Reports

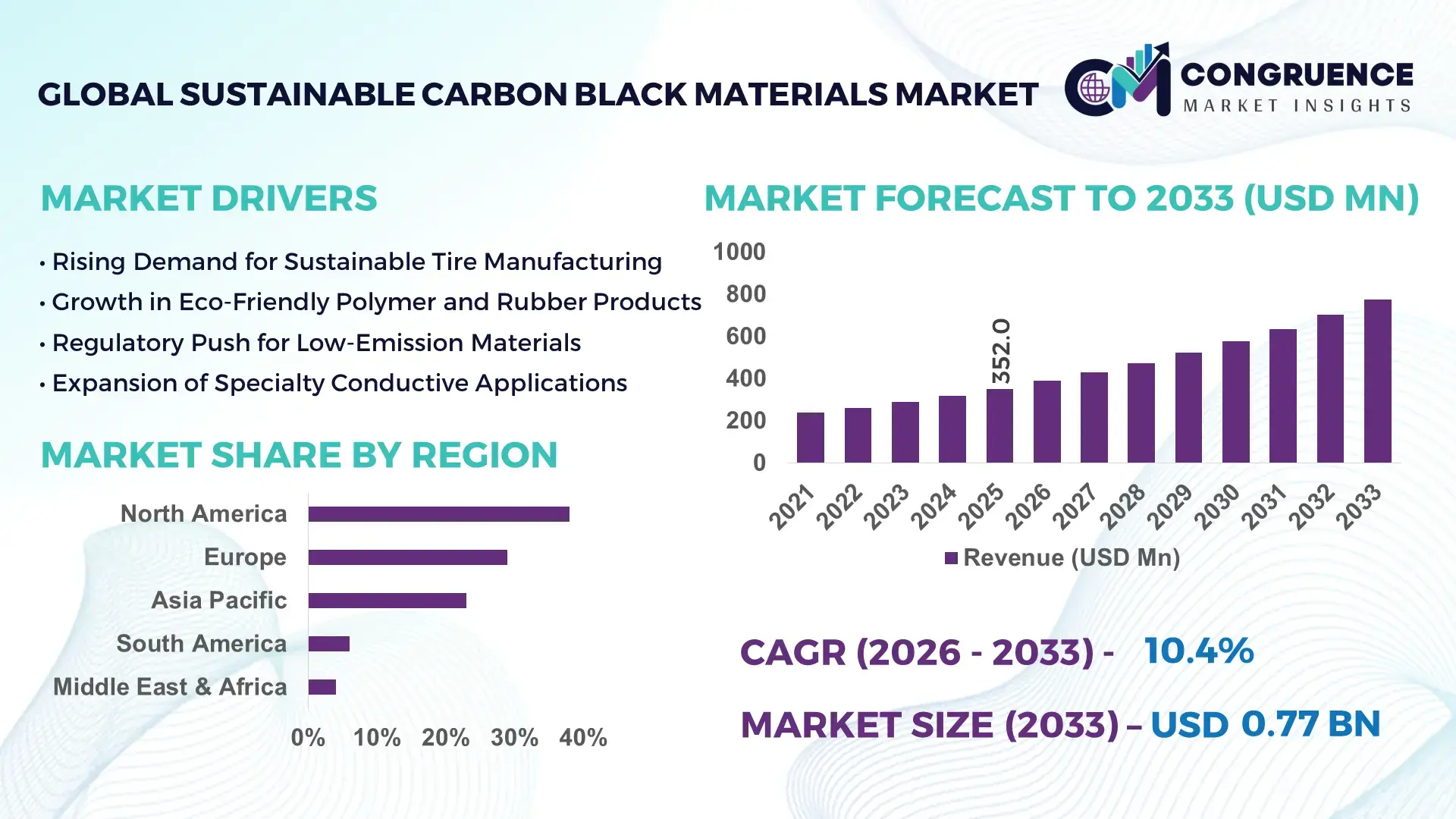

The Global Sustainable Carbon Black Materials Market was valued at USD 352.0 Million in 2025 and is anticipated to reach a value of USD 774.0 Million by 2033 expanding at a CAGR of 10.35% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market growth is primarily driven by increasing adoption of circular economy practices and rising regulatory pressure to reduce carbon emissions across tire, plastics, and coatings industries.

