Reports

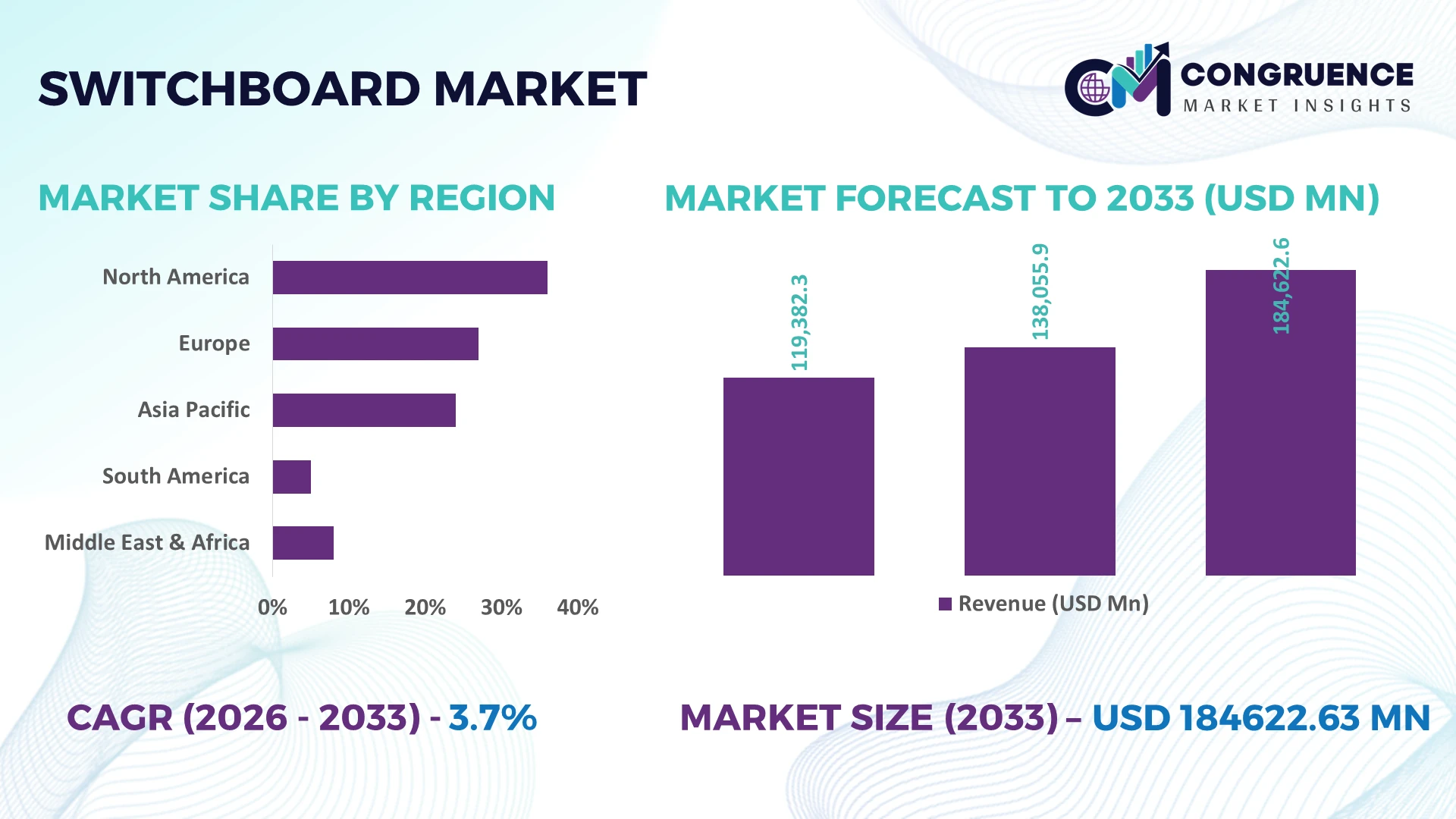

The Global Switchboard Market was valued at USD 138055.87 Million in 2025 and is anticipated to reach a value of USD 184622.63 Million by 2033 expanding at a CAGR of 3.7% between 2026 and 2033. Rising grid modernization projects, industrial electrification, renewable energy integration, and digital power distribution infrastructure are accelerating deployment of intelligent switchboard systems with advanced monitoring and protection capabilities.

