual SynRM adoption through mining modernization, wastewater infrastructure upgrades, and industrial energy-efficiency initiatives. Brazil and Chile account for the majority of regional deployment activity, particularly across pump-intensive mining and utility operations. The region contributed nearly 6% of global SynRM demand in 2025, with adoption concentrated in industrial retrofitting projects focused on reducing operational electricity costs. In 2026, selected mining facilities in Chile achieved approximately 12% lower motor-related energy usage after replacing conventional induction systems with advanced SynRM platforms. Despite infrastructure limitations and import dependency challenges, companies are increasing regional distribution partnerships and localized servicing capabilities to strengthen deployment reliability and aftermarket support.

Brazil Market Outlook: Brazil leads South American SynRM adoption due to its large industrial processing base, expanding wastewater infrastructure projects, and strong manufacturing activity in food processing and mining sectors. Industrial operators in São Paulo and Minas Gerais accelerated upgrades toward premium-efficiency motor systems to offset rising electricity costs and improve operational reliability. Nearly 27% of industrial motor modernization projects initiated during 2026 focused on integrated drive platforms capable of supporting predictive maintenance and automated process optimization within continuous-duty operating environments.

Infrastructure Modernization and Utility Investments Accelerate Adoption

The Middle East & Africa market is expanding through industrial diversification programs, water infrastructure investments, and energy-efficiency modernization initiatives. Gulf countries are increasing deployment of SynRM systems across desalination facilities, HVAC-intensive commercial infrastructure, and oil processing operations requiring continuous-duty motor performance. The region represented approximately 5% of global market deployment in 2025, with strongest demand concentration across Saudi Arabia and the United Arab Emirates. In 2026, several large-scale utility modernization projects in the Gulf integrated digitally monitored SynRM pumping systems that improved operational energy efficiency by nearly 13%. Companies are strengthening regional engineering alliances and expanding technical service networks to support large-scale infrastructure deployment and long-term maintenance requirements.

Saudi Arabia Market Outlook: Saudi Arabia remains the most strategically significant market in the region due to large-scale industrial diversification investments, expanding utility infrastructure, and rapid smart-city development programs. Industrial zones linked to petrochemical processing and water desalination projects accelerated adoption of premium-efficiency SynRM systems during 2025–2026 to reduce operational electricity intensity and improve asset reliability. More than 30% of newly upgraded utility pumping installations within selected infrastructure projects incorporated advanced variable-speed motor technologies aligned with national energy-efficiency modernization objectives.

The SynRM market is led by technology-focused global manufacturers including ABB, Siemens, WEG, Nidec, and Danfoss, competing directly against regional industrial motor suppliers focused on cost-efficient retrofit solutions. The top five players collectively control nearly 54% of global market activity through integrated drive platforms, advanced efficiency engineering, and large industrial service networks. Competition increasingly centers on energy performance, digital integration, and delivery reliability rather than base motor pricing alone. Premium-efficiency integrated systems lowered industrial energy usage by up to 20%, while predictive maintenance integration reduced downtime nearly 15%, strengthening technology-driven differentiation. Leading manufacturers are expanding localized assembly operations, securing rotor lamination supply chains, and forming automation partnerships to improve deployment speed and aftermarket penetration. Market competition is shifting toward vertically integrated smart motor ecosystems as industrial buyers prioritize lifecycle efficiency and operational continuity. Success increasingly depends on combining high-efficiency engineering, digital diagnostics, localized servicing, and supply-chain resilience.

Nidec Corporation

Danfoss

Toshiba Corporation

Regal Rexnord Corporation

CG Power and Industrial Solutions

TECO Electric & Machinery

Hitachi Industrial Equipment Systems

Fuji Electric

Wolong Electric Group

Hyundai Electric

Bharat Bijlee Limited

High-efficiency IE4 and IE5 SynRM platforms currently dominate industrial deployments as manufacturers prioritize lower energy consumption, reduced rotor losses, and rare-earth-free motor architectures. Integrated variable frequency drive systems improved operational efficiency by nearly 18% in continuous-load pump and compressor applications during 2026. More than 42% of newly deployed industrial SynRM systems now include embedded digital monitoring and predictive diagnostics. Compared with legacy IE3 induction motors, advanced liquid-cooled SynRM platforms reduce energy losses by up to 40% while lowering maintenance intervention frequency. Industrial operators benefit through faster retrofit payback periods, lower thermal stress, and improved process stability across automated manufacturing environments.