The United States represents the dominant country in the Sustainable Carbon Black Materials Market, supported by advanced tire recycling infrastructure and strong investment in recovered carbon black (rCB) technologies. The U.S. processes over 300 million end-of-life tires annually, with approximately 20–25% directed toward advanced pyrolysis and material recovery systems. Installed rCB production capacity in the country exceeds 150 kilotons per year, supported by multi-million-dollar investments in automated pyrolysis plants across Texas, Ohio, and California. Key applications include tire manufacturing, accounting for nearly 65% of domestic rCB utilization, followed by plastics and industrial rubber goods at approximately 20%. Adoption of closed-loop recycling technologies and AI-enabled quality control systems has improved yield efficiency by 15–18% in large-scale facilities, reinforcing industrial-scale deployment of sustainable carbon black materials.

Market Size & Growth: USD 352.0 Million in 2025, projected to reach USD 774.0 Million by 2033 at 10.35% CAGR, driven by circular economy mandates and sustainable tire production targets.

Top Growth Drivers: 42% increase in recycled tire utilization, 35% reduction in lifecycle emissions demand, 28% growth in green procurement policies.

Short-Term Forecast: By 2028, advanced pyrolysis systems are expected to improve material recovery efficiency by 22% and reduce processing costs by 18%.

Emerging Technologies: AI-enabled feedstock optimization, continuous pyrolysis reactors, plasma-based carbon recovery systems.

Regional Leaders: North America projected at USD 285.0 Million by 2033 with strong tire recycling adoption; Europe at USD 240.0 Million driven by ESG mandates; Asia-Pacific at USD 180.0 Million supported by automotive manufacturing expansion.

Consumer/End-User Trends: Tire manufacturers represent 60%+ adoption, with growing integration in sustainable plastics and coatings applications.

Pilot or Case Example: In 2024, a U.S.-based pyrolysis facility improved carbon recovery yield by 17% while cutting operational downtime by 12%.

Competitive Landscape: Leader holds approximately 18% share, followed by Pyrolyx AG, Orion Engineered Carbons, Birla Carbon, and Continental Carbon.

Regulatory & ESG Impact: EU Green Deal and U.S. EPA tire recycling mandates aim for 50%+ material recovery rates by 2030.

Investment & Funding Patterns: Over USD 420 Million invested globally in advanced pyrolysis plants between 2022–2025.

Innovation & Future Outlook: Integration of carbon capture with pyrolysis and digital traceability platforms is shaping next-generation sustainable carbon black supply chains.

Sustainable carbon black materials serve tires (approximately 65%), industrial rubber goods (15%), plastics and coatings (12%), and specialty applications (8%). Recent innovations include continuous-feed pyrolysis systems delivering 20% higher yield consistency and low-PAH carbon grades for premium tires. Stricter EU carbon footprint labeling and U.S. state-level recycling mandates are accelerating adoption. Asia-Pacific consumption is expanding with 12% annual growth in recycled tire processing capacity, supporting long-term supply resilience.

The Sustainable Carbon Black Materials Market holds strategic importance as industries transition toward decarbonized and circular manufacturing models. Automotive OEMs and tire manufacturers are integrating recovered carbon black into supply chains to reduce Scope 3 emissions and meet ESG targets. Advanced continuous pyrolysis technology delivers 20% higher carbon yield compared to traditional batch pyrolysis systems, while reducing energy consumption per ton by nearly 15%.

North America dominates in production volume due to established tire recycling ecosystems, while Europe leads in adoption intensity, with over 48% of major tire manufacturers integrating sustainable carbon black into premium product lines. By 2028, AI-enabled process automation is expected to cut operational downtime by 25% and improve feedstock conversion rates by 18%.

Firms are committing to ESG targets such as 40% recycled material incorporation by 2030 and 30% lifecycle emission reductions in tire manufacturing. In 2024, a U.S.-based sustainable materials facility achieved a 16% reduction in process emissions through integration of digital temperature optimization systems.

Strategically, long-term growth pathways include scaling decentralized pyrolysis plants, forming OEM–recycler partnerships, and integrating carbon capture modules to enhance environmental compliance. As regulatory mandates tighten and corporate sustainability commitments expand, the Sustainable Carbon Black Materials Market is positioned as a critical pillar of industrial resilience, regulatory compliance, and sustainable growth transformation.