The United States dominates the global switchboard market with approximately 28% of installed demand, supported by nationwide grid upgrades, more than 210 GW of utility-scale renewable power capacity, and expanding investments in data centers, semiconductor manufacturing, and industrial facilities. Compared with Germany, where adoption is driven primarily by energy-efficient industrial automation, the U.S. benefits from larger infrastructure replacement programs following the Infrastructure Investment and Jobs Act, reinforcing leadership in advanced electrical distribution equipment deployment.

Strategic investments in digital switchboards, localized manufacturing, and intelligent power management solutions will determine long-term competitiveness as critical infrastructure modernization accelerates worldwide.

Market Size & Growth: USD 138055.87 Million (2025) to USD 184622.63 Million (2033) at 3.7% CAGR, supported by smart grid expansion and industrial electrification.

Top Growth Drivers: Renewable integration (+31%), industrial automation (+27%), infrastructure modernization (+24%) continue strengthening global demand.

Short-Term Forecast: By 2028, predictive maintenance lowers equipment downtime by 19% while operational efficiency improves 16%.

Emerging Technologies: AI-powered diagnostics, IoT-enabled monitoring, and digital twin platforms enhance switchboard performance and lifecycle management.

Regional Leaders: Asia-Pacific exceeds USD 63 Billion, North America reaches USD 50 Billion, while Europe surpasses USD 44 Billion through smart-grid investments.

Consumer/End-User Trends: More than 61% of new industrial facilities specify intelligent monitoring and remote asset management capabilities.

Pilot/Case Example: A 2026 smart manufacturing deployment improved electrical reliability by 21% and maintenance response time by 24%.

Competitive Landscape: Leading supplier holds approximately 12% market share alongside ABB, Siemens, Schneider Electric, Eaton, and Legrand.

Regulatory & ESG Impact: Updated energy-efficiency standards reduce electrical distribution losses by up to 13% across upgraded installations.

Investment & Funding: More than USD 12 Billion supports production expansion, regional manufacturing, and strategic supply-chain localization initiatives.

Innovation & Future Outlook: Modular digital switchboards, cybersecurity-enabled control systems, and predictive analytics strengthen resilient global electrical infrastructure.

The Switchboard Market is expanding across utilities, commercial buildings, manufacturing plants, renewable energy facilities, and hyperscale data centers as organizations prioritize intelligent power distribution and operational resilience. Digital protection relays, modular architectures, and cloud-connected monitoring platforms continue advancing product innovation, while nearly 47% of newly commissioned industrial projects specify smart electrical distribution systems. Supply-chain localization and evolving electrical safety regulations are reshaping procurement priorities, providing a strong foundation for the strategic market discussion.

The Switchboard Market has become strategically significant as governments and private utilities accelerate grid modernization, industrial electrification, and resilient power infrastructure investments. Digital substations, renewable integration, and expanding hyperscale data centers are redefining procurement priorities, while supply-chain restructuring encourages localized production of electrical equipment. Manufacturers increasingly compete through intelligent monitoring capabilities, lifecycle services, and modular product portfolios rather than conventional hardware differentiation.

Digitally enabled switchboards equipped with IoT diagnostics and predictive maintenance reduce maintenance costs by approximately 22% and improve fault detection efficiency by nearly 30% compared with conventional switchboards requiring manual inspection. China continues leading large-scale manufacturing capacity and infrastructure deployment, while Germany emphasizes high-efficiency industrial automation and compliance-driven electrical upgrades across advanced production facilities. Over the next two to three years, intelligent monitoring functionality is expected to be incorporated into more than 55% of newly commissioned industrial switchboard installations, reflecting the transition toward connected power distribution systems.

A recent industrial facility modernization project integrated smart switchboards with energy management software, reducing electrical downtime by 18% while improving asset utilization across multiple production lines. Manufacturers are responding through localized production expansion, software partnerships, and digital service investments to strengthen lifecycle support. Companies capable of combining intelligent electrical infrastructure with resilient manufacturing operations will secure stronger competitive positioning as critical infrastructure modernization accelerates.

Utility infrastructure replacement and industrial electrification remain the primary structural drivers supporting switchboard deployment. More than 64% of newly commissioned manufacturing facilities now specify intelligent electrical distribution equipment, while digital monitoring systems reduce unplanned outages by approximately 25% and maintenance intervention by 20%. The United States continues expanding transmission and distribution modernization programs, increasing demand for advanced switchboards capable of supporting renewable integration and critical facilities. In response, manufacturers are expanding localized production, introducing modular product platforms, and forming technology partnerships to integrate predictive diagnostics and remote monitoring. The strategic advantage increasingly lies in delivering standardized, software-enabled switchboards that improve operational continuity while reducing lifecycle maintenance requirements.