Emerging technologies are reshaping SynRM integration across smart factories and precision process industries. AI-enabled condition monitoring increased predictive maintenance accuracy by approximately 27%, while sensorless vector control systems improved speed stability by nearly 14% in conveyor and HVAC operations. Japanese and German automation suppliers are expanding compact integrated drive architectures that reduce commissioning complexity and installation footprint. Adoption of cloud-connected motor analytics surpassed 30% within digitally managed industrial facilities, strengthening lifecycle management and remote operational visibility.

Between 2026 and 2028, disruptive advances in magnet-free IE6 motor platforms, silicon carbide drive electronics, and modular digital twin integration will redefine industrial motor competitiveness. Global automation leaders and advanced OEMs will gain strongest advantage through lower lifecycle operating costs, faster deployment scalability, and stronger compliance alignment with tightening industrial efficiency regulations.

February 2024 – ABB launched the world’s first liquid-cooled IE5 SynRM motor platform designed for high-power industrial applications, delivering up to 40% lower energy losses versus IE3 systems. The innovation strengthened ABB’s premium industrial retrofit positioning across marine, plastics, and food processing operations. Source: (https://new.abb.com)

September 2025 – ABB expanded its IE5 SynRM portfolio with smaller frame sizes covering 0.75–450 kW, broadening deployment flexibility for compact industrial automation environments. The upgrade improved energy savings by nearly 40% compared with conventional IE3 motors, accelerating retrofit adoption in manufacturing and wastewater facilities. Source: (https://prtimes.jp)

July 2025 – ABB introduced expanded IE6 hyper-efficiency SynRM motor configurations with rare-earth-free architecture for industrial continuous-load applications. The platform improved operational efficiency and reduced maintenance exposure across compressors, pumps, and mining operations, strengthening ABB’s leadership in next-generation premium-efficiency industrial motion systems.

September 2025 – ABB extended its magnet-free IE5 SynRM motor lineup with additional low-frame configurations to improve deployment compatibility across HVAC and process industries. The expanded portfolio shortened retrofit implementation cycles and enhanced industrial energy optimization strategies for automation-intensive facilities.

The Synchronous Reluctance Motor (SynRM) Market Report provides detailed analysis across major motor types including Standard SynRM, High-Efficiency SynRM, IE4 SynRM, IE5 SynRM, and Integrated Drive SynRM platforms. The report evaluates deployment trends across pumps, compressors, HVAC systems, fans and blowers, and conveyor applications, while assessing operational demand from manufacturing, water and wastewater, oil and gas, food processing, chemical, and power generation industries. Nearly 40% of current industrial deployments are concentrated within continuous-load energy-intensive operations focused on efficiency modernization and predictive maintenance integration.

The report delivers region-wise strategic analysis covering North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level operational insights and industrial deployment positioning. It examines emerging technologies including AI-enabled motor diagnostics, sensorless control systems, integrated digital drives, and IE6 magnet-free motor architectures shaping industrial automation between 2026 and 2033. The study supports expansion planning, industrial retrofit strategies, supplier benchmarking, investment prioritization, and competitive positioning through detailed evaluation of technology adoption patterns, enterprise procurement shifts, and evolving industrial efficiency mandates.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 272 Million |

|

Market Revenue in 2033 |

USD 562.18 Million |

|

CAGR (2026 - 2033) |

9.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nidec Corporation, Danfoss, Toshiba Corporation, Regal Rexnord Corporation, CG Power and Industrial Solutions, TECO Electric & Machinery, Hitachi Industrial Equipment Systems, Fuji Electric, Wolong Electric Group, Hyundai Electric, Bharat Bijlee Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |