Reports

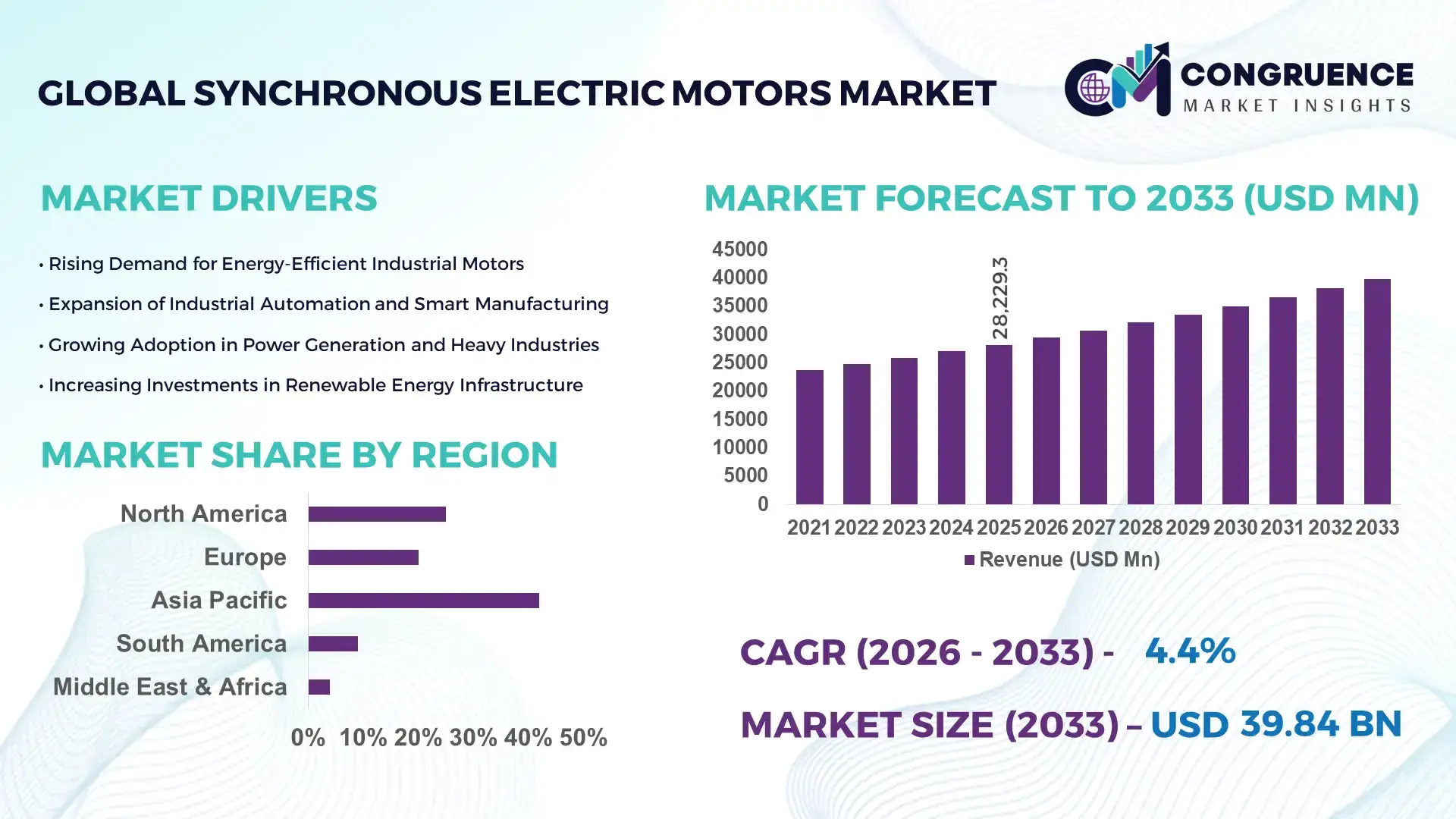

The Global Synchronous Electric Motors Market was valued at USD 28,229.34 Million in 2025 and is anticipated to reach a value of USD 39,838.66 Million by 2033 expanding at a CAGR of 4.4% between 2026 and 2033. Rising industrial automation and the growing adoption of energy-efficient motor technologies across manufacturing and infrastructure sectors are accelerating global demand.