Persistent volatility in copper, aluminum, and electrical component sourcing continues affecting production costs and procurement planning. Material prices have fluctuated by nearly 18% over recent procurement cycles, while specialized electronic component lead times remain approximately 20% above historical averages for several manufacturers. India and several emerging industrial economies continue facing project delays because localized component ecosystems remain underdeveloped for advanced switchboard assemblies. These constraints increase inventory costs, extend installation schedules, and compress project margins. Manufacturers are mitigating exposure through supplier diversification, regional manufacturing expansion, long-term procurement agreements, and greater component standardization to improve production flexibility and strengthen supply-chain resilience.

Digital transformation is expanding opportunities beyond conventional electrical distribution by integrating switchboards with energy management, predictive analytics, and industrial automation platforms. Smart monitoring solutions improve electrical asset utilization by approximately 21%, while remote diagnostics reduce inspection costs by nearly 19%. Japan continues investing in intelligent factory infrastructure where connected electrical systems support automation and energy optimization objectives. Manufacturers are increasing investment in embedded sensors, AI-assisted diagnostics, and cloud-based monitoring ecosystems while forming partnerships with industrial software providers. The strongest long-term opportunity lies in delivering integrated electrical intelligence that combines operational visibility, predictive maintenance, and energy efficiency within a unified infrastructure platform.

The transition toward digitally connected switchboards introduces significant execution challenges across interoperability, workforce capability, and cybersecurity management. Approximately 43% of industrial facilities continue operating mixed legacy and digital electrical infrastructure, increasing system integration complexity, while cybersecurity incidents targeting operational technology environments have risen by nearly 30% in recent years. Germany and the United States are strengthening cybersecurity requirements for critical electrical infrastructure, increasing compliance obligations for manufacturers. Companies must invest in secure communication protocols, engineering expertise, software validation, and lifecycle support partnerships to ensure reliable deployment. Organizations that successfully integrate secure digital functionality with standardized electrical architectures will strengthen long-term operational competitiveness and customer retention.

Smart Monitoring Becomes Standard: Industrial operators are integrating IoT-enabled switchboards into electrical distribution networks, with intelligent monitoring specified in nearly 58% of new industrial projects and predictive diagnostics reducing maintenance interventions by 24%. Stricter electrical reliability requirements and workforce shortages are accelerating remote asset management, prompting manufacturers to expand software partnerships, embedded analytics, and cloud-enabled lifecycle service offerings.

Modular Designs Accelerate Deployment: Prefabricated and modular switchboard architectures reduce installation time by approximately 30% while lowering on-site commissioning activities by 18%. Large manufacturing projects in the United States and India increasingly prioritize standardized configurations to minimize construction delays and labor dependency. Suppliers are restructuring production with modular product platforms and localized assembly operations to improve delivery speed and operational flexibility.

Localized Supply Chains Expand: Manufacturers are shifting component sourcing closer to end markets, reducing average procurement lead times by nearly 20% and inventory exposure by 15%. Rising geopolitical uncertainty and stricter domestic procurement policies are encouraging production expansion in countries with established electrical manufacturing ecosystems. Companies are strengthening supplier partnerships, qualifying secondary vendors, and increasing regional production capacity to improve fulfillment resilience.

Digital Protection Systems Advance: Intelligent protection relays and cybersecurity-enabled switchboards are becoming integral to critical infrastructure, improving fault isolation accuracy by approximately 28% while reducing restoration time by 17%. Utilities and data center operators increasingly require secure communication protocols alongside conventional electrical protection. Manufacturers are embedding advanced firmware, secure network architectures, and software update capabilities into next-generation switchboards, creating long-term service differentiation beyond equipment sales.

Low Voltage switchboards remain the dominant segment because they serve commercial buildings, manufacturing facilities, healthcare infrastructure, and data centers where scalable, cost-efficient electrical distribution is essential. Nearly 52% of new building electrical installations specify low-voltage systems due to lower installation complexity, easier maintenance, and compatibility with intelligent monitoring platforms. Main Switchboards continue serving as the primary distribution backbone for large facilities, while Distribution Switchboards strengthen downstream power management through modular expansion and simplified maintenance. Manufacturers are introducing compact digital architectures and standardized product families to improve installation flexibility and lifecycle performance.