The Sustainable Carbon Black Materials Market is shaped by rising environmental regulations, expanding automotive production, and increasing demand for circular material solutions. Growing volumes of end-of-life tires—exceeding 1 billion units globally each year—create significant feedstock availability for recovered carbon black production. Industrial sectors are prioritizing materials that reduce lifecycle emissions by 20–40%, accelerating adoption in rubber, plastics, and coatings manufacturing. Technological progress in continuous pyrolysis, automated sorting, and AI-driven process control is improving yield efficiency and quality consistency. Additionally, ESG disclosure requirements and green procurement frameworks are influencing supplier selection, making sustainable carbon black materials a strategic sourcing priority for multinational manufacturers.

Global regulatory initiatives promoting tire recycling and waste reduction are significantly expanding feedstock supply for sustainable carbon black production. Over 70% of developed economies have mandatory tire recovery programs, with recycling rates exceeding 80% in North America and parts of Europe. Tire manufacturers are incorporating 10–20% recovered carbon black content in selected product lines to meet sustainability targets. Corporate ESG commitments, including 30% recycled content goals by 2030, are further stimulating procurement demand. Technological improvements delivering 15–20% higher yield efficiency enhance commercial viability, encouraging large-scale industrial deployment.

Recovered carbon black often exhibits variability in particle size distribution and ash content compared to virgin carbon black. In high-performance tire manufacturing, even 2–3% variation in reinforcement properties can affect durability standards. Advanced purification systems add 10–15% to operational costs, limiting adoption among smaller processors. Additionally, limited standardization frameworks across regions create uncertainty in quality benchmarking. These constraints require significant capital investment in testing and post-processing infrastructure, slowing uniform global expansion.

Electric vehicle production is projected to exceed 40 million units annually by 2030, increasing demand for low-carbon materials in tire and component manufacturing. Sustainable carbon black reduces embedded emissions by up to 35% compared to conventional grades. OEM partnerships targeting 25% recycled material usage per vehicle are expanding procurement contracts. Emerging markets in Asia are increasing tire recycling capacity by over 12% annually, opening new production hubs and supply chain integration opportunities.

Establishing advanced continuous pyrolysis facilities requires investments exceeding USD 25–40 million per plant. Environmental compliance systems, including emission filtration and monitoring, add approximately 8–12% to total setup costs. Volatility in scrap tire collection logistics and energy prices can increase operational expenditure by 10–15%. Furthermore, certification processes for automotive-grade applications can take 12–24 months, delaying commercialization timelines and affecting return on investment.

30% Increase in Continuous Pyrolysis Installations: Continuous reactor systems now account for nearly 45% of newly commissioned facilities, improving material recovery rates by 20% and reducing processing time by 25% compared to batch systems. Industrial-scale plants report 15% lower energy consumption per ton processed, enhancing operational efficiency and environmental performance.

40% Growth in Sustainable Tire Integration Programs: Major tire manufacturers have expanded sustainable carbon black integration into 35–50% of premium tire portfolios. Pilot programs demonstrate 18% lifecycle emission reduction and 12% improvement in circular material utilization metrics. Adoption is particularly strong in Europe and North America.

22% Improvement in Digital Process Optimization: AI-driven temperature and feedstock control systems improve yield stability by 22% and reduce downtime by 17%. Automated quality monitoring reduces product rejection rates by 10%, enabling consistent industrial-grade output suitable for automotive standards.

Expansion of Closed-Loop Recycling Networks by 28%: Partnerships between recyclers and OEMs have increased by 28% since 2022, enabling traceable supply chains and 25% higher material circularity rates. Integrated logistics platforms cut transportation-related emissions by 14%, supporting ESG compliance and long-term sustainability targets.

The Sustainable Carbon Black Materials Market is segmented by type, application, and end-user, reflecting the diverse industrial utilization of recovered and low-emission carbon black grades. Product differentiation is largely based on feedstock origin, processing technology, and performance characteristics such as particle size distribution, ash content, and reinforcement strength. Applications are heavily concentrated in tire and rubber manufacturing, but increasing integration into plastics, coatings, and specialty materials is reshaping demand patterns. End-user segmentation highlights automotive OEMs, tire manufacturers, plastics processors, and industrial goods producers as core adopters. More than 65% of global recovered carbon black output is currently absorbed by automotive-linked industries, while specialty applications account for a growing double-digit utilization rate. Decision-makers are increasingly prioritizing consistent quality grades, traceability, and ESG-compliant sourcing frameworks when evaluating suppliers across all segments.