China remains the most dominant country in the synchronous electric motors market due to its extensive industrial production ecosystem and large-scale electrification initiatives. The country manufactures over 40% of the world’s industrial electric motors through more than 2,000 motor manufacturing facilities integrated with advanced automation systems. China’s synchronous motor installations are widely used in steel production, mining operations, high-capacity compressors, and electric rail transport systems. In 2024, the country produced over 310 million industrial motors annually, with synchronous models increasingly deployed in high-efficiency industrial drives and renewable energy applications such as wind turbines. Significant investment in smart manufacturing and digital motor control systems has further strengthened China’s technological capabilities, particularly in permanent magnet synchronous motor production used in electric vehicles and precision machinery.

• Market Size & Growth: The synchronous electric motors market is valued at USD 28229.34 million in 2025 and is projected to reach USD 39838.66 million by 2033, expanding at a CAGR of 4.4% driven by industrial energy-efficiency regulations and increased electrification of heavy machinery.

• Top Growth Drivers: Industrial automation adoption rising by 38%, high-efficiency motor demand improving energy savings by 25%, and electric mobility expansion increasing motor utilization by 32%.

• Short-Term Forecast: By 2028, digital motor monitoring systems and smart drive integration are expected to improve operational efficiency by nearly 18% while reducing maintenance costs by around 14%.

• Emerging Technologies: Permanent magnet synchronous motors, IoT-enabled motor condition monitoring, and advanced variable frequency drive integration are transforming industrial motor performance and predictive maintenance capabilities.

• Regional Leaders: Asia Pacific projected to exceed USD 18 billion by 2033 with strong manufacturing demand; North America expected to reach USD 9 billion supported by energy-efficiency regulations; Europe forecast to surpass USD 7 billion due to electrified transport and industrial modernization.

• Consumer/End-User Trends: Heavy industries, electric vehicle manufacturers, renewable energy facilities, and large HVAC systems represent the primary users, with manufacturing accounting for more than 45% of installed synchronous motor capacity globally.

• Pilot or Case Example: In 2024, a European industrial plant upgraded compressor systems with permanent magnet synchronous motors, achieving a 22% energy efficiency improvement and reducing equipment downtime by 17%.

• Competitive Landscape: Siemens leads the market with an estimated 16% share, followed by ABB, WEG, Toshiba, Nidec, and Mitsubishi Electric operating across industrial and infrastructure segments.

• Regulatory & ESG Impact: Government energy-efficiency mandates such as IE4 and IE5 motor standards are accelerating adoption, while carbon-reduction policies encourage industries to replace conventional induction motors with high-efficiency synchronous alternatives.

• Investment & Funding Patterns: More than USD 2.5 billion has been invested globally in motor efficiency upgrades, electrified industrial equipment, and smart motor control technologies during the past two years.

• Innovation & Future Outlook: Advanced materials for permanent magnets, AI-enabled motor diagnostics, and integration with industrial IoT ecosystems are expected to reshape high-efficiency motor applications in manufacturing and transportation.

The synchronous electric motors market plays a crucial role in sectors such as manufacturing, transportation, energy, and heavy industrial operations. Industrial machinery accounts for nearly 45% of global synchronous motor installations, while renewable energy applications such as wind turbine generators contribute around 18% of usage. Innovations in permanent magnet rotor design and digital motor controllers have improved efficiency levels to above 95% in many industrial configurations. Government policies promoting electrification and carbon reduction are encouraging companies to replace legacy induction motors with high-efficiency synchronous alternatives. Additionally, rising investments in smart factories and predictive maintenance systems are accelerating the integration of intelligent motor monitoring platforms, shaping long-term market expansion and technological advancement.