Medium Voltage switchboards represent the fastest-growing segment as utilities, renewable energy projects, and industrial facilities modernize electrical infrastructure requiring higher operational reliability. Adoption has increased by approximately 19% across grid modernization projects, while digital protection integration exceeds 40% in newly commissioned utility installations. High Voltage switchboards remain strategically important for transmission infrastructure and large industrial campuses, supporting long-term grid resilience. Companies continue investing in intelligent protection technologies, localized manufacturing, and product innovation to address changing infrastructure requirements and strengthen competitive differentiation.

Power Distribution continues leading application demand because every industrial, commercial, and institutional facility depends on reliable electrical control and protection. Approximately 60% of new switchboard deployments support primary distribution infrastructure, driven by grid modernization, facility expansion, and electrical reliability upgrades. Utilities continue expanding transmission and distribution assets, while Commercial Buildings increasingly deploy intelligent switchboards to improve energy monitoring and operational efficiency. Manufacturers are scaling modular product portfolios and integrating advanced monitoring capabilities to support increasingly digital electrical networks.

Renewable Energy represents the fastest-growing application as solar, wind, and battery storage projects require sophisticated power management and protection systems. Deployment across renewable installations has increased by nearly 23%, while Industrial Plants continue upgrading legacy electrical infrastructure with automated switchboard systems that improve maintenance productivity by approximately 20%. Companies are expanding engineering partnerships, integrating renewable-compatible protection technologies, and strengthening manufacturing capacity to support evolving infrastructure requirements across multiple application environments.

Utilities remain the largest end-user segment because national grid expansion, substation modernization, and distribution network upgrades require extensive switchboard deployment. Nearly 46% of large infrastructure procurement programs include advanced switchboard systems supporting network reliability and digital monitoring capabilities. Manufacturing follows as the fastest-evolving industrial buyer, with automated production facilities increasingly replacing conventional electrical infrastructure to improve operational continuity. Suppliers are strengthening utility-focused engineering services, expanding localized production, and offering customized protection solutions to secure long-term procurement contracts.

Manufacturing represents the fastest-growing end-user as industrial automation, electrification, and smart factory investments accelerate equipment replacement cycles. Adoption of intelligent switchboards has increased by approximately 21% across newly commissioned manufacturing facilities, while Commercial Buildings continue integrating connected electrical infrastructure to improve energy optimization. Construction maintains stable demand through large infrastructure developments, whereas Oil & Gas focuses on ruggedized switchboards for high-reliability environments. Manufacturers are responding through sector-specific product customization, strategic technology alliances, and lifecycle service offerings that improve customer retention and operational performance.

North America accounted for the largest market share at 34.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 4.6% CAGR between 2026 and 2033.

Grid modernization strengthens digital electrical infrastructure

North America remains the largest regional market as utilities, hyperscale data centers, semiconductor manufacturing, and commercial infrastructure continue replacing aging electrical distribution assets. More than 34% of global switchboard deployments are concentrated across the region, supported by extensive transmission upgrades and industrial automation investments. Intelligent switchboards equipped with predictive monitoring are increasingly specified for critical infrastructure projects, while localized manufacturing improves procurement resilience. Utilities and engineering firms are expanding strategic partnerships to integrate digital protection systems, reducing maintenance interventions by nearly 22% and improving operational continuity across industrial facilities.

United States Market Outlook: The United States leads regional deployment through large-scale investments in transmission infrastructure, advanced manufacturing, and hyperscale data centers. Utility modernization programs continue accelerating replacement of legacy electrical systems with intelligent switchboards supporting remote diagnostics and cybersecurity-enabled protection. More than 60% of newly commissioned industrial facilities now incorporate digitally connected electrical distribution platforms, while domestic manufacturing expansion and semiconductor investments strengthen long-term procurement demand for advanced switchboard technologies.

Energy transition drives infrastructure modernization

Europe continues strengthening its position through industrial decarbonization, grid modernization, and stricter electrical efficiency standards. Approximately 25% of global switchboard deployment is associated with European industrial infrastructure, where manufacturers prioritize intelligent monitoring, modular architectures, and energy-efficient distribution systems. Utility operators continue upgrading substations supporting renewable integration, while industrial automation projects increase demand for advanced protection technologies. Cross-border electricity infrastructure expansion and digital substation deployment continue improving network resilience while encouraging suppliers to expand localized engineering and manufacturing capabilities.