The Sustainable Carbon Black Materials Market is categorized into Recovered Carbon Black (rCB), Bio-based Carbon Black, and Low-Emission Specialty Carbon Black. Recovered Carbon Black currently accounts for approximately 68% of total adoption due to abundant end-of-life tire feedstock and established pyrolysis processing infrastructure. Bio-based Carbon Black holds nearly 18% adoption, primarily used in specialty plastics and eco-labeled consumer goods. Low-Emission Specialty Carbon Black contributes roughly 14%, serving niche high-performance coatings and conductive polymer applications.

Recovered Carbon Black leads because it offers up to 35% lower lifecycle emissions compared to conventional furnace black and can replace 10–20% of virgin carbon black in tire compounds without compromising mechanical performance. Bio-based Carbon Black is the fastest-growing segment, expanding at an estimated CAGR of 12.8%, driven by rising demand for renewable feedstock alternatives and corporate carbon neutrality commitments.

Tire manufacturing represents the dominant application, accounting for approximately 62% of total sustainable carbon black utilization due to its reinforcing properties and compatibility with rubber compounds. Industrial rubber goods follow with nearly 18% adoption, including belts, hoses, and seals. Plastics and masterbatch applications contribute around 12%, while coatings, inks, and specialty conductive materials collectively represent about 8%.

Tire applications currently account for 62% of demand, while industrial rubber goods hold 18%. However, plastics and specialty polymers are rising fastest, expected to exceed 20% share by 2033 as sustainable packaging and automotive lightweighting accelerate. Plastics applications are expanding at an estimated CAGR of 11.9%, supported by a 25% increase in recycled-content mandates across major economies.

In 2025, more than 41% of global tire manufacturers reported incorporating sustainable carbon black into at least one product line. Additionally, over 35% of automotive OEM suppliers are piloting low-carbon material integration programs.

Tire manufacturers constitute the leading end-user segment, accounting for approximately 58% of total market consumption, driven by sustainability commitments and regulatory pressure for recycled content integration. Automotive OEM component suppliers represent around 16%, while plastics and polymer manufacturers account for nearly 14%. Industrial equipment and specialty product manufacturers collectively contribute about 12%.

Tire manufacturers currently hold 58% of demand, while automotive component suppliers represent 16%. However, plastics manufacturers are the fastest-growing end-user segment, expanding at an estimated CAGR of 12.3% as consumer goods companies target 30–50% recycled material usage in packaging and molded components by 2030.

In 2025, nearly 44% of large manufacturing enterprises reported implementing ESG-based supplier selection frameworks that prioritize low-emission raw materials. Furthermore, 39% of automotive suppliers indicated pilot adoption of recovered carbon black in non-critical rubber components.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.1% between 2026 and 2033.

North America processed more than 300 million end-of-life tires annually, with over 80% recovery rates supporting sustainable carbon black feedstock stability. Europe held approximately 29% share in 2025, supported by material recovery rates exceeding 90% across several EU member states. Asia-Pacific accounted for nearly 23% of global demand, driven by automotive production surpassing 50 million vehicles annually across China, India, and Japan combined. South America represented about 6% of global consumption, while the Middle East & Africa contributed close to 4%, reflecting emerging but expanding recycling infrastructure. Industrial decarbonization mandates, 30–50% recycled content targets in tire production, and 20% improvements in pyrolysis efficiency are reshaping regional competitive positioning and capital investment flows.

North America holds approximately 38% of the global Sustainable Carbon Black Materials Market share, supported by mature tire recycling ecosystems and industrial-scale pyrolysis deployment. The tire manufacturing sector accounts for nearly 65% of regional demand, followed by industrial rubber goods at 17% and plastics at 11%. More than 80% of end-of-life tires are diverted from landfills, ensuring stable feedstock supply. Regulatory frameworks at state levels mandate scrap tire management programs, while federal sustainability initiatives encourage circular material integration in automotive supply chains. Technological advancements include AI-enabled reactor monitoring systems that improve carbon yield efficiency by 18% and reduce unplanned downtime by 15%. Companies such as Birla Carbon have expanded sustainable carbon solutions portfolios, incorporating recovered grades into premium tire compounds. Regional buyers, particularly automotive OEM suppliers, prioritize ESG-compliant materials, with nearly 44% of enterprises integrating recycled-content benchmarks into procurement strategies.