The synchronous electric motors market has become strategically important for industries seeking improved energy efficiency, precision motion control, and lower operational costs. These motors maintain constant rotational speed under varying loads, making them highly suitable for applications in compressors, pumps, electric vehicles, and industrial robotics. As global electricity consumption continues to rise, industrial companies are prioritizing energy-efficient motor technologies to reduce energy intensity and improve operational performance. In large manufacturing facilities, synchronous electric motors can deliver up to 15% higher efficiency compared to traditional induction motors under heavy-load conditions.

Technological transformation is further reshaping the strategic direction of the synchronous electric motors market. Permanent magnet synchronous motor technology delivers nearly 20% improvement in torque density compared to conventional wound-rotor synchronous motors. This performance enhancement allows manufacturers to design compact motor systems with greater efficiency and lower energy consumption. Asia Pacific dominates the market in production volume due to large-scale manufacturing infrastructure, while Europe leads in advanced adoption with nearly 48% of industrial enterprises implementing high-efficiency motor upgrades to comply with strict energy-efficiency regulations.

Over the next few years, digitalization and smart motor technologies will play a major role in market expansion. By 2028, predictive maintenance platforms powered by AI-based motor diagnostics are expected to reduce unplanned equipment downtime by nearly 25% across large industrial plants. Integration of IoT sensors into motor systems enables real-time monitoring of temperature, vibration, and load performance, significantly improving equipment reliability and lifecycle management. Sustainability commitments are also shaping market pathways. Many industrial firms are committing to energy-intensity reductions of 30% by 2030 through upgrades to IE4 and IE5 efficiency motor systems. These initiatives are supported by government incentives encouraging energy-efficient motor installations across manufacturing and infrastructure sectors.

Industrial automation is rapidly transforming global manufacturing environments, driving the need for high-efficiency and precision motor systems. Synchronous electric motors play a critical role in automated production lines, robotics systems, and high-speed machinery where consistent rotational speed and precise control are essential. In automated assembly plants, synchronous motors provide torque stability that improves production accuracy and equipment reliability. Studies indicate that advanced synchronous motors can reduce energy consumption in industrial drive systems by up to 20% compared to older induction motor technologies. In sectors such as steel production, chemical processing, and mining, synchronous motors are widely used in large compressors and pumps to maintain operational efficiency under heavy load conditions. Additionally, smart factory initiatives integrating digital control systems and predictive maintenance technologies are further boosting demand for synchronous motor installations, enabling manufacturers to optimize productivity while minimizing operational energy losses.

Despite their efficiency advantages, synchronous electric motors often require higher initial investment compared to conventional induction motors, which can limit adoption in small and medium-scale industrial facilities. The cost of permanent magnet materials, advanced rotor components, and sophisticated control systems contributes to the higher price of these motors. Additionally, installation and integration with existing industrial equipment may require specialized power electronics such as variable frequency drives and digital controllers. For many legacy industrial plants operating with traditional motor infrastructure, upgrading to synchronous systems involves equipment replacement and system redesign, increasing capital expenditure and operational disruption during implementation. In some developing regions, limited technical expertise in advanced motor control systems also presents barriers to adoption. As a result, industries with tight capital budgets may delay investments in synchronous motor upgrades despite the long-term energy savings they offer.

The rapid expansion of renewable energy infrastructure presents significant opportunities for synchronous electric motor technologies. These motors are widely used in wind turbine generators, grid synchronization systems, and energy storage equipment due to their ability to maintain constant speed and stable power output. Global wind power installations exceeded 900 gigawatts in 2024, with synchronous generator systems playing a major role in converting mechanical energy into stable electrical output. Permanent magnet synchronous motors are also being integrated into electric vehicles, industrial electric drives, and advanced HVAC systems to improve overall system efficiency. In addition, increasing adoption of smart grid technologies requires highly stable motor and generator systems capable of supporting power frequency regulation. As governments continue to invest in renewable energy development and electrification infrastructure, synchronous electric motors are expected to become essential components in modern energy systems.