Germany Market Outlook: Germany remains the regional technology leader through advanced manufacturing, industrial automation, and electrical engineering expertise. Factory modernization initiatives continue replacing conventional switchboards with intelligent electrical control systems capable of supporting automated production environments. Digital monitoring functionality has been incorporated into more than half of newly modernized industrial electrical installations, while engineering companies continue investing in software-integrated switchboard platforms that improve operational efficiency and equipment reliability.

Manufacturing expansion accelerates deployment scale

Asia-Pacific represents the fastest-expanding regional market as industrialization, urban infrastructure development, renewable energy deployment, and manufacturing investments continue increasing electrical distribution requirements. The region contributes approximately 31% of global switchboard production capacity, supported by strong domestic manufacturing ecosystems and expanding infrastructure projects. Large-scale factory construction, commercial development, and utility modernization are increasing deployment volumes, while manufacturers strengthen export capabilities through production automation and localized component sourcing. Investment in intelligent manufacturing continues improving production efficiency and delivery performance across electrical equipment suppliers.

China Market Outlook: China dominates regional production through integrated electrical equipment manufacturing, extensive utility expansion, and large-scale industrial infrastructure projects. Government-backed modernization programs continue supporting intelligent power distribution technologies across manufacturing clusters and renewable energy developments. More than 40% of regional switchboard production capacity is concentrated within China, enabling manufacturers to strengthen export competitiveness while accelerating adoption of digital monitoring and modular electrical distribution systems.

Infrastructure investment reshapes industrial demand

South America continues expanding switchboard deployment through power infrastructure upgrades, mining investments, and industrial modernization initiatives. Although representing a smaller share of global demand, electrical infrastructure replacement projects are increasing procurement activity across utilities and manufacturing facilities. Renewable power integration and urban development continue supporting demand for reliable electrical distribution systems. Manufacturers are strengthening distributor partnerships and regional assembly operations to improve delivery responsiveness, while infrastructure funding gradually enhances deployment consistency despite ongoing logistics and procurement challenges.

Brazil Market Outlook: Brazil leads regional demand through transmission expansion, industrial production, and renewable energy development. Large manufacturing facilities and utility operators continue replacing aging electrical infrastructure with digitally enabled switchboards supporting improved operational reliability. Utility modernization initiatives and expanding commercial construction activity have increased demand for intelligent distribution systems, encouraging suppliers to establish stronger local engineering support and regional manufacturing partnerships.

Strategic infrastructure investment transforms electrical networks

The Middle East & Africa market is benefiting from sustained investment in utility expansion, smart city developments, oil and gas infrastructure, and commercial construction. Modern electrical distribution systems are increasingly specified for mission-critical infrastructure requiring operational resilience and remote monitoring capabilities. Infrastructure modernization programs continue supporting deployment of advanced switchboards across industrial facilities, airports, and utility projects. International manufacturers are expanding regional partnerships, localized service networks, and engineering capabilities to improve project execution and lifecycle support for large infrastructure developments.

Saudi Arabia Market Outlook: Saudi Arabia remains the region's most influential market through major infrastructure diversification programs, industrial cities, utility modernization, and large commercial developments. Digital electrical infrastructure is becoming standard across new industrial and smart city projects, while utility investments continue strengthening demand for intelligent switchboards capable of supporting high-reliability power distribution. Ongoing industrial diversification and large-scale infrastructure construction continue creating sustained procurement opportunities for advanced electrical equipment manufacturers.

The competitive landscape is led by ABB, Siemens, Schneider Electric, Eaton, and Legrand, competing directly against diversified electrical equipment manufacturers and fast-growing regional producers across Asia. The top five companies collectively account for approximately 46% of global market share, while regional manufacturers compete through localized production and pricing advantages. Global leaders differentiate through digital switchboards, cybersecurity integration, and lifecycle services, whereas regional suppliers focus on shorter lead times and customized engineering. Intelligent monitoring platforms improve maintenance efficiency by nearly 24%, while modular production reduces project delivery time by approximately 18%, strengthening technology-led differentiation. Companies continue expanding manufacturing capacity, forming software partnerships, investing in digital protection systems, and increasing vertical integration to secure critical electrical components. Competition is shifting toward software-enabled electrical infrastructure as supply-chain resilience and digital functionality become purchasing priorities. High certification requirements, engineering expertise, and established service networks create significant entry barriers for new participants. Winning requires integrated hardware, intelligent software, resilient manufacturing, rapid delivery, and long-term customer support capabilities.