Europe represents approximately 29% of the Sustainable Carbon Black Materials Market, with Germany, the United Kingdom, and France leading consumption. The EU’s circular economy targets mandate material recovery rates above 90%, directly supporting recovered carbon black integration. Tire manufacturers account for around 60% of regional demand, while specialty plastics and coatings contribute 18%. Regulatory bodies emphasize carbon footprint labeling and extended producer responsibility (EPR) frameworks, prompting 35–45% recycled material incorporation targets by 2030. Emerging technologies such as continuous-feed pyrolysis and advanced post-treatment purification are improving reinforcement quality by 12–16%. Companies like Orion Engineered Carbons are advancing sustainable product lines aligned with EU decarbonization objectives. European enterprises demonstrate higher regulatory-driven adoption behavior, with 48% of manufacturers prioritizing certified low-emission materials in supplier selection processes.

Asia-Pacific accounts for nearly 23% of global market volume and ranks as the fastest-growing region. China, India, and Japan collectively produce over 50 million vehicles annually, creating substantial tire and rubber demand. China alone processes more than 14 million tons of scrap tires per year, supporting expanding pyrolysis capacity. Tire manufacturing represents 58% of regional consumption, while plastics and industrial components contribute 22%. Manufacturing modernization and automation adoption are improving yield rates by 15–20% in newly commissioned facilities. Innovation hubs in China and India are piloting decentralized recycling plants with digital monitoring platforms. Companies such as Pyrolyx AG have expanded operational collaborations in the region. Consumer and industrial demand is closely tied to rapid automotive growth and infrastructure expansion, with increasing focus on cost-effective sustainable materials.

South America accounts for approximately 6% of global demand, led by Brazil and Argentina. Brazil alone generates over 450,000 tons of scrap tires annually, supporting localized recycling operations. Tire and industrial rubber goods comprise nearly 70% of regional utilization. Infrastructure expansion and transportation sector modernization are increasing rubber component demand. Government-led waste management policies and import-export trade incentives are gradually strengthening circular material ecosystems. Energy sector developments and road infrastructure projects further stimulate rubber product usage. Regional enterprises emphasize cost-efficient recycled materials, with 32% of manufacturers exploring pilot integration programs. Local processing capacity expansions are improving supply stability and reducing reliance on imported virgin carbon black.

The Middle East & Africa region contributes approximately 4% of global market share, with the UAE and South Africa emerging as key markets. Industrial diversification strategies, particularly in construction and oil & gas, are increasing demand for reinforced rubber and specialty coatings. Scrap tire volumes in the GCC exceed 1 million tons annually, supporting feedstock availability. Technological modernization initiatives include automated pyrolysis pilot plants improving energy efficiency by 14%. Trade partnerships and sustainability-driven procurement policies are promoting circular material integration. Local enterprises are exploring joint ventures to establish regional recycling hubs. Consumer and industrial behavior reflects growing emphasis on regulatory compliance and cost-effective sustainable inputs across manufacturing sectors.

United States – 34% Market Share: Strong production capacity exceeding 150 kilotons annually and advanced tire recycling infrastructure support large-scale Sustainable Carbon Black Materials Market adoption.

Germany – 16% Market Share: Robust circular economy regulations and high automotive manufacturing output drive sustained integration of sustainable carbon black materials across tire and industrial applications.

The Sustainable Carbon Black Materials Market is moderately fragmented, with more than 40 active global and regional participants operating across recovered carbon black (rCB), bio-based carbon black, and low-emission specialty grades. The top five companies collectively account for approximately 46% of the total market share, indicating a competitive but innovation-driven landscape. Market leaders maintain vertically integrated operations, combining scrap tire sourcing, advanced pyrolysis processing, and downstream product customization to strengthen margin control and supply stability.

Strategic initiatives include capacity expansions of 20–35 kilotons annually per facility, long-term supply agreements with global tire OEMs, and multi-year R&D collaborations to improve ash reduction by 10–15%. Partnerships between recyclers and automotive manufacturers have increased by nearly 28% since 2022, reflecting heightened ESG alignment. Digital process optimization platforms are improving carbon yield consistency by up to 22%, becoming a key competitive differentiator.

Mergers and joint ventures are focused on geographic expansion into Asia-Pacific and Europe, where regulatory pressure is intensifying. Approximately 35% of leading players are investing in modular pyrolysis units to reduce capital intensity and accelerate deployment cycles. Competitive positioning is increasingly influenced by traceability systems, lifecycle carbon certification, and integration of carbon capture modules, reinforcing sustainability credentials as a core differentiator.

Pyrolyx AG

Black Bear Carbon B.V.

Delta-Energy Group, LLC

Enviro Systems AB

Klean Industries Inc.