One of the major challenges affecting the synchronous electric motors market is the heavy dependence on rare earth materials used in permanent magnet rotor systems. Materials such as neodymium and dysprosium are essential for manufacturing high-performance permanent magnet synchronous motors that deliver superior efficiency and torque density. However, global supply of these materials is concentrated in limited geographic regions, making the supply chain vulnerable to geopolitical tensions and trade restrictions. Fluctuating raw material prices can significantly increase production costs for motor manufacturers and affect pricing stability in the market. Additionally, environmental regulations related to mining and processing rare earth elements may further limit material availability. Manufacturers are actively researching alternative magnet materials and improved motor designs to reduce rare earth dependency, but large-scale commercial implementation of such solutions remains an ongoing technological challenge for the industry.

• Rapid Adoption of Permanent Magnet Motor Technology: Permanent magnet synchronous motors are becoming increasingly prevalent across industrial automation and electric mobility sectors due to their superior efficiency and compact design. These motors can achieve efficiency levels exceeding 95%, reducing energy consumption by nearly 20% compared to conventional induction motors. Industrial plants upgrading to permanent magnet synchronous systems have reported operational energy savings of 15% to 18% annually. In electric vehicle manufacturing, over 70% of newly produced traction motors are now based on permanent magnet synchronous motor technology due to their high torque density and lightweight construction. Manufacturing facilities integrating these motors into automated production equipment have also observed up to 25% improvement in power utilization efficiency.

• Expansion of Smart Motor Monitoring and Predictive Maintenance Systems: The integration of digital sensors and advanced monitoring platforms is transforming how synchronous electric motors are managed in industrial environments. Approximately 62% of large manufacturing plants worldwide have begun implementing IoT-enabled motor monitoring systems that track temperature, vibration, and load conditions in real time. Predictive maintenance technologies using machine learning algorithms have demonstrated the ability to reduce unexpected equipment failures by nearly 30%. Industrial operators deploying these digital monitoring systems have also reported maintenance cost reductions of approximately 18%. Additionally, more than 40% of newly installed synchronous motors in advanced manufacturing facilities are now equipped with built-in digital diagnostic capabilities to support remote monitoring and performance optimization.

• Accelerating Electrification Across Transportation and Industrial Equipment: Electrification initiatives across transportation systems and heavy industrial machinery are significantly increasing demand for synchronous electric motors. In electric vehicle production, synchronous motors are used in nearly 72% of new electric drivetrain systems due to their high torque efficiency and consistent rotational performance. Industrial electric drive systems in mining, steel manufacturing, and chemical processing have increased synchronous motor installations by approximately 35% over the past five years. Electrified rail transportation systems also rely heavily on synchronous motors for traction applications, with over 60% of modern high-speed train propulsion systems incorporating advanced synchronous motor technology for improved energy efficiency and reliability.

• Growth of Energy-Efficient Motor Standards and Industrial Sustainability Initiatives: Global regulatory frameworks promoting high-efficiency motor technologies are accelerating the transition toward synchronous electric motors. More than 45 countries have introduced advanced motor efficiency standards equivalent to IE4 or higher, encouraging industries to replace legacy motor systems with high-efficiency alternatives. Industrial facilities adopting synchronous motors as part of energy optimization programs have reported electricity consumption reductions ranging between 12% and 20%. In addition, over 50% of newly constructed manufacturing plants now include energy-efficient motor systems as part of sustainability compliance strategies aimed at reducing carbon emissions and improving energy management performance across large-scale operations.

The synchronous electric motors market is structured across multiple segments including product type, application area, and end-user industry, each contributing distinct growth dynamics. Product type segmentation is dominated by permanent magnet synchronous motors and wound rotor synchronous motors, which serve various industrial and transportation applications. Permanent magnet designs are increasingly favored for their compact size and superior efficiency, especially in electric vehicles and robotics systems. Application segmentation highlights industrial machinery, power generation systems, and electric transportation as primary areas of deployment. Industrial manufacturing alone accounts for a significant portion of synchronous motor installations due to the demand for high-power compressors, pumps, and automated equipment. End-user segmentation includes manufacturing, energy and utilities, transportation, and infrastructure sectors. Rapid industrial modernization, electrification initiatives, and stricter energy-efficiency standards are encouraging industries to deploy synchronous motors across both existing facilities and new infrastructure projects, strengthening their role in global electrification strategies.