ABB

Siemens

Schneider Electric

Eaton

Legrand

Mitsubishi Electric

Fuji Electric

Hitachi Energy

Toshiba Energy Systems & Solutions

Powell Industries

Lucy Electric

Hyundai Electric & Energy Systems

Larsen & Toubro

CHINT Group

Digitalization is transforming switchboard technology through IoT-enabled monitoring, intelligent protection relays, AI-assisted diagnostics, and cloud-connected asset management. More than 57% of newly specified industrial switchboards now incorporate remote monitoring capabilities, while predictive diagnostics reduce maintenance interventions by approximately 25%. Manufacturers increasingly integrate cybersecurity features, digital communication protocols, and real-time analytics into electrical distribution systems, allowing operators to improve asset reliability and optimize maintenance planning. These technologies provide measurable operational advantages for utilities, industrial facilities, and mission-critical infrastructure where uninterrupted power distribution is essential.

Compared with conventional switchboards requiring periodic manual inspection, intelligent digital switchboards improve fault detection accuracy by nearly 30% and reduce maintenance costs by approximately 22%. Modular digital architectures also shorten commissioning time by about 20%, enabling faster project delivery. Global technology leaders benefit from integrated software ecosystems and engineering expertise, while industrial customers gain higher operational visibility, improved compliance, and reduced lifecycle costs through connected electrical infrastructure.

Between 2026 and 2028, digital twin integration, edge computing, and AI-driven energy optimization will become mainstream across industrial electrical networks. Adoption of intelligent switchboards is expected to exceed 60% in newly commissioned critical infrastructure projects, driven by grid modernization and industrial automation. Companies investing now in secure communication protocols, software platforms, and predictive maintenance capabilities will strengthen competitive positioning, accelerate service-based business models, and establish long-term differentiation as intelligent electrical distribution becomes the industry standard.

June 2025: Siemens partnered with Cadolto and Legrand to introduce a modular edge data center integrating SIVACON power distribution and switchboard technologies. The prefabricated solution reduces deployment planning cycles to 6–12 months, enabling faster AI-ready infrastructure delivery and scalable electrical distribution. Source: press.siemens.com

August 2025: Schneider Electric signed a long-term framework agreement with E.ON to accelerate deployment of SF₆-free medium-voltage switchgear across European electricity networks ahead of new regulatory requirements. The partnership supports 100% SF₆-free deployment for covered projects, strengthening sustainable grid modernization. Source: se.com

April 2026: Siemens launched its new direct-current switching portfolio featuring the SENTRON 3QD2 semiconductor circuit breaker, delivering fault interruption up to 1,000 times faster than conventional systems while enabling up to 80% lower peak power consumption in selected DC applications. The innovation strengthens next-generation switchboard performance for data centers and industrial facilities. Source: press.siemens.com

June 2026: ABB expanded its collaboration with NVIDIA by integrating digital models of medium-voltage switchgear and electrical distribution equipment into the Omniverse DSX Blueprint platform. The solution compresses engineering design cycles through digital-twin validation before construction, improving project execution for AI infrastructure deployments.

The report provides comprehensive analysis of the global Switchboard Market across Low Voltage, Medium Voltage, High Voltage, Main Switchboards, and Distribution Switchboards, while evaluating demand across power distribution, industrial plants, commercial buildings, utilities, renewable energy, and major end-user industries. It assesses deployment patterns across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating operational trends, technology adoption, manufacturing developments, and competitive positioning. More than 60% of recent industrial installations emphasize intelligent monitoring and digital electrical infrastructure.

The study examines emerging technologies including AI-enabled diagnostics, IoT-connected monitoring, modular architectures, cybersecurity-enabled protection, and predictive maintenance platforms. It evaluates competitive strategies across leading manufacturers, investment priorities, supply-chain localization, infrastructure modernization, and enterprise partnerships between 2026 and 2033. The report delivers actionable insights supporting expansion planning, product portfolio optimization, procurement strategies, regional prioritization, risk assessment, and long-term competitive positioning across both mature and emerging electrical infrastructure markets.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 138055.87 Million |

Market Revenue in 2033 | USD 184622.63 Million |

CAGR (2026 - 2033) | 3.7% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | ABB, Siemens, Schneider Electric, Eaton, Legrand, Mitsubishi Electric, Fuji Electric, Hitachi Energy, Toshiba Energy Systems & Solutions, Powell Industries, Lucy Electric, Hyundai Electric & Energy Systems, Larsen & Toubro, CHINT Group |

Customization & Pricing | Available on Request (10% Customization is Free) |