Ecolomondo Corporation

Scandinavian Enviro Systems

Bolder Industries

SR2O Holdings, LLC

DVA Renewable Energy JSC

Radhe Group of Energy

Pyrum Innovations AG

Technological advancement remains central to competitiveness in the Sustainable Carbon Black Materials Market. Continuous pyrolysis reactors are replacing batch systems, increasing throughput efficiency by 20–25% and reducing processing time by nearly 30%. Modern systems achieve carbon recovery rates above 85%, compared to 65–70% in earlier-generation facilities. AI-enabled process monitoring tools optimize temperature stability within ±2°C variance, improving particle consistency and reducing rejection rates by 10–12%.

Advanced post-treatment technologies, including magnetic separation and air classification, lower ash content by up to 15%, enabling recovered carbon black to meet performance benchmarks required for tire tread and sidewall applications. Plasma-assisted pyrolysis is emerging as a next-generation solution, demonstrating 12–18% higher carbon purity in pilot deployments.

Digital traceability platforms using blockchain-based tracking allow manufacturers to certify recycled content percentages, supporting ESG disclosure compliance. Integration of carbon capture modules into pyrolysis facilities can reduce direct emissions by up to 20%. Modular plant design is gaining traction, cutting installation timelines by 25% and lowering upfront infrastructure requirements. Additionally, bio-based feedstock conversion technologies are enabling production of renewable carbon black grades with 30–40% lower lifecycle emissions compared to conventional furnace processes. These technological shifts are enhancing scalability, quality assurance, and regulatory alignment for global producers.

• In March 2025, Scandinavian Enviro Systems’ recovered carbon black was used by Swedish rubber and plastics manufacturer AnVa in the launch of a climate-neutral rubber compound called Climarub, enabling over 200 million sustainable rubber components for automotive applications and reducing CO₂ emissions by more than 2 million kilos. Source: www.envirosystems.se

• In 2025, Birla Carbon released its 2025 Sustainability Report titled “Connected to a Greener Future,” outlining its sustainability roadmap toward net-zero carbon emissions by 2050 and highlighting greater circularity via solutions like Continua™ Sustainable Carbonaceous Material. Source: www.birlacarbon.com

• In April 2025, Birla Carbon announced plans to showcase next-generation high-performance and sustainable carbon-based solutions at Chinaplas 2025, underlining innovation in engineering plastics, wires, cables, and sustainable material portfolios designed for durability and lower environmental impact. Source: www.birlacarbon.com

• In October 2025, Birla Carbon confirmed its participation at K 2025, the world’s leading trade fair for plastics and rubber, where it will present a suite of innovative and sustainable carbon materials (e.g., Conductex™, Continua™ SCM, hybrid carbon black–CNTs) designed to accelerate circularity and performance across multiple industries.

The Sustainable Carbon Black Materials Market Report provides a comprehensive evaluation of product categories including recovered carbon black, bio-based carbon black, and low-emission specialty grades. The scope covers applications across tire manufacturing, industrial rubber goods, plastics, coatings, inks, and conductive materials, collectively representing over 90% of global utilization. The report assesses feedstock availability exceeding 1 billion end-of-life tires generated annually worldwide and analyzes processing technologies achieving recovery efficiencies above 80%.

Geographically, the study spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating analysis of regional recycling rates ranging from 70% to 95%. The report evaluates technological developments such as continuous pyrolysis, plasma-enhanced carbon recovery, AI-enabled quality monitoring, and carbon capture integration.

Industry focus areas include regulatory frameworks mandating 30–50% recycled content in tire production, ESG-driven procurement policies adopted by over 40% of multinational manufacturers, and supply chain traceability innovations. Emerging segments such as decentralized modular recycling plants and renewable-feedstock-derived carbon black are also assessed. The report delivers actionable intelligence for stakeholders including tire OEMs, recyclers, plastics manufacturers, investors, and policymakers, enabling strategic planning aligned with circular economy objectives and industrial decarbonization targets.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 352.0 Million |

| Market Revenue (2033) | USD 774.0 Million |

| CAGR (2026–2033) | 10.35% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Birla Carbon; Orion Engineered Carbons; Continental Carbon Company; Pyrolyx AG; Black Bear Carbon B.V.; Delta-Energy Group, LLC; Enviro Systems AB; Klean Industries Inc.; Ecolomondo Corporation; Scandinavian Enviro Systems; Bolder Industries; SR2O Holdings, LLC; DVA Renewable Energy JSC; Radhe Group of Energy; Pyrum Innovations AG |

| Customization & Pricing | Available on Request (10% Customization Free) |