The synchronous electric motors market includes several product types such as permanent magnet synchronous motors, wound rotor synchronous motors, and hysteresis synchronous motors, each serving specialized industrial applications. Permanent magnet synchronous motors currently dominate the segment, accounting for approximately 46% of total installations due to their high efficiency, compact structure, and strong torque density. These motors are widely used in electric vehicles, robotics systems, and advanced automation equipment where precision motion control is critical. Wound rotor synchronous motors represent roughly 32% of the market and remain widely used in heavy industrial equipment such as compressors, pumps, and high-capacity conveyors that require stable rotational speed and large power capacity. Permanent magnet synchronous motors are also the fastest-growing segment, expanding at an estimated 6.1% annual growth rate due to increasing adoption in electric mobility and energy-efficient industrial drives. Their ability to deliver higher power density and reduced maintenance requirements compared to conventional motor designs has made them particularly attractive for next-generation manufacturing facilities and automated production lines. Other specialized types including hysteresis synchronous motors and reluctance synchronous motors collectively contribute nearly 22% of the market, serving niche applications such as precision instruments, aerospace equipment, and timing devices where constant speed performance is required.

Application segmentation in the synchronous electric motors market spans industrial machinery, electric vehicles, renewable energy systems, HVAC equipment, and transportation infrastructure. Industrial machinery remains the leading application segment, accounting for nearly 41% of total synchronous motor installations. These motors are widely used in pumps, compressors, conveyors, and processing equipment where stable speed control and high efficiency are essential for maintaining operational productivity. In large-scale manufacturing plants, synchronous motors have demonstrated energy consumption reductions of approximately 15% compared to older induction motor systems. Electric vehicles represent the fastest-growing application segment with an estimated growth rate of 7.3% annually. The rapid expansion of electric mobility is driving increased adoption of permanent magnet synchronous motors due to their superior torque density and energy efficiency. More than 70% of newly manufactured electric passenger vehicles now use synchronous motor technology for traction systems.Renewable energy generation, particularly wind power systems, accounts for roughly 22% of synchronous motor and generator installations. These systems rely on synchronous machines to maintain stable grid frequency and improve power generation efficiency.,Other applications such as HVAC systems, marine propulsion, and electric rail transport collectively contribute around 17% of total installations. Modern rail propulsion systems increasingly rely on synchronous traction motors capable of delivering high torque performance and efficient acceleration for high-speed trains.

The synchronous electric motors market serves a diverse range of end-users including manufacturing industries, energy and utilities, transportation, and infrastructure sectors. Manufacturing industries remain the dominant end-user segment, accounting for nearly 44% of global synchronous motor usage. Heavy industrial sectors such as steel production, chemical processing, mining, and automotive manufacturing rely heavily on synchronous motors to operate high-capacity compressors, pumps, and automated production equipment. The ability of synchronous motors to maintain consistent rotational speed while supporting large mechanical loads makes them essential in industrial environments requiring stable performance.

The transportation sector represents the fastest-growing end-user category with an estimated growth rate of approximately 6.5% annually. Increasing electrification of transportation systems including electric vehicles, rail propulsion, and electric buses is significantly boosting demand for high-performance synchronous motor technologies. Electric vehicles alone now account for nearly 28% of synchronous motor usage within the transportation sector. Energy and utilities contribute around 18% of market adoption through synchronous generator systems used in wind turbines, hydropower facilities, and power grid stabilization equipment. Infrastructure sectors such as water treatment plants, large commercial buildings, and metro transportation systems account for the remaining 10% of installations.

Asia Pacific accounted for the largest market share at 42% in 2025 however, Region North America is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

The synchronous electric motors market shows strong regional variations influenced by industrial development, electrification initiatives, and infrastructure modernization. Asia Pacific leads global installations due to its massive manufacturing sector and expanding electric mobility ecosystem. China alone operates more than 45% of global industrial motor manufacturing facilities, producing over 300 million electric motors annually, including a large volume of synchronous motors used in heavy industry and transportation. Japan and South Korea are also key technology hubs, contributing advanced permanent magnet motor innovations. North America follows with around 27% of total installations driven by energy-efficient motor replacement programs across manufacturing and utilities. Europe represents nearly 21% of the global synchronous motor demand due to strict energy-efficiency regulations and rapid electrification of transportation infrastructure. Meanwhile, South America and the Middle East & Africa collectively account for approximately 10% of the global market, supported by mining operations, oil and gas infrastructure, and renewable energy developments. Increasing investments in industrial automation and smart manufacturing systems are expected to influence future regional growth patterns.

How are advanced industrial automation and energy regulations accelerating high-efficiency motor adoption?

North America represents approximately 27% of global synchronous electric motors installations, driven largely by industrial modernization and electrification initiatives across the United States and Canada. Manufacturing sectors such as automotive production, oil and gas processing, and aerospace engineering are key contributors to demand for high-performance synchronous motors. More than 60% of large manufacturing plants in the region have implemented energy-efficient motor replacement programs to reduce electricity consumption and operational costs. Government energy efficiency policies promoting IE4 and IE5 motor standards are encouraging industries to upgrade legacy induction motors. Technological transformation is also evident, with nearly 48% of industrial facilities integrating IoT-based motor monitoring systems for predictive maintenance and operational optimization. A regional motor manufacturer recently introduced a high-torque permanent magnet synchronous motor designed for heavy industrial compressors capable of improving mechanical efficiency by approximately 18%. Consumer and enterprise behavior in this region shows strong adoption among industrial automation providers, particularly in sectors such as aerospace manufacturing, data center cooling systems, and precision machinery.

What factors are accelerating industrial electrification and high-efficiency motor deployment across advanced manufacturing ecosystems?

Europe accounts for approximately 21% of the global synchronous electric motors market, with strong demand originating from Germany, the United Kingdom, France, and Italy. Germany alone operates over 8,000 advanced manufacturing facilities that increasingly deploy high-efficiency synchronous motors for robotics and industrial automation. Sustainability regulations across the region are a major driver, with strict efficiency standards encouraging replacement of older motor technologies. Nearly 52% of industrial companies in the region have adopted advanced motor efficiency upgrades aligned with sustainability targets. The expansion of renewable energy infrastructure is another important contributor, particularly wind power systems that require synchronous generators for stable electricity generation. Several motor manufacturers in the region have introduced digital control platforms capable of improving equipment reliability by up to 20% through predictive monitoring. Regional enterprise behavior strongly reflects regulatory pressure, with industries prioritizing energy-efficient machinery and transparent performance monitoring technologies to comply with environmental standards and carbon-reduction targets.

Why is large-scale industrial production driving the fastest expansion of advanced motor technologies?

Asia-Pacific holds the highest market volume globally, accounting for approximately 42% of synchronous electric motor installations. The region’s dominance is supported by massive industrial manufacturing capacity across China, Japan, India, and South Korea. China alone manufactures more than 310 million industrial motors annually and accounts for nearly half of global electric vehicle motor production. Japan remains a major innovation hub for high-precision synchronous motors used in robotics, while India is rapidly expanding demand through industrial automation and infrastructure development. The region has more than 120 large motor manufacturing clusters specializing in high-efficiency electric drive systems. Technological advancements such as permanent magnet rotor designs and digital motor control systems are increasingly integrated into manufacturing equipment across electronics and automotive sectors. A major regional motor manufacturer recently launched an advanced synchronous motor designed for automated production lines capable of delivering nearly 22% greater torque density compared with traditional designs. Consumer and enterprise behavior across this region strongly reflects rapid industrialization and large-scale electrification programs.

How are mining expansion and industrial modernization shaping demand for high-performance electric motors?

South America accounts for roughly 6% of the global synchronous electric motors market, with Brazil and Argentina emerging as the primary consuming countries. Brazil alone contributes nearly 60% of the region’s industrial motor demand due to its large mining, steel production, and agricultural processing industries. Synchronous motors are widely deployed in heavy-duty compressors, pumps, and conveyor systems used in mineral extraction operations. The region has more than 400 major mining facilities that rely on high-capacity motor systems to operate large mechanical equipment. Governments are also promoting renewable energy infrastructure development, particularly wind power installations that require synchronous generator systems for grid stability. Industrial modernization programs across several countries have encouraged replacement of older mechanical equipment with energy-efficient motor technologies capable of reducing power consumption by approximately 15%. Consumer behavior in the region is closely linked to infrastructure investment and industrial expansion, with strong demand coming from mining operations, manufacturing plants, and power generation facilities.

What role do energy infrastructure and industrial diversification play in accelerating motor adoption?

The Middle East & Africa region represents nearly 4% of global synchronous electric motor installations but is steadily expanding due to growing investments in energy infrastructure and industrial diversification. Major growth markets include the United Arab Emirates, Saudi Arabia, and South Africa where synchronous motors are used extensively in oil refining facilities, water treatment plants, and large-scale construction projects. The region operates more than 500 large oil and gas processing facilities requiring high-capacity electric drive systems capable of maintaining constant operational speed under heavy loads. Governments are investing heavily in industrial automation and renewable energy projects as part of economic diversification strategies. For instance, solar and wind power installations across the Gulf region increasingly rely on synchronous generator systems for efficient power conversion. Industrial technology modernization is also visible in new smart infrastructure projects integrating digital monitoring systems that improve equipment performance by nearly 16%. Consumer behavior across this region is strongly tied to energy infrastructure development and large-scale industrial projects.

• China – 29% market share in the Synchronous Electric Motors Market, supported by extensive industrial motor manufacturing capacity and strong electric vehicle motor production.

• United States – 21% market share in the Synchronous Electric Motors Market, driven by high adoption in industrial automation, aerospace manufacturing, and energy infrastructure modernization.

The synchronous electric motors market features a moderately consolidated competitive structure with approximately 35 to 40 active global manufacturers competing across industrial, transportation, and energy sectors. The top five companies collectively control nearly 48% of global installations, supported by extensive product portfolios, large-scale manufacturing capabilities, and global distribution networks. Leading manufacturers focus heavily on high-efficiency permanent magnet synchronous motors, advanced motor control systems, and integrated digital monitoring technologies. Continuous innovation in rotor design, high-performance magnetic materials, and power electronics integration has become a key differentiator among competitors.

Product development and strategic partnerships remain common competitive strategies. Several manufacturers have recently introduced high-efficiency synchronous motors capable of achieving operational efficiencies above 95% for heavy industrial applications. Many companies are also expanding research and development investments to improve torque density and reduce dependence on rare earth materials. Industrial automation providers are increasingly collaborating with motor manufacturers to integrate synchronous motors into robotics systems and advanced manufacturing equipment.

The competitive environment is further influenced by mergers, joint ventures, and global manufacturing expansions. Many companies operate production facilities across Asia, Europe, and North America to support supply chain resilience and regional market demand. Additionally, the integration of digital motor monitoring platforms and predictive maintenance technologies is becoming a critical innovation area, allowing manufacturers to differentiate their solutions in highly automated industrial environments.

ABB

Siemens

WEG

Toshiba

Mitsubishi Electric

Nidec Corporation

Regal Rexnord Corporation

Rockwell Automation

Schneider Electric

Hitachi Industrial Equipment Systems

Yaskawa Electric Corporation

Hyundai Electric

CG Power and Industrial Solutions

Brook Crompton

Johnson Electric

Technological advancements are playing a central role in reshaping the synchronous electric motors market, particularly through improvements in energy efficiency, materials engineering, and digital integration. One of the most significant developments is the widespread adoption of permanent magnet synchronous motor (PMSM) technology, which can achieve efficiency levels above 95% while delivering torque densities up to 30% higher than traditional induction motors. These motors are widely deployed in electric vehicles, robotics, high-speed compressors, and precision manufacturing equipment where performance stability and energy efficiency are critical. Another key technology influencing the market is the use of advanced magnetic materials such as neodymium-iron-boron magnets. These materials enable compact motor designs while delivering stronger magnetic fields, allowing manufacturers to reduce motor size by nearly 20% while maintaining high power output. In electric vehicle applications, synchronous motors equipped with advanced magnet technology can deliver peak efficiencies of around 97%, improving vehicle range and drivetrain performance.

Digital motor control technologies are also transforming synchronous motor systems. Modern motor drives now incorporate high-speed digital signal processors capable of monitoring rotational speed, temperature, torque load, and vibration levels in real time. Approximately 45% of new industrial synchronous motors are now paired with intelligent variable frequency drives that optimize energy consumption and improve performance under fluctuating load conditions. These systems can reduce electricity consumption in industrial operations by nearly 15%. In addition, predictive maintenance technologies powered by artificial intelligence are being integrated into industrial motor platforms. Smart sensors embedded within motor assemblies collect operational data that can detect early signs of mechanical wear or electrical faults. Facilities implementing predictive monitoring systems have reported downtime reductions of nearly 28% and maintenance cost reductions of around 20%.

• In April 2025, ABB introduced its next-generation high-efficiency synchronous motor platform designed for heavy industrial applications. The new motors achieve efficiency levels exceeding 96% and support digital condition monitoring systems that enable predictive maintenance and improved equipment reliability in manufacturing and energy facilities. Source: www.abb.com

• In October 2024, Siemens expanded its SIMOTICS synchronous motor portfolio by launching advanced permanent magnet motors optimized for electric vehicle production equipment and high-speed industrial automation systems. The new design improves torque density by approximately 15% and supports digital integration with industrial IoT monitoring platforms. Source: www.siemens.com

• In February 2025, Nidec Corporation announced the development of a high-performance traction synchronous motor for electric vehicles capable of achieving 97% efficiency. The motor incorporates improved cooling technology and compact magnet architecture designed to enhance vehicle power density and extend driving range.

• In November 2024, WEG introduced a new synchronous motor series designed for large compressors and pumps used in oil, gas, and mining industries. The motors feature enhanced rotor design and advanced insulation systems capable of increasing operational reliability by nearly 20% under heavy industrial load conditions. Source: www.weg.net

The Synchronous Electric Motors Market Report provides a comprehensive analysis of the global industry landscape, covering a wide range of market segments, technological developments, and industrial applications. The report examines synchronous electric motors used across multiple power ranges, from small precision motors used in automation equipment to high-capacity industrial motors exceeding 10 megawatts deployed in power generation and heavy manufacturing operations. It evaluates motor types including permanent magnet synchronous motors, wound rotor synchronous motors, and specialized synchronous designs used in high-performance applications. The report analyzes key industry sectors utilizing synchronous motors such as manufacturing, electric mobility, renewable energy, infrastructure systems, and industrial processing. Manufacturing industries account for a significant portion of motor installations due to widespread use in compressors, conveyors, pumps, and automated production equipment. The transportation sector is also examined extensively, particularly the adoption of synchronous motors in electric vehicles, high-speed rail systems, and electric buses where high torque density and efficiency are essential performance requirements.

Geographically, the report covers major industrial regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Asia-Pacific currently represents the largest manufacturing hub for electric motors with more than 300 million units produced annually across various motor technologies. The report evaluates regional consumption patterns, manufacturing clusters, and industrial infrastructure developments influencing demand for synchronous electric motors. Technological analysis within the report focuses on advanced motor materials, digital motor control systems, smart monitoring technologies, and emerging high-efficiency designs. It also explores the growing integration of synchronous motors within electrified transportation systems and renewable energy infrastructure. In addition, the report evaluates supply chain dynamics, production capacity expansions, and industrial automation trends shaping the future direction of the synchronous electric motors market across both developed and emerging economies.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ABB, Siemens, WEG, Toshiba, Mitsubishi Electric, Nidec Corporation, Regal Rexnord Corporation, Rockwell Automation, Schneider Electric, Hitachi Industrial Equipment Systems, Yaskawa Electric Corporation, Hyundai Electric, CG Power and Industrial Solutions, Brook Crompton, Johnson Electric |